Quick Navigation

- Report Scope

- Key Takeaways

- Analyst’s View

- Key Statistics

- Regional Analysis

- By Component Type

- By Technology

- By Application

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Challenging Factors

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Scope

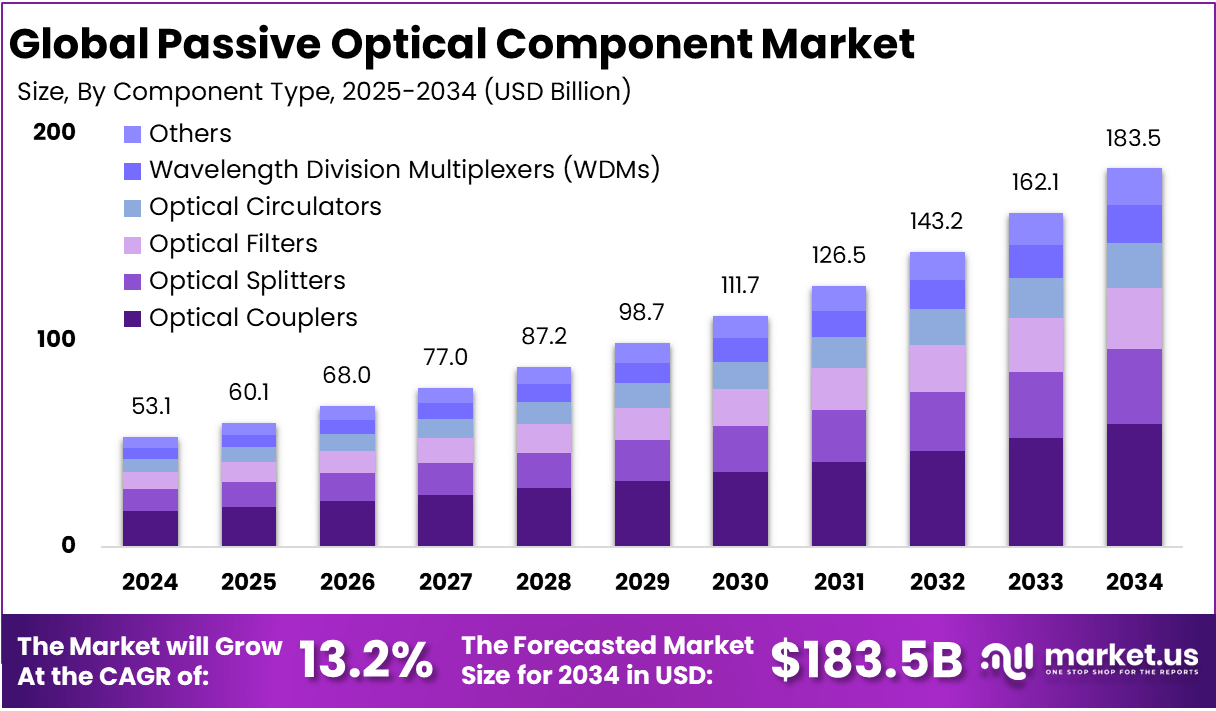

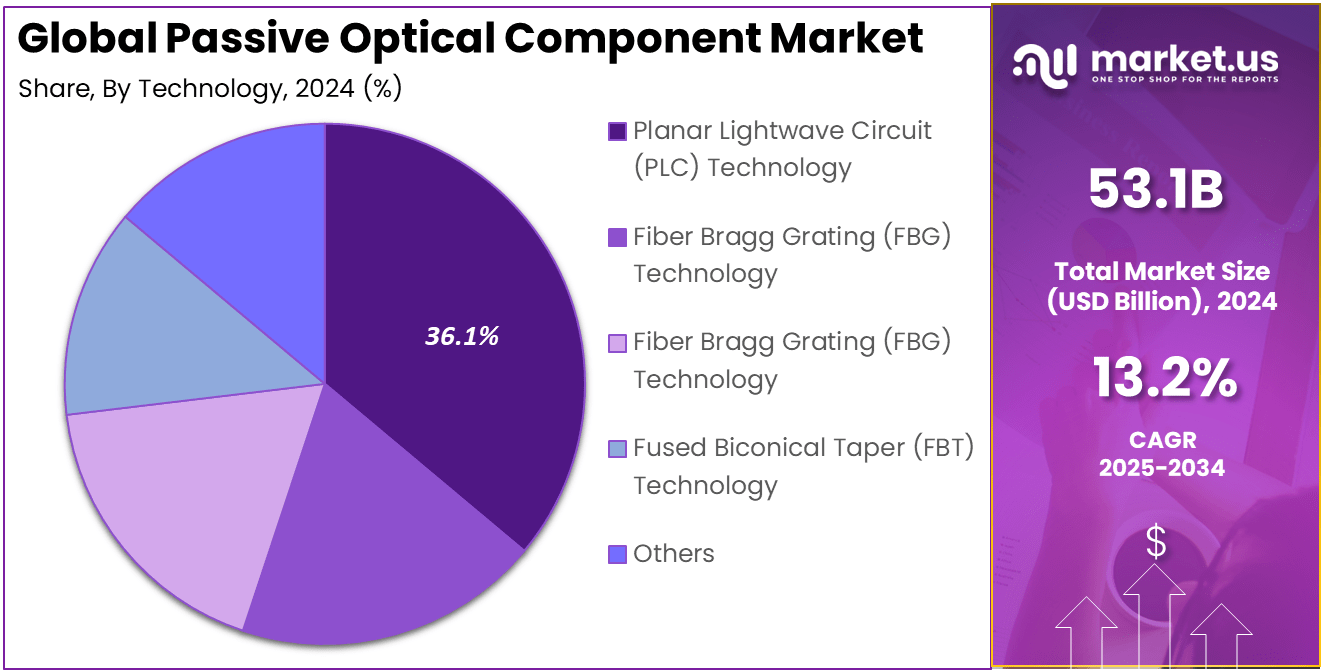

The Global Passive Optical Component Market is expected to be worth around USD 183.5 Billion By 2034, up from USD 53.1 Billion in 2024. It is expected to grow at a CAGR of 13.2% from 2025 to 2034.

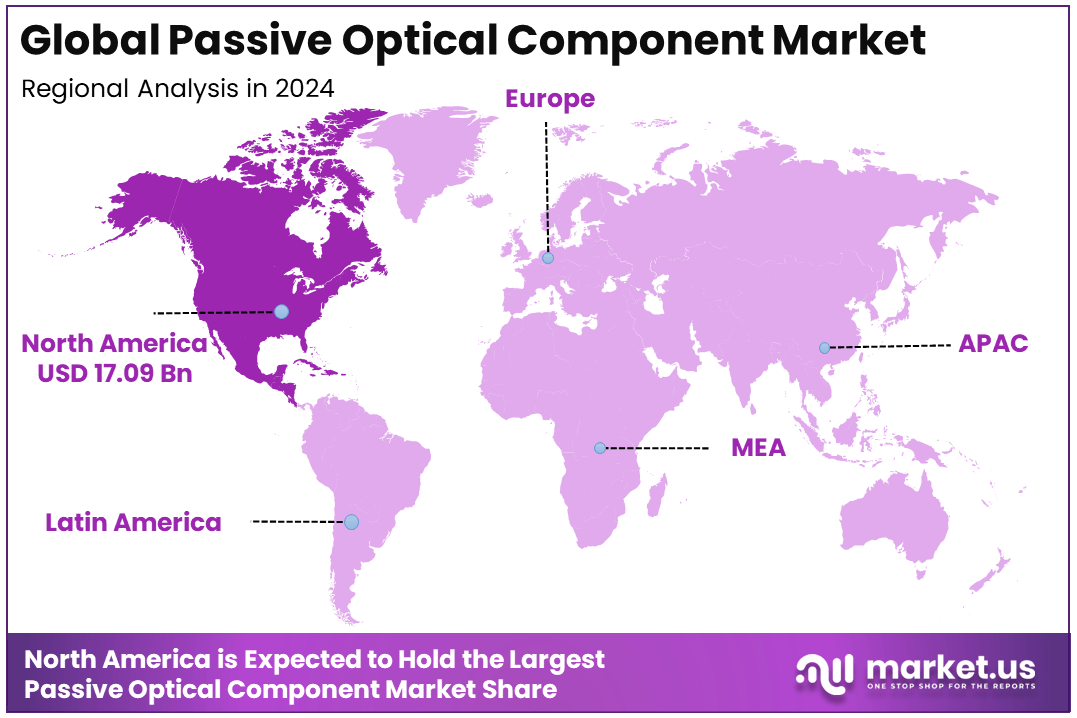

In 2024, North America held a dominant market position, capturing over a 32.2% share and earning USD 17.09 Billion in revenue. Further, the United States dominates the market by USD 14.9 Billion, steadily holding a strong position.

A Passive Optical Component (POC) is a device used in optical communication systems that does not require any electrical power. These components function by transmitting, reflecting, splitting, or redirecting optical signals without the need for active electrical circuits.

Common examples of passive optical components include optical fibers, optical splitters, couplers, and multiplexers. These components are essential in building and maintaining optical networks, particularly in applications like broadband internet, fiber-optic communication, and cable television. Their primary function is to manipulate light signals to ensure the efficient transmission of data over long distances.

The Passive Optical Component Market refers to the industry involved in the manufacturing, distribution, and application of these essential components in optical communication systems. The market has been experiencing significant growth due to the increasing demand for high-speed internet and the rapid expansion of fiber-optic networks globally.

The growth of technologies such as 5G, cloud computing, and IoT has further accelerated the need for efficient, high-performance optical components. The market is driven by the shift towards digitalization, the need for reliable communication systems, and the increasing penetration of fiber-to-the-home (FTTH) networks.

Key Takeaways

- Market Growth: The Passive Optical Component Market is projected to grow from USD 53.1 billion in 2024 to USD 183.5 billion by 2034, reflecting a CAGR of 13.2% during the forecast period.

- Dominant Component Type: Optical Couplers hold the largest market share, accounting for 32.4% in 2024, driven by their key role in splitting and combining optical signals in communication systems.

- Leading Technology: Planar Lightwave Circuit (PLC) Technology is the dominant technology in the market, capturing 36.1% of the market share, and offering significant benefits like miniaturization and high-performance optical signal processing.

- Key Application: Telecommunications remains the leading application for passive optical components, contributing 28.3% of the market share, driven by the growing demand for high-speed internet and the expansion of optical networks.

- Regional Insights: North America holds 32.2% of the global market share, with the U.S. contributing USD 14.9 billion in revenue, supported by the demand for advanced optical communication systems and fiber-optic network expansion.

Analyst’s View

Key driving factors in the Passive Optical Component Market include the increasing demand for high-bandwidth internet, the expansion of fiber-optic networks, and the rollout of 5G services. As the demand for faster and more reliable communication systems continues to rise, so does the need for efficient optical components. Additionally, governments worldwide are investing in infrastructure development, particularly in fiber-optic networks, which further boosts the demand for passive optical components.

The growing adoption of FTTH and FTTx (fiber-to-the-X) technologies presents significant opportunities for the Passive Optical Component Market. These technologies require a large number of optical components, such as splitters, filters, and connectors, to ensure the delivery of high-speed internet to homes and businesses.

Moreover, the rising demand for 5G networks, which require advanced optical networks for backhaul connections, is another key growth opportunity. Additionally, industries like data centers and cloud service providers require optical components to manage large amounts of data efficiently.

Technological advancements in optical communication, such as the development of Wavelength Division Multiplexing (WDM), have led to improved efficiency and capacity in optical networks, which has directly impacted the demand for passive optical components. Furthermore, innovations like low-loss optical fibers and advanced optical splitters are enabling better performance in long-distance transmission.

The integration of smart technologies into passive optical components also promises enhanced reliability and scalability, making them even more essential for the next-generation telecommunication infrastructure. As these technologies continue to evolve, the market for passive optical components will likely see sustained growth.

Key Statistics

User and Application Statistics

- Internet Users: As of 2023, there are around 5.07 billion internet users globally, which is expected to drive demand for passive optical components as more users require high-speed internet access.

- Broadband Subscriptions: The number of fixed broadband subscriptions worldwide reached approximately 1.2 billion in 2023, indicating a growing market for passive optical components used in these networks.

Component Breakdown

- Optical Fiber Segment: The optical fiber segment is expected to hold a market share of about 40% in the passive optical component market by 2025.

- Optical Splitters: The optical splitter segment is projected to grow at a CAGR of approximately 14% from 2024 to 2030, reflecting increasing demand in fiber-to-the-home (FTTH) applications.

Import and Export Data

- Global Trade Values: In 2022, the global trade value for passive optical components was estimated at around USD 15 billion, with exports accounting for approximately 60% of this value.

- Major Exporters: Countries like China, the USA, and Germany are among the top exporters, with China alone accounting for about 30% of global exports in this sector.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than 32.2% of the global share in the Passive Optical Component Market, with USD 17.09 billion in revenue. This leadership can be attributed to the region’s advanced infrastructure and the high adoption rate of next-generation telecommunications and optical communication technologies.

The demand for fiber-optic networks, especially with the rollout of 5G services and fiber-to-the-home (FTTH) initiatives, has led to a substantial rise in the need for passive optical components like optical couplers and planar lightwave circuits (PLC), which are essential for high-speed data transfer and network optimization.

Furthermore, the United States dominates the market in North America, contributing USD 14.9 billion in revenue. This significant market share is driven by the continuous investments in telecommunication infrastructure, especially in urban and suburban areas, and the strong presence of key players like Cisco and Juniper Networks, which foster innovation in optical network technologies. The U.S. also benefits from substantial government initiatives aimed at improving broadband connectivity across the country.

North America’s dominance is also fueled by high demand from enterprise-level users, where industries such as BFSI, IT, and media rely heavily on advanced optical technologies for seamless communication and large-scale data processing. With increasing reliance on cloud computing and high-speed networks, the region is poised to continue leading the global market for passive optical components.

By Component Type

In 2024, the Optical Couplers segment held a dominant market position, capturing more than a 32.4% share in the Passive Optical Component Market. This leadership is primarily driven by the critical role optical couplers play in fiber-optic communication systems.

Optical couplers are essential for splitting or combining light signals in optical networks, which makes them integral to high-speed data transfer and signal management. As demand for high-bandwidth networks grows, especially with the expansion of 5G, fiber-to-the-home (FTTH), and cloud-based applications, the need for optical couplers has surged.

Furthermore, the ability of optical couplers to efficiently manage signal distribution in telecommunications, data centers, and enterprise networks has solidified their market dominance. They offer low signal loss and high reliability, making them the preferred choice for optical network infrastructure.

The increasing demand for secure, fast, and reliable communication systems is driving further adoption of optical couplers in both consumer and business applications. With advancements in fiber-optic technology and the growing emphasis on scalable and efficient network solutions, the optical coupler segment is expected to maintain its dominant position throughout the forecast period.

By Technology

In 2024, the Planar Lightwave Circuit (PLC) Technology segment held a dominant market position, capturing more than a 36.1% share of the Passive Optical Component Market. PLC technology is widely recognized for its superior ability to integrate multiple optical functions onto a single chip, making it an essential component in the development of advanced optical networks. The technology is crucial for high-performance systems in applications such as Wavelength Division Multiplexing (WDM), fiber-optic communications, and data center management.

PLC’s advantage lies in its ability to handle multiple optical signals with minimal loss, providing high reliability and scalability. As demand for faster, more efficient optical networks continues to grow—especially with the rise of 5G networks, FTTH services, and cloud-based infrastructures—PLC technology is seen as the ideal solution for ensuring seamless data transmission and low-cost, high-volume production.

Moreover, PLC technology supports compact designs and integration with other optical components, further increasing its popularity in modern communication systems. This technology’s widespread use in telecommunications, data centers, and enterprise networks solidifies its leading position in the market and ensures its continued growth over the forecast period.

By Application

In 2024, the Telecommunications segment held a dominant market position, capturing more than a 28.3% share of the Passive Optical Component Market. The dominance of the telecommunications segment can be attributed to the rapid expansion of fiber-optic networks and the growing demand for high-speed data transmission. As the world transitions to 5G networks, there is an increasing need for high-capacity, reliable optical components to support the growing volume of data traffic and improve network performance.

Telecommunications companies heavily rely on passive optical components like optical splitters, couplers, and filters to optimize their network infrastructure, enabling them to provide fast and reliable internet services. Additionally, the demand for fiber-to-the-home (FTTH) and fiber-optic broadband services, driven by the need for faster internet connections, further boosts the telecommunications market.

With a surge in demand for video streaming, cloud computing, and smart devices, the need for efficient and scalable optical networks continues to grow. This trend positions the telecommunications industry as a major driver of the Passive Optical Component Market, ensuring its continued dominance throughout the forecast period.

Key Market Segments

By Component Type

- Optical Couplers

- Optical Splitters

- Optical Filters

- Optical Circulators

- Wavelength Division Multiplexers (WDMs)

- Others

By Technology

- Planar Lightwave Circuit (PLC) Technology

- Fiber Bragg Grating (FBG) Technology

- Thin film technology

- Fused Biconical Taper (FBT) Technology

- Others

By Application

- Telecommunications

- Data Centers

- Cable Television (CATV)

- Fiber to the Home (FTTH)

- Enterprise Networks

- Industrial Networking

- Others

Driving Factors

Increasing Demand for High-Speed Internet and 5G Networks

The growing demand for high-speed internet services, coupled with the rapid roll-out of 5G networks, is a key driving factor for the Passive Optical Component Market. As more businesses and consumers rely on internet connectivity for streaming, cloud computing, gaming, and remote work, the need for robust, high-capacity networks becomes critical. Passive optical components such as optical couplers, splitters, and filters play a crucial role in supporting these infrastructure requirements by enabling faster and more reliable data transmission.

The advent of 5G technology further accelerates the demand for fiber-optic networks, as 5G requires high bandwidth, low latency, and high-speed communication. With telecom companies increasingly investing in fiber-to-the-home (FTTH) and fiber-optic broadband to offer faster internet, passive optical components are integral in optimizing network efficiency and performance.

This trend is expected to continue as global internet usage rises, especially in emerging markets where the need for modern, high-speed connectivity is rapidly increasing. With telecommunication infrastructure being a central pillar for economic development, this demand will continue to drive the market for passive optical components well into the future.

Restraining Factors

High Installation and Maintenance Costs

A significant restraint for the Passive Optical Component Market is the high installation and maintenance costs associated with deploying fiber-optic networks. While optical components offer substantial performance benefits, the initial cost of fiber-optic cable installation, coupled with the need for specialized equipment and expertise, can be prohibitively expensive, particularly in emerging markets.

For telecommunications providers and network operators, the cost of upgrading existing infrastructure to accommodate advanced optical technologies can be a significant barrier. This is especially true for remote or underserved regions, where the required investment in laying fiber-optic cables and establishing related infrastructure may not be financially viable. The complexity of maintenance and repair of optical networks also contributes to ongoing operational costs, which can deter smaller players from entering the market.

Moreover, some regions still lack the necessary regulatory frameworks and incentives to encourage large-scale investments in fiber-optic infrastructure, slowing down the widespread adoption of passive optical components. While demand for faster, more reliable connectivity continues to grow, these financial and logistical challenges may limit the overall growth of the market in certain regions.

Growth Opportunities

Expansion of Fiber-to-the-Home (FTTH) Networks

One of the most promising growth opportunities for the Passive Optical Component Market lies in the global expansion of fiber-to-the-home (FTTH) networks. With the increasing demand for high-speed internet and seamless connectivity, more countries are investing in fiber-optic infrastructure to offer broadband directly to consumers’ homes.

FTTH networks provide faster, more reliable internet compared to traditional copper-based connections, making them ideal for modern-day internet usage, such as video conferencing, streaming, and smart-home applications.

In developing markets, the push for digital inclusion and government initiatives aimed at expanding broadband access further propels the demand for FTTH deployments. Passive optical components, including optical splitters, couplers, and filters, are essential in establishing these high-performance networks.

Telecom operators in both mature and emerging markets are ramping up efforts to deploy FTTH technology to support increased data traffic, particularly as the demand for internet services grows amid digital transformations across industries.

Challenging Factors

Technological Complexity and Standardization Issues

A notable challenge faced by the Passive Optical Component Market is the technological complexity associated with developing and implementing cutting-edge optical solutions. While passive optical components offer numerous advantages in terms of efficiency and performance, the technology required to manufacture and integrate these components can be complex, particularly when combined with other advanced technologies such as 5G networks and smart devices.

Another challenge is the lack of standardization in optical components. As the market is still evolving, various manufacturers may offer slightly different technologies and designs, which can create interoperability issues.

The absence of a universal standard across the industry makes it difficult for network operators to seamlessly integrate new optical components into existing infrastructures, potentially slowing down adoption rates. Furthermore, technological advancements in optical fibers and signal transmission require continuous innovation, meaning companies need to invest heavily in research and development to stay competitive.

Growth Factors

Expanding Demand for High-Speed Connectivity

The growth of the Passive Optical Component Market is largely driven by the increasing demand for high-speed internet and the global roll-out of 5G networks. As more businesses and consumers require faster and more reliable connections for activities like streaming, remote work, and e-commerce, the need for fiber-optic infrastructure has soared.

According to recent data, the global demand for fiber-optic broadband is expected to rise significantly, with global fiber-optic deployments estimated to grow by over 13% annually. In particular, 5G networks, which require high-capacity backhaul connections, are helping to fuel the adoption of passive optical components like splitters, couplers, and multiplexers.

With 5G expected to cover more than 50% of the global population by 2025, the market for passive optical components will continue to experience rapid growth, as these components are critical for enabling the required data speeds and reliability.

Emerging Trends

Integration with IoT and Smart Cities

As smart city and Internet of Things (IoT) technologies continue to gain traction, there is an increasing demand for high-bandwidth and low-latency data transmission, which is pushing the adoption of passive optical components. In particular, fiber-to-the-home (FTTH) networks are growing at an exceptional rate due to their ability to deliver high-speed internet to consumers and businesses.

This trend is expected to accelerate as smart homes and connected devices require fast, secure, and uninterrupted connectivity. According to reports, the FTTH market is expected to grow at a CAGR of 13.2% through the next decade, with substantial investments in optical network deployments worldwide. Passive optical components such as optical filters and multiplexers are being increasingly used in these applications, helping to optimize data transmission and reduce network congestion.

Business Benefits

Cost-Effectiveness and Scalability

For businesses, passive optical components offer significant benefits in terms of cost-effectiveness and scalability. Unlike active components, passive optical components do not require external power, which reduces both operational costs and system complexity. Furthermore, optical fiber networks are scalable, meaning that businesses can expand their networks to accommodate growing bandwidth demands without significant additional costs.

This scalability is particularly attractive to telecom providers and large enterprises that need to future-proof their networks. The global telecom market is predicted to grow at a CAGR of 5.5%, and as telecom companies expand their fiber-optic infrastructure, the demand for passive optical components is likely to increase substantially.

Additionally, passive optical networks (PONs) offer enhanced network reliability and signal strength, reducing downtime and improving overall service quality for end-users, which translates into improved customer satisfaction and loyalty for businesses.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

NEC Corporation, a key player in the Passive Optical Component Market, has been actively involved in expanding its presence through strategic acquisitions and partnerships. Recently, NEC acquired KMW Inc., a leader in telecommunications equipment. This acquisition enables NEC to enhance its product portfolio, particularly in the domain of fiber-optic network solutions and optical components.

Fujitsu Limited, another major player in the passive optical component space, has focused heavily on research and development to strengthen its market position. The company recently launched a new line of Planar Lightwave Circuit (PLC) components, designed to enhance the performance of fiber-optic networks. Fujitsu’s strategic partnerships with global telecom giants have positioned them as a key supplier in FTTH and 5G deployments.

Furukawa Electric Co., Ltd. has been a significant player in the optical fiber and passive optical component markets. The company has focused on advancing fiber-optic technologies, including the development of optical circulators and multiplexers. Furukawa has also made several key acquisitions and strategic alliances, particularly with telecom operators and manufacturers to bolster its position in the global market.

Top Key Players in the Market

- NEC Corporation

- Fujitsu Limited

- Furukawa Electric Co., Ltd.

- Huber+Suhner AG

- Broadcom Inc.

- Nokia Corporation

- Cisco Systems, Inc.

- Ciena Corporation

- II-VI Incorporated

- Huawei Technologies Co., Ltd.

- Lumentum Holdings Inc.

- Molex LLC

- Other Major Players

Recent Developments

- In 2024, Furukawa Electric Co., Ltd. launched a new series of optical circulators designed for 5G and data center applications.

- In 2024, NEC Corporation expanded its product line with the introduction of next-generation optical couplers and splitters.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 53.1 Billion |

| Forecast Revenue (2034) | USD 183.5 Billion |

| CAGR (2025-2034) | 13.2% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component Type (Optical Couplers, Optical Splitters, Optical Filters, Optical Circulators, Wavelength Division Multiplexers (WDMs), Others), By Technology (Planar Lightwave Circuit (PLC) Technology, Fiber Bragg Grating (FBG) Technology, Thin film technology, Fused Biconical Taper (FBT) Technology, Others), By Application (Telecommunications, Data Centers, Cable Television (CATV), Fiber to the Home (FTTH), Enterprise Networks, Industrial Networking, Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | NEC Corporation, Fujitsu Limited, Furukawa Electric Co., Ltd., Huber+Suhner AG, Broadcom Inc., Nokia Corporation, Cisco Systems, Inc., Ciena Corporation, II-VI Incorporated, Huawei Technologies Co., Ltd., Lumentum Holdings Inc., Molex LLC, Other Major Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |