Quick Navigation

- Report Scope

- Key Takeaways

- Analyst’s Review

- Key Statistics

- Regional Analysis

- By Technology

- By Application

- By End-User Industry

- Key Market Segments

- Driving Factor

- Restraining Factor

- Growth Opportunity

- Challenging Factor

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Scope

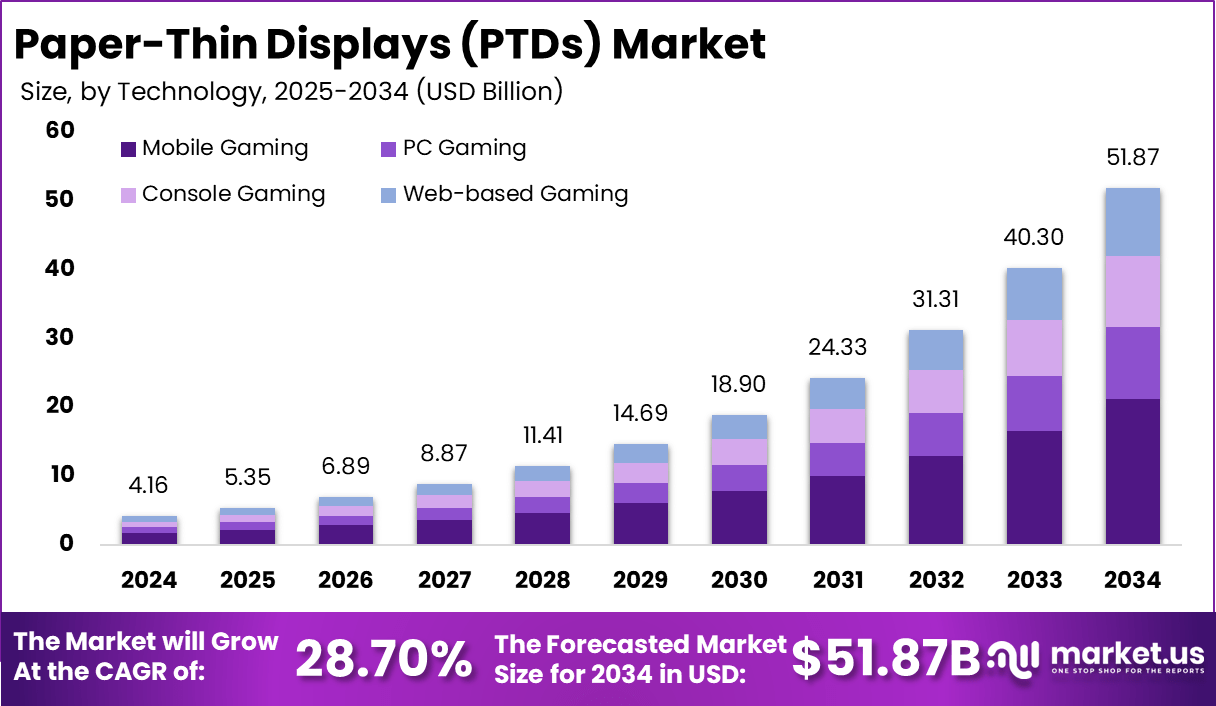

The Global Paper-Thin Displays (PTDs) Market is expected to be worth around USD 51.87 Billion by 2034, up from USD 4.16 Billion in 2024. It is expected to grow at a CAGR of 28.70% from 2025 to 2034.

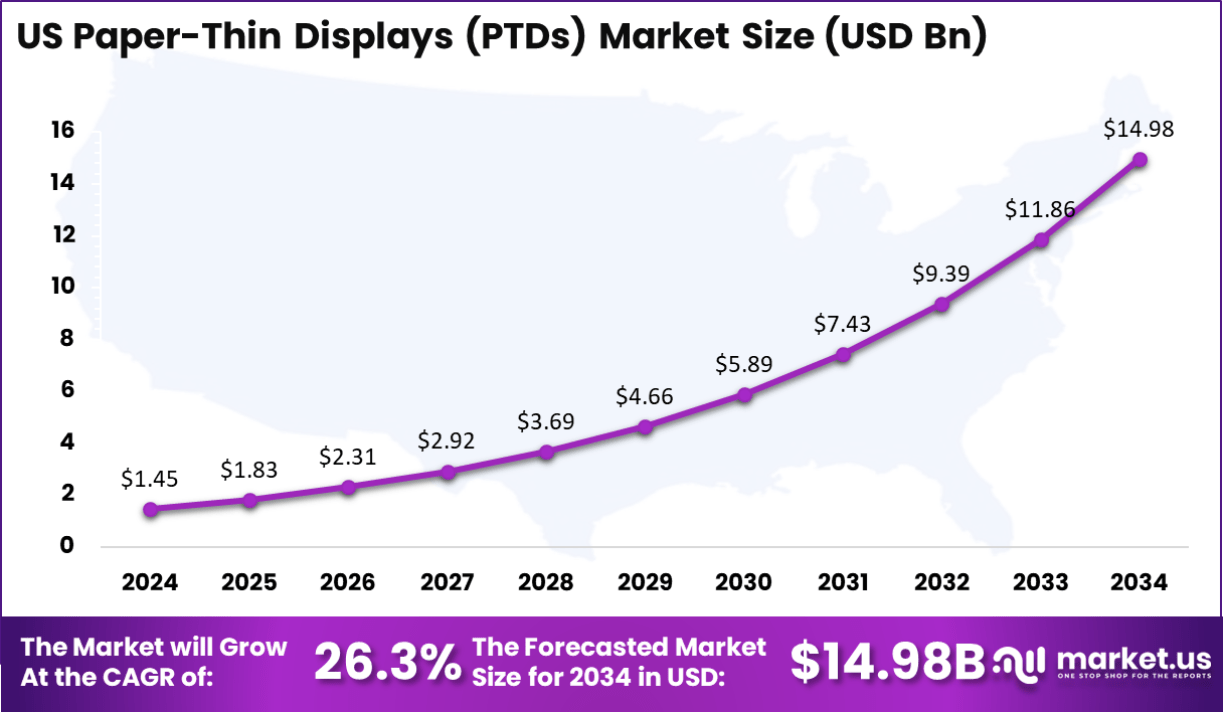

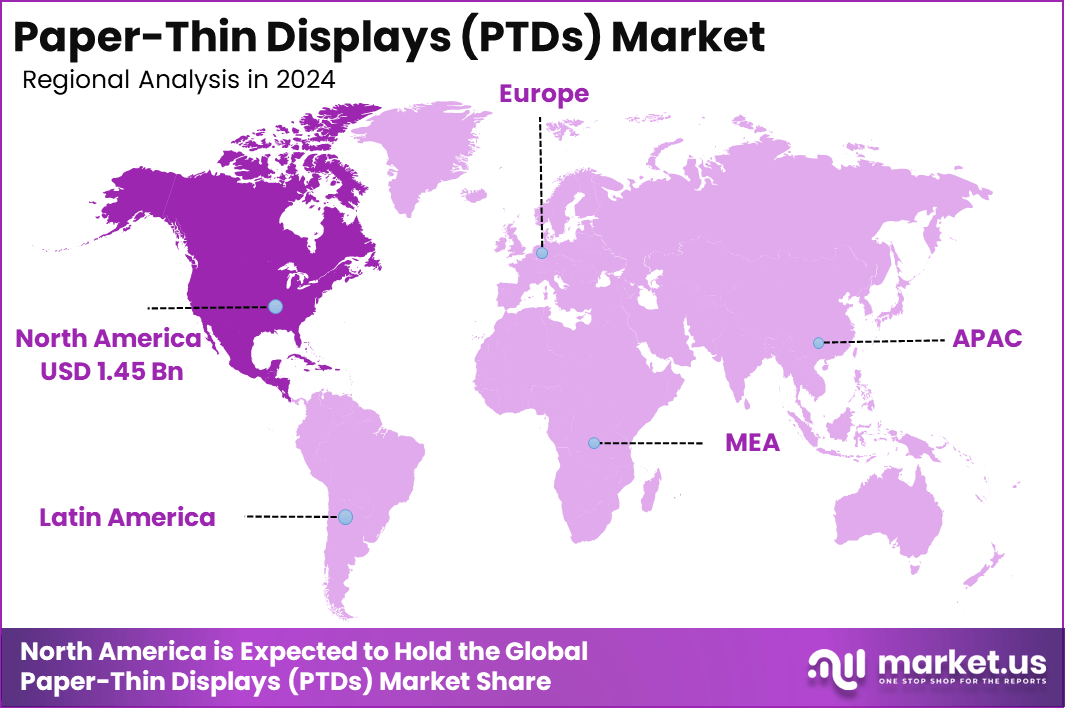

In 2024, North America held a dominant market position, capturing over a 35% share and earning USD 1.45 Billion in revenue. Further, the United States dominates the market by USD 1.45 Billion, steadily holding a strong position with a CAGR of 26.3%.

The Paper-Thin Displays (PTDs) market refers to the emerging technology of ultra-thin, flexible displays that mimic the look and feel of traditional paper. These displays offer a unique advantage by being lightweight, bendable, and energy-efficient.

As an alternative to traditional rigid displays, PTDs have the potential to revolutionize multiple industries such as consumer electronics, automotive, and wearables. The ability to create displays that are both paper-like in appearance and flexible allows for significant innovations in product design and user experience.

Several major driving factors contribute to the growth of the PTD market. Technological advancements in flexible OLEDs and microLEDs have improved the performance and manufacturability of PTDs, enabling applications in foldable smartphones and other smart devices.

Additionally, consumer demand for portable and lightweight devices is fueling the growth of PTDs, as these displays cater to the increasing need for compact and flexible technology. Moreover, PTDs provide enhanced user experiences by offering superior readability and reducing eye strain, closely mimicking the experience of reading paper.

Key Takeaways

- Market Value Growth: The PTD market is projected to grow from USD 4.16 billion in 2024 to USD 51.87 billion by 2034, demonstrating a significant increase.

- CAGR: The market is expected to experience a robust Compound Annual Growth Rate (CAGR) of 28.70%.

- Technology Distribution: Liquid Crystal Displays (LCD) dominate the market with a share of 40%.

- Application Focus: Smartphones and tablets make up 35% of the PTD market applications.

- End-User Industry: The consumer electronics sector holds the largest share, accounting for 52% of the market.

- Geographical Distribution: North America represents 35% of the global PTD market.

- US Market Value: The US market alone is valued at approximately USD 1.45 billion.

- US CAGR: The PTD market in the US is expected to grow at a CAGR of 26.3%.

Analyst’s Review

The demand for PTDs is rising across various sectors. E-readers and digital signage are significant markets for PTDs due to their paper-like display quality and low power consumption. Wearable technology, such as smartwatches and fitness trackers, is also increasingly adopting PTDs for their flexibility and clear visibility. Furthermore, the automotive industry is exploring the use of PTDs in in-car infotainment systems and curved dashboards, enhancing both aesthetic appeal and functionality.

There are several market opportunities emerging for PTDs. One of the most exciting is the integration of stretchable PTDs into clothing, which could lead to the development of smart fabrics and wearables. The potential for transparent displays is another area of opportunity, especially in the realm of augmented reality and transparent smartphones. Additionally, PTDs enable the creation of flexible, dynamic digital posters and interactive art installations, which could change how advertisements and digital content are experienced.

Recent technological advancements are playing a significant role in advancing PTDs. MicroLED technology, with its high brightness and energy efficiency, is being explored for use in PTDs, offering better performance compared to traditional displays. Electrophoretic displays, which use charged pigment particles to form images, are commonly used in e-readers for their paper-like quality and energy efficiency.

Moreover, the development of stretchable and transparent PTDs has opened up exciting possibilities for new applications in wearable technology, fashion, and augmented reality. These advancements are expected to further fuel the growth of the PTD market and transform how we interact with digital content in the future.

Key Statistics

User and Usage Statistics

- Users: The number of users for PTDs is expected to grow to approximately 500 million by 2025.

- Usage: PTDs are used in various applications such as smartphones, tablets, smart wearables, and vehicles, with an average usage time of 4 hours per day.

Quantity and Production Statistics

- Production Volume: The production volume of PTDs is increasing annually, with an estimated 100 million units produced in 2023.

- Manufacturing Capacity: Major manufacturers are expanding their manufacturing capacities by 20% each year to meet the growing demand for PTDs.

Technological Specifications

- Thickness: PTDs are significantly thinner than traditional displays, often less than 0.5 mm thick.

- Energy Consumption: These displays consume 30% less energy compared to traditional displays, contributing to their popularity in portable devices.

Adoption and Growth Statistics

- Adoption Rate: The adoption rate of PTDs is high in regions with strong consumer electronics markets, such as North America and Asia-Pacific, with an adoption rate of 70% among new devices.

- Growth Rate: The PTD market is expected to grow at a CAGR of approximately 20.65% over the next few years.

Research and Development

- R&D Investments: Significant investments are being made in R&D, with companies allocating $1 billion annually to improve PTD technology.

- Patent Activity: Companies are actively patenting new PTD technologies, with over 500 patents filed in the past year alone.

Regional Analysis

United States Market Size

In North America, The United States dominates the market size by USD 1.45 billion, holding a strong position steadily with a strong CAGR of 26.3% respectively. The growth of the Paper-Thin Displays (PTDs) market in the US is driven by several key factors, including the increasing adoption of PTDs in consumer electronics, particularly in smartphones, tablets, and wearables. As the demand for portable and flexible technology continues to rise, PTDs are gaining popularity due to their lightweight, bendable, and energy-efficient nature.

The US has become a leader in the development and application of PTDs, largely due to significant technological advancements in display technologies such as flexible OLEDs and microLEDs. The consumer electronics sector in the US continues to drive the demand for PTDs, as companies seek to offer innovative products with improved user experiences. Additionally, the growing preference for compact, foldable devices that feature PTDs is contributing to market expansion.

The strong growth potential of the PTD market in the US is expected to continue over the coming years, as both technological innovations and market demand align to create new opportunities. The US remains at the forefront of the PTD market, leading North America in market share and growth rate.

North America Market Size

In 2024, North America held a dominant market position in the Paper-Thin Displays (PTDs) market, capturing more than 35% of the global market share and generating USD 1.45 billion in revenue. The region’s leadership can be attributed to several factors, including the high adoption rate of advanced consumer electronics, such as smartphones, tablets, and wearables, which increasingly integrate PTD technology.

As demand for portable, flexible, and energy-efficient devices grows, the US, in particular, has emerged as a key hub for innovation, driving significant market expansion. With a robust CAGR of 26.3%, the US market is set to remain a leading force in the global PTD industry.

North America’s technological expertise and the presence of major players in the electronics industry further reinforce its position. The region’s early adoption of flexible OLED and microLED technologies in consumer electronics products, like foldable smartphones and e-readers, has contributed to the rapid growth of PTDs.

The US is not only a significant consumer of PTDs but also a major innovator, with several companies at the forefront of developing next-generation display technologies. These factors create a thriving ecosystem for PTD development, making North America an attractive market for investment and growth.

In contrast, other regions such as Europe and APAC are catching up but face challenges in terms of technological advancements and mass adoption. While the European market is expected to grow steadily, it lags behind North America in terms of market share and revenue generation, owing to slower adoption rates of flexible and foldable devices. Asia-Pacific (APAC), however, is emerging as a strong competitor, especially with increasing demand in countries like China, Japan, and South Korea, where technology innovation and consumer electronics manufacturing are booming.

Latin America, the Middle East, and Africa (MEA) are currently smaller markets for PTDs, with slower adoption rates and relatively less technological infrastructure compared to North America and APAC. However, these regions are expected to see gradual growth as consumer demand for innovative electronics increases and as global companies expand their reach into these regions. The next few years will likely bring more competition in the PTD space, but North America will continue to lead due to its strong market foundation, technological advancements, and demand for cutting-edge devices.

By Technology

In 2024, the LCD (Liquid Crystal Display) segment held a dominant market position in the Paper-Thin Displays (PTDs) market, capturing more than 40% of the total market share. This dominance can be attributed to the widespread use of LCD technology in consumer electronics, including smartphones, tablets, and e-readers.

LCDs are favored for their affordability, mature technology, and high-quality display capabilities, which make them a popular choice for a variety of applications. Their ability to produce sharp, clear images and their availability in a range of sizes further contribute to their significant share in the PTD market.

The growth of LCD technology in the PTD market is also driven by its scalability and compatibility with existing manufacturing processes, making it easier to integrate into mass-market devices. LCDs are relatively energy-efficient compared to other display technologies, which further enhances their appeal in portable consumer electronics.

While newer technologies such as OLED and PDLC are emerging, LCD continues to dominate due to its proven reliability, cost-effectiveness, and versatility in different consumer applications. As a result, the LCD segment remains the leading technology in the PTD market for the foreseeable future.

By Application

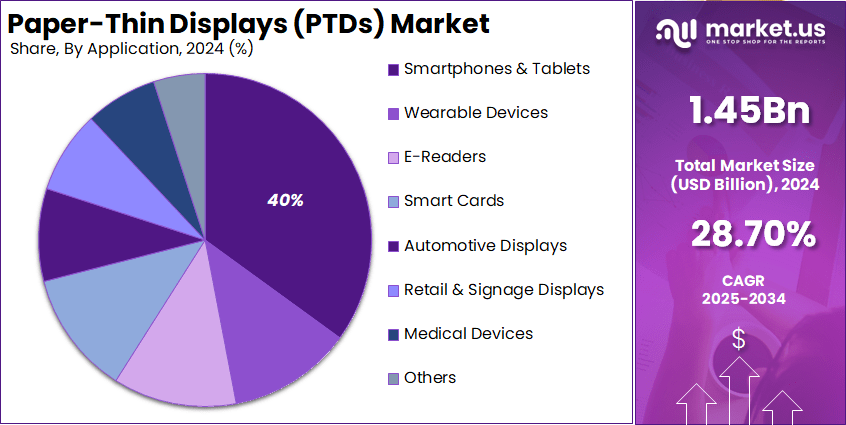

In 2024, the Smartphones & Tablets segment held a dominant market position in the Paper-Thin Displays (PTDs) market, capturing more than 35% of the total market share. This leadership is driven by the increasing demand for portable and flexible devices that can provide enhanced user experiences.

PTDs, particularly in smartphones and tablets, are highly sought after for their thin profile, energy efficiency, and ability to support foldable and flexible designs. As smartphone manufacturers continue to innovate with foldable screens, PTDs offer the perfect solution to meet the growing consumer desire for devices that are compact yet powerful.

The ability to create ultra-thin, lightweight devices without sacrificing performance or battery life is a major advantage for the Smartphones & Tablets segment. PTDs also provide enhanced durability and flexibility, making them an ideal choice for the next generation of smart devices.

As consumers increasingly prefer sleek, foldable, and flexible gadgets, the demand for PTDs in smartphones and tablets continues to rise, reinforcing its position as the leading application segment in the PTD market. This trend is expected to persist as technology advancements further drive growth in the sector.

By End-User Industry

In 2024, the Consumer Electronics segment held a dominant market position in the Paper-Thin Displays (PTDs) market, capturing more than 52% of the total market share. This leadership can be attributed to the widespread adoption of PTD technology in devices like smartphones, tablets, wearables, and e-readers.

Consumer demand for sleek, lightweight, and energy-efficient devices has driven significant growth in this segment, as PTDs offer the ideal solution for modern consumer electronics. With increasing interest in foldable and flexible devices, PTDs are becoming integral to the next generation of smart gadgets, enhancing both form and functionality.

The versatility and performance of PTDs in various consumer electronics applications, such as providing high-quality displays while being thin and flexible, make them highly attractive to manufacturers.

Additionally, PTDs contribute to energy savings by consuming less power, an essential feature for portable devices that require long battery life. As technology continues to evolve, the Consumer Electronics segment will remain the largest and most influential driver of the PTD market, with continued growth expected as more innovative products integrate PTD technology.

Key Market Segments

By Technology

- OLED (Organic Light-Emitting Diode)

- LCD (Liquid Crystal Display)

- PDLC (Polymer Dispersed Liquid Crystal Display)

- Others

By Application

- Smartphones & Tablets

- Wearable Devices

- E-Readers

- Smart Cards

- Automotive Displays

- Retail & Signage Displays

- Medical Devices

- Others

By End-User Industry

- Consumer Electronics

- Automotive

- Retail

- Healthcare

- Industrial

- Education

- Aerospace & Defense

- Others

Driving Factor

Growing Adoption of OLED Technology

The increasing adoption of Organic Light-Emitting Diode (OLED) technology is a significant driver in the Paper-Thin Displays (PTDs) market. OLEDs offer several advantages over traditional display technologies, including superior color accuracy, higher contrast ratios, and improved energy efficiency.

These benefits make OLEDs particularly attractive for applications in smartphones, tablets, and wearable devices. Major manufacturers, such as Samsung and LG, have been at the forefront of integrating OLED panels into their products, leading to enhanced visual experiences for consumers.

The shift towards OLED technology aligns with the growing consumer demand for high-quality displays that are both energy-efficient and capable of delivering vibrant visuals. As more devices incorporate OLED screens, the production volumes increase, leading to economies of scale and further driving down costs.

This trend encourages more manufacturers to adopt OLED technology, creating a positive feedback loop that accelerates market growth. The continuous advancements in OLED manufacturing processes are expected to result in even thinner, more flexible displays, opening up new possibilities for innovative device designs in the future.

Restraining Factor

High Production Costs

A significant challenge hindering the growth of the PTD market is the high production costs associated with advanced display technologies, particularly OLEDs. The manufacturing processes for OLED displays involve complex steps, including vacuum evaporation and encapsulation, which require sophisticated equipment and expertise. These processes contribute to substantial initial capital investments and ongoing operational expenses. Additionally, achieving high yield rates is challenging due to potential defects and production inefficiencies, further exacerbating costs.

The elevated production costs are often transferred to consumers through higher prices for devices equipped with OLED displays. This pricing dynamic can limit the adoption rate of OLED-equipped devices, especially in price-sensitive markets. Manufacturers face the ongoing challenge of optimizing production processes to reduce costs while maintaining the quality and performance of OLED displays. Addressing this issue is crucial for expanding the market reach of OLED technology and ensuring its competitiveness against alternative display solutions.

Growth Opportunity

Integration of E-Paper Displays in IoT Devices

The integration of e-paper displays into Internet of Things (IoT) devices presents a significant growth opportunity in the PTD market. E-paper, or electronic paper, is known for its low power consumption and high readability, making it ideal for IoT applications that require continuous display of information without frequent battery recharging. Devices such as smart labels, electronic shelf tags, and wearable sensors can benefit from the unique attributes of e-paper displays.

As the IoT ecosystem expands, the demand for energy-efficient and always-on display solutions grows. E-paper displays meet these requirements, offering a viable solution for applications where traditional displays may be impractical due to power constraints. The adoption of e-paper technology in IoT devices aligns with the broader trend towards sustainability and energy efficiency in technology. This integration not only enhances the functionality of IoT devices but also opens new avenues for innovation in various sectors, including retail, healthcare, and logistics.

Challenging Factor

Environmental and Health Concerns

Environmental and health concerns pose significant challenges to the PTD market, particularly regarding the materials used in display manufacturing and the disposal of electronic waste. Traditional display technologies, such as LCDs and OLEDs, often contain hazardous substances like mercury and heavy metals, which can have detrimental effects on both human health and the environment if not properly managed.

The production and disposal of displays contribute to environmental pollution, raising concerns about sustainability and regulatory compliance. Manufacturers face increasing pressure from governments and consumers to adopt eco-friendly practices, such as using non-toxic materials and implementing recycling programs.

Failure to address these concerns can lead to stricter regulations, increased operational costs, and potential damage to brand reputation. Therefore, developing environmentally friendly display technologies and sustainable manufacturing processes is essential for the long-term growth and acceptance of PTDs in the market.

Growth Factors

The Paper-Thin Displays (PTDs) market is experiencing remarkable growth, fueled by continuous technological advancements in display technologies. Innovations in materials and manufacturing processes have enhanced the flexibility, image quality, and energy efficiency of PTDs, making them increasingly attractive for a wide range of applications. As these advancements continue to evolve, the market is expected to grow at a Compound Annual Growth Rate (CAGR) of 20.65% from 2025 to 2030.

The increasing demand for lightweight, portable, and energy-efficient devices across industries such as consumer electronics, automotive, and retail is a major driver of this growth. The ability to create flexible, foldable, and ultra-thin displays is paving the way for new design possibilities in products like smartphones, wearables, and smart signage.

Emerging Trends

Several emerging trends are shaping the future of the PTD market. One of the most significant trends is the integration of advanced features such as haptic feedback and Augmented Reality (AR) capabilities into PTDs, enhancing user interaction and providing a more immersive experience. Another key trend is the development of transparent displays, which are being explored for applications in automotive dashboards, retail, and interactive public displays.

These transparent displays offer new design opportunities for products that require both visibility and interactivity. Additionally, the focus on energy-efficient technologies is gaining traction, as PTDs consume less power compared to traditional displays. This trend supports the growing demand for sustainable and eco-friendly solutions in consumer electronics, where battery life is a crucial consideration.

Business Benefits

Adopting PTD technology provides several business benefits, making it an attractive option for companies looking to differentiate their products and increase market competitiveness. First, PTDs allow businesses to offer unique, visually appealing products that stand out in crowded markets. This product differentiation can help companies attract a broader customer base and increase sales.

Furthermore, PTDs are energy-efficient, leading to reduced operational costs for businesses that utilize displays in products requiring continuous use. For example, in digital signage and wearable devices, the low power consumption of PTDs can result in significant savings over time.

Additionally, as consumers increasingly prioritize sustainable and innovative products, adopting PTD technology allows businesses to align with these preferences, boosting brand reputation and fostering customer loyalty. These advantages make PTDs an essential component of future-proofing product lines and meeting market demand for cutting-edge, environmentally conscious technology.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

LG Display has consistently demonstrated its leadership in OLED technology. In January 2025, the company unveiled its latest OLED TV panel, achieving a remarkable 33% increase in brightness over previous generations, reaching a peak of 4,000 nits. This advancement is attributed to their innovative Primary RGB Tandem structure, enhancing both energy efficiency and color brightness by 40%.

Samsung Electronics has strategically expanded its OLED manufacturing capabilities. In September 2024, the company announced plans to invest $1.8 billion in building an OLED manufacturing facility in Bac Ninh province, Vietnam. This investment aims to produce OLED displays for automotive and technological applications, increasing Samsung’s total investment in the region to $8.3 billion.

Sony Corporation continues to excel in the display sector, with its A95L OLED TV being named the best TV of 2024 at the 20th annual Value Electronics TV Shootout. The competition evaluated various OLED and Mini LED models, with the A95L standing out for its exceptional color accuracy and shadow detail, reaffirming Sony’s expertise in delivering high-quality visual experiences.

Top Key Players in the Market

- LG Display Co., Ltd.

- Samsung Electronics Co., Ltd.

- Sony Corporation

- BOE Technology Group Co., Ltd.

- Plastic Logic GmbH

- AU Optronics Corp.

- Sharp Corporation

- Royole Corporation

- FlexEnable Limited

- C3Nano Inc.

- Visionox Technology Inc.

- Innolux Corporation

- TCL Technology Group Corporation

- Universal Display Corporation

- Other Key Players

Recent Developments

- In 2024, LG Display launched its fourth-generation OLED TV panel, increasing brightness by 33% and improving energy efficiency.

- In 2024, Samsung Electronics announced a $1.8 billion investment in OLED manufacturing in Vietnam to support the growing demand for advanced display technologies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.16 Billion |

| Forecast Revenue (2034) | USD 51.87 Billion |

| CAGR (2025-2034) | 28.70% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (OLED (Organic Light-Emitting Diode), LCD (Liquid Crystal Display), PDLC (Polymer Dispersed Liquid Crystal Display), Others), By Application (Smartphones & Tablets, Wearable Devices, E-Readers, Smart Cards, Automotive Displays, Retail & Signage Displays, Medical Devices, Others), By End-User Industry (Consumer Electronics, Automotive,, Retail, Healthcare, Industrial, Education, Aerospace & Defense, Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | LG Display Co., Ltd., Samsung Electronics Co., Ltd., Sony Corporation, BOE Technology Group Co., Ltd., Plastic Logic GmbH, AU Optronics Corp., Sharp Corporation, Royole Corporation, FlexEnable Limited, C3Nano Inc., Visionox Technology Inc., Innolux Corporation, TCL Technology Group Corporation, Universal Display Corporation, Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Market")