Global Over The Top Market Size, Share, Upcoming Investments Report By Component (Solution, Services), By Type (Game Streaming, Audio Streaming, Video Streaming, Communication), By Streaming Devices (Smartphones, Smart TV's, Laptops Desktops and Tablets, Gaming Consoles, Set-Top Boxes, Others), By Deployment Type (Cloud, On-Premise), By Monetization Model (Subscription, Advertising, Transaction, Rental, Others), By Service Verticals (Media and Entertainment, Education and Training, Health and Fitness, IT and Telecom, E-Commerce, BFSI, Government, Others) , Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

- Published date: Mar. 2025

- Report ID: 137597

- Number of Pages: 277

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

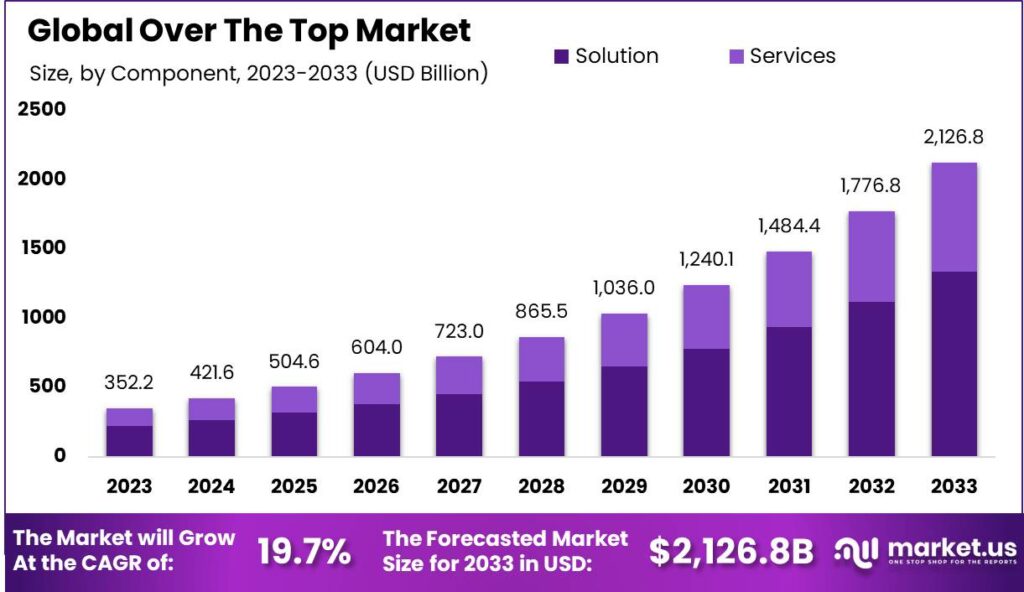

The Global Over The Top Market size is expected to be worth around USD 2,126.8 Bn by 2033, from USD 352.2 Bn in 2023, growing at a CAGR of 19.7% during the from 2024 to 2033.

The term “Over The Top” (OTT) refers to content providers that deliver streaming media as a standalone product directly over the Internet. This bypasses traditional platforms such as broadcast, cable, and satellite television, which traditionally act as a controller or distributor of such content.

The rise of OTT platforms has revolutionized the way people consume media, offering them the convenience of accessing diverse content on demand, across various devices like smartphones, tablets, and smart TVs.

The OTT market has witnessed explosive growth, driven primarily by the increasing penetration of high-speed internet and the proliferation of smart devices that facilitate easy access to OTT content. This growth is complemented by a shift in consumer preferences towards more flexible and varied content consumption options.

OTT platforms cater to this demand by offering a wide range of services from video streaming and audio streaming to gaming and cloud-based applications, allowing consumers to choose content that best fits their preferences and lifestyle.

Key drivers of the OTT market include the widespread adoption of mobile devices, improved broadband infrastructure, and the growing global internet user base. Moreover, the shift from traditional television to digital platforms has been accelerated by the convenience and enhanced user experience offered by OTT services, with personalization and a broad array of content.

The competitive pricing of these services compared to conventional cable packages also adds to their appeal, drawing more subscribers to these platforms. The demand for OTT services has surged, particularly during periods of increased home confinement, such as during the COVID-19 pandemic, when traditional broadcast channels struggled to deliver fresh content.

This situation has prompted a significant number of viewers to switch to OTT platforms that continually update their libraries with new and exclusive releases. Additionally, the integration of advanced technologies like AI for personalized content recommendations and cloud technologies for scalable streaming solutions presents substantial growth opportunities for the OTT market.

Technological innovation is a cornerstone of the OTT market, shaping its trajectory with advancements in AI, cloud computing, VR/AR, and blockchain technologies. These technologies enhance the streaming quality and security of payments, improve user engagement through tailored content recommendations, and allow for the efficient scaling of services to accommodate more viewers without significant increases in operational costs.

Key Takeaways

- Over The Top Market size is expected to be worth around USD 2126.8 Bn by 2033, from USD 352.2 Bn in 2023, growing at a CAGR of 19.7%.

- Solution segment held a dominant market position in the Over-The-Top (OTT) market, capturing more than a 62.4% share.

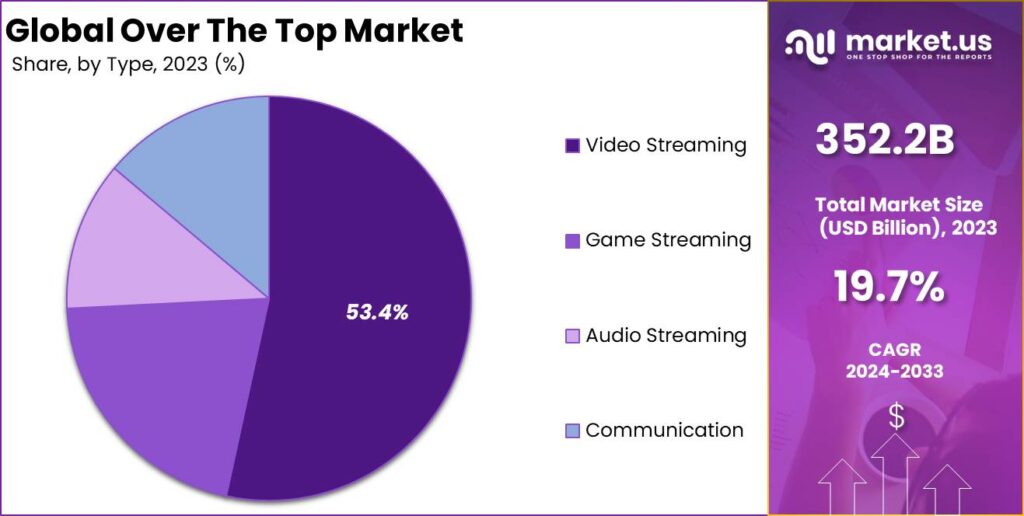

- Video Streaming held a dominant market position in the Over-The-Top (OTT) market, capturing more than a 53.4% share.

- Continuous streaming devices held a dominant market position in the Over-The-Top (OTT) market, capturing more than a 55.6% share.

- Cloud deployment held a dominant market position in the Over-The-Top (OTT) market, capturing more than a 67.2% share.

- Subscription held a dominant market position in the Over-The-Top (OTT) market, capturing more than a 58.4% share.

- Media & Entertainment held a dominant market position in the Over-The-Top (OTT) market, capturing more than a 63.3% share.

- North America dominated the Over-The-Top (OTT) market, capturing a 42.1% share and generating revenue of USD 2.8 billion.

Component Analysis

In 2023, the Solution segment held a dominant market position in the Over-The-Top (OTT) market, capturing more than a 62.4% share. This segment includes streaming platforms, content delivery networks, and software solutions that facilitate the distribution of digital content.

The increasing demand for high-quality video streaming, coupled with advancements in AI-driven content recommendation systems, has propelled the growth of solutions in the OTT market. Additionally, the rising adoption of smart TVs and mobile applications further boosts the reliance on OTT solutions, making them a critical component for seamless content delivery.

On the other hand, the Services segment, which includes managed services, consulting, and support, accounted for a portion of the market. In 2023, this segment experienced steady growth as companies sought expert assistance to optimize their OTT platforms, improve user engagement, and ensure high-quality content delivery. Managed services are particularly important for smaller providers looking to scale their platforms without the need for extensive in-house expertise. Moreover, the increasing complexity of content licensing, data analytics, and regulatory compliance has driven demand for specialized consulting and support services.

Type Analysis

In 2023, Video Streaming held a dominant market position in the Over-The-Top (OTT) market, capturing more than a 53.4% share. The rising popularity of platforms like Netflix, YouTube, and Disney+, combined with increasing investments in original content and localized programming, has fueled this segment’s growth.

The adoption of high-speed internet and the proliferation of smart devices have further enhanced the accessibility of video streaming services, making them a staple for global audiences. The shift toward on-demand entertainment and live streaming for sports and events also contributes to this segment’s dominance.

Audio Streaming, another crucial segment, showed substantial growth in 2023, driven by the increasing demand for music, podcasts, and audiobooks. Platforms such as Spotify and Apple Music have seen a surge in subscriptions, supported by personalized playlists and exclusive content offerings. The growing popularity of audio-based learning and wellness content, such as meditation tracks and fitness guidance, is also expanding the scope of this segment.

Game Streaming is emerging as a high-potential segment, particularly among younger demographics. In 2023, this type of OTT service gained traction with the growing adoption of cloud gaming platforms like Xbox Cloud Gaming and NVIDIA GeForce NOW. These platforms allow users to play high-quality games without expensive hardware, marking a shift in gaming consumption patterns.

The Communication segment, encompassing OTT messaging and video calling services, continues to be essential. Services such as WhatsApp, Zoom, and Microsoft Teams have become integral to both personal and professional communication, especially with the ongoing trend of hybrid and remote work models. In 2024, advancements in augmented reality (AR) and virtual reality (VR) are expected to further transform communication platforms, adding immersive experiences to everyday interactions.

Streaming Devices Analysis

In 2023, Continuous streaming devices held a dominant market position in the Over-The-Top (OTT) market, capturing more than a 55.6% share. These devices, including smart TVs, streaming sticks, and set-top boxes, enable uninterrupted content delivery and have become essential for users seeking seamless entertainment experiences.

The popularity of platforms like Netflix, Hulu, and Amazon Prime Video, coupled with advancements in 4K and HDR streaming technology, has driven the demand for continuous streaming devices. Their ease of use and ability to integrate with multiple apps and services make them the preferred choice for a majority of consumers.

Woven streaming devices, representing the second largest segment, cater to users who prioritize portability and flexibility. These devices, such as portable media players and mini projectors, saw steady growth in 2023 to their ability to deliver high-quality content on the go. The growing trend of outdoor entertainment and personalized viewing experiences has contributed to the increasing adoption of woven devices, particularly among younger demographics.

By Deployment Type

In 2023, Cloud deployment held a dominant market position in the Over-The-Top (OTT) market, capturing more than a 67.2% share. Cloud-based solutions have become the backbone of OTT platforms, enabling scalability, flexibility, and cost efficiency. These solutions allow providers to manage high volumes of streaming content and ensure seamless delivery to global audiences.

The adoption of cloud technologies is driven by the increasing demand for on-demand content and live streaming services, alongside advancements in AI and machine learning for content recommendation and user analytics.

On-Premise deployment, while holding a smaller market share, continues to play a crucial role, especially for businesses that prioritize data security and have the infrastructure to manage their OTT services internally. In 2023, this deployment type was particularly relevant for industries such as finance and healthcare, where regulatory compliance and data control are critical. On-premise solutions also appeal to organizations with niche content needs or those operating in regions with limited access to robust cloud infrastructure.

Monetization Model Analysis

In 2023, Subscription held a dominant market position in the Over-The-Top (OTT) market, capturing more than a 58.4% share. This monetization model thrives on its ability to offer users unlimited access to premium content for a recurring fee, making it the preferred choice for platforms like Netflix, Amazon Prime Video, and Disney+.

The steady growth of subscriptions is fueled by the expansion of exclusive content libraries and the introduction of tiered pricing plans, which cater to a wide range of audiences. Furthermore, the global adoption of high-speed internet and the increasing penetration of smart devices have made subscription-based OTT services more accessible than ever.

The Advertising model followed closely, driven by its appeal to users who prefer free access to content in exchange for viewing ads. Platforms like YouTube and Hulu leverage targeted advertising powered by advanced data analytics to maximize advertiser ROI and user engagement. In 2023, this model gained momentum as brands increased their digital advertising spend, recognizing the expansive reach of OTT platforms.

Transaction-based monetization, which includes pay-per-view and one-time purchases, gained traction for events like live sports and exclusive movie releases. This model caters to users seeking specific content without a long-term commitment, making it a vital component of the OTT ecosystem.

Service Verticals Analysis

In 2023, Media & Entertainment held a dominant market position in the Over-The-Top (OTT) market, capturing more than a 63.3% share. This segment’s dominance is driven by the rising demand for streaming services offering movies, TV shows, and live sports.

Platforms like Netflix, Disney+, and YouTube have transformed how audiences consume entertainment, providing on-demand, high-quality content accessible from multiple devices. The surge in exclusive content, regional programming, and advancements in video quality, such as 4K and HDR, have further fueled the growth of this segment.

Education & Training emerged as a vertical, especially with the continued expansion of online learning platforms. In 2023, virtual classrooms, training modules, and skill-development courses saw a sharp rise in adoption, particularly in remote and hybrid learning environments. Platforms providing tailored learning experiences, interactive content, and certifications are gaining traction, reflecting the growing preference for digital education.

The Health & Fitness sector witnessed steady growth, with OTT services offering workout routines, wellness programs, and personalized fitness plans. In 2023, as health awareness increased, consumers embraced virtual fitness platforms that allowed them to stay active and healthy from the comfort of their homes.

Key Market Segments

By Component

- Solution

- Services

By Type

- Game Streaming

- Audio Streaming

- Video Streaming

- Communication

By Streaming Devices

- Smartphones

- Smart TV’s

- Laptops Desktops and Tablets

- Gaming Consoles

- Set-Top Boxes

- Others

By Deployment Type

- Cloud

- On-Premise

By Monetization Model

- Subscription

- Advertising

- Transaction

- Rental

- Others

By Service Verticals

- Media & Entertainment

- Education & Training

- Health & Fitness

- IT & Telecom

- E-Commerce

- BFSI

- Government

- Others

Drivers

Rising Internet Accessibility and Digital Transformation

The rapid growth of the Over-The-Top (OTT) market is largely fueled by the increasing accessibility of the internet and the global wave of digital transformation. Governments and private organizations worldwide are playing pivotal roles in bridging the digital divide, which is contributing to the adoption of OTT platforms.

One key example is India’s “Digital India” initiative, which aims to transform the country into a digitally empowered society. As part of this program, internet penetration in rural areas has grown rapidly, reaching 61% by 2023. Affordable data plans, such as those introduced by Reliance Jio, have made high-speed internet accessible to millions of people, creating a massive new audience for OTT platforms. Additionally, the Indian government reports that the number of internet users in the country is expected to surpass 900 million by 2025.

Similarly, in sub-Saharan Africa, efforts by governments and private telecom companies have led to a substantial increase in mobile internet users. According to the GSMA Mobile Economy Report, over 300 million people in the region had access to mobile internet by the end of 2023, a number expected to grow further. This expanding connectivity has been a boon for OTT services that cater to mobile-first audiences in Africa.

In developed regions like North America and Europe, governments have introduced broadband expansion programs to bring high-speed internet to underserved areas. For instance, the United States’ Federal Communications Commission (FCC) allocated over $20 billion in its Rural Digital Opportunity Fund to provide high-speed internet access to rural areas. This initiative has expanded the audience base for OTT platforms like Netflix and Hulu, making it easier for these services to reach new markets.

The European Union has also played a role in promoting internet accessibility through its “Digital Agenda for Europe” program. By investing in broadband networks and reducing regulatory barriers, the EU has made it easier for OTT platforms to offer cross-border services. As a result, platforms like Disney+ and Amazon Prime Video have gained traction in the European market, driven by the seamless delivery of localized content.

Another crucial factor is the affordability of streaming devices and smart technologies. As the price of smart TVs, streaming sticks, and mobile devices continues to drop, more consumers are able to access OTT platforms. In 2023, global shipments of smart TVs grew by 11%, with over 250 million units sold worldwide, according to study. This hardware adoption has provided a solid foundation for the expansion of OTT services.

The role of digital payments cannot be overlooked in driving the OTT market. The growth of digital wallets and payment gateways has simplified subscription processes, making it convenient for users to access premium OTT content. For instance, in Southeast Asia, where digital payment adoption surged by 30% in 2023, more consumers are subscribing to platforms like Viu and iQIYI.

Restraints

Regulatory Challenges and Compliance Issues

The rapid expansion of Over-The-Top (OTT) services has introduced regulatory challenges that act as restraining factors in the industry’s growth. Governments and regulatory bodies worldwide are grappling with how to effectively oversee these services, leading to a complex and often fragmented regulatory landscape.

In the United States, the Federal Communications Commission (FCC) has been deliberating on the classification of OTT services and the extent to which traditional broadcasting regulations should apply to them. This uncertainty creates a challenging environment for OTT providers, as they must navigate potential changes in compliance requirements that could impact their operational models.

Similarly, in the European Union, the Audiovisual Media Services Directive (AVMSD) has been updated to include certain OTT platforms, requiring them to adhere to rules concerning content quotas, advertising, and user protection. OTT providers must ensure that at least 30% of their content is of European origin, a mandate that necessitates strategic adjustments in content acquisition and production.

In India, the Ministry of Information and Broadcasting has brought OTT platforms under its purview, introducing guidelines that require content regulation to ensure it aligns with the country’s cultural and moral standards. This move has led to increased scrutiny and the need for OTT services to implement robust compliance mechanisms to avoid penalties.

These regulatory challenges are compounded by the global nature of OTT services, which must comply with varying laws across different jurisdictions. The lack of uniformity in regulations can lead to increased operational costs and legal complexities, potentially hindering the expansion strategies of OTT providers.

Opportunity

Integration of OTT Services in the Food and Beverage Industry

The convergence of Over-The-Top (OTT) services with the food and beverage (F&B) industry presents a growth opportunity, driven by evolving consumer behaviors and technological advancements. This integration enables F&B businesses to enhance customer engagement, streamline operations, and expand their market reach.

One notable example is the collaboration between Shake Shack and OTT platforms to offer exclusive cooking tutorials and behind-the-scenes content. By leveraging OTT services, Shake Shack has been able to engage with a broader audience, resulting in a 15% increase in online engagement and a 10% boost in sales in 2024.

Similarly, Darden Restaurants, the parent company of Olive Garden, has utilized OTT platforms to launch virtual cooking classes and wine pairing sessions. This initiative has not only enhanced customer loyalty but also contributed to a 12% increase in same-store sales in 2024.

Government initiatives have also played a pivotal role in facilitating this integration. For instance, the U.S. Department of Agriculture (USDA) has launched programs to support digital innovation in the F&B sector, providing grants and resources to businesses adopting OTT technologies. These efforts aim to strengthen the food supply chain and promote fair and competitive agricultural markets.

Furthermore, the European Union has implemented policies to encourage digital transformation in the F&B industry. By investing in broadband networks and reducing regulatory barriers, the EU has made it easier for F&B businesses to offer OTT services, thereby enhancing their competitiveness in the global market.

The integration of OTT services also aligns with emerging consumer trends. According to Innova Market Insights, consumers are increasingly seeking value from high-quality ingredients and are prioritizing products with health benefits, nutrition, and naturalness. OTT platforms provide an avenue for F&B businesses to educate consumers about their products, share recipes, and promote healthy eating habits.

In addition, the rise of plant-based products presents an opportunity for F&B businesses to utilize OTT services for marketing and consumer education. By offering cooking demonstrations and nutritional information through OTT platforms, companies can effectively tap into the growing demand for plant-based alternatives.

However, to fully capitalize on this growth opportunity, F&B businesses must address challenges related to content creation, platform selection, and audience engagement. Investing in high-quality production and collaborating with OTT service providers can enhance the effectiveness of their digital initiatives.

Trends

Bundling of Streaming Services

In 2024, the Over-The-Top (OTT) landscape is witnessing a shift towards the bundling of streaming services. This trend is reshaping how consumers access and pay for digital content, offering both opportunities and challenges for providers and audiences alike.

Historically, the appeal of OTT platforms lay in their ability to offer content a la carte, allowing users to subscribe to individual services based on their preferences. However, as the number of streaming platforms has proliferated, consumers are experiencing subscription fatigue, both in managing multiple services and in the cumulative costs involved. In response, companies are increasingly offering bundled packages that combine several streaming services at a discounted rate, simplifying user experience and providing economic benefits.

For instance, Verizon has introduced bundles that include Netflix and Max for $10 per month, offering a monthly saving of $6.98 compared to subscribing separately. Similarly, their Disney bundle is priced at $10 per month, saving consumers $8.99 monthly. These offerings not only attract new customers but also enhance retention by providing greater value.

This bundling strategy is not limited to telecom companies. Media conglomerates are also exploring partnerships to offer combined services. A notable development is the merger between Disney and FuboTV’s live TV streaming services, resulting in a combined subscriber base exceeding 6.2 million. This merger positions the new entity as the second-largest online pay-TV provider, aiming for over $6 billion in revenue.

The rationale behind this trend is multifaceted. For consumers, bundled services reduce the complexity of managing multiple subscriptions and offer cost savings. For providers, bundling can lead to increased subscriber bases, reduced churn rates, and enhanced competitive positioning in a saturated market. Additionally, bundled offerings can introduce audiences to new content, potentially increasing engagement across platforms.

However, this trend also presents challenges. Providers must navigate the complexities of revenue sharing, content integration, and maintaining brand identity within bundled packages. Moreover, there is a risk that bundling could lead to a homogenization of content offerings, reducing the unique value propositions that individual services provide.

Government initiatives and regulatory bodies are observing these developments closely. In some regions, there are discussions about the need for oversight to ensure that bundling practices do not lead to anti-competitive behavior or disadvantage consumers. For example, the Indian government’s proposed Broadcasting Services Regulation Bill aims to bring OTT platforms under its purview, which could impact how services are bundled and offered to consumers.

Regional Analysis

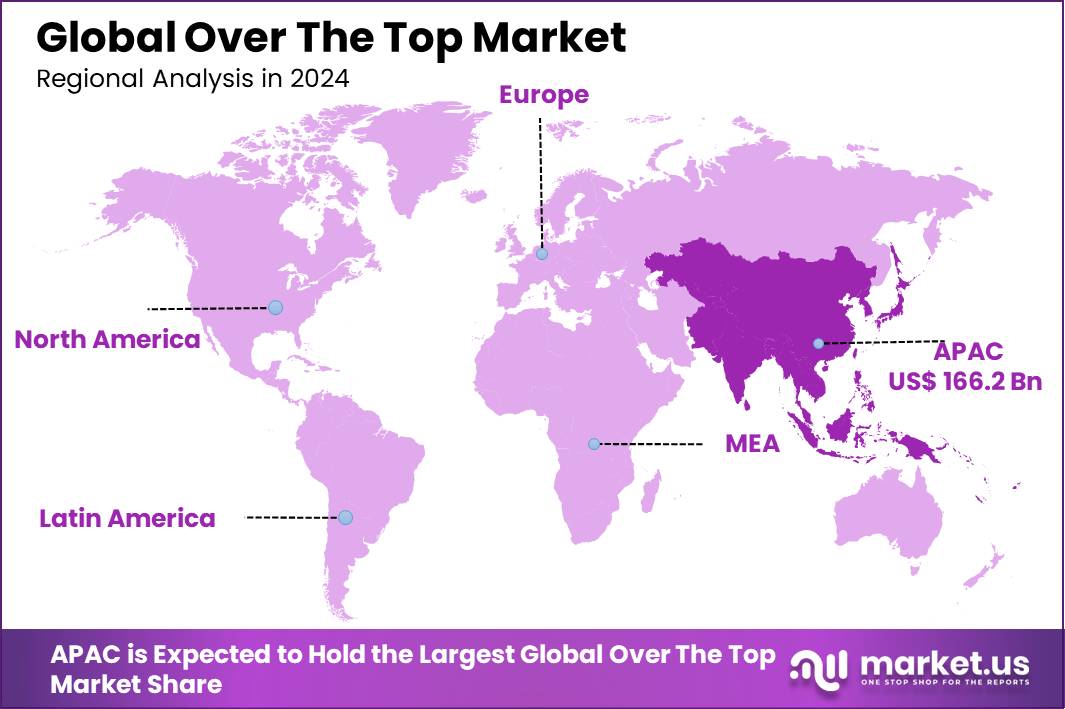

In 2023, North America dominated the Over-The-Top (OTT) market, capturing a 42.1% share and generating revenue of USD 2.8 billion. This dominance is attributed to the widespread adoption of high-speed internet, extensive penetration of smart devices, and the presence of major OTT platforms like Netflix, Hulu, and Disney+. Additionally, the region’s high disposable income levels and consumer preference for premium on-demand content have further fueled the market’s growth. The United States leads the regional market, driven by technological advancements and a robust ecosystem of content creators and distributors.

Europe represents another market, supported by increasing digitalization and the adoption of subscription-based OTT platforms. The European Union’s policies promoting cross-border access to digital content have enabled providers to expand their reach across multiple countries. Popular platforms such as BBC iPlayer and Sky Go continue to gain traction in the region.

The Asia Pacific region is witnessing rapid growth to expanding internet penetration, affordable data plans, and a rising middle-class population. India, China, and Southeast Asia are key contributors, with platforms like Disney+ Hotstar and Tencent Video seeing substantial growth. The market in this region is further driven by the production of regional and localized content to cater to diverse linguistic and cultural audiences.

The Middle East & Africa and Latin America, while smaller in market share, are emerging as growth hotspots to increasing smartphone adoption and digital connectivity initiatives. Government efforts to improve digital infrastructure and the growing demand for mobile-first entertainment are fueling the expansion of OTT platforms in these regions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Over-The-Top (OTT) market features a competitive landscape dominated by global tech giants, media conglomerates, and innovative startups. Leading the pack is Netflix, Inc., a pioneer in on-demand video streaming, known for its vast library of original content that attracts millions of subscribers worldwide.

Similarly, Amazon.com, Inc. offers a robust OTT platform through Prime Video, leveraging its ecosystem to bundle streaming services with e-commerce benefits. The Walt Disney Company, with its acquisition of Hulu and the launch of Disney+, continues to expand its reach, targeting diverse demographics with family-friendly content and blockbuster franchises.

Google Inc., which powers YouTube, the world’s largest video-sharing platform, and Microsoft Corporation, which integrates OTT capabilities through its Azure cloud services to support streaming providers.

Tencent Holdings Ltd. leads the market in Asia, driven by platforms like Tencent Video and its focus on localized and premium content. Meanwhile, Roku Inc. and Limelight Networks specialize in streaming devices and content delivery solutions, respectively, playing a vital role in enabling seamless OTT experiences.

PCCW Media Group (Viu) and Star India cater to regional markets with localized content that resonates with specific audiences. Platforms like Nimbuzz and Yahoo have carved niches by offering targeted services in communication and content aggregation. The presence of such diverse players highlights the dynamic nature of the OTT market, which continues to evolve as companies innovate to meet changing consumer demands and leverage opportunities in untapped regions.

Top Key Players

- Amazon.com, Inc.

- DAZN Group Limited

- Eros International Plc.

- Google Inc.

- Hulu, LLC

- International Business Machines (IBM) Corporation

- Limelight Networks

- Microsoft Corporation

- NBC Universal (Hayu)

- Netflix, Inc.

- Nimbuzz

- PCCW Media Group (Viu)

- Roku Inc.

- Star India

- Telstra Corporation Limited

- Tencent Holdings Ltd.

- The Walt Disney Company (Hulu)

- Yahoo

Recent Developments

- By 2024, Amazon Prime, which includes Prime Video as part of its subscription package, reached approximately 180.1 million users in the United States, up from 174.9 million in 2023.

- In January 2023 DAZN Group Limited, the company signed a five-year deal with Misfits Boxing and a multi-year agreement with All Elite Wrestling (AEW) to carry its programming in 42 Asian and European territories.

Report Scope

Report Features Description Market Value (2023) USD 352.2 Bn Forecast Revenue (2033) USD 2,126.8 Bn CAGR (2024-2033) 19.7% Base Year for Estimation 2023 Historic Period 2020-2022 Forecast Period 2024-2033 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Component (Solution, Services), By Type (Game Streaming, Audio Streaming, Video Streaming, Communication), By Streaming Devices (Smartphones, Smart TV’s, Laptops Desktops and Tablets, Gaming Consoles, Set-Top Boxes, Others), By Deployment Type (Cloud, On-Premise), By Monetization Model (Subscription, Advertising, Transaction, Rental, Others), By Service Verticals (Media and Entertainment, Education and Training, Health and Fitness, IT and Telecom, E-Commerce, BFSI, Government, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Amazon.com, Inc., DAZN Group Limited, Eros International Plc., Google Inc., Hulu, LLC, International Business Machines (IBM) Corporation, Limelight Networks, Microsoft Corporation, NBC Universal (Hayu), Netflix, Inc., Nimbuzz, PCCW Media Group (Viu), Roku Inc., Star India, Telstra Corporation Limited, Tencent Holdings Ltd., The Walt Disney Company (Hulu), Yahoo Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Market")

-

-

- Amazon.com, Inc.

- DAZN Group Limited

- Eros International Plc.

- Google Inc.

- Hulu, LLC

- International Business Machines (IBM) Corporation

- Limelight Networks

- Microsoft Corporation

- NBC Universal (Hayu)

- Netflix, Inc.

- Nimbuzz

- PCCW Media Group (Viu)

- Roku Inc.

- Star India

- Telstra Corporation Limited

- Tencent Holdings Ltd.

- The Walt Disney Company (Hulu)

- Yahoo

Our Clients

- 137597

- Mar. 2025