Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of Organic Cheese Market

- By Product Type Analysis

- By Form Analysis

- By Application Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

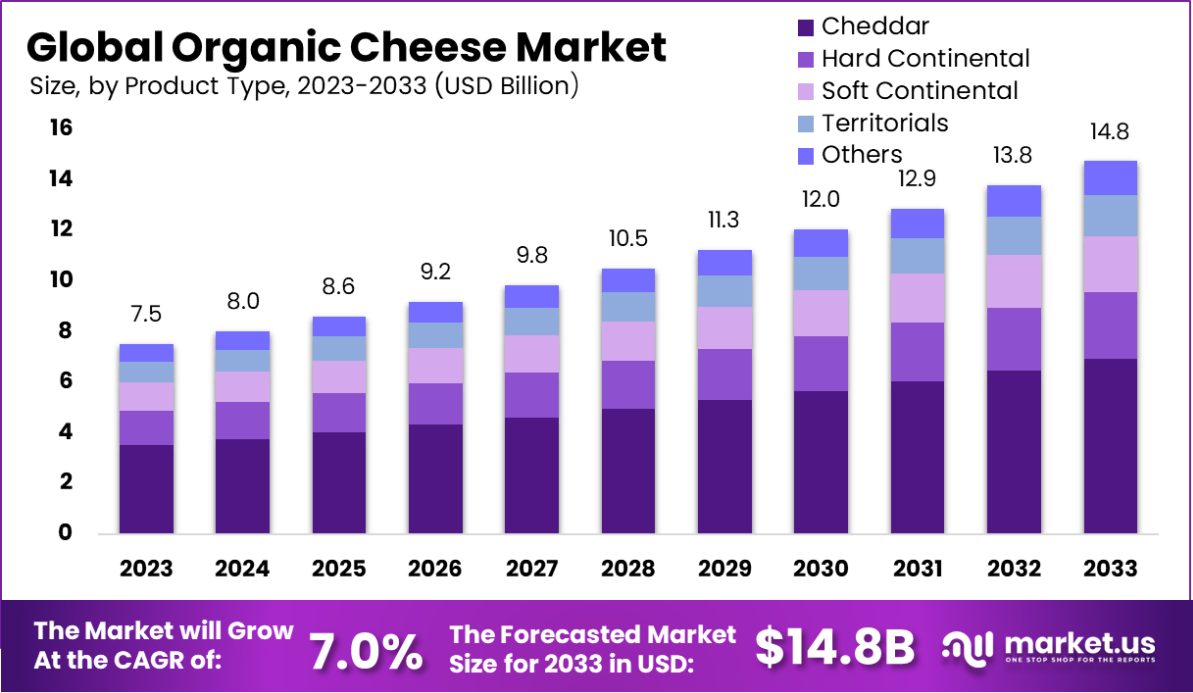

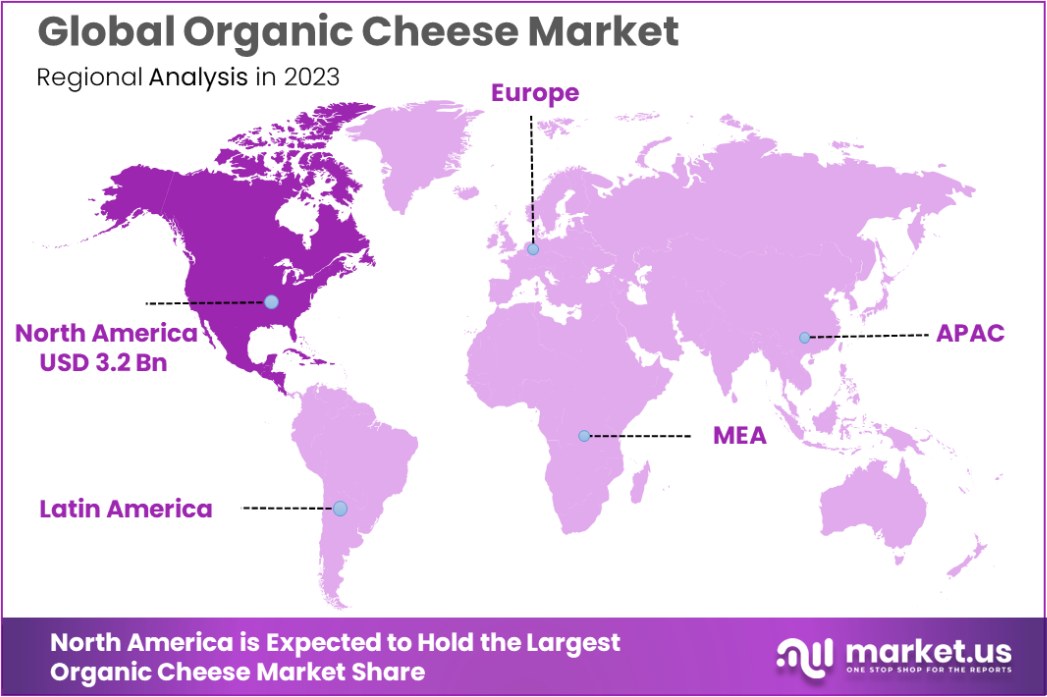

The Global Organic Cheese Market is expected to be worth around USD 14.8 Billion by 2033, up from USD 7.5 Billion in 2023, and grow at a CAGR of 7.0% from 2024 to 2033. North America dominates the organic cheese market, 43.3%, USD 3.2 billion.

The organic cheese market is currently experiencing significant growth, driven by rising consumer awareness of health and environmental concerns. This market segment benefits from a global shift towards organic and natural food products, aligning with consumer preferences for sustainable and chemical-free diets.

From an industrial standpoint, the production of organic cheese adheres to stringent regulations that prohibit the use of artificial chemicals, hormones, and GMOs in dairy farming. This compliance fosters a transparent supply chain and supports sustainable agricultural practices.

The market’s growth is further propelled by governmental support in many countries, encouraging organic farming through subsidies and incentives, which in turn stimulates the organic cheese industry.

Key driving factors include the increasing prevalence of lifestyle diseases and a growing inclination towards healthier diets among consumers, especially in developed economies. These trends are substantiated by data from government sources such as the United States Department of Agriculture (USDA) and the European Commission, which report a steady increase in the consumption of organic products.

Moreover, the expansion of retail formats offering organic products has made organic cheese more accessible to a broader audience, further driving market growth.

Future growth opportunities in the organic cheese market lie in innovation and product diversification. Producers are increasingly experimenting with new flavors and cheese types to cater to diverse consumer tastes and dietary requirements. Additionally, the integration of organic cheese into fast food and ready-to-eat meals presents a potential growth area, given the current trend toward convenience foods.

The organic cheese market is increasingly buoyed by substantial federal support, reflecting growing consumer preference for sustainable and health-conscious dairy options. In 2024, the Rumiano Cheese Company, a prominent player in California’s organic dairy sector, secured a notable $3 million investment from the Agricultural Marketing Service.

This funding aims to enhance market opportunities for organic dairy producers through value-added processing and targeted marketing initiatives, underscoring a strategic push toward expanding the organic cheese segment.

Moreover, the Organic Market Development Grant program further bolstered this segment by allocating an additional $10 million in 2024. This influx of capital is poised to catalyze innovation and expansion, further enhancing the market’s growth trajectory.

Complementing these financial initiatives, the USDA’s Natural Resources Conservation Service (NRCS) has also been instrumental, providing $5 million to Oregon Tilth and the Organic Farming Research Foundation. This funding is designated for fortifying organic expertise, crucial for advancing organic practices and products.

The NRCS continued its support into 2023 by distributing $12 million across 22 states, establishing 112 contracts with producers transitioning to organic operations. Furthermore, the Organic Certification Cost Share Program (OCCSP) significantly reduces the financial burden on producers by covering up to 75% of organic certification costs, capped at $750 per category in 2024.

Key Takeaways

- The Global Organic Cheese Market is expected to be worth around USD 14.8 Billion by 2033, up from USD 7.5 Billion in 2023, and grow at a CAGR of 7.0% from 2024 to 2033.

- Cheddar dominates the Organic Cheese Market, holding a substantial 47.4% share by product type.

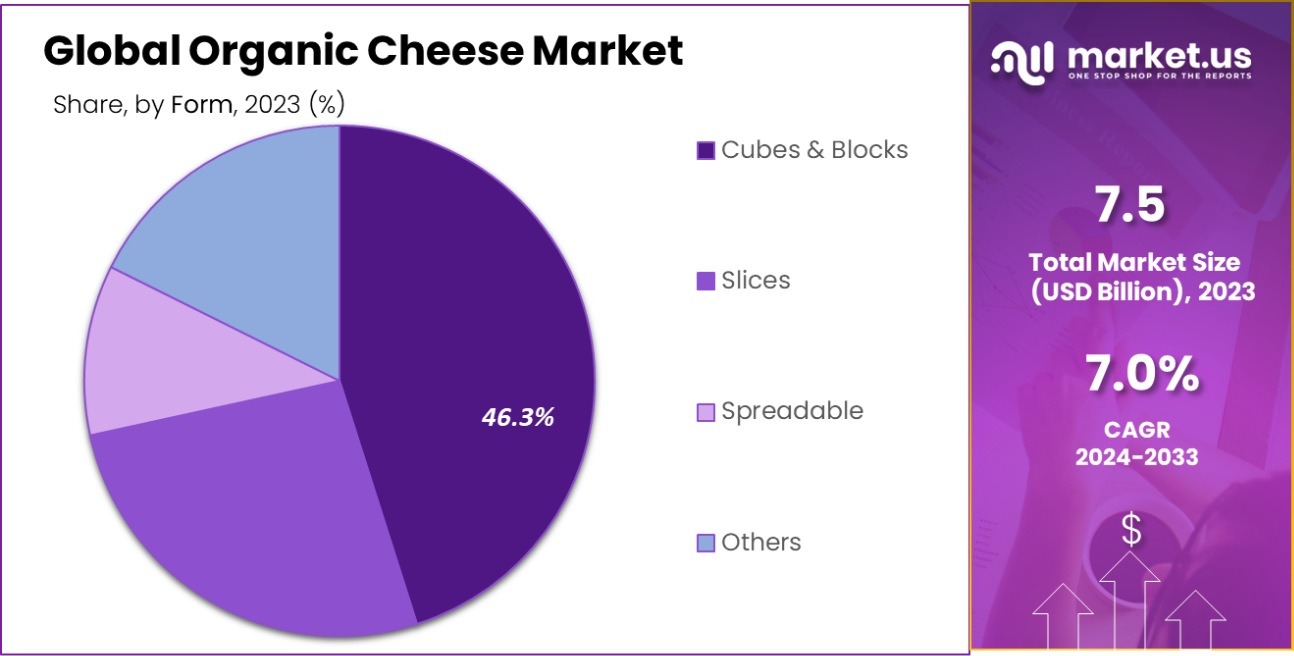

- Cubes and blocks form the most popular shapes, making up 46.3% of the market.

- Bakery goods are a leading application for organic cheese, accounting for 28.3% of usage.

- Supermarkets and hypermarkets are key distribution channels, commanding 47.4% of the market share.

- North America dominates the Organic Cheese Market with 43.3%, valued at USD 3.2 billion.

Business Benefits of Organic Cheese Market

The organic cheese market offers significant business benefits, particularly for producers, retailers, and allied industries. One primary advantage is the premium pricing associated with organic products. Due to the growing consumer demand for healthier and environmentally friendly options, businesses can charge higher prices for organic cheese, enhancing profit margins.

Producers benefit from government initiatives that support organic farming. For example, programs such as the Organic Certification Cost Share Program (OCCSP) subsidize certification costs, reducing the financial burden on farmers. Additionally, grants from agencies like the USDA encourage investments in organic dairy production and market expansion.

Retailers gain from the rising popularity of organic cheese by attracting health-conscious and environmentally aware consumers. These products enhance a store’s image as a provider of high-quality, sustainable food options, increasing customer loyalty and foot traffic.

Organic cheese production also supports sustainability goals by promoting eco-friendly farming practices, including reduced pesticide use and improved soil health. These methods align with global trends toward sustainability, enabling businesses to meet environmental standards and reduce carbon footprints.

By Product Type Analysis

Cheddar dominates the product type at 47.4% in the organic cheese market.

In 2023, Cheddar held a dominant market position in the By Product Type segment of the Organic Cheese Market, capturing a 47.4% share. This significant portion underscores the enduring popularity and widespread consumer preference for Cheddar in the organic sector. The robust demand for Cheddar is attributed to its versatile culinary applications and established presence in both retail and food service channels.

Following Cheddar, Hard Continental Cheeses represented a noteworthy segment, reflecting diverse European influences and a growing appreciation for robust, mature flavors among organic consumers. Soft Continental varieties, known for their delicate textures and milder flavors, also captured a substantial market share, catering to a demographic seeking lighter, more refined cheese experiences.

Territorials, another key segment, includes region-specific varieties that appeal to consumers interested in traditional and artisanal products. This segment benefits from a niche market that values authenticity and provenance, which are critical factors in the purchasing decisions of organic cheese consumers.

Overall, these segments collectively represent a dynamic and diverse organic cheese market. Each category addresses different consumer preferences and culinary needs, supported by an expanding infrastructure for organic production and marketing initiatives aimed at educating consumers about the benefits of organic cheese.

By Form Analysis

Cubes and blocks lead forms at 46.3% in organic cheese offerings.

In 2023, Cubes and Blocks held a dominant market position in the By Form segment of the Organic Cheese Market, with a 46.3% share. This form factor’s prominence is largely due to its convenience and versatility, making it a preferred choice for both cooking and direct consumption. Cubes and blocks of organic cheese are particularly popular in households and culinary settings where portion control and ease of use are paramount.

Slices followed as the second most popular form, capturing a significant portion of the market. Pre-sliced organic cheese caters to the consumer demand for ready-to-use options that reduce meal preparation time, ideal for quick sandwiches or as toppings. This form’s appeal is enhanced by its accessibility and user-friendly packaging, which appeals to a broad demographic including busy families and young professionals.

Spreadable organic cheeses also carved out a substantial niche. Their growing popularity is driven by the increasing consumer interest in gourmet yet convenient spread options for crackers, bread, and a dip base. The creamy texture and rich flavors of spreadable organic cheeses make them attractive for both entertaining and everyday snacking.

These form segments—cubes and blocks, slices, and spreadable—collectively address a diverse array of consumer needs and preferences, each supporting the overall growth and dynamism of the organic cheese market.

By Application Analysis

Bakery goods are a primary application, accounting for 28.3% of use.

In 2023, Bakery Goods held a dominant market position in the By Application segment of the Organic Cheese Market, accounting for 28.3% of the share. The significant share of bakery goods reflects the rising consumer preference for organic cheese as a key ingredient in artisanal bread, pastries, and savory baked items.

Organic cheese enhances the flavor profile and nutritional value of bakery products, making it a preferred choice among health-conscious consumers and specialty bakery brands.

Confectionery and Sauces and Dips emerged as other significant applications. Confectionery benefited from the increasing popularity of cheese-based desserts like cheesecakes, where organic ingredients align with consumer demand for natural indulgence.

Meanwhile, sauces and dips showcased strong growth due to their widespread use in culinary applications, including pasta sauces and cheese dips, appealing to both home cooks and the food service industry.

Ready-to-Eat (RTE) Meals and Savory Snacks also displayed robust growth. The convenience of incorporating organic cheese into pre-packaged meals and snack products resonates with busy lifestyles and the demand for premium, health-focused options.

Additionally, Seasoning and Flavorings and Desserts segments, though smaller, continue to gain traction, driven by innovations in product offerings and the expanding scope of organic cheese usage in enhancing taste and texture.

By Distribution Channel Analysis

Supermarkets and hypermarkets distribute 47.4% of organic cheese sales.

In 2023, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Organic Cheese Market, capturing a 47.4% share. The prominence of this channel can be attributed to its extensive reach, wide product assortment, and the convenience of one-stop shopping.

Supermarkets and hypermarkets offer organic cheese in various forms and applications, often alongside promotional discounts, further driving consumer preference.

Specialty Stores followed as a significant distribution channel, catering to niche audiences seeking premium, artisanal, and locally sourced organic cheese. These stores emphasize product authenticity and quality, making them attractive to discerning consumers focused on health and sustainability.

Modern Trade and Convenience Stores also played crucial roles in distribution. Modern trade outlets leverage structured retail formats and advanced inventory management to provide fresh organic cheese products, while convenience stores cater to impulse buyers and those seeking quick, accessible options.

The Online Store channel, while relatively smaller, demonstrated rapid growth driven by the e-commerce boom and increasing consumer reliance on digital platforms for grocery shopping. With doorstep delivery and customization options, online channels are reshaping accessibility for organic cheese.

Traditional Grocery Stores continue to cater to local markets, maintaining relevance by offering organic cheese to community-focused consumers. Collectively, these channels drive the organic cheese market’s accessibility and growth.

Key Market Segments

By Product Type

- Cheddar

- Hard Continental

- Soft Continental

- Territorials

- Others

By Form

- Cubes and Blocks

- Slices

- Spreadable

- Others

By Application

- Bakery Goods

- Confectionery

- Sauces and Dips

- Rte Meals

- Savory Snacks

- Seasoning and Flavorings

- Desserts

- Others

By Distribution Channel

- Specialty Stores

- Modern Trade

- Convenience Stores

- Traditional Grocery Stores

- Online store

- Others

Driving Factors

Rising Consumer Preference for Healthier Food Choices

Increasing awareness about health and wellness is a major driver of the organic cheese market. Consumers are actively seeking healthier and more natural food options, and organic cheese is perceived as a safer, chemical-free alternative to conventional dairy.

The absence of synthetic pesticides, additives, and hormones aligns with the growing demand for clean-label products. This trend is further supported by the expanding health-conscious demographic, particularly among millennials and Gen Z, who are willing to pay a premium for organic dairy products.

Government Support and Funding for Organic Agriculture

Government initiatives and funding are playing a crucial role in driving the organic cheese market. Programs like the Organic Market Development Grant and the Organic Certification Cost Share Program significantly reduce production costs for farmers.

Additional investments in organic farming expertise and infrastructure enable producers to transition more easily into the organic sector. Such policy support not only strengthens supply chains but also boosts consumer trust in certified organic products, further propelling market growth and innovation.

Expanding Distribution Networks Across Retail Channels

The expansion of supermarkets, hypermarkets, and online platforms has greatly enhanced the availability of organic cheese. Retailers are increasingly dedicating shelf space to organic products due to high consumer demand.

E-commerce platforms further simplify access, offering a diverse range of organic cheese options delivered conveniently to consumers’ doorsteps. This widespread distribution ensures that organic cheese is no longer limited to niche markets, driving greater adoption among mainstream consumers and fostering market growth on a global scale.

Restraining Factors

High Production Costs Impacting Affordability for Consumers

Organic cheese production involves stringent processes, including organic feed for livestock, pesticide-free farming, and certification compliance, all of which raise costs. These expenses are reflected in the higher retail prices of organic cheese compared to conventional options.

While health-conscious consumers are willing to pay a premium, the cost remains a significant barrier for price-sensitive buyers. This affordability gap limits the market’s reach, particularly in developing regions where disposable incomes are lower and consumer spending on premium food products is restricted.

Limited Awareness in Emerging and Rural Markets

Despite the growing popularity of organic cheese in developed countries, awareness in emerging and rural markets remains limited. Many consumers are unfamiliar with the benefits of organic cheese or skeptical about its authenticity. Furthermore, inadequate marketing campaigns and a lack of education on organic food options hinder its penetration into new regions.

Bridging this awareness gap requires concerted efforts by manufacturers and retailers to inform consumers, highlighting the product’s health and environmental benefits to foster broader adoption.

Shorter Shelf Life and Distribution Challenges

Organic cheese, free from synthetic preservatives, typically has a shorter shelf life compared to conventional cheese. This poses challenges in storage, transportation, and distribution, especially for retailers operating in regions with inadequate cold-chain infrastructure. Additionally, spoilage risks can increase logistical costs, deterring smaller retailers from stocking organic cheese.

These factors limit its availability and affect consumer confidence in its freshness, constraining market growth, particularly in remote and underserved areas. Solving these issues requires investments in advanced supply chain solutions and efficient distribution strategies.

Growth Opportunity

Rising Demand for Organic Cheese in Emerging Markets

Emerging markets present significant growth opportunities for the organic cheese industry. As disposable incomes rise and awareness of organic products increases, consumers in countries like India, China, and Brazil are beginning to prioritize healthier food options.

The urban middle class in these regions is particularly inclined toward premium and natural products. Expanding distribution networks and targeted marketing campaigns in these areas can help manufacturers tap into this untapped potential, driving growth and broadening the global footprint of organic cheese.

Innovation in Organic Cheese Varieties and Flavors

Developing new organic cheese varieties and unique flavors is a key growth opportunity. Manufacturers can cater to evolving consumer preferences by offering innovative options like plant-based organic cheese, infused flavors, or regional specialties.

These innovations can attract niche markets, such as vegans, food enthusiasts, or health-conscious buyers looking for novel products. Additionally, launching these offerings in attractive, eco-friendly packaging can further enhance their appeal, creating a strong brand identity while satisfying diverse customer demands in both domestic and international markets.

Expanding Online Retail and E-Commerce Platforms

The rapid growth of e-commerce offers vast opportunities for the organic cheese market. Online platforms allow producers to reach a wider audience without geographical limitations, offering convenience and accessibility to consumers. Digital marketplaces also facilitate personalized marketing through data analytics, helping brands target specific customer groups effectively.

By leveraging e-commerce, manufacturers can introduce subscription models, special bundles, and direct-to-consumer strategies, enhancing customer loyalty and increasing sales. This channel’s scalability and potential for global reach make it an essential driver for future market expansion.

Latest Trends

Growing Popularity of Plant-Based Organic Cheese Options

The rise of veganism and lactose intolerance awareness has driven the development of plant-based organic cheese. Consumers seeking sustainable and allergen-free alternatives are fueling demand for cheese made from ingredients like nuts, seeds, and plant-based milk.

This trend aligns with the broader shift toward environmentally friendly and ethical food choices. Manufacturers are leveraging innovative technologies to improve the taste, texture, and nutritional profile of plant-based organic cheese, capturing a growing niche market and diversifying the organic cheese product portfolio.

Increased Focus on Functional and Nutritional Benefits

Consumers are increasingly valuing organic cheese for its functional and nutritional attributes, such as high protein content, probiotics, and essential vitamins. This trend is driven by health-conscious individuals looking for foods that provide added benefits beyond taste.

Producers are incorporating functional elements into their products, such as calcium-enriched or gut-health-boosting formulations. Marketing these benefits effectively through labeling and education campaigns is further driving consumer interest, positioning organic cheese as a nutritious and health-forward dairy choice.

Integration of Sustainable Packaging for Organic Cheese Products

Sustainable packaging is becoming a critical trend in the organic cheese market. With growing environmental concerns, consumers prefer products packaged in biodegradable, recyclable, or reusable materials. Manufacturers are adopting eco-friendly packaging solutions that align with the organic ethos, ensuring minimal environmental impact.

This approach not only reduces waste but also enhances brand perception and loyalty among environmentally conscious buyers. Highlighting sustainability initiatives in marketing campaigns strengthens consumer trust and positions brands as socially responsible leaders in the organic cheese industry.

Regional Analysis

North America dominates the organic cheese market, holding a 43.3% share, valued at USD 3.2 billion.

The Organic Cheese Market exhibits regional diversity, with North America leading as the dominant market, holding a 43.3% share and valued at USD 3.2 billion in 2023. The region’s stronghold is driven by high consumer awareness, a well-established organic food industry, and government initiatives supporting organic farming. The United States contributes significantly, with rising demand for premium, health-conscious dairy products and robust retail infrastructure.

Europe follows closely, supported by the region’s deep-rooted cheese culture and stringent organic certification standards. Countries like Germany, France, and the UK are key markets due to the increasing adoption of organic diets and government subsidies promoting organic farming practices.

Asia Pacific is emerging as a lucrative market, fueled by growing disposable incomes, urbanization, and increased consumer awareness about organic products. Markets such as China, Japan, and India show rapid growth, driven by expanding e-commerce and modern trade channels.

The Middle East & Africa and Latin America represent developing markets with untapped potential. In these regions, organic cheese demand is gradually rising, supported by urbanization, changing dietary habits, and growing retail penetration. While their current market share is modest, increased investments in organic farming and consumer education are expected to accelerate growth in these regions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global organic cheese market witnessed dynamic contributions from leading players, each leveraging their unique strengths to drive growth and innovation. Arla Foods and Fonterra Co-operative Group Limited maintained strong market positions through extensive product portfolios and robust global distribution networks. Their commitment to sustainability and organic certifications further reinforced consumer trust and brand loyalty.

Danone S.A. and Groupe Lactalis S.A. capitalized on their expertise in dairy and organic innovation, introducing premium and functional cheese varieties tailored to health-conscious consumers. Similarly, Aurora Organic Dairy and Organic Valley stood out as pioneers in organic farming practices, emphasizing authenticity and farm-to-table quality.

Retail giants like Whole Foods Market, Inc., Safeway Inc., and Kroger Co. played a pivotal role in expanding market accessibility. By offering a wide range of organic cheese products, these retailers supported consumer demand and boosted market penetration. Horizon Organic, part of Danone, leveraged its strong brand identity to target families and health-focused buyers.

Unilever N.V. and Kerry Group plc focused on value-added cheese products, enhancing flavors and textures to meet evolving consumer preferences. Smaller players such as Eden Valley Creamery upheld artisanal values, catering to niche markets demanding traditional organic cheese.

Overall, strategic investments in product innovation, distribution, and sustainability positioned these companies as key contributors to market growth. Collaborations, acquisitions, and advancements in organic farming technologies are expected to further strengthen their market presence in the coming years.

Top Key Players in the Market

- Arla Foods

- Aurora Organic Dairy

- Danone S.A.

- Eden Valley Creamery

- Fonterra Co-operative Group Limited

- Groupe Lactalis S.A

- Horizon Organic

- Hormel Foods

- Kerry Group plc

- Organic Valley

- Ornua

- Safeway Inc.

- The Kroger Co.

- The WhiteWave Foods Company

- Unilever N.V.

- Whole Foods Market, Inc.

Recent Developments

- In 2024, Aurora Organic Dairy enhanced animal welfare with video monitoring at three farms and implemented group calf housing. They focus on sustainable, humane practices while producing high-quality organic dairy products for U.S. retailers, reinforcing their market leadership.

- In 2023, Arla Foods, a leading dairy cooperative, reported strong growth in the latter half of the year, achieving a total revenue of EUR 13.7 billion, closely matching the previous year’s EUR 13.8 billion. This performance enabled Arla to propose a supplementary payment of 270 million EUR to its farmer-owners.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 7.5 Billion |

| Forecast Revenue (2033) | USD 14.8 Billion |

| CAGR (2024-2033) | 7.0% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Cheddar, Hard Continental, Soft Continental, Territorials, Others), By Form (Cubes and Blocks, Slices, Spreadable, Others), By Application (Bakery Goods, Confectionery, Sauces and Dips, Rte Meals, Savory Snacks, Seasoning and Flavorings, Desserts, Others), By Distribution Channel (Specialty Stores, Modern Trade, Convenience Stores, Traditional Grocery Stores, Online store, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Danone S.A., Eden Valley Creamery, Fonterra Co-operative Group Limited, Groupe Lactalis S.A, Horizon Organic, Hormel Foods, Kerry Group plc, Organic Valley, Ornua, Safeway Inc., The Kroger Co., The WhiteWave Foods Company, Unilever N.V., Whole Foods Market, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |