Quick Navigation

Report Overview

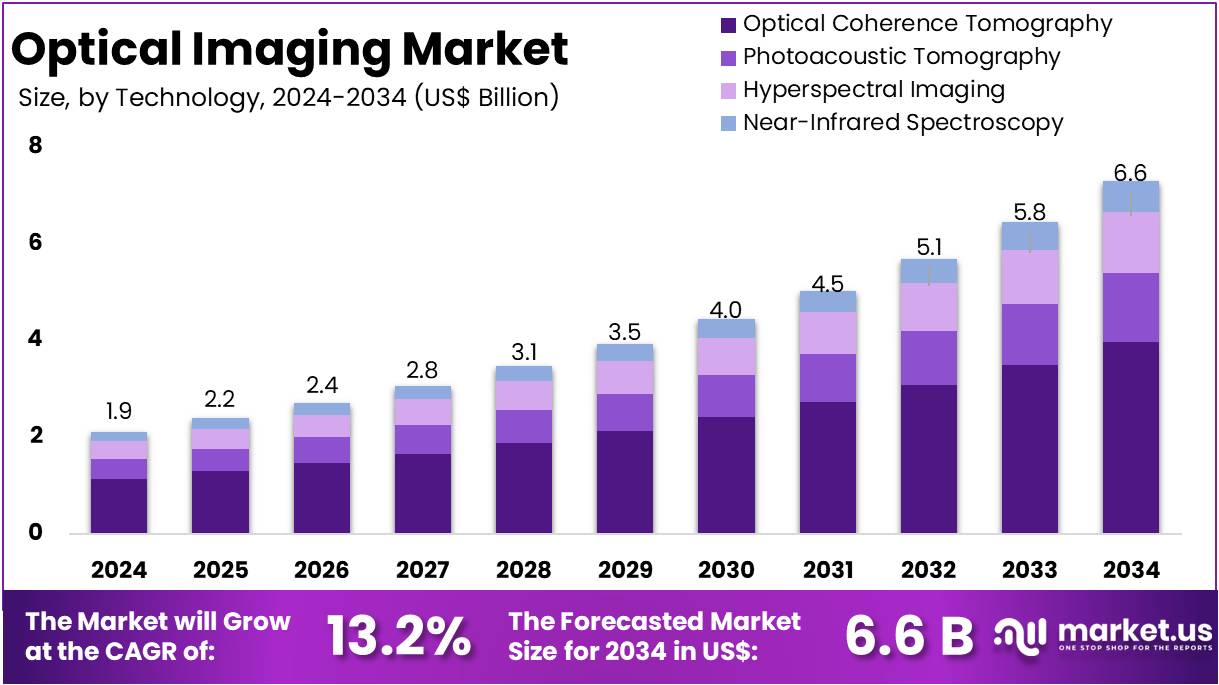

The Global Optical Imaging Market Size is expected to be worth around US$ 6.6 Billion by 2034, from US$ 1.9 Billion in 2024, growing at a CAGR of 13.2% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 36.4% share and holds US$ 0.6 Billion market value for the year.

Optical imaging is a technique that uses light, such as visible, ultraviolet, or infrared light, to capture images of objects or scenes. This method plays a crucial role in various fields like medical diagnostics, biology, material science, and astronomy. Optical imaging is non-invasive, offering high spatial resolution, which makes it ideal for visualizing biological tissues, examining materials, and conducting scientific research.

Several types of optical imaging techniques are commonly used today. For instance, light and fluorescence microscopy are widely employed in biological studies to magnify small objects. Endoscopy allows internal imaging of the body through a flexible tube with a camera, aiding non-invasive medical examinations. Optical Coherence Tomography (OCT) is often used in ophthalmology to capture high-resolution images of the retina, offering insight into eye health.

A key driver of the optical imaging market is the rising global prevalence of eye-related health issues. According to the World Health Organization (WHO), the demand for eye care is expected to grow significantly in the coming decades. This has led to an increase in the adoption of optical imaging techniques for diagnosing conditions like myopia. A study covering over five million children found that myopia prevalence rose from 24% in 1990 to 36% in recent years, with projections suggesting it will reach 40% by 2050.

Technological advancements also contribute to the growth of optical imaging. The development of sophisticated and user-friendly devices has improved diagnostic accuracy and patient outcomes. For example, the integration of optical imaging with other diagnostic tools like PET and CT scans has expanded its applications, offering better capabilities for disease detection and monitoring.

The regulatory landscape also supports the sector’s expansion. The WHO provides guidelines for the post-market surveillance of medical devices, ensuring that optical imaging technologies meet high safety and effectiveness standards. As the market grows, the ongoing improvements in optical imaging techniques and devices continue to offer enhanced diagnostic and therapeutic options for patients worldwide.

Key Takeaways

- The Global Optical Imaging market is projected to reach approximately US$ 6.6 billion by 2034, rising from US$ 1.9 billion in 2024.

- A robust compound annual growth rate (CAGR) of 13.2% is expected for the optical imaging market during the 2025 to 2034 forecast period.

- In 2024, Optical Coherence Tomography (OCT) accounted for over 60.3% of the technology segment, maintaining a leading position in optical imaging applications.

- The optical imaging systems product category held a dominant share of over 58.4% in 2024, reflecting strong demand across clinical and research settings.

- Pharmaceutical and biotechnological firms represented the leading end users in 2024, capturing more than 43.5% of the market share in that segment.

- Within therapeutic applications, oncology accounted for the largest share in 2024, contributing over 32.2% to the overall optical imaging market.

- North America led the global market in 2024 with a share exceeding 36.4%, translating to a regional market value of approximately US$ 0.6 billion.

Technology Analysis

In 2024, Optical Coherence Tomography (OCT) held a dominant market position in the Technology Segment of Optical Imaging, capturing more than a 60.3% share. This strong lead is driven by OCT’s high-resolution imaging and non-invasive nature. It is widely used in ophthalmology, cardiology, and oncology. Advances like spectral-domain and swept-source OCT have improved image clarity and speed. These factors support its increasing use in hospitals and diagnostic centers. The demand is also boosted by its role in early disease detection.

Photoacoustic Tomography (PAT) is the next promising technology in this segment. It combines optical and ultrasound imaging to offer detailed views of soft tissues. PAT is especially useful in cancer detection and brain imaging. Its adoption is rising in academic and clinical research. However, higher system costs and limited product availability have slowed commercial uptake. Despite these challenges, ongoing studies and innovation are expected to drive growth in this segment over the coming years.

Hyperspectral Imaging (HSI) and Near-Infrared Spectroscopy (NIRS) represent smaller but emerging segments. HSI enables tissue classification and surgical guidance through spectral and spatial data. It is gaining traction in neurology and dermatology. However, its complex data processing limits wider adoption. NIRS is mainly used for brain monitoring and muscle oxygenation. Its portability and non-invasive nature are key benefits. Yet, low resolution and shallow penetration restrict its clinical utility. Both segments show potential with increased research and development activities.

Product Analysis

In 2024, Optical held a dominant market position in the Product Segment of Optical Imaging, capturing more than a 58.4% share. This dominance is due to its wide usage and precise imaging capabilities. Optical components, including lenses and mirrors, are vital in various imaging systems. Their accuracy and consistency make them essential in both clinical and research settings. The demand remains strong due to their role in enhancing image quality and system performance across medical and scientific applications.

Imaging Systems held the second-largest share in 2024. These systems combine hardware and software to enable high-quality imaging. They are widely used in neurology, oncology, and surgical procedures. Real-time imaging offered by these systems supports accurate diagnosis. Spectral Imaging also saw growth. It helps capture data across different wavelengths. This feature improves tissue contrast and supports early disease detection. Its adoption is rising in drug discovery and biological research due to its precision and clarity.

Optical Imaging Software showed moderate growth in 2024. It improves image analysis and diagnostic accuracy. With AI and machine learning, software tools now offer faster and clearer results. Illumination Systems, including lasers and LEDs, are also key. They support image clarity through precise lighting. The demand is increasing for non-invasive methods. Other Products, like accessories and connectors, play a supporting role. While their share is smaller, they are essential for system integration. All segments are expected to support future market expansion.

End Use Analysis

In 2024, Pharmaceutical and Biotechnological Companies held a dominant market position in the End Use Segment of Optical Imaging, capturing more than a 43.5% share. This dominance was due to the growing use of optical imaging in drug discovery and development. These companies relied on high-resolution imaging tools for evaluating drug responses. Optical imaging helped in visualizing molecular and cellular activity with precision. The technology was also preferred for its safety, cost-efficiency, and non-invasive nature.

Hospitals and Clinics followed as the second-largest end users in the optical imaging market. Their share increased due to the rising demand for advanced diagnostic methods. Optical imaging was frequently used in oncology, cardiology, and ophthalmology. It supported early disease detection and improved surgical accuracy. Many hospitals adopted this technology to offer real-time imaging during minimally invasive procedures. Its benefits, such as fast results and high sensitivity, made it a useful tool in clinical settings.

Research Laboratories accounted for a stable share of the market. These facilities used optical imaging for basic and applied scientific research. It played a key role in fields such as neuroscience, cell biology, and genetic studies. Academic institutes and private labs invested in this technology to support innovation. Increased funding in life sciences and greater interest in imaging-based experiments supported its growth. The research segment is expected to grow further with continued advancements in imaging technologies.

Therapeutic Area Analysis

In 2024, Oncology companies held a dominant market position in the Therapeutic Area Segment of Optical Imaging, capturing more than a 32.2% share. This dominance was attributed to the rising demand for accurate cancer diagnosis and treatment monitoring. Optical imaging was widely used due to its high resolution and ability to detect tumors in early stages. Healthcare providers increasingly adopted it to improve patient outcomes. The segment continued to expand with growing research investments in oncology-specific imaging solutions.

Ophthalmology emerged as the second-largest segment within the optical imaging market. The increase in age-related eye disorders led to greater use of non-invasive imaging tools. Optical coherence tomography (OCT) remained a preferred method for retinal imaging. It provided clear and quick visualizations of eye conditions. The adoption of OCT in clinics and hospitals improved diagnostic efficiency. These developments contributed to the growth of the ophthalmology segment in therapeutic applications of optical imaging.

Neurology, dermatology, and cardiology also contributed notable shares. Optical imaging in neurology enabled the study of brain activity and vascular functions. It showed promise in diagnosing neurodegenerative diseases. Dermatology benefited from non-invasive methods for examining skin layers and detecting early signs of skin cancer. In cardiology, techniques like intravascular optical imaging supported vascular assessments. Although smaller in share, these segments are expected to grow. Technological advancements and broader clinical adoption continue to drive their expansion in the coming years.

Key Market Segments

By Technology

- Photoacoustic Tomography

- Optical Coherence Tomography

- Hyperspectral Imaging

- Near-Infrared Spectroscopy

By Product

- Imaging Systems

- Optical

- Spectral

- Optical Imaging Software

- Illumination Systems

- Other

By End Use

- Research Labs

- Hospitals & Clinics

- Pharmaceutical and Biotechnological Companies

By Therapeutic Area

- Ophthalmology

- Cardiology

- Oncology

- Dermatology

- Neurology

Drivers

Rising Prevalence Of Chronic Diseases

The rising number of chronic diseases is a major factor driving demand for advanced diagnostic tools. Conditions such as cancer, heart disease, and neurological disorders are becoming more common. These diseases often require early detection for effective treatment. As a result, healthcare providers are looking for safer, faster, and more accurate diagnostic methods. Non-invasive imaging techniques are now preferred due to reduced patient risk. The need for better diagnostic accuracy is encouraging the use of modern imaging technologies across various healthcare settings.

Optical imaging has emerged as a preferred option among non-invasive imaging tools. It offers high-resolution imaging that helps in detecting disease at an early stage. This technology uses light to view internal structures without surgery or harmful radiation. As a result, it is considered safer than traditional imaging methods. Optical imaging is especially useful in detecting tumors, vascular conditions, and brain abnormalities. Its real-time visualization further enhances its value in clinical diagnosis and treatment planning.

The demand for optical imaging continues to rise with the growing burden of chronic illnesses. Healthcare systems are focusing on technologies that offer cost-effective and early diagnostic capabilities. Optical imaging fits these needs by enabling quick and accurate insights into disease progression. It is also widely adopted in research and development, contributing to new treatment approaches. As chronic disease cases increase globally, the market for non-invasive imaging solutions is expected to witness sustained growth in the coming years.

Restraints

High Installation And Operational Costs

The adoption of advanced optical imaging systems faces a major restraint due to their high installation costs. These systems often require specialized infrastructure, trained professionals, and custom setup. Hospitals and diagnostic centers must make significant upfront investments. For many institutions, this cost becomes a deterrent. Especially in regions with limited healthcare budgets, such capital expenses are not easily justified. As a result, even with the promise of improved diagnostics, many providers delay or avoid adoption. This limits the technology’s overall reach and potential.

In addition to installation, the operational costs of optical imaging systems remain high. These systems often need regular calibration, software upgrades, and servicing. Maintenance can be costly, requiring skilled technicians and original parts. Furthermore, the consumables used in some optical systems add to ongoing expenses. This makes the long-term cost of ownership a concern. Healthcare facilities operating under tight financial constraints may find it difficult to maintain these systems efficiently. Thus, sustained usage becomes a challenge over time.

This cost barrier is particularly evident in low- and middle-income regions. In these areas, healthcare spending is often directed toward essential services. Capital-intensive technologies like advanced imaging systems are not prioritized. Governments and institutions in such regions face tough choices in allocating limited funds. As a result, adoption of these systems remains low. The benefits of early diagnosis and high-resolution imaging are not fully realized. Bridging this gap requires funding support, partnerships, and policy reforms to improve access and affordability in underserved markets.

Opportunities

Growing Integration Of AI And Machine Learning

The integration of artificial intelligence (AI) and machine learning into optical imaging systems is creating significant growth opportunities. These technologies enable advanced image processing, which improves the speed and clarity of diagnostic imaging. With faster data analysis, clinicians can make quicker and more accurate decisions. This not only enhances workflow efficiency but also reduces human error. As a result, healthcare providers are increasingly adopting AI-powered imaging tools. This trend is particularly strong in hospitals and diagnostic labs focused on precision medicine.

AI and machine learning are also transforming how imaging data is interpreted. Algorithms can identify patterns and anomalies that might be missed by human eyes. This supports early disease detection and helps doctors provide targeted treatments. Additionally, automated reporting features are making diagnostics more consistent. The increased reliability and reproducibility of results are encouraging adoption in research and academic institutions. These advancements are pushing the optical imaging market toward more data-driven and technology-based solutions.

The growing demand for efficiency in healthcare systems is further supporting AI integration. Optical imaging solutions with built-in AI can streamline diagnostics and reduce workload for clinicians. This benefit is critical as global healthcare systems face resource constraints. As more vendors incorporate machine learning features, product offerings are becoming more competitive. In turn, this is driving innovation and investment in the sector. The enhanced capabilities and broader applications of AI-enhanced imaging are expected to fuel long-term market growth.

Trends

Shift Toward Multimodal Imaging Systems

A significant trend in the medical imaging field is the shift toward multimodal imaging systems. These systems integrate optical imaging with other established modalities such as MRI, PET, or CT. The aim is to enhance diagnostic capabilities by combining the unique advantages of each technology. Optical imaging offers high sensitivity, while MRI, PET, and CT provide deeper tissue penetration and anatomical detail. Together, they deliver more accurate results. This approach is gaining traction in clinical research and diagnostic applications for complex diseases.

Multimodal imaging is gaining importance due to its ability to provide comprehensive insights into disease pathology. For example, optical imaging can detect cellular activity, while MRI reveals structural changes in tissues. PET adds functional data, and CT highlights bone and organ structure. When combined, these techniques improve disease detection and treatment planning. This fusion enables clinicians to see both molecular and anatomical changes. As a result, diagnosis becomes more reliable and precise, especially in cancer, neurology, and cardiovascular diseases.

The adoption of multimodal imaging is also supported by advancements in imaging software and hardware integration. These improvements make it easier to align and interpret data from multiple imaging sources. Additionally, such systems reduce the need for repeated scans, lowering patient exposure to radiation and streamlining clinical workflows. As technology advances, the cost-effectiveness and accessibility of these systems are expected to improve. This shift represents a promising step toward personalized medicine, where treatments are tailored using detailed, multi-dimensional diagnostic information.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 36.4% share and holds US$ 0.6 billion market value for the year. The region’s growth is supported by early adoption of optical imaging technologies. These include applications in healthcare, research, and industry. Hospitals and clinics in the U.S. and Canada use non-invasive imaging tools for diagnosis. Advanced infrastructure and skilled professionals have made adoption easier. High demand for precision diagnostics has further driven regional market growth.

Government initiatives and research funding have played a crucial role. Academic institutions across North America are investing in optical imaging systems. This has improved innovation and encouraged clinical use. Many organizations focus on early disease detection, particularly for cancer and neurological disorders. Optical imaging allows for detailed, real-time insights. It also reduces the need for invasive procedures. These advantages have made the technology popular in both research and clinical settings.

The presence of key manufacturers enhances regional competitiveness. Companies continue to launch advanced products that meet medical and industrial needs. The U.S. market benefits from strong regulatory support and healthcare spending. These factors speed up the approval and use of new technologies. There is also a growing patient demand for efficient diagnostics. North America’s ability to combine innovation with practical application ensures continued growth. As a result, the region is likely to maintain its leadership in the global optical imaging market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global optical imaging market includes several key players contributing to innovation and competition. Abbott is a major player, known for its strong presence in cardiovascular and diagnostic imaging. The company focuses on optical coherence tomography (OCT), especially in cardiology. Continued investments in clinical research and expanding imaging solutions have helped strengthen Abbott’s market position. Its integration of OCT into broader diagnostic offerings supports global reach and reliability. These strategic efforts make Abbott a key contributor to the overall growth of the optical imaging sector.

PerkinElmer Inc. plays an important role with its wide range of imaging systems. The company offers preclinical, fluorescence, and molecular imaging platforms. Strategic acquisitions and partnerships have helped expand its capabilities in research and clinical diagnostics. PerkinElmer focuses heavily on life science applications and translational research. These areas are significant growth drivers. The company’s efforts to support precision medicine and early disease detection further improve its relevance in the market. Its diverse imaging solutions contribute significantly to market competitiveness.

Carl Zeiss Meditec AG holds a strong position in ophthalmic imaging. It is a leader in optical coherence tomography systems. The company enables early detection and monitoring of eye diseases. It invests heavily in research and development and incorporates artificial intelligence (AI) into its imaging solutions. These advances improve diagnostic accuracy and workflow efficiency. Zeiss’s strong presence in ophthalmology supports its global market share. The company’s innovation-driven approach ensures continued relevance and leadership in the optical imaging sector.

Koninklijke Philips N.V. and TOPCON CORPORATION are also leading contributors. Philips offers integrated imaging technologies across multiple clinical applications. Its digital transformation strategy and collaborations with healthcare institutions support its role in optical imaging. TOPCON focuses on advanced ophthalmic diagnostic tools. It integrates digital imaging and AI to enhance its product line. Both companies benefit from global networks and strategic partnerships. Additional players, including Canon Inc. and Optovue Inc., contribute through niche technologies. This broad participation strengthens the industry’s innovation and competitive landscape.

Market Key Players

- Abbott

- PerkinElmer Inc.

- Carl Zeiss Meditec AG

- Koninklijke Philips N.V.

- TOPCON CORPORATION

- Leica Microsystems

- Canon Inc.

- Heidelberg Engineering GmbH

- Optovue Corporation

- Headwall Photonics

Recent Developments

- In October 2023: Abbott introduced its new vascular imaging platform powered by Ultreon 1.0 Software in India. This innovative software merges optical coherence tomography (OCT) with artificial intelligence (AI), providing high-definition imaging from within blood vessels. The platform enhances precision in coronary stenting procedures by differentiating between calcified and non-calcified blockages, measuring vessel diameter, and optimizing stent deployment. It allows physicians to make better treatment decisions and reduces procedural variability.

- In August 2024: Topcon received U.S. FDA certification for its Maestro 2 Optical Coherence Tomography (OCT)-Angiography system. This fully automated system enables non-invasive visualization of blood vessels without requiring drug injections, reducing patient burden. The certification allows Topcon to expand its user base, including optical chain stores and ophthalmologists, further promoting its screening equipment in North America.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 1.9 Billion |

| Forecast Revenue (2034) | US$ 6.6 Billion |

| CAGR (2025-2034) | 13.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Photoacoustic Tomography, Optical Coherence Tomography, Hyperspectral Imaging, Near-Infrared Spectroscopy), By Product (Imaging Systems, Optical, Spectral, Optical Imaging Software, Illumination Systems, Other), By End Use (Research Labs, Hospitals & Clinics, Pharmaceutical and Biotechnological Companies), By Therapeutic Area (Ophthalmology, Cardiology, Oncology, Dermatology, Neurology) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Abbott, PerkinElmer Inc., Carl Zeiss Meditec AG, Koninklijke Philips N.V., TOPCON CORPORATION, Leica Microsystems, Canon Inc., Heidelberg Engineering GmbH, Optovue Corporation, Headwall Photonics |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |