Quick Navigation

Report Overview

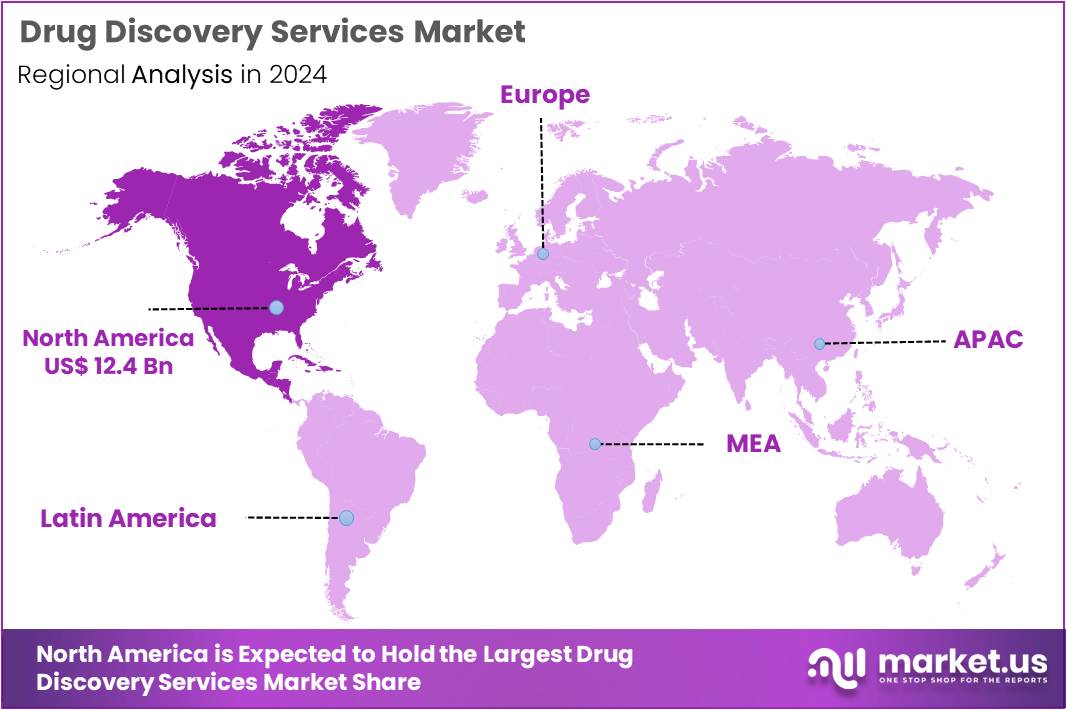

The Global Drug Discovery Services Market Size is expected to be worth around US$ 70.3 Billion by 2034, from US$ 27.4 Billion in 2024, growing at a CAGR of 9.9% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 45.2% share and holds US$ 12.4 Billion market value for the year.

The global drug discovery services market has witnessed significant growth over recent years, driven by increasing demand for new therapeutic solutions and the rising prevalence of chronic diseases, including cancer, diabetes, and neurological disorders.

- In 2020, the International Agency for Research on Cancer (IARC) estimated that there were approximately 19.3 million new cancer cases and 10 million cancer-related deaths worldwide.

- By 2022, approximately 828 million adults worldwide were living with diabetes, representing 14% of the adult population. The highest prevalence rates are observed in regions such as the Pacific Islands, the Caribbean, the Middle East, North Africa, Pakistan, and Malaysia. India, China, and the United States have the largest number of individuals with diabetes.

- In 2021, more than 3 billion people globally were living with a neurological condition, accounting for 43% of the world’s population. The most prevalent neurological disorders include tension headaches (approximately 2 billion cases) and migraines (about 1.1 billion cases).

Drug discovery services encompass a range of activities, from early-stage research to preclinical and clinical trials, aiding pharmaceutical and biotechnology companies in developing novel drugs. These services are provided by specialized contract research organizations (CROs), academic institutions, and in-house teams within pharmaceutical companies.

The market is fueled by the growing need for efficient, cost-effective, and faster drug development processes. With the complexities involved in discovering and developing new drugs, companies often outsource their drug discovery services to benefit from the expertise of CROs and reduce overhead costs. Key services include drug screening, hit identification, lead optimization, in vitro and in vivo testing, bioinformatics, and medicinal chemistry. These services are critical in ensuring that only the most promising drug candidates proceed to clinical trials.

Technological advancements have played a pivotal role in shaping the landscape of the drug discovery services market. High-throughput screening (HTS), artificial intelligence (AI), and machine learning (ML) technologies have revolutionized the drug discovery process, improving the accuracy and efficiency of identifying drug candidates. Furthermore, the integration of bioinformatics and computational chemistry tools has enhanced the drug design process, enabling more precise targeting of specific diseases.

Geographically, North America holds a dominant position in the drug discovery services market, primarily due to the presence of leading pharmaceutical companies, robust healthcare infrastructure, and significant investments in R&D. Europe and Asia-Pacific are also witnessing rapid growth, driven by expanding pharmaceutical industries in countries like China and India, where the availability of skilled labor and cost-effective services attracts global clients.

The global drug discovery services market is also characterized by increasing collaborations between pharmaceutical companies and CROs. Partnerships help expedite the drug discovery process while minimizing costs and improving the success rate of drug development. With the growing complexity of diseases and the need for personalized medicine, the demand for specialized drug discovery services is expected to continue rising.

Global Drug Discovery Services, Global Analysis, 2020-2024 (US$ Billion)

| Global | 2020 | 2021 | 2022 | 2023 | 2024 | CAGR |

|---|---|---|---|---|---|---|

| Revenue | 17.12 | 20.05 | 23.08 | 25.13 | 27.41 | 9.9% |

Key Takeaways

- The Drug Discovery Services market generated a revenue of US$ 27.4 Billion and is predicted to reach US$ 70.3 Billion, with a CAGR of 9.9%.

- Based on the Process, the Lead Optimization segment generated the most revenue for the market with a market share of 29.9%.

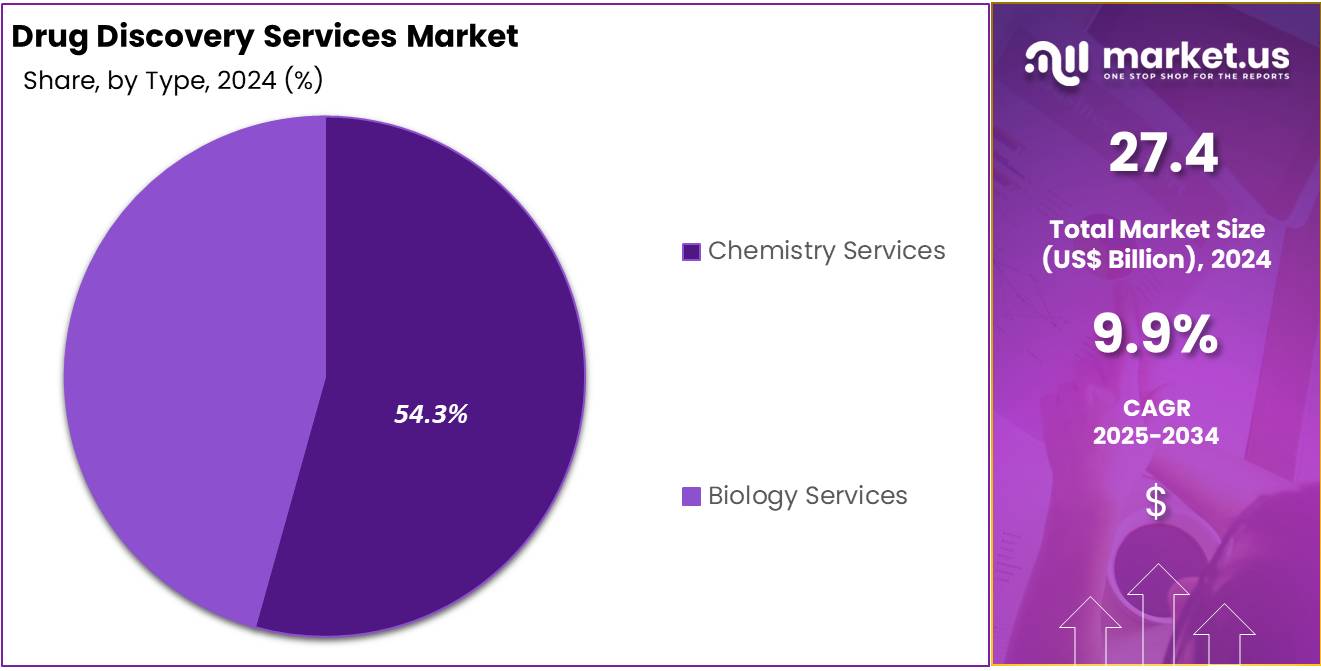

- Based on the Type, the Chemistry Services segment generated the most revenue for the market with a market share of 54.3%.

- Based on the Drug Type, the Small Molecule Drugs segment generated the most revenue for the market with a market share of 60.6%.

- Based on the Therapeutic Area, the Oncology segment generated the most revenue for the market with a market share of 43.1%.

- Based on the End-User, the Pharmaceutical and Biotechnology Companies segment generated the most revenue for the market with a market share of 58.3%.

- Region-wise, North America remained the lead contributor to the market, by claiming the highest market share, amounting to 45.2%.

Process Analysis

In 2024, The Lead Optimization segment dominated the process segment and has garnered 29.9% of segmental share, registering a CAGR of 9.7% during the forecast period. Lead optimization is a critical phase in the drug discovery process where lead compounds are refined to enhance therapeutic efficacy and reduce unwanted side effects. This stage focuses on improving drug candidates to ensure they effectively target the disease while maintaining acceptable safety profiles and favorable pharmacokinetic and pharmacodynamic characteristics.

Pharmacokinetics (PK) involves the study of a drug’s absorption, distribution, metabolism, and excretion in the body. Optimizing PK properties ensures that the drug reaches the intended site of action in sufficient concentrations, sustains its effectiveness over time, and is safely eliminated without causing toxicity. Pharmacodynamics (PD), which examines the drug’s biological effects and mechanism of action, is optimized to establish the dose-response relationship, helping to determine the effective drug dosage.

Global Drug Discovery Services, by Process Analysis, 2020-2024 (US$ Billion)

| Process | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Target Selection | 3.23 | 3.77 | 4.33 | 4.69 | 5.10 |

| Target Validation | 2.64 | 3.08 | 3.52 | 3.81 | 4.13 |

| Hit-To-LeadIdentification | 3.77 | 4.47 | 5.20 | 5.72 | 6.31 |

| Lead Optimization | 5.16 | 6.03 | 6.93 | 7.53 | 8.20 |

| Candidate Validation | 2.31 | 2.70 | 3.10 | 3.37 | 3.66 |

Type Analysis

In 2024, the Chemistry Services segment held a dominant market position in the Type Segment of the Drug Discovery Services Market, capturing more than a 54.3% share.

The Chemistry Services segment held a dominant position in the type category of the global drug discovery services market, driven by its critical role in the early stages of drug development. This segment encompasses a range of activities, including hit identification, lead generation, and lead optimization, which are essential for identifying and refining potential drug candidates. Advances in computational chemistry, high-throughput screening, and structure-based drug design have further bolstered the efficiency and accuracy of these services, making them indispensable to pharmaceutical and biotech companies.

The increasing complexity of drug discovery processes and the growing demand for specialized expertise have led companies to outsource chemistry services to contract research organizations (CROs). These organizations provide access to advanced technologies, skilled professionals, and cost-effective solutions. Additionally, the rise of personalized medicine and the need for novel therapies have further fueled the demand for chemistry services, solidifying their dominance in the drug discovery services market.

Global Drug Discovery Services, by Type Analysis, 2020-2024 (US$ Billion)

| Type | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Chemistry Services | 9.38 | 10.96 | 12.59 | 13.68 | 14.90 |

| Biology Services | 7.74 | 9.09 | 10.49 | 11.45 | 12.51 |

Drug Type Analysis

In 2024, the small molecule drugs segment dominated the drug type category in the global drug discovery services market, capturing a significant 60.6% market share. Small molecule drugs are widely preferred due to their well-established role in treating a broad range of diseases, their ease of administration (often orally), and their ability to target intracellular pathways effectively. These drugs are generally cost-effective to produce and have a long history of successful development, making them attractive to pharmaceutical companies.

The dominance of small molecule drugs is also attributed to advancements in computational chemistry and structure-based drug design, which have significantly improved the efficiency of identifying and optimizing these compounds. Additionally, their relatively small size enables better absorption and distribution in the body, making them highly versatile across therapeutic applications. Despite the growing interest in biologics, the proven track record, scalability, and diverse applications of small molecule drugs continue to drive their leadership in the market.

Global Drug Discovery Services, by Drug Type Analysis, 2020-2024 (US$ Billion)

| Drug Type | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Small Molecule Drugs | 10.53 | 12.29 | 14.09 | 15.29 | 16.61 |

| Biologics Drug | 6.59 | 7.76 | 8.99 | 9.84 | 10.80 |

Therapeutic Area Analysis

In 2024, the oncology segment held a dominant market position in the Therapeutic Area Segment of the Drug Discovery Services Market, capturing more than a 43.1% share. The oncology segment leads the therapeutic area category in the drug discovery services market, driven by the rising global burden of cancer and the urgent need for innovative therapies.

Cancer remains a leading cause of morbidity and mortality worldwide, prompting pharmaceutical and biotech companies to prioritize oncology in their R&D efforts. Advances in targeted therapies, immunotherapies, and personalized medicine have further spurred growth in this segment, making it a focal point for drug discovery services.

The high prevalence of various cancers, coupled with increasing investments in cancer research, has created a strong demand for specialized drug discovery platforms. Contract research organizations (CROs) play a pivotal role by providing advanced technologies, such as high-throughput screening and biomarker identification, to accelerate the development of oncology drugs. Additionally, supportive regulatory frameworks, along with funding from governmental and private entities, contribute to the dominance of oncology within the therapeutic area segment.

Global Drug Discovery Services, by Therapeutic Area Analysis, 2020-2024 (US$ Billion)

| Therapeutic Area | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Oncology | 7.26 | 8.54 | 9.87 | 10.79 | 11.82 |

| Neurological Diseases | 3.10 | 3.64 | 4.20 | 4.59 | 5.02 |

| Cardiovascular Diseases | 1.72 | 2.02 | 2.33 | 2.53 | 2.77 |

| Respiratory Diseases | 0.89 | 1.04 | 1.18 | 1.28 | 1.39 |

| Digestive System Diseases | 0.59 | 0.68 | 0.77 | 0.83 | 0.89 |

| Others | 3.55 | 4.13 | 4.72 | 5.10 | 5.52 |

End-User Analysis

In 2024, the Pharmaceutical and Biotechnology segment held a dominant market position in the End-User Segment of the Drug Discovery Services Market, capturing more than a 58.3% share. Pharmaceutical and biotechnology companies dominate the end-user segment of the global drug discovery services market due to their extensive involvement in the development of new therapies.

These companies rely on drug discovery services to identify potential drug candidates, conduct preclinical studies, and optimize drug formulations. The increasing demand for novel treatments, especially for chronic and complex diseases, has fueled investments in drug discovery. Additionally, the rise in collaborations between biotech firms and contract research organizations (CROs) enables pharmaceutical companies to access specialized expertise, technologies, and resources, further strengthening their position in the market.

Global Drug Discovery Services, by End-User Analysis, 2020-2024 (US$ Billion)

| End-User | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Pharmaceutical and Biotechnology Companies | 9.96 | 11.67 | 13.44 | 14.65 | 15.99 |

| Clinical Laboratories | 3.94 | 4.61 | 5.31 | 5.78 | 6.30 |

| Academic and Research Institutes | 3.22 | 3.77 | 4.33 | 4.70 | 5.12 |

Key Market Segments

By Process

- Target Selection

- Target Validation

- Hit-To-LeadIdentification

- Lead Optimization

- Candidate Validation

By Type

- Chemistry Services

- Biology Services

By Drug Type

- Small Molecule Drugs

- Biologics Drug

By Therapeutic Area

- Oncology

- Neurological Diseases

- Cardiovascular Diseases

- Respiratory Diseases

- Digestive System Diseases

- Others

By End-User

- Pharmaceutical and Biotechnology Companies

- Clinical Laboratories

- Academic and Research Institutes

Drivers

Increase in Research and Development Expenditure

The growing trend of increased investment in research and development (R&D) by pharmaceutical and biotechnology companies is a key driver propelling the growth of the global drug discovery services market. As these companies seek to develop new drug candidates to address unmet medical needs and maintain a competitive edge, they often require specialized expertise and access to advanced technologies.

This demand frequently surpasses the in-house capabilities of many firms, particularly smaller ones or those entering new therapeutic areas, making external services from contract research organizations (CROs) and other specialized providers indispensable. To leverage external expertise and cutting-edge technologies without incurring substantial capital expenditure, many pharmaceutical companies form strategic collaborations and partnerships with these service providers.

- In February 2023, Exscientia plc announced that EXS4318 (‘4318), a compound precision-designed by Exscientia and in-licensed by Bristol Myers Squibb in August 2021, entered Phase 1 clinical trials in the United States. The compound is being developed for immunology and inflammation (I&I) indications.

Additionally, the global expansion of pharmaceutical companies into emerging markets further intensifies the demand for drug discovery services. These markets offer new opportunities but also present challenges, such as diverse regulatory environments and market conditions. As a result, the role of service providers in ensuring regulatory compliance and facilitating market entry becomes even more vital.

According to the National Center for Science and Engineering Statistics, U.S. R&D spending saw a $72 billion increase in 2021, reaching $789 billion. Projections for 2022 suggested a further rise to $886 billion. Major pharmaceutical companies such as Pfizer and Roche have continuously expanded their R&D budgets to explore new drugs and therapeutic areas.

In 2022, Pfizer alone allocated around $10 billion to its R&D activities, underscoring its strong commitment to advancing its drug development pipeline. The increasing complexity of modern drug discovery, involving cutting-edge technologies such as CRISPR for gene editing, AI for predictive modeling, and advanced biotechnological methods, demands significant financial investment..

Restrains

High Cost and Stringent Regulations in Drug Discovery

Discovering and developing a new drug is an expensive and complex undertaking, presenting significant barriers to entry, particularly for smaller companies and startups. The entire process, from initial discovery to market approval, can span over a decade and often requires substantial financial investment, sometimes surpassing $1 billion. These high costs and lengthy timelines are primarily due to the intricate and rigorous stages of drug development, which include discovery, preclinical testing, clinical trials, and regulatory approval.

In the early drug discovery phase, researchers identify potential drug candidates based on specific biological and pharmacological properties. This phase is particularly expensive, involving high-throughput screening, computational biology, and extensive laboratory research to identify effective compounds. For biotech startups, this stage can consume millions of dollars without any guarantee that a candidate will advance to the next phase.

After discovery, the preclinical testing phase involves laboratory and animal studies to assess the safety and efficacy of drug candidates. This phase is essential but costly, as it requires specialized facilities and adherence to regulatory standards. Smaller companies often face financial challenges during this stage, as they may lack the resources that larger pharmaceutical firms typically have to support such studies. Clinical trials, which involve testing the drug on humans, are divided into three phases and make up the most significant portion of drug development costs.

Each phase must achieve specific milestones before progressing to the next, with Phase III being especially extensive and expensive. For instance, conducting large-scale, randomized controlled trials to demonstrate a drug’s safety and effectiveness can cost hundreds of millions of dollars. Startups often struggle at this point, as they may not have sufficient capital to cover these expenses and may need to seek additional funding or form strategic partnerships.

The final hurdle is securing regulatory approval from authorities like the U.S. Food and Drug Administration (FDA) or the European Medicines Agency (EMA). This process involves submitting comprehensive trial data and ensuring compliance with stringent regulatory requirements, making it financially and operationally prohibitive for smaller companies.

A prime example of these challenges is Vertex Pharmaceuticals’ development of Kalydeco, a treatment for cystic fibrosis. Vertex invested years of research and significant funds, collaborating with the Cystic Fibrosis Foundation to bring Kalydeco to market. Such an achievement would be extremely difficult for smaller startups without access to similar resources and support.

Opportunities

Emergence of Artificial Intelligence

The integration of Artificial Intelligence (AI) and machine learning into drug discovery is transforming the pharmaceutical industry by accelerating research and improving the accuracy of predictions regarding drug efficacy and safety. These technologies are addressing long-standing challenges in pharmaceutical R&D, including high failure rates, significant costs, and lengthy development cycles.

AI and machine learning excel at analyzing vast datasets more efficiently than traditional methods, uncovering insights often missed by human researchers. This capability is instrumental in identifying potential drug candidates, predicting interactions with the human body, and anticipating side effects early in development. This accelerates the discovery phase while enhancing safety profiles before clinical trials. For example, Atomwise leverages deep learning technology, AtomNet, to predict molecule behavior against targets, enabling rapid identification of promising compounds for diseases like Ebola, significantly reducing time and costs.

AI also optimizes clinical trial design and patient recruitment. Companies like Deep 6 AI use machine learning to analyze extensive clinical data from electronic medical records, identifying suitable trial candidates more efficiently. In September 2023, Deep 6 AI introduced a genomics module to accelerate enrollment in precision medicine and oncology research. This software scans genomics data from electronic medical records and genetic reports to pinpoint patients with specific genetic markers in real-time, enhancing precision and trial efficiency.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the drug discovery services market, shaping its growth and dynamics. Economic fluctuations impact R&D budgets, with tighter financial conditions potentially curbing investments in innovative drug discovery initiatives. Inflation and rising operational costs further pressure service providers, leading to increased pricing or reduced margins.

Geopolitical tensions can disrupt global supply chains for raw materials, laboratory equipment, and biological reagents, delaying projects and escalating costs. For instance, trade restrictions or tariffs on key materials can hinder the smooth execution of drug discovery programs. Additionally, shifting geopolitical alliances and regulations influence cross-border collaborations and clinical trials, complicating global operations.

On the positive side, government initiatives in response to public health crises, such as increased funding for pandemic-related drug development, spur market growth. Similarly, geopolitical stability in key regions fosters international partnerships and outsourcing opportunities, enabling companies to leverage specialized expertise and cost efficiencies globally.

Trends

The global drug discovery services market is evolving rapidly, driven by advancements in technology and shifting industry demands. The integration of artificial intelligence (AI) and machine learning is streamlining drug discovery processes, enabling faster and more precise identification of drug candidates while reducing costs.

Outsourcing trends are rising, with pharmaceutical companies partnering with specialized service providers to leverage cutting-edge tools and expertise, optimizing R&D timelines. The increasing focus on personalized medicine is another notable trend, emphasizing the development of targeted therapies based on individual genetic profiles, which necessitates advanced biomarker discovery and validation services.

Additionally, the market is expanding into emerging economies, where growing healthcare infrastructure and demand for innovative treatments create new growth opportunities. Despite challenges like regulatory complexities and high costs, these trends highlight the market’s dynamic nature, fostering innovation and driving its expansion to address unmet medical needs globally.

Regional Analysis

North America Dominates the Global Drug Discovery Services Market

In 2024, North America accounted for a significant 45.2% share of the global drug discovery services market, driven by a robust pharmaceutical infrastructure, substantial investments in biomedical research, and a favorable legal and regulatory environment supporting innovation.

The region’s pharmaceutical sector is among the largest and most dynamic globally, hosting major players like Pfizer, Merck, and Johnson & Johnson. These industry leaders not only drive internal drug discovery efforts but also create demand for external services through collaborations with biotech firms and contract research organizations (CROs). The ecosystem is further bolstered by emerging biotech startups in innovation hubs such as Boston, San Francisco, and San Diego, which focus on advanced technologies like CRISPR, monoclonal antibodies, and mRNA therapies.

Government support, particularly from the National Institutes of Health (NIH), plays a pivotal role, funding early-stage research and facilitating breakthroughs in areas such as gene therapy and personalized medicine. Additionally, the FDA’s initiatives, such as Fast Track and Breakthrough Therapy designations, expedite drug development for critical unmet medical needs.

A strong intellectual property (IP) framework in the U.S. incentivizes investment by providing robust patent protection for new discoveries. Furthermore, the U.S. leads globally in clinical trials, with 168,520 registered between 1999 and 2022, underscoring its dominance in advancing drug discovery and development.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global drug discovery services market is highly competitive, driven by the presence of established players and emerging companies. Major contract research organizations (CROs) like Charles River Laboratories, Labcorp Drug Development, WuXi AppTec, and Evotec dominate the market, offering a comprehensive range of services across various stages of drug discovery.

These companies leverage cutting-edge technologies, such as artificial intelligence (AI) and advanced screening tools, to enhance efficiency and attract partnerships with pharmaceutical and biotech firms. Smaller, specialized providers also contribute to the landscape by focusing on niche areas such as high-throughput screening, biomarker discovery, and computational chemistry.

Regional players in emerging markets, particularly in Asia-Pacific, are gaining prominence by offering cost-effective solutions and tapping into local talent pools. Strategic collaborations, mergers, and acquisitions are common, enabling companies to expand their service portfolios and geographical presence. This dynamic environment fosters innovation and competitive growth in the drug discovery services sector.

Top Key Players in the Drug Discovery Services Market

- Thermo Fisher Scientific Inc.

- EVOTEC SE

- Laboratory Corporation of America Holdings

- WuXi AppTec Co., Ltd.

- Charles River Laboratories

- Dalton Pharma Services

- Eurofins Discovery

- Syngene International Limited

- GenScript ProBio

- Domainex Ltd.

Recent Developments

- In November 2023, Evotec and Bayer announced a new strategic collaboration aimed at accelerating the discovery and development of drugs across multiple therapeutic areas. As part of the agreement, Evotec will grant Bayer access to its integrated drug discovery platform, encompassing expertise in target identification and validation, hit-to-lead and lead optimization, and preclinical development.

- In 2020, PharmaResources and Eurofins formed a partnership to establish a drug discovery platform focused on developing small molecule drugs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 27.4 Billion |

| Forecast Revenue (2033) | US$ 70.3 Billion |

| CAGR (2024-2033) | 9.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2019-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Process- Target Selection, Target Validation, Hit-To-Lead Identification, Lead Optimization and Candidate Validation, By Type- Chemistry Services and Biology Services, By Drug Type- Small Molecule Drugs and Biologics Drug, By Therapeutic Area- Oncology, Neurological Diseases, Cardiovascular Diseases, Respiratory Diseases, Digestive System Diseases and Others, By End-User- Pharmaceutical and Biotechnology Companies, Clinical Laboratories and Academic and Research Institutes. |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Thermo Fisher Scientific Inc., EVOTEC SE, Laboratory Corporation of America Holdings, WuXi AppTec Co., Ltd., Charles River Laboratories, Dalton Pharma Services, Eurofins Discovery, Syngene International Limited, GenScript ProBio and Domainex Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |