Quick Navigation

Report Overview

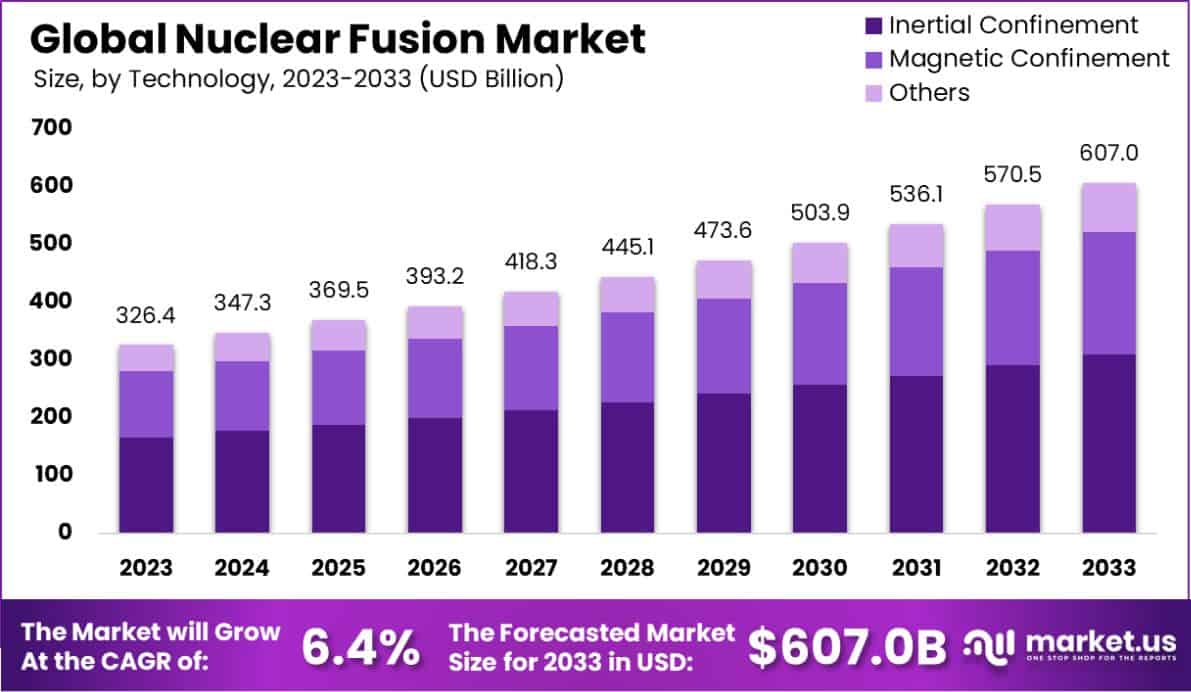

The Global Nuclear Fusion Market size is expected to be worth around USD 607.0 Bn by 2033, from USD 326.4 Bn in 2023, growing at a CAGR of 6.4% during the forecast period from 2024 to 2033.

Nuclear fusion is a process where two light atomic nuclei combine to form a heavier nucleus, releasing energy. This process is fundamental to the operation of the sun and stars and represents a potential source of nearly limitless and clean energy on Earth, should the technical challenges of controlling it be overcome.

The nuclear fusion market refers to the economic landscape surrounding the technologies and services associated with the development and potential commercialization of nuclear fusion energy. It includes investments in research and development, fusion reactor projects, and related engineering and technological services.

The nuclear fusion market is poised at a pivotal juncture with significant growth potential and substantial investments steering its trajectory. Nuclear energy, contributing approximately 9% to global electricity production and generating around 2602 TWh in 2023 through 440 operational reactors, underscores a robust foundation for low-carbon energy sources.

This established nuclear sector complements the burgeoning interest and advancements in nuclear fusion technology.

In 2023, the U.S. Congress underscored its commitment to fusion research by appropriating substantial funds, notably approving $630 million for Inertial Confinement Fusion research, with at least $380 million allocated to the National Ignition Facility (NIF).

Furthermore, the U.S. Department of Energy enhanced its investment in Fusion Energy Sciences, earmarking $763 million—an increase of $50 million from the previous year. This funding is intended to support a range of initiatives, including critical research at NIF.

However, the allocation falls short of the authorized $1.025 billion, highlighting a gap that may represent both a challenge and an opportunity for stakeholders. The continued financial backing is crucial as it fosters innovation and accelerates the development of fusion technologies which promise to revolutionize energy systems with high-output, low-emission power solutions.

The market for nuclear fusion, therefore, stands as a dynamic sector with transformative potential, demanding focused investment and international cooperation to unlock its full capacity and achieve commercial viability.

The growth of the nuclear fusion market can be attributed to increasing energy demands and the need for sustainable and clean energy solutions. Technological advancements in plasma physics and magnetic confinement are essential drivers, accelerating research and experimental projects.

Demand in the nuclear fusion market is driven by governmental and private sector funding aimed at mitigating climate change through the development of clean energy technologies. This demand is bolstered by international collaborations, such as the ITER project, which aims to make fusion energy viable.

The market presents opportunities in the advancement of materials technology that can withstand extreme conditions within reactors, as well as in the development of efficient and scalable fusion reactor designs. Successful commercialization of fusion energy could transform energy grids worldwide with high-output, low-emission power solutions.

Key Takeaways

- The Global Nuclear Fusion Market size is expected to be worth around USD 607.0 Bn by 2033, from USD 326.4 Bn in 2023, growing at a CAGR of 6.4% during the forecast period from 2024 to 2033.

- Magnetic confinement dominates the Nuclear Fusion Market with a 51.2% share, reflecting its widespread adoption.

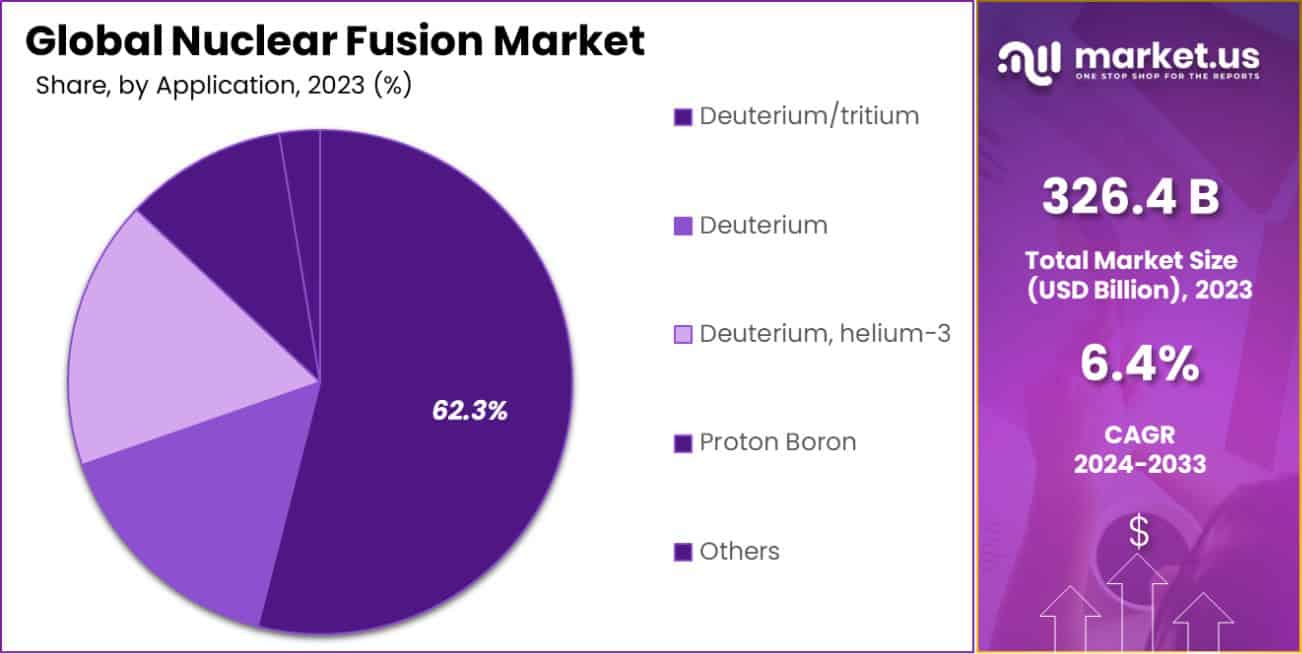

- Deuterium/Tritium is the leading fuel choice in the Nuclear Fusion Market, holding a 62.3% share.

- Electricity generation is the primary application in the Nuclear Fusion Market, capturing 72.3% of the market.

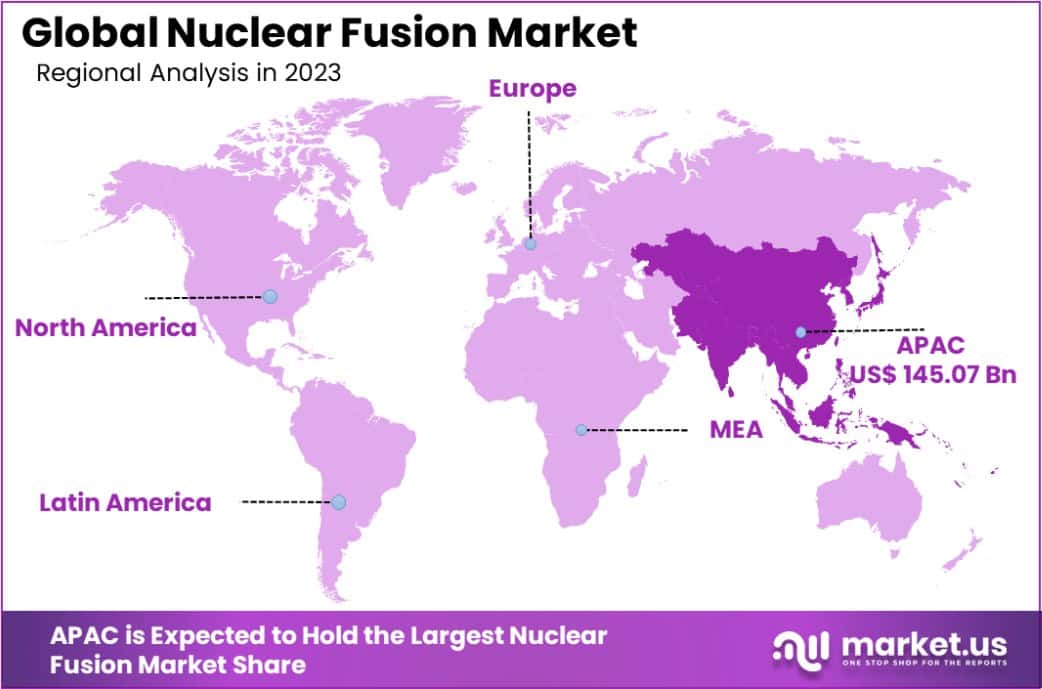

- The Asia Pacific nuclear fusion market holds a 44.5% share, valued at USD 145.07 billion, indicating robust regional growth.

By Technology Analysis

Magnetic confinement dominates with 51.2% due to its efficiency in containing high-energy plasma stably.

In 2023, Magnetic Confinement held a dominant market position in the “By Technology” segment of the Nuclear Fusion Market, commanding a 51.2% share. This technology, pivotal in the sustained development of fusion reactions, outperformed its counterpart, Inertial Confinement, which captured the remaining market share.

Magnetic Confinement Fusion (MCF) technology, leveraging strong magnetic fields to confine plasma, is central to advancing nuclear fusion as a viable energy source. Its prominence is attributed to its potential for steady and controlled energy output, making it a focal point for significant investments and research.

In contrast, Inertial Confinement, which utilizes high-energy lasers or ion beams to compress fuel to extreme densities and temperatures, accounted for a smaller portion of the market.

Although it plays a crucial role in fusion research, particularly in the pursuit of achieving ignition and net energy gain, Magnetic Confinement has gained more traction due to its scalability and the progress in projects like ITER and tokamak-based reactors.

The distribution of market shares highlights the strategic priorities within the nuclear fusion sector, where Magnetic Confinement stands as the cornerstone for future developments, aiming to harness cleaner and virtually limitless energy.

This segment’s dynamics are critical for stakeholders to understand the evolving landscape and investment potential within the broader energy market.

By Fuels Analysis

Deuterium/Tritium fuels lead at 62.3%, favored for their abundant availability and high fusion power output.

In 2023, Deuterium/Tritium held a dominant market position in the “By Fuels” segment of the Nuclear Fusion Market, with a 62.3% share. This fuel combination is the most widely used in nuclear fusion research due to its relatively lower ignition temperature and higher cross-section for fusion reactions compared to other isotopes.

Its dominance underscores the focus on achieving practical and efficient energy production, with significant advancements made in reactor design and containment methods.

Other fuels like pure Deuterium, Deuterium combined with Helium-3, and Proton Boron, while promising, captured smaller segments of the market. Pure Deuterium is explored for its abundance and safety but faces challenges in achieving the conditions necessary for fusion.

Deuterium and Helium-3, known for producing less radioactive waste, represent a future-oriented approach but are limited by the current scarcity of Helium-3. Proton Boron, despite its appeal of generating no neutrons and hence no radioactivity, remains in the experimental stages due to the high temperatures required for fusion.

The prioritization of Deuterium/Tritium in the current market landscape is driven by the goal of developing commercially viable fusion power. As technologies evolve and new fuel sources become more practical, the market shares are expected to shift, reflecting advancements and efficiencies in fusion energy production.

By Application Analysis

Electricity generation leads applications at 72.3%, showing the potential to significantly contribute to clean energy solutions.

In 2023, Electricity Generation held a dominant market position in the “By Application” segment of the Nuclear Fusion Market, with a 72.3% share. This application underscores the central goal of nuclear fusion technology—providing a sustainable and extensive source of energy.

The substantial market share reflects the widespread emphasis on addressing global energy needs through scalable and environmentally friendly solutions.

Research & Development, as well as Space Propulsion, accounted for the remaining market shares, emphasizing the diverse potential of nuclear fusion beyond electricity. Research & Development serves as a critical component, focusing on overcoming technical challenges and enhancing the efficiency of fusion reactions.

Space Propulsion, although smaller in current market share, represents a forward-looking application, exploiting the high thrust and efficiency of fusion-based propulsion systems for future space exploration missions.

Electricity Generation’s predominance in the market highlights the priority given to transforming energy systems and reducing reliance on fossil fuels. It signals strong confidence in the scalability of fusion technology to meet global demand, positioning nuclear fusion not only as a technological marvel but as a cornerstone for future energy security and sustainability.

Key Market Segments

By Technology

- Inertial Confinement

- Magnetic Confinement

- Others

By Fuels

- Deuterium/tritium

- Deuterium

- Deuterium, helium-3

- Proton Boron

- Others

By Application

- Electricity Generation

- Research & Development

- Space Propulsion

- Others

Driving Factors

Advances in Magnetic Confinement Boost Fusion Efficiency

Technological breakthroughs in magnetic confinement, particularly with tokamaks and stellarators, are pivotal in enhancing the efficiency of nuclear fusion reactions. These advancements allow for better containment and stabilization of the high-temperature plasma essential for sustained fusion.

As researchers achieve longer plasma retention times and higher temperatures, the feasibility of nuclear fusion as a practical energy source becomes more attainable. This factor is driving significant investments and collaborations in the nuclear fusion sector, promising a future with abundant clean energy.

Growing Global Demand for Sustainable Energy Solutions

As global energy demands rise, so does the urgency for sustainable and clean energy sources. Nuclear fusion offers a nearly limitless supply of energy with minimal environmental impact, positioning it as a potential solution to future energy needs. This promise drives governmental and private sector funding towards fusion research and development projects.

The pursuit of fusion energy is fueled by its potential to provide a stable, scalable, and clean energy alternative, aligning with global sustainability goals and carbon neutrality commitments.

Increased International Collaboration and Funding

International collaborations, such as the ITER project, exemplify the global commitment to advancing nuclear fusion technology. These partnerships pool resources, knowledge, and financial support, accelerating technological advancements and overcoming the substantial engineering challenges of fusion energy.

Funding from various countries supports extensive research and development efforts, underscoring a collective approach to achieving the breakthroughs needed for commercial fusion power. Such collaborations enhance the sharing of breakthroughs and reduce the overall technological risks associated with nuclear fusion development.

Restraining Factors

High Costs of Research and Development Limit Progress

The extensive financial requirements for developing nuclear fusion technology present a significant barrier. Building and maintaining fusion reactors, such as tokamaks, require massive capital investments, often in the billions of dollars.

This financial burden can deter private sector involvement and limit government funding, especially in economic downturns. The uncertainty of achieving a commercial energy output further exacerbates hesitancy to invest, slowing the pace of technological advancements and the scalability of fusion energy projects.

Technical Challenges in Achieving Sustainable Fusion

Sustaining a controlled nuclear fusion reaction that produces more energy than it consumes remains an unresolved technical challenge. The conditions necessary for fusion—extremely high temperatures and pressures—are difficult to maintain. Current technology has not yet achieved net energy gain in a stable, continuous manner, which is crucial for practical energy production.

This fundamental challenge restricts the progression from experimental to operational fusion reactors, impacting the overall development timeline and feasibility of fusion as a viable energy and power source.

Regulatory and Safety Concerns Impede Development

The development of nuclear fusion technology is also hindered by stringent regulatory and safety requirements. The potential risks associated with fusion reactors, including radiation hazards and the handling of tritium, a radioactive isotope of hydrogen, necessitate comprehensive safety measures.

Regulatory frameworks are often slow to adapt to the novel needs of fusion technology, leading to delays in reactor approval and construction. These regulatory challenges can discourage investment and innovation in the fusion sector, slowing down its development and commercialization.

Growth Opportunity

Expansion of Renewable Energy Portfolios Drives Fusion Investment

As nations and corporations intensify their commitments to renewable energy, nuclear fusion stands out as a highly promising addition to energy portfolios. Fusion Energy’s potential to provide vast amounts of clean power aligns with global decarbonization goals.

This alignment prompts increased investments from governments and private entities looking to pioneer sustainable energy technologies. As awareness and support for fusion grow, the influx of funding can accelerate research, development, and eventually, the integration of fusion power into the mainstream energy grid.

Technological Innovations Lower Operational Costs

Continuous advancements in materials science and magnetic containment technologies present a substantial growth opportunity for the nuclear fusion market. Innovations like high-temperature superconductors and improved plasma control systems are progressively reducing the operational costs of fusion reactors.

These technological breakthroughs enhance the efficiency and safety of reactors, making fusion a more feasible option for large-scale energy production. As these technologies mature, they could significantly lower the threshold for commercial viability of fusion energy.

Collaborative International Projects Boost Market Dynamics

Global collaborative projects, such as ITER and similar initiatives, serve as catalysts for the nuclear fusion market. These international endeavors not only pool financial and intellectual resources but also foster standard-setting and regulatory approvals across borders.

As these projects demonstrate incremental successes, they validate the potential of fusion energy and encourage further international and cross-sector cooperation. Such collaborations are vital for overcoming technical and financial challenges, propelling the nuclear fusion market towards commercialization and widespread adoption.

Latest Trends

Advancements in Artificial Intelligence Enhance Fusion Reactor Efficiency

The integration of artificial intelligence (AI) in nuclear fusion research is a transformative trend. AI algorithms optimize the control of plasma, the hot fuel used in fusion reactors, enhancing stability and efficiency.

These technological advancements enable more precise predictions and real-time adjustments during fusion experiments, significantly improving the performance and scalability of reactors.

As AI continues to evolve, its application in fusion research promises to accelerate the path to achieving sustainable and commercially viable fusion energy.

Use of Advanced Materials for Improved Reactor Performance

Research into new, more resistant materials capable of withstanding the extreme conditions inside fusion reactors is a key trend. Developments in materials science, such as the creation of damage-resistant alloys and ceramics, enhance the durability and lifespan of reactor components.

These materials are critical for maintaining the integrity of the reactor under intense heat and radiation, which can significantly extend operation periods and reduce maintenance costs. This ongoing innovation in materials technology supports the feasibility of long-term fusion energy production.

Increased Public-Private Partnerships Fuel Development Efforts

There is a growing trend of public-private partnerships (PPPs) in the nuclear fusion sector. Governments and private companies are increasingly collaborating to share the financial, technical, and operational risks associated with fusion research and development.

These partnerships are vital for pooling resources and expertise, facilitating the necessary investments to advance fusion technology toward commercialization. As more private enterprises enter the fusion market, spurred by potential economic and environmental benefits, these collaborations are expected to expand, driving faster innovation and development in the field.

Regional Analysis

The Asia-Pacific nuclear fusion market holds a 44.5% share, valued at USD 145.07 billion.

The global nuclear fusion market is characterized by significant regional variation, with Asia Pacific leading with a 44.5% market share, valued at USD 145.07 billion. This dominance is driven by substantial investments from countries like China, South Korea, and Japan in fusion technology and research infrastructure.

North America also plays a pivotal role, focusing on advancing plasma physics and magnetic confinement technologies, aiming to optimize the efficiency and safety of fusion reactors. Europe follows closely, benefiting from collaborative projects like ITER, based in France, which pools resources and expertise from member countries to accelerate the path to commercial fusion energy.

In contrast, the Middle East & Africa and Latin America regions are currently less active in the nuclear fusion sector. However, these regions hold potential for future growth as global energy demands increase and technological transfer becomes more prevalent.

Investments in these areas are expected to rise, particularly in educational and research capabilities, to support the long-term development of nuclear fusion.

Collectively, these regional dynamics underscore the transformative potential of nuclear fusion as a sustainable energy source, with Asia-Pacific currently leading the way in market development and innovation.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the global Nuclear Fusion Market, key players are strategically positioning themselves to capitalize on the emerging opportunities within this highly specialized and technologically intensive field. As of 2023, companies like Commonwealth Fusion and General Fusion are at the forefront, leveraging advanced magnetic confinement techniques to progress toward viable commercial energy production.

Commonwealth Fusion, in particular, is making significant strides by developing high-temperature superconductors that could potentially revolutionize reactor designs by allowing smaller, more efficient systems.

Tokamak Energy and First Light Fusion are notable for their distinctive approaches. Tokamak Energy focuses on compact, modular tokamak reactors that promise quicker development cycles and scalability, while First Light Fusion explores inertial confinement as an alternative route to achieving fusion, which could offer a simpler path to commercialization.

Emerging contenders like Helion and Zap Energy underscore the diversity within the sector. Helion aims to commercialize its pulsed fusion device, which seeks to combine the best aspects of magnetic confinement fusion and inertial fusion. Zap Energy, on the other hand, is working on sheared-flow stabilized Z-pinch technology, which offers a potentially simpler and more cost-effective approach.

Lockheed Martin and Southern Company reflect the interest of large-scale and traditional energy firms in fusion technology, each exploring different technological pathways and collaborative efforts to integrate fusion into the broader energy landscape.

The dual presence of startups like HB11, which is pioneering a novel approach using hydrogen-boron fusion, and established corporations indicates a dynamic market environment. This blend of innovation, backed by both agile startups and well-funded corporate entities, drives the market forward amidst technical challenges and substantial capital requirements.

The collaborative projects, such as those involving TAE Technologies and Marvel Fusion GmbH, further highlight the trend towards international partnerships to pool expertise, reduce risks, and accelerate technological advancements.

Top Key Players in the Market

- Agni Fusion Energy

- Brilliant Light Power Inc

- Commonwealth Fusion

- First Light Fusion

- General Fusion

- HB11

- Helion

- Hyperjet Fusion

- Lockheed Martin

- Marvel Fusion

- Marvel Fusion GmbH

- Southern Company

- TAE Technologies

- Tokamak Energy

- Zap Energy

Recent Developments

- In 2024, HB11 Energy, an Australian company, made significant strides in the nuclear fusion sector by demonstrating a new method using high-power lasers to fuse hydrogen and boron-11. This innovative approach eliminates the need for extreme temperatures and radioactive materials, unlike traditional fusion processes.

- In 2024, Helion Energy is set to demonstrate net electricity production from fusion, a critical step towards harnessing fusion power commercially. This marks a significant milestone in fusion energy development, potentially paving the way for future fusion power plants.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 326.4 Billion |

| Forecast Revenue (2033) | USD 607.0 Billion |

| CAGR (2024-2033) | 6.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Inertial Confinement, Magnetic Confinement), By Fuels (Deuterium/tritium, Deuterium, Deuterium, helium-3, Proton Boron), By Application (Electricity Generation, Research & Development, Space Propulsion) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Agni Fusion Energy, Brilliant Light Power Inc, Commonwealth Fusion, First Light Fusion, General Fusion, HB11, Helion, Hyperjet Fusion, Lockheed Martin, Marvel Fusion, Marvel Fusion GmbH, Southern Company, TAE Technologies, Tokamak Energy, Zap Energy |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |