Quick Navigation

- Report Overview

- Key Takeaways

- Analysts’ Viewpoint

- Impact of AI

- US Primary Edtech Market

- By Deployment Mode Analysis

- By Type Analysis

- By Sector Analysis

- By End-User Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

The North America Primary Edtech Market size is expected to be worth around USD 207.5 Billion By 2034, from USD 62.8 billion in 2024, growing at a CAGR of 14.2% during the forecast period from 2025 to 2034. The US Primary Edtech Market Size was exhibited at USD 57.6 Billion in 2024 with CAGR of 14%.

Educational technology (Edtech) in North America primarily focuses on enhancing learning experiences through technological advancements and digital resources. The sector includes a variety of tools and platforms aimed at improving educational outcomes in primary education. These technologies are designed to make learning more interactive, accessible, and customized to individual student needs.

The growth of the North American Edtech market can be attributed to several key factors. A primary driver is the high penetration of internet connectivity in the region, with over 94% of the population in the United States and Canada having access to the internet. This connectivity facilitates widespread adoption of digital learning platforms and resources.

Educational institutions are increasingly adopting these technologies to cater to diverse learning needs, provide flexible learning options, and improve educational outcomes. AI and AR/VR technologies, for example, allow for personalized learning experiences and interactive content, which are crucial for engaging students more effectively and enhancing their learning retention.

Based on data from Passive Secrets, EdTech adoption among K-12 schools increased by 99%, reflecting a strong shift toward digital learning environments. This surge can be linked to the rising integration of advanced technologies such as Augmented Reality (AR) and Virtual Reality (VR) in classrooms.

In 2023, the education AR market was valued at $5.3 billion, underscoring its role in enhancing engagement and interactivity in learning. At the same time, Virtual Reality head-mounted display (HMD) revenues in education surpassed $640 million, indicating growing institutional investments in immersive learning tools.

The demand for Edtech solutions in North America is driven by the widespread acceptance of blended learning models and the increasing requirement for educational accessibility. The trends towards mobile learning and the use of gamification techniques in education further stimulate this demand. The market is also witnessing a shift towards more online and hybrid learning environments, accelerated by the pandemic’s impact on traditional educational methods.

The primary Edtech market in North America is also influenced by various factors including the increasing digitization of education, government initiatives supporting educational technology, and significant investments flowing into the sector. These factors collectively facilitate a conducive environment for the growth of Edtech solutions.

Key Takeaways

- The North America Primary Edtech market is projected to expand significantly, reaching approximately USD 207.5 billion by 2034, up from USD 62.8 billion in 2024. This represents a robust compound annual growth rate (CAGR) of 14.2% over the forecast period.

- In the U.S., the Edtech sector showcased a substantial valuation of USD 57.6 billion in 2024. With a continued growth trajectory, the market is anticipated to maintain a CAGR of 14%.

- The On-Premise solutions stood out in 2024, holding a dominant 71.5% share of the market. This preference underscores the significant reliance on localized, server-based educational technologies within the region.

- Hardware remained a critical component of the Edtech landscape, securing a significant 39.6% market share in 2024. The emphasis on tangible, tech-based educational tools illustrates the foundational role of physical devices in facilitating educational processes.

- The K-12 education segment overwhelmingly dominated the market, with an 81.6% share in 2024. This segment’s prominence highlights the pivotal role of Edtech in primary and secondary education environments.

- Businesses’ engagement with Edtech solutions was markedly high, capturing more than 65.5% of the market in 2024. This indicates a strong inclination towards using educational technologies for corporate training and development initiatives.

Analysts’ Viewpoint

Investment opportunities in the North American primary Edtech market are grow rapidly, particularly in areas involving AI and immersive learning technologies. The expansion of corporate training and upskilling initiatives presents additional avenues for Edtech companies to develop enterprise solutions that cater to adult learners and professional development needs.

According to the findings from Market.us, global EdTech market is projected to reach USD 810.3 billion by 2033, rising from USD 220.5 billion in 2023, and registering a CAGR of 13.9% over the forecast period from 2024 to 2033. In 2023, North America accounted for over 37.3% of the global market, generating USD 82.24 billion in revenue, driven by early adoption of digital platforms and strong institutional investments.

Edtech offers numerous business benefits, including the potential for reaching a broader audience, scalability of educational products and services, and enhanced capabilities for tracking learning progress and outcomes. These benefits contribute to the growing appeal of Edtech solutions among educational institutions and businesses.

The regulatory landscape for Edtech in North America is evolving, with increased focus on data privacy and security. Regulations are being crafted to ensure that student information is protected while fostering an environment that encourages technological innovation in education.

Impact of AI

The impact of Artificial Intelligence (AI) on the North America Primary Edtech Market is significant, demonstrating profound changes across various educational sectors. Here are five key points illustrating AI’s influence:

- Enhanced Personalization and Efficiency: AI technologies are integral in personalizing learning experiences, adapting educational content to meet individual student needs. This customization improves engagement and learning outcomes by addressing specific educational strengths and weaknesses.

- Immersive Learning Technologies: The integration of virtual and augmented reality, powered by AI, is revolutionizing traditional learning environments. These technologies provide immersive experiences that enhance understanding and retention of complex subjects, making learning more engaging and interactive.

- Streamlining Administrative Tasks: AI is automating time-consuming administrative tasks such as grading and scheduling. This shift allows educators to focus more on teaching and interacting with students, thereby improving educational quality and efficiency.

- Data-Driven Insights for Tailored Education: AI’s capability to analyze extensive data sets provides educators with valuable insights into student performance and learning habits. This information helps in tailoring teaching methods and educational content to better suit individual learning styles and needs, thereby optimizing educational outcomes.

- Broadening Access and Inclusivity: AI technologies facilitate the expansion of educational opportunities to underserved and remote areas, providing scalable and accessible learning solutions. This is particularly crucial in emerging markets where traditional educational resources may be limited.

US Primary Edtech Market

The US Primary Edtech Market is valued at approximately USD 57.6 Billion in 2024 and is predicted to increase from USD 65.7 Billion in 2025 to approximately USD 213.5 Billion by 2034, projected at a CAGR of 14% from 2025 to 2034.

The integration of cutting-edge technologies in education, driven by substantial investments in research and development, is a key factor. U.S. companies and educational institutions are at the forefront of adopting innovative technologies such as artificial intelligence (AI), machine learning, and augmented reality (AR), which enhance the learning experience by making it more interactive and personalized.

Market Share by Country (2019-2024) (%)

| Country | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|---|

| The US | 92.5% | 92.3% | 92.1% | 92.0% | 91.8% | 91.6% |

| Canada | 7.5% | 7.7% | 7.9% | 8.0% | 8.2% | 8.4% |

Moreover, the U.S. boasts a robust digital infrastructure that supports widespread access to high-speed internet and advanced technological devices. This infrastructure facilitates the seamless implementation and scaling of Edtech solutions across diverse educational settings, from urban to rural, ensuring a broader reach and more equitable access to quality education.

By Deployment Mode Analysis

In 2024, the On-Premise segment of the North America Primary Edtech market held a dominant market position, capturing more than a 71.5% share. This significant market share is attributed to several key factors that favor on-premise solutions over cloud-based alternatives in specific contexts.

Primarily, the preference for on-premise deployment can be linked to greater control over data and system security. Educational institutions often handle sensitive information, including student records and proprietary educational content, which necessitates stringent security measures.

On-premise systems provide organizations the ability to directly manage and secure their infrastructure, thus reducing the vulnerability associated with external hosting and data breaches. Moreover, on-premise solutions offer enhanced customization and integration capabilities.

Market Share, Deployment Analysis (2019-2024) (%)

| Deployment Mode | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|---|

| Cloud | 26.2% | 26.7% | 27.1% | 27.6% | 28.1% | 28.5% |

| On-Premise | 73.8% | 73.3% | 72.9% | 72.4% | 71.9% | 71.5% |

Schools and colleges with specific educational needs or legacy systems find it easier to tailor on-premise software to fit into their existing technological ecosystems without significant disruptions. This customization extends to both the educational content and the functionality of the platforms, allowing institutions to maintain a consistent educational experience aligned with their pedagogical goals.

However, despite these advantages, the on-premise segment faces challenges such as higher upfront costs and the need for ongoing maintenance. These factors require institutions to allocate significant budgets and resources for the deployment and upkeep of the technology.

Nonetheless, for many North American educational institutions, the benefits of having direct control and high customization capabilities continue to outweigh these challenges, sustaining the segment’s leading position in the market.

By Type Analysis

In 2024, the Hardware segment of the North America Primary Edtech market held a dominant market position, capturing more than a 39.6% share. This prominence in the market is attributed to several pivotal factors that underscore the essential role of hardware in educational technology.

The significance of the Hardware segment stems primarily from its foundational role in facilitating digital learning environments. Devices such as computers, tablets, interactive whiteboards, and other physical tech tools are critical for implementing digital curricula.

These tools serve as the primary interface through which students and educators interact with educational software and content. As schools continue to modernize and integrate technology into their classrooms, the demand for robust and reliable educational hardware remains strong.

Market Share, Type Analysis (2019-2024) (%)

| Type | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|---|

| Hardware | 42.4% | 41.9% | 41.3% | 40.7% | 40.2% | 39.6% |

| Software | 27.6% | 28.0% | 28.4% | 28.7% | 29.2% | 29.5% |

| Content | 30.0% | 30.2% | 30.4% | 30.6% | 30.6% | 30.9% |

Additionally, the surge in hardware demand is closely linked to the increasing trend of personalized learning environments and the integration of technology in early education settings. Hardware solutions provide the necessary infrastructure for these initiatives, supporting a range of educational applications and multimedia resources that enhance the learning experience.

However, the market for hardware is not without its challenges. The initial cost of investment and the rapid pace of technological advancement necessitate frequent updates and replacements, which can be a significant financial burden for educational institutions. Despite these challenges, the tangible benefits of educational hardware, such as enhanced student engagement and improved learning outcomes, solidify its critical position in the market.

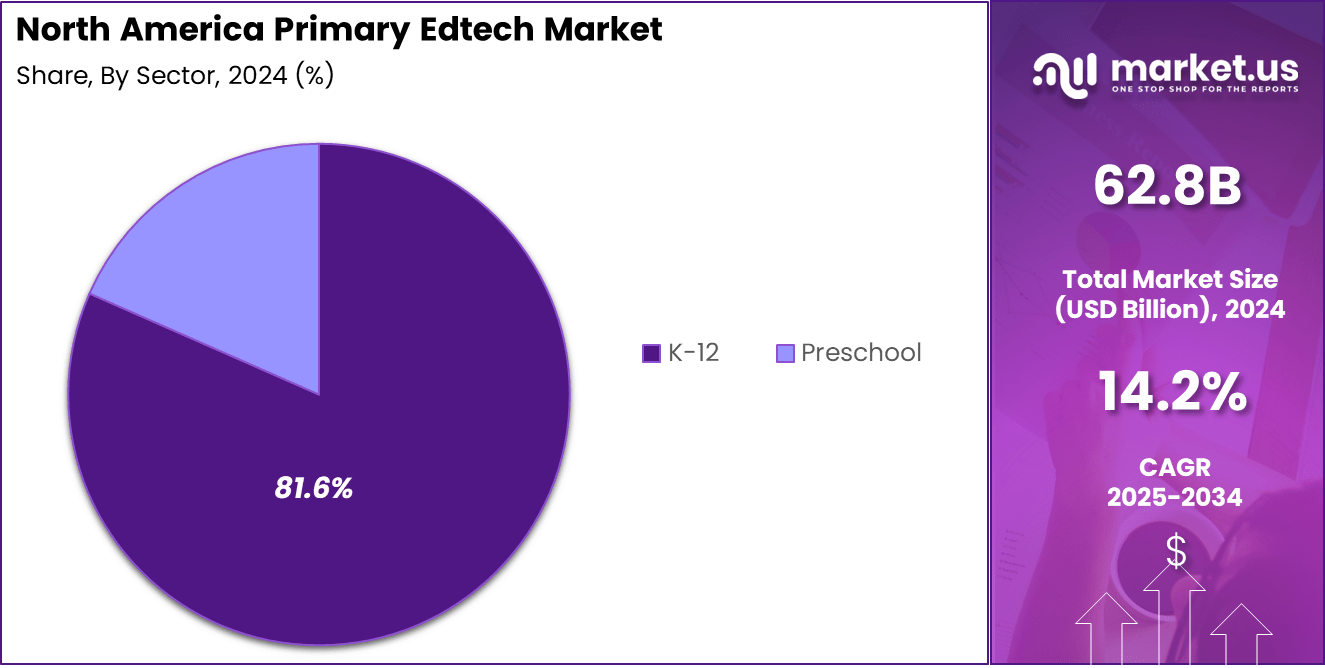

By Sector Analysis

In 2024, the K-12 segment held a dominant market position in the North America Primary Edtech market, capturing more than an 81.6% share. This commanding presence is primarily due to the comprehensive integration of educational technologies across primary and secondary schools, aimed at enhancing learning outcomes and operational efficiencies.

The dominance of the K-12 segment can be attributed to several key factors. First, the widespread implementation of digital curricula and standardized testing requires robust Edtech solutions that facilitate both teaching and administrative tasks.

Educational technologies in K-12 schools include learning management systems (LMS), student information systems (SIS), and classroom assessment tools, all designed to improve the quality of education and the efficiency of classroom management.

Market Share, Sector Analysis (2019-2024) (%)

| Sector | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|---|

| K–12 | 82.4% | 82.3% | 82.1% | 81.9% | 81.8% | 81.6% |

| Preschool | 17.6% | 17.7% | 17.9% | 18.1% | 18.2% | 18.4% |

Furthermore, government policies and funding in North America have significantly supported the adoption of Edtech in the K-12 sector. Initiatives aimed at closing the digital divide and providing equal access to technology for all students have propelled the integration of Edtech solutions across the region. These policies ensure that schools are equipped with the latest technologies to support a 21st-century learning environment.

Lastly, the COVID-19 pandemic accelerated the need for remote learning solutions, which has sustained high demand for Edtech in the K-12 sector. Schools have adopted various digital tools to facilitate distance learning and ensure continuity of education during school closures, further embedding technology into daily educational practices.

By End-User Analysis

In 2024, the Business segment held a dominant market position in the North America Primary Edtech market, capturing more than a 65.5% share. This substantial market share is primarily driven by the increasing demand for corporate training and professional development programs that leverage educational technologies.

The leadership of the Business segment is underpinned by several factors. Firstly, there is a growing recognition among corporations of the strategic importance of upskilling and reskilling employees in response to rapidly changing technologies and market conditions.

Businesses are investing in Edtech solutions such as Learning Management Systems (LMS), online course platforms, and virtual training tools to facilitate continuous learning and development opportunities for their employees.

Market Share, End-User Analysis (2019-2024) (%)

| End-User | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|---|

| Business | 67.6% | 67.2% | 66.8% | 66.3% | 65.9% | 65.5% |

| Consumer | 32.4% | 32.8% | 33.2% | 33.7% | 34.1% | 34.5% |

Additionally, the integration of Edtech in business settings is enhanced by the focus on measurable outcomes, such as improved employee performance and productivity. Edtech platforms provide businesses with analytics and data-driven insights that help tailor educational programs to the specific needs of the workforce, thereby maximizing return on investment in employee training.

Moreover, the shift towards remote work has also propelled the adoption of Edtech solutions in the business sector. Companies are utilizing Edtech tools to deliver training and professional development remotely, ensuring that employees, regardless of their location, have access to necessary learning resources and collaboration tools.

Key Market Segments

By Deployment Mode

- Cloud

- On-Premise

By Type

- Hardware

- Software

- Content

By Sector

- K-12

- Preschool

By End-User

- Business

- Consumer

Driver

Increased Integration of Artificial Intelligence

Artificial Intelligence (AI) is playing a pivotal role in driving the growth of the North American primary Edtech market. AI’s capabilities to enhance personalized learning experiences are particularly significant. These technologies allow educational platforms to tailor content to individual student needs, automatically adjusting to their learning pace and style.

This personalization not only improves engagement but also addresses diverse learning preferences and challenges, making education more effective and accessible. As schools continue to adopt AI-driven tools, they benefit from more insightful data analytics and improved learning outcomes, fostering an environment that supports continuous educational innovation and effectiveness.

Restraint

Inequitable Access to Technology

One major restraint facing the North American primary Edtech market is the unequal access to necessary technological resources. Many students in rural and underserved urban areas lack the essential internet connectivity and digital devices needed for effective participation in digital learning. This digital divide limits the reach and impact of Edtech solutions, posing a significant challenge to educational equity.

Addressing this issue requires not only infrastructural investments but also policies that ensure all students have the necessary tools for accessing digital education. This barrier affects the scalability of Edtech solutions and could slow down the potential growth of the market unless comprehensive solutions are implemented.

Opportunity

Expansion of Blended Learning Models

The North American primary Edtech market is witnessing significant opportunities in the expansion of blended learning models. This educational approach combines traditional classroom methods with digital media, allowing for a more flexible and engaging learning experience. Blended learning models cater to the modern educational needs by providing students with the ability to learn at their own pace and access resources anytime and anywhere.

The rise of hybrid learning environments, supported by Edtech platforms, facilitates a more personalized education system and opens up new avenues for interactive, student-centered learning. This trend not only enhances educational outcomes but also broadens the market for Edtech products and services across North America.

Challenge

Integration and Training Issues

A persistent challenge within the North American primary Edtech market is the effective integration of new technologies into existing educational frameworks and the adequate training of educators to use these technologies.

Many teachers face difficulties in adapting to new digital tools, which can hinder the effectiveness of Edtech solutions.The lack of sufficient training and support results in underutilization of potentially transformative technologies, thereby impacting the overall learning experience.

Moreover, resistance from educators, who are accustomed to traditional teaching methods, further complicates the adoption of innovative educational technologies. Overcoming this challenge is crucial for maximizing the benefits of Edtech and requires focused efforts on professional development and support systems for educators.

Growth Factors

The North American primary Edtech market is witnessing substantial growth, driven by several pivotal factors. A key growth factor is the rising demand for personalized and flexible learning solutions. Educational institutions are increasingly leveraging AI-driven platforms, virtual and augmented reality tools, and other digital solutions to provide customized learning experiences that cater to diverse student needs.

This shift towards personalized learning is not just enhancing educational outcomes but also aligning with broader pedagogical trends towards accommodating individual learning styles and paces. Moreover, the increasing integration of technology in educational practices, such as the use of gamified content and microlearning courses, supports a more engaging and effective learning environment.

Emerging Trends

Emerging trends in the Edtech sector further underscore its dynamic evolution. One of the most significant trends is the growing emphasis on blended and online learning platforms, which combine traditional classroom methods with digital media.

This hybrid model facilitates greater flexibility and accessibility, allowing students to manage their learning more effectively. The rise of these platforms has been accelerated by the pandemic but continues to be a focal point of educational strategies post-pandemic.

Additionally, the adoption of advanced technologies like AI, AR, and VR is transforming educational content delivery. These technologies are being used to create more immersive and interactive learning experiences, which not only engage students more effectively but also cater to a variety of learning needs and styles.

Business Benefits

The business benefits of Edtech in North America are manifold. Edtech solutions enhance educational delivery by enabling more interactive and engaging learning experiences, which can lead to improved student performance and satisfaction. Schools and educational institutions that adopt these technologies often see higher engagement rates and better educational outcomes as a result.

Furthermore, the Edtech sector’s growth is also fostering economic benefits, such as the creation of new jobs in tech and education sectors and the attraction of investments into the region. The continuous innovation within the Edtech space not only strengthens the educational infrastructure but also supports the broader economic landscape by contributing to a more skilled workforce.

Key Player Analysis

The landscape of the North American Primary Edtech market is shaped by a blend of established and emerging companies, each contributing uniquely to the evolution of educational technology. Prominent players include Coursera Inc., 2U Inc., Udemy Inc., and Chegg Inc. These companies are recognized for their significant influence and comprehensive educational platforms that cater to a wide range of learning needs.

Coursera and Udemy are particularly noted for their vast array of online courses that span multiple disciplines, appealing to lifelong learners across the globe. 2U, known for partnering with top-tier universities to offer online degree programs, combines the prestige of traditional education with the accessibility of modern technology.

These key players are continually innovating and expanding their offerings to adapt to the dynamic market demands, focusing on inclusivity and accessibility to ensure education reaches every corner of the society. Their strategies often involve significant investments in AI and personalized learning environments, enhancing their platforms’ capability to offer customized education solutions at scale.

Top Key Players in the Market

- Duolingo

- McGraw Hill

- IXL Learning

- Seesaw

- ViewSonic Corporation

- DreamBox Learning

- Byju’s (Think and Learn Pvt. Ltd.)

- Outschool, Inc.

- Anthology Inc.

- Dell Technologies Inc.

- Samsung Electronics Co., Ltd.

Recent Developments

- In March 2025, McGraw Hill acquired Essaypop, an interactive, cloud-based writing platform, to strengthen its portfolio of digital literacy tools and enhance personalized learning capabilities for K-12 students.

- In August 2024, IXL Learning acquired Carson Dellosa Education, a leading publisher of teaching supplies, to expand its offerings and support learners with both physical and digital educational resources.

- In July 2024, Duolingo acquired Detroit-based animation and motion design studio Hobbes to enhance its design and animation capabilities, aiming to make learning more engaging.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 62.8 Bn |

| Forecast Revenue (2034) | USD 236.9 Bn |

| CAGR (2025-2034) | 14.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Deployment Mode (Cloud, On-Premise), By Type (Hardware, Software, Content), By Sector (K-12, Preschool), By End-User (Business, Consumer) |

| Competitive Landscape | Duolingo, McGraw Hill, IXL Learning, Seesaw, ViewSonic Corporation, DreamBox Learning, Byju’s (Think and Learn Pvt. Ltd.), Outschool, Inc., Anthology Inc., Dell Technologies Inc., Samsung Electronics Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |