Quick Navigation

Report Overview

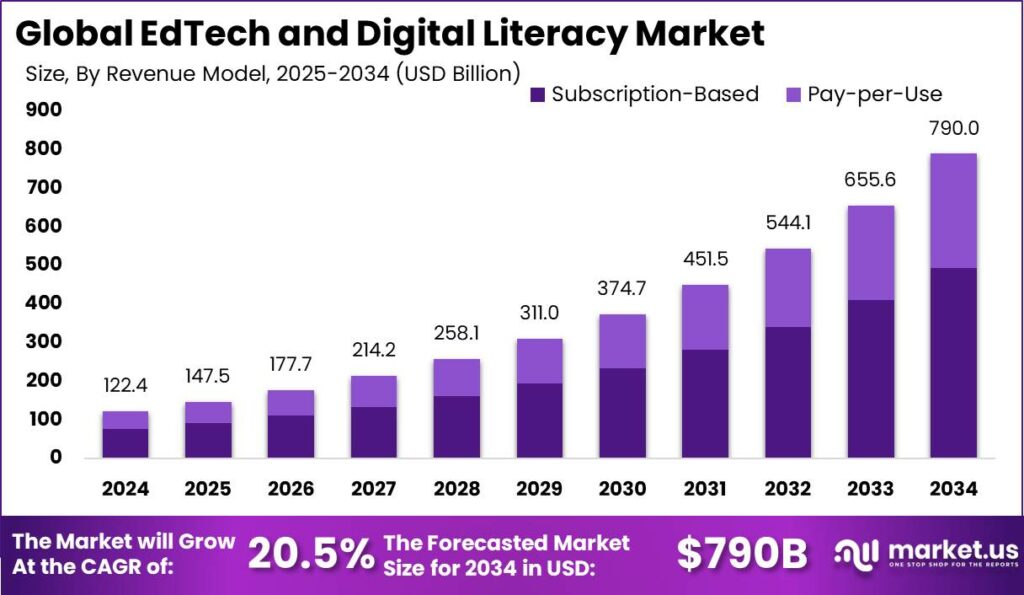

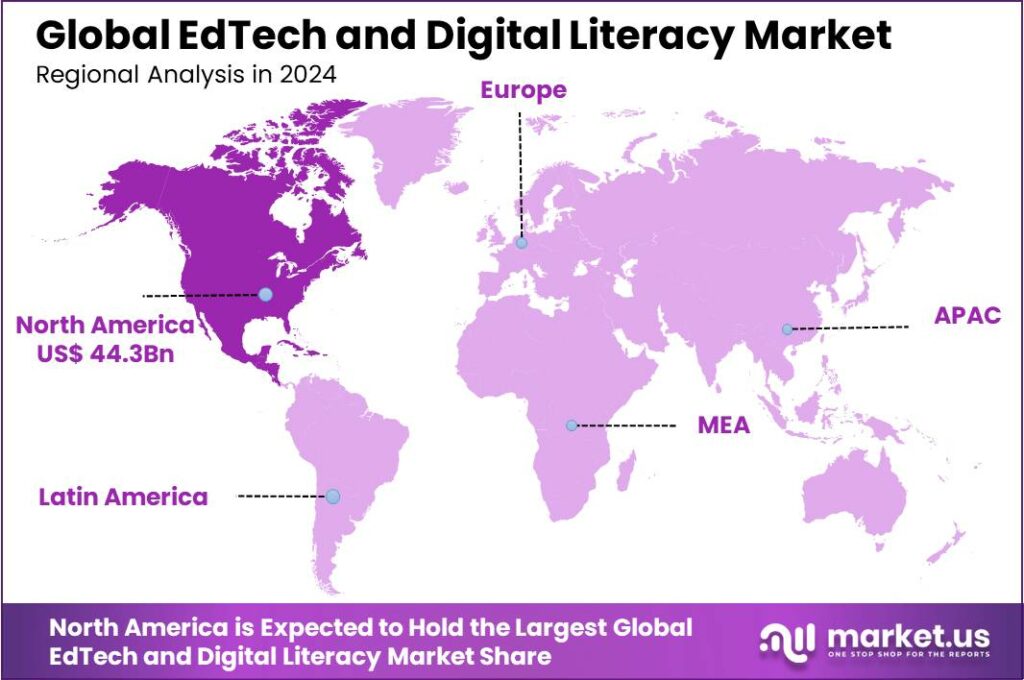

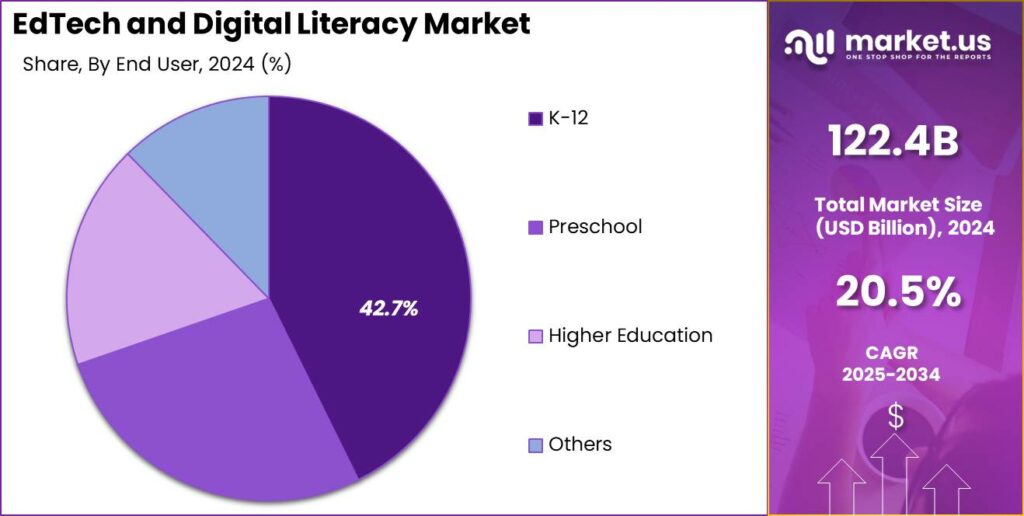

The Global EdTech and Digital Literacy Market size is expected to be worth around USD 790 Billion By 2034, from USD 122.4 billion in 2024, growing at a CAGR of 20.5% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 36.2% share, holding USD 44.3 Billion revenue.

The EdTech and digital literacy market is a rapidly expanding sector within the global education industry. This market focuses on providing technological solutions and training to improve educational outcomes and increase digital proficiency among learners of all ages. As the world increasingly moves towards digital platforms for both learning and professional activities, the demand for comprehensive digital literacy and advanced educational technologies is growing.

The primary drivers of the EdTech and digital literacy market include the widespread adoption of digital devices in education, the globalization of education through online learning platforms, and the increasing requirement for digital skills in the job market. These factors are pushing educational institutions and governments to invest in digital infrastructure and literacy programs to ensure that students and employees are well-prepared for the demands of the modern workplace.

The demand in the EdTech and digital literacy market is primarily driven by the need to bridge the gap between traditional educational methods and modern workplace requirements. There’s a significant opportunity for developing platforms that are user-friendly and cater to diverse learning needs and environments. Market opportunities also extend into the integration of artificial intelligence and machine learning to personalize learning experiences and improve educational outcomes.

Technological advancements play a pivotal role in shaping the EdTech sector. Innovations such as virtual reality (VR), augmented reality (AR), and adaptive learning platforms are revolutionizing how educational content is delivered. These technologies offer immersive and interactive experiences that make learning more engaging and effective. Additionally, data analytics tools are increasingly being used to track learner progress and tailor educational strategies to individual needs.

According to the latest survey, the global EdTech market is projected to grow at a remarkable pace over the next decade. The market size, valued at USD 220.5 billion in 2023, is expected to reach USD 810.3 billion by 2033, expanding at a compound annual growth rate (CAGR) of 13.9% from 2024 to 2033.

Digital literacy is on the rise globally, with a 12% improvement in recent years. However, there’s a noticeable gap between urban and rural areas. For instance, in India, the digital literacy rate stands at 61% in urban areas, while rural regions lag at 25%. Meanwhile, the European Union has set an ambitious target to ensure 70% of adults have basic digital skills by 2025.

The COVID-19 pandemic acted as a catalyst for EdTech adoption worldwide, leading to a 150% increase in online education usage since 2019. Over 1.2 billion children across 186 countries transitioned to online learning during the pandemic. This rapid shift has fundamentally changed the way education is delivered, with 79% of teachers now integrating EdTech tools into their daily teaching practices.

For businesses, Investing in EdTech and digital literacy programs offers substantial benefits for businesses. It leads to a more skilled workforce capable of handling advanced technological tools and systems, which can increase efficiency and productivity. For educational institutions, incorporating technology in teaching and learning processes attracts a broader student base and enhances the learning experience, potentially improving outcomes and satisfaction rates.

Key Takeaways

- The EdTech and Digital Literacy market is poised for substantial growth. It is estimated to soar from USD 122.4 billion in 2024 to approximately USD 790 billion by 2034. This growth represents a robust compound annual growth rate (CAGR) of 20.5% from 2025 to 2034.

- In 2024, North America was at the forefront of this market, holding a significant 36.2% market share, translating to revenues of USD 44.3 billion.

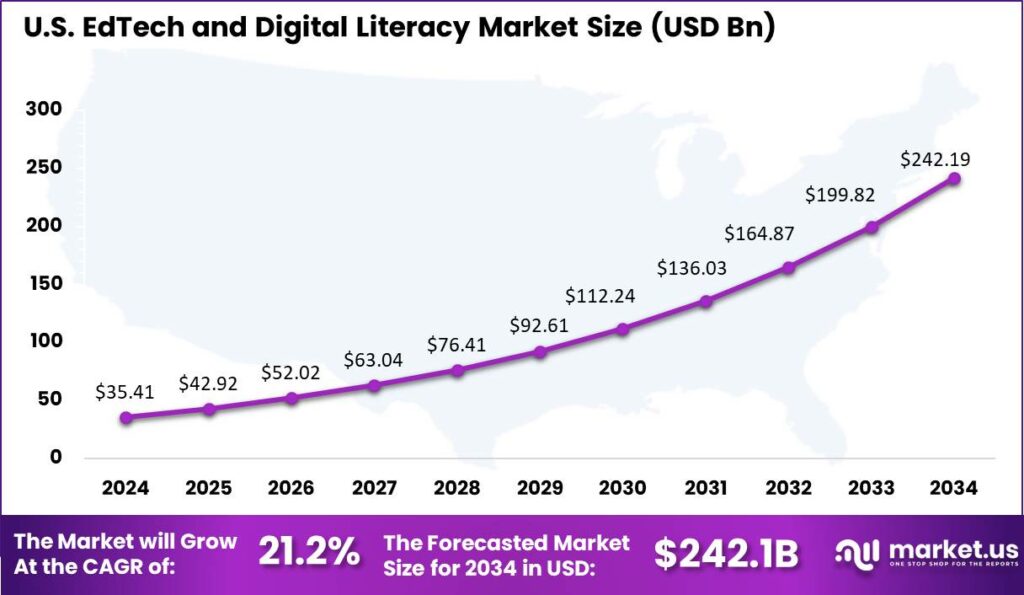

- Zooming into the United States, the EdTech and Digital Literacy market showcased a solid performance with a size of USD 35.41 billion in 2024 and a projected CAGR of 21.2%.

- Focusing on specific segments, Learning Management Systems (LMS) captured a substantial portion of the market, accounting for 36.4% of the total in 2024.

- In the same year, the K-12 segment demonstrated strong market dominance, securing over 42.7% of the market share.

- Additionally, the Subscription-Based model proved to be highly favored within the market, commanding more than 62.6% of the market’s share.

U.S. Market Size and Growth

The US EdTech and Digital Literacy Market exhibited a substantial market size of USD 35.41 billion in 2024, with a notable compound annual growth rate (CAGR) of 21.2%. This remarkable growth trajectory underscores the pivotal role of the United States in the global EdTech landscape, driven by several key factors.

Firstly, the United States boasts a strong technological infrastructure, which is fundamental to the rapid deployment and scalability of EdTech solutions. Home to Silicon Valley and numerous technology giants, the US offers a fertile ground for innovation and early adoption of digital education tools. This environment not only fosters the development of cutting-edge technologies but also integrates them swiftly into educational contexts.

Secondly, there is a high level of investment from both the public and private sectors in the US. Government initiatives aimed at enhancing educational technology in schools, coupled with substantial venture capital investments in EdTech startups, propel the development and adoption of new technologies in education. For instance, federal funding for digital education and significant investments in R&D by leading tech companies often set trends that shape global market dynamics.

Moreover, the US market shows a strong demand for personalization and accessibility in educational technologies, which drives innovation in this sector. EdTech companies are increasingly focusing on creating personalized learning experiences using AI and data analytics, which have shown potential to significantly improve learning outcomes by catering to the individual needs of students.

In 2024, North America held a dominant market position in the EdTech and Digital Literacy sector, capturing more than a 36.2% share, generating approximately USD 44.3 billion in revenue. This leadership can be attributed to several key factors, including the region’s strong technological infrastructure, high levels of investment in education, and the widespread adoption of digital learning tools across both K-12 and higher education institutions.

The United States, in particular, plays a critical role in this dominance, with a substantial portion of market growth driven by its robust EdTech ecosystem. Home to major technology hubs like Silicon Valley, the US is a global leader in the development and commercialization of educational technologies. Additionally, federal initiatives such as the ESSA and other funding programs have fostered widespread adoption of digital literacy programs and platforms, supporting the sector’s growth.

Another driving force behind North America’s market leadership is the high demand for personalized learning solutions. With significant investments in AI and data analytics, EdTech companies in North America have developed advanced platforms that deliver customized educational experiences, aligning with the growing trend of tailored learning.

These innovations cater to diverse learning styles and support students’ specific educational needs, from K-12 to adult learning, thereby enhancing the overall education system’s accessibility and effectiveness. Moreover, North America benefits from extensive collaboration between educational institutions, tech companies, and government agencies.

This collaborative environment accelerates the implementation of new educational technologies, facilitating greater access to digital learning resources across a broad spectrum of learners, including underserved and remote communities. As a result, the region is well-positioned to maintain its dominant share in the EdTech and Digital Literacy market as technological advancements continue to evolve.

Technology Analysis

In 2024, the Learning Management Systems (LMS) segment held a dominant market position, capturing more than a 36.4% share of the EdTech and Digital Literacy market. This prominence can be attributed to several critical factors that underscore the segment’s importance and its continued growth potential.

LMS platforms are integral not only in educational settings but also across corporate environments, where they facilitate the efficient delivery of training and development programs. This broad application across sectors ensures steady demand and diversifies the user base, which includes academic institutions, government agencies, and businesses across various industries like healthcare, finance, and manufacturing

The segment benefits significantly from continual technological advancements, such as the integration of artificial intelligence (AI) and cloud computing. These technologies enhance the learning experience by offering personalized content and more accessible, flexible learning options that cater to a global user base.

The ability for users to access learning materials from anywhere at any time, particularly in today’s mobile and remote-first world, plays a crucial role in the adoption and expansion of LMS solutions. Strong support from educational policies and government funding, particularly in regions like North America, has further propelled the adoption of LMS.

Initiatives aimed at digitalizing educational processes and enhancing workforce development through professional training are significant drivers. This is complemented by the educational sector’s rapid shift towards online solutions, amplified by global events such as the COVID-19 pandemic, which necessitated remote learning and digital education platforms.

End User Analysis

In 2024, the K-12 segment within the EdTech and Digital Literacy market held a commanding position, securing more than a 42.7% market share. This substantial share is indicative of the segment’s pivotal role in primary and secondary education, where technology integration is increasingly seen as crucial for enhancing learning outcomes and educational delivery.

The dominance of the K-12 segment can largely be attributed to several key factors. First, there is a growing emphasis on the adoption of digital tools and platforms that facilitate a more interactive and engaging learning environment. This includes the utilization of cloud-based solutions which offer scalability and flexibility, crucial for adapting to various learning and teaching needs.

Such technologies not only support traditional educational practices but also enable innovative approaches like blended and hybrid learning, which have become more prevalent following the global shifts in educational practices due to the COVID-19 pandemic. Moreover, governmental policies and investments have significantly supported the integration of technology in K-12 education.

Initiatives aimed at improving digital literacy and infrastructure have propelled the adoption of EdTech solutions in schools. This is complemented by the rising demand among educators and institutions to incorporate advanced technologies such as AI and machine learning to personalize the education experience and improve student outcomes.

Finally, the shift towards STEM education and the need for skills development from an early age have fueled the expansion of the K-12 EdTech segment. With a strong focus on preparing students for future challenges, schools are increasingly relying on EdTech tools to provide essential skills in science, technology, engineering, and mathematics, making the K-12 sector a critical area for ongoing EdTech development and investment.

Revenue Model Analysis

In 2024, the Subscription-Based segment in the EdTech and Digital Literacy market held a dominant position, capturing more than a 62.6% share of the market. This leadership can be attributed to several key factors that underscore the appeal of subscription models in educational technology.

Subscription-based models offer a predictable revenue stream for EdTech companies, which is essential for sustained investment in technology and content updates. This model also allows for continuous engagement with users, as it provides them with the flexibility to access a wide range of educational resources and tools for a periodic fee, which can be more cost-effective than one-time purchases for both providers and consumers.

The preference for subscription-based services is further driven by the demand for personalized learning experiences. Subscription platforms often utilize data analytics to tailor educational content to individual learner needs, enhancing learner outcomes. This personalization is crucial in today’s educational landscape, where the emphasis on catering to individual learning styles is increasing.

Furthermore, the COVID-19 pandemic has significantly accelerated the adoption of digital learning platforms. The shift towards remote and hybrid learning environments has made subscription-based digital learning solutions more attractive to educational institutions and learners, providing them with the necessary tools to continue education in fluctuating circumstances.

Overall, the dominance of the Subscription-Based model in the EdTech sector is supported by its ability to provide flexible, scalable, and personalized learning solutions that meet the evolving needs of the global education market. This trend is expected to continue, driven by advancements in educational technologies and a growing emphasis on lifelong learning and professional development.

Key Market Segments

By Technology

- Learning Management Systems (LMS)

- Smart Classrooms

- Artificial Intelligence (AI) in Education

- Augmented Reality (AR) and Virtual Reality (VR)

- Gamification

- Others

By End User

- K-12

- Preschool

- Higher Education

- Others

By Revenue Model

- Subscription-Based

- Pay-per-Use

Driver

Growing Global Demand for Customized Learning Solutions

The EdTech market is rapidly expanding, driven by the global demand for personalized education that caters to diverse learning needs and schedules. Innovative platforms leverage AI to analyze learning patterns, tailoring content dynamically to individual preferences.

This approach enhances educational outcomes by ensuring learners receive the necessary support and resources tailored to their learning style. Adaptive learning platforms like DreamBox and Carnegie Learning are leading this trend by offering tailored educational experiences, particularly in subjects like mathematics.

Restraint

Digital Adoption Gaps and Technological Disparities

One of the primary restraints in the EdTech sector is the significant gap in technology adoption across different regions and demographics. Despite advancements in educational technologies, disparities in access to these resources can hinder the effectiveness of EdTech solutions.

Many areas, especially in developing countries, still struggle with basic issues such as reliable internet connectivity and access to modern devices, which are crucial for digital learning. These challenges are compounded by regulatory hurdles and the lack of digital infrastructure, which can stifle the growth and potential impact of EdTech initiatives.

Opportunity

Expansion of Nanolearning Platforms

Nanolearning platforms present a significant opportunity within the EdTech market. These platforms offer short, focused educational modules that make complex subjects accessible and manageable, often in 10-minute segments.

This model supports lifelong learning and quick skill acquisition, aligning well with the modern, fast-paced lifestyle and the growing trend towards continuous education. Popularized by platforms like Duolingo, this approach not only facilitates effective learning but also opens up new markets by catering to busy professionals who might not commit to longer study sessions.

Challenge

Keeping Pace with Rapid Technological Changes

One of the main challenges facing the EdTech sector is the rapid pace of technological advancements. The integration of cutting-edge technologies such as AI, AR/VR, and cloud computing into educational platforms requires constant updates and maintenance.

Educational institutions and EdTech providers must stay proactive and adaptable to incorporate these technologies effectively. This not only involves financial investment but also requires ongoing professional development for educators to keep them abreast of new tools and teaching methodologies that can enhance learning experiences and operational efficiencies.

Growth Factors

The growth of the EdTech and digital literacy market is driven by several pivotal factors. Primarily, the global pandemic accelerated the adoption of digital tools in education, creating a lasting impact on how learning is approached. With a shift towards remote and hybrid learning models, the demand for digital platforms that support these methods has surged.

Additionally, the integration of AI and data analytics in education has revolutionized personalized learning, making it possible to tailor educational content to individual needs and learning styles. The emphasis on improving digital literacy across all age groups further fuels this growth, as it’s essential for navigating modern educational and professional environments.

Emerging Trends

Emerging trends in the EdTech sector include the growing use of game-based learning and gamification to enhance student engagement and motivation. Tools that incorporate elements of gaming not only make learning more enjoyable but are shown to improve retention of information.

The expansion of Extended Reality (XR), encompassing Virtual Reality (VR) and Augmented Reality (AR), offers immersive learning experiences that are being increasingly adopted in schools and higher education institutions. Furthermore, the demand for educational resources that support multilingual and multicultural inclusivity is shaping the development of new EdTech products, ensuring accessibility for a diverse global user base.

Impact of AI

AI’s impact on education is profound and multi-faceted. On one hand, AI technologies like ChatGPT provide significant advantages as educational tools, serving as interactive aids for both students and teachers. These tools can act as personal tutors, offering customized learning experiences and supporting a wide range of educational activities.

On the other hand, there are challenges and concerns, such as the potential for promoting intellectual dishonesty and the need for tools to ensure academic integrity. Despite these challenges, the overall contribution of AI to the EdTech sector is seen as overwhelmingly positive, with ongoing innovations aimed at enhancing its effectiveness and ethical use in educational settings.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

Here’s a detailed analysis of the key players in the EdTech and Digital Literacy market, focusing on recent strategic moves like acquisitions and new product launches:

Byju’s has been a notable player in EdTech, continuously expanding through strategic acquisitions. A recent significant move was their acquisition of Aakash Educational Services, enhancing their offerings in the test preparation sector. This strategic acquisition allows Byju’s to broaden its market reach and enhance its product portfolio, particularly in the competitive test prep market.

Coursera has made strides in widening its course offerings and enhancing user engagement through partnerships with tech giants like Google and IBM. These partnerships have allowed Coursera to offer more specialized professional certificates, which cater to individuals aiming to upgrade their skills in high-demand areas such as data science and artificial intelligence.

Khan Academy Known for its strong foothold in the free educational platform space, Khan Academy has consistently improved its user interface and personalized learning experiences. They focus on expanding their resources, particularly in K-12 education, to support more personalized and accessible learning.

Top Key Players in the Market

- Google LLC

- Blackboard Inc.

- Promethean Limited.

- HMH Education Company

- CENTURY Tech

- Microsoft Digital Literacy

- Cisco Systems Inc.

- Mozilla Corporation

- Pearson plc

- Others

Recent Developments

- In January 2025, Promethean announced the upcoming release of its ActivPanel 10 interactive display and ActivSuite software. This new technology aims to give educators more flexibility in how they teach.

- Adobe launched a global initiative in October 2024 to help 30 million learners gain AI literacy, content creation, and digital marketing skills by 2030. The program offers training and certificates through partnerships with Coursera, NGOs, schools, and universities

- BCcampus released the B.C. Digital Literacy Hub in March 2024. This collection of course materials and professional development resources aims to help educators improve their digital literacy skills and teach these skills to students.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 122.4 Bn |

| Forecast Revenue (2034) | USD 790 Bn |

| CAGR (2025-2034) | 20.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Learning Management Systems (LMS), Smart Classrooms, Artificial Intelligence (AI) in Education, Augmented Reality (AR) and Virtual Reality (VR), Gamification and Others), By End User (K-12, Preschool, Higher Education, Others), By Revenue Model (Subscription-Based, Pay-per-Use |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Google LLC, Blackboard Inc., Promethean Limited., HMH Education Company, CENTURY Tech, Microsoft Digital Literacy, Cisco Systems Inc., Mozilla Corporation, Pearson plc, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |