Quick Navigation

- Report Overview

- Key Takeaways

- U.S. Market Size and Growth

- Stage of Investment Analysis

- Education Sector Analysis

- EdTech Vertical Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Top Opportunities Awaiting for Players

- Recent Developments

- Report Scope

Report Overview

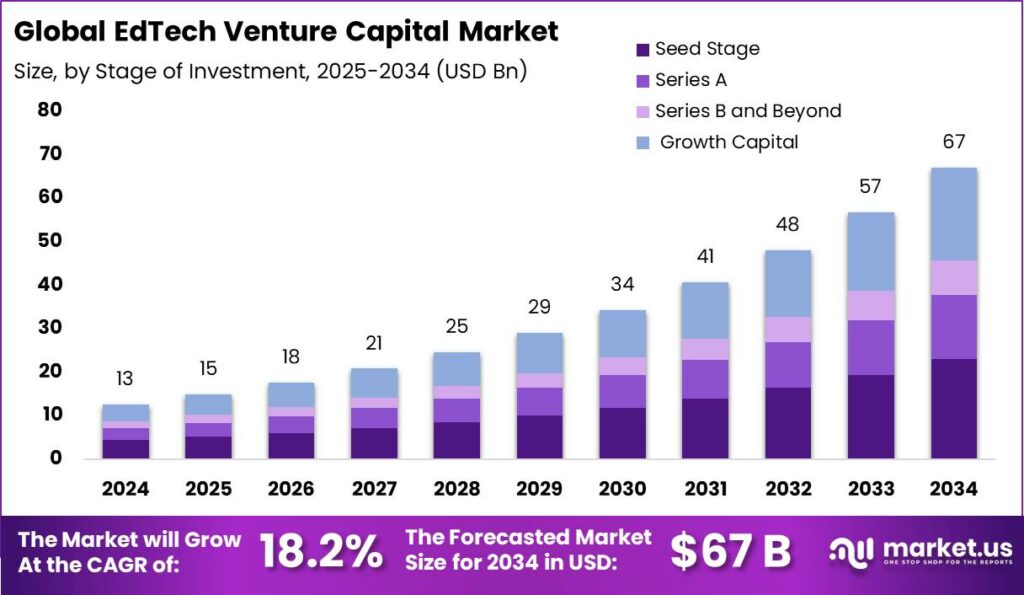

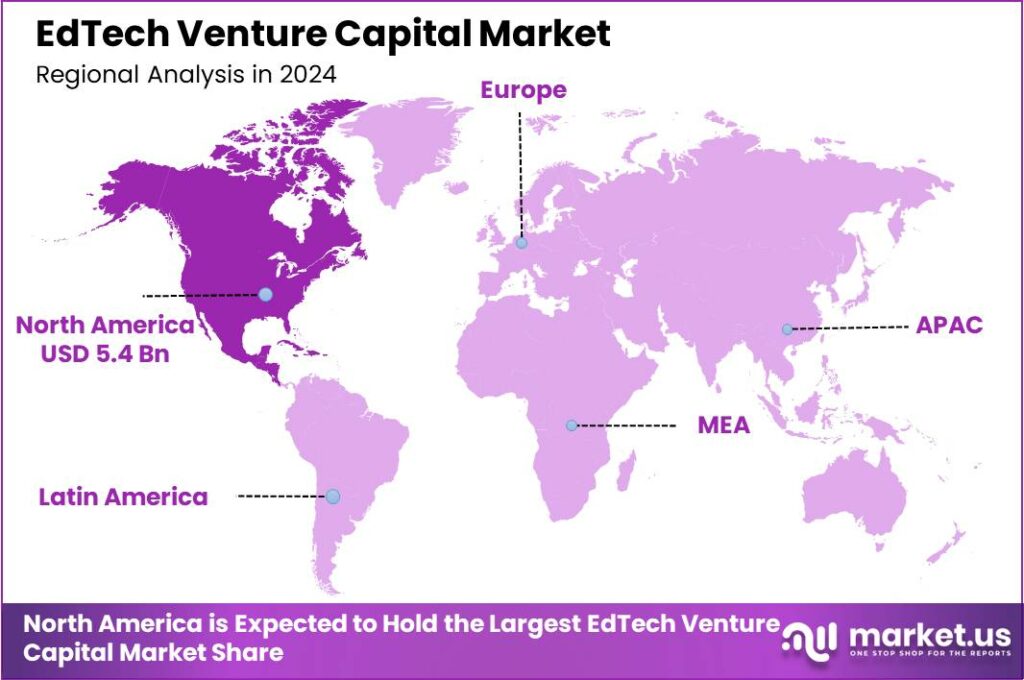

The Global EdTech Venture Capital Market size is expected to be worth around USD 67 Billion By 2034, from USD 12.6 Billion in 2024, growing at a CAGR of 18.20% during the forecast period from 2025 to 2034. In 2024, North America dominated the EdTech venture capital market with over 43.4% market share, totaling around USD 5.4 billion in revenue.

EdTech Venture Capital refers to the specialized segment of venture capital investment that targets startups and companies operating within the educational technology sector. This form of investment focuses on providing capital to businesses that are leveraging technology to enhance learning and educational outcomes.

Venture capital firms in this niche often seek out startups that innovate and disrupt the traditional education models with digital solutions, including learning management systems, e-learning platforms, and educational apps that incorporate advanced technologies such as artificial intelligence and machine learning.

The EdTech venture capital market has experienced significant growth, driven by the increasing integration of technology in education and the rising demand for personalized learning experiences. This market involves various venture capital firms that invest at different stages of company development, from early-stage startups to more established companies aiming to expand and scale.

The primary goal of these investments is not only to generate financial returns but also to foster innovations that can significantly improve educational processes and outcomes on a global scale. The major driving factors of the EdTech venture capital market include the growing demand for accessible and flexible learning solutions, the increasing adoption of mobile devices and internet penetration, and the need for personalized learning approaches.

The COVID-19 pandemic has also accelerated the shift towards online learning and digital educational platforms, highlighting the essential role of technology in modern education. These factors collectively create a fertile environment for EdTech startups, attracting increased attention and investment from venture capitalists.

Market demand in the EdTech sector is robust, driven by both educational institutions and individual learners seeking innovative solutions that cater to diverse learning needs and styles. There is a particular emphasis on platforms that offer adaptive learning technologies, which adjust the educational content based on the learner’s pace and understanding, thereby enhancing learning efficiency and engagement.

According to PitchBook, $2.7 billion was invested in edtech startups across 453 deals in 2024. This marks a significant decline from the sector’s peak in 2021, when VC funding hit $17.2 billion as the pandemic pushed education and training online.

HolonIQ data shows that venture capital in edtech has dropped to its lowest level since 2014, reaching just $2.4 billion in 2024 – a dramatic 89% drop from the 2021 high. Early-stage deals gained prominence as larger funding rounds became scarce. Notable exceptions included PhysicsWallah’s $210 million funding round, alongside major investments in Eruditus, Zum, and SpringHealth.

North America led in funding value, capturing over 50% of global VC investment with about a third of the total deal volume. Europe accounted for roughly 30% of global deals but saw smaller transaction sizes. South Asia stood out with 20% of global deal volume, thanks to mega-rounds like PhysicsWallah’s $210 million and Eruditus’ $150 million, which helped double the region’s funding value compared to the previous year.

Technological advancements are continuously shaping the EdTech sector. Innovations such as AI and machine learning are being integrated into educational software to provide personalized learning experiences. Moreover, advancements in data analytics enable educators and institutions to track progress and adapt teaching methods to improve student outcomes effectively.

For businesses, investing in EdTech offers numerous benefits including access to a booming market poised for long-term growth due to technological integration and educational reforms. EdTech investments allow venture capitalists and firms to contribute to transformative impacts in education while potentially achieving substantial financial returns.

Key Takeaways

- The Global EdTech Venture Capital Market size is projected to reach USD 67 Billion by 2034, growing from USD 12.6 Billion in 2024, with a CAGR of 18.20% during the forecast period from 2025 to 2034.

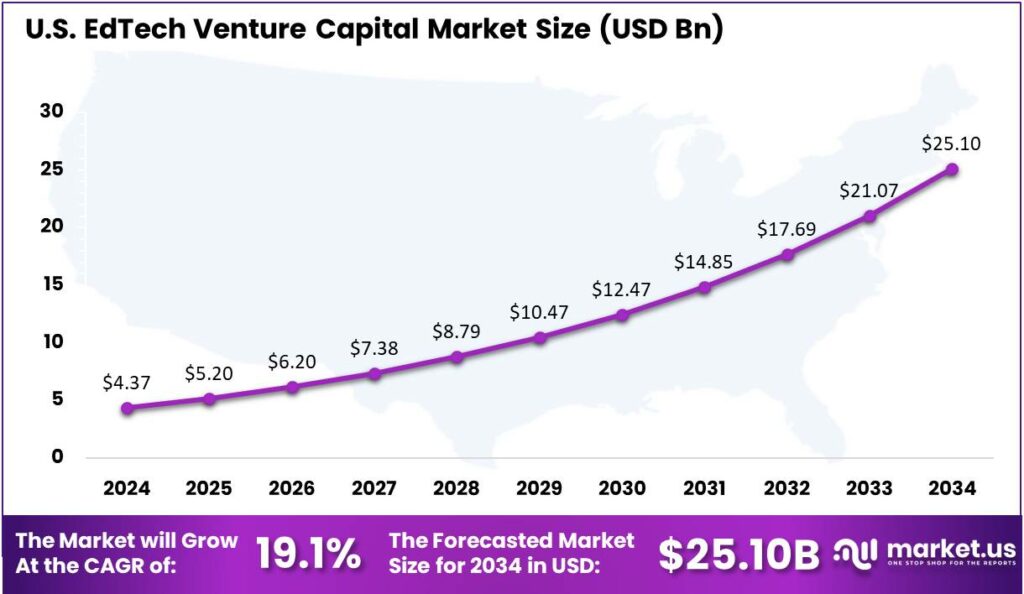

- The U.S. EdTech venture capital market is expected to reach a valuation of $4.37 billion in 2024, driven by a strong CAGR of 19.1%.

- North America is anticipated to maintain a dominant position in the EdTech venture capital market in 2024, holding over 43.4% of the global market share, translating to approximately USD 5.4 billion in revenue.

- In 2024, the Seed Stage segment is projected to capture more than 34.2% of the total market share in the EdTech venture capital market.

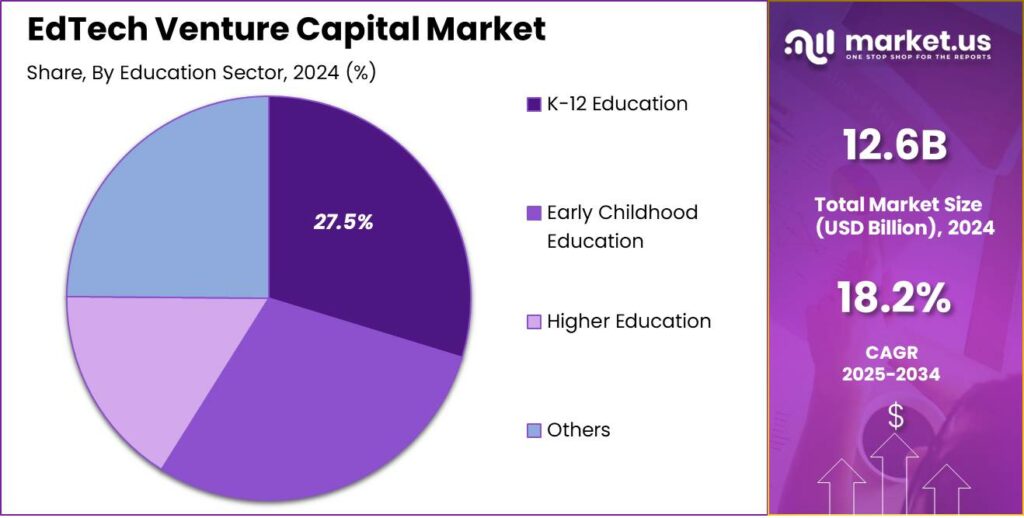

- The K-12 Education segment is expected to hold a dominant position in 2024, accounting for more than 27.5% of the overall market share in EdTech venture capital.

- The Content Delivery Platforms segment is also set to be a leading player in 2024, securing more than 24.6% of the market share in the EdTech venture capital landscape.

U.S. Market Size and Growth

The U.S. EdTech venture capital market is projected to reach a valuation of $4.37 billion in 2024, driven by a robust compound annual growth rate (CAGR) of 19.1%. This significant growth underscores the increasing investor interest in the education technology sector, which continues to be a hotbed for innovation.

The rise of digital learning tools, online platforms, and AI-driven solutions has accelerated demand for investments, as educational institutions, corporations, and individuals embrace technology to enhance learning experiences and outcomes. As a result, EdTech companies are attracting venture capital funding to scale their operations, expand product offerings, and penetrate new markets.

The rapid expansion of the EdTech market is not just a reflection of technological advancement but also of changing educational needs. Increasingly, schools, universities, and even corporate learning environments are adopting technology to cater to a diverse set of learners, ranging from K-12 students to professionals seeking continuous development.

In 2024, North America held a dominant market position in the EdTech venture capital landscape, capturing over 43.4% of the global market share, translating to approximately USD 5.4 billion in revenue. This region leads due to the presence of major tech companies, strong educational infrastructure, and a high adoption rate of digital learning solutions.

The U.S. remains a global leader in EdTech investment, backed by public and private initiatives to transform education through technology. North American venture capital firms are funding companies offering innovative solutions like AI for personalized learning, VR classrooms, and data analytics tools, driving rapid growth in the sector.

The region’s favorable regulations and strong funding ecosystem support its EdTech dominance. U.S. venture capital firms have been early adopters, driving funding into startups. North America’s market share is fueled by high-tech innovation, with universities, research institutions, and EdTech companies collaborating on next-generation learning technologies, attracting continued investment.

Stage of Investment Analysis

In 2024, the Seed Stage segment held a dominant market position in the EdTech venture capital market, capturing more than 34.2% of the total share. This is primarily due to the rising number of early-stage EdTech startups that are exploring innovative ways to disrupt the education industry.

Seed Stage investments are typically the first round of funding, where investors take a higher risk by funding nascent companies with unproven business models and technologies. The dominant share of Seed Stage is attributed to investors’ increasing confidence in the EdTech sector’s potential for growth, despite the inherent risks involved in funding startups.

Seed Stage is leading the market due to a rise in educational tech startups seeking funding for innovative solutions. These startups are leveraging AI, machine learning, and immersive learning tools, attracting strong investor interest.

Seed Stage investments are vital for driving innovation in the EdTech sector. Entrepreneurs at this stage refine products, test markets, and build customer bases. Investors offer not just capital, but also strategic guidance, mentorship, and industry connections essential for early growth and survival.

Education Sector Analysis

In 2024, the K-12 Education segment held a dominant market position, capturing more than a 27.5% share of the overall EdTech venture capital market. This significant share can be attributed to the growing adoption of digital tools across primary and secondary schools.

As the demand for remote and hybrid learning solutions increased, K-12 institutions have become key drivers of EdTech investment. EdTech solutions that cater to this segment are focused on enhancing learning experiences, streamlining classroom management, and providing personalized educational content, which appeals to both educators and parents.

K-12 Education leads the EdTech market due to its broad appeal and urgent need for improvement. EdTech platforms address diverse student needs, enhance teacher-student interaction, and offer innovative solutions like gamification and adaptive learning, creating vast potential for growth in this sector.

Moreover, K-12 Education is undergoing significant transformation due to increased government investments in digital infrastructure. Many countries are prioritizing digital literacy and equitable access to educational resources, making K-12 institutions key adopters of technology.

EdTech Vertical Analysis

In 2024, the Content Delivery Platforms segment held a dominant market position, capturing more than a 24.6% share of the EdTech venture capital market. K-12 Education’s leadership is driven by the global shift to digital learning, especially post-pandemic, as educational institutions, businesses, and learners increasingly turn to online platforms for formal and informal education.

0These platforms have effectively bridged the gap between students and teachers by providing scalable, flexible, and diverse content delivery models, ranging from video lessons to interactive simulations, catering to different learning preferences. This adaptability has made content delivery platforms a cornerstone in the growth of the EdTech sector.

Content Delivery Platforms dominate due to AI-driven personalized learning and mobile-first designs, enabling on-the-go access. As remote and hybrid learning grow, these platforms continue to innovate for more engaging and effective education.

Another key factor contributing to the supremacy of content delivery platforms is the scalability they offer. Unlike traditional educational models that are often constrained by physical infrastructure or location, digital content delivery platforms are accessible worldwide, breaking down geographical barriers and democratizing access to quality education.

Key Market Segments

By Stage of Investment

- Seed Stage

- Series A

- Series B and Beyond

- Growth Capital

By Education Sector

- Early Childhood Education

- K-12 Education

- Higher Education

- Others

By EdTech Vertical

- Content Delivery Platforms

- Test Preparation

- Language Learning

- STEM Learning

- Lifelong Learning

- Edutainment

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Growing Demand for Digital Learning Solutions

The EdTech sector is experiencing significant growth, primarily driven by the increasing demand for digital learning solutions. As more people and institutions shift toward online learning, especially post-pandemic, the adoption of educational technologies has accelerated.

Schools, colleges, universities, and corporations are investing in digital tools that enable personalized learning experiences, access to a wide range of resources, and improved student outcomes. The need for remote learning solutions, learning management systems, and digital collaboration tools continues to expand as education becomes more accessible to diverse groups, including those in remote or underserved areas.

Restraint

Regulatory Challenges

One major restraint faced by the EdTech industry is navigating complex and varying regulations across different regions and countries. Education systems and requirements differ from one jurisdiction to another, creating difficulties for EdTech companies to offer solutions that comply with local laws and standards.

In some countries, data privacy laws like GDPR in Europe impose strict regulations on how student information is collected, stored, and used, making it harder for EdTech platforms to operate across borders. Additionally, the lack of standardized regulations within the sector itself can lead to confusion, delays in product development, and increased costs for companies trying to ensure compliance.

Opportunity

Personalized Learning through AI

One of the biggest opportunities in the EdTech space lies in the development of AI-driven personalized learning platforms. Artificial intelligence has the potential to revolutionize education by offering adaptive learning solutions that cater to the unique needs, abilities, and interests of individual learners.

AI algorithms can analyze student data to identify their strengths and weaknesses, creating tailored lesson plans that ensure more effective learning outcomes. This shift from one-size-fits-all education to customized, learner-centric models can help address issues like low engagement and high dropout rates. Furthermore, AI-powered platforms can provide instant feedback and real-time assessments, helping learners stay on track and allowing educators to intervene when necessary.

Challenge

User Engagement and Retention

A significant challenge faced by EdTech companies is ensuring user engagement and retention. While the growth of online learning platforms is undeniable, keeping students motivated and engaged remains a difficult task. In traditional classrooms, the physical presence of a teacher and peer interactions play a crucial role in maintaining student focus.

However, online education often lacks these elements, which can lead to decreased engagement. Furthermore, the digital learning environment presents numerous distractions for students, from social media to personal devices. For EdTech startups, creating a platform that is not only educational but also engaging and motivating is a major hurdle.

Emerging Trends

One of the most prominent trends is the integration of Artificial Intelligence (AI) and Machine Learning (ML) into educational platforms. These technologies are used to personalize learning experiences, analyze student behavior, and improve learning outcomes by providing tailored educational content.

Another emerging trend is the increased focus on lifelong learning and upskilling. With the rise of remote work and the rapid pace of technological advancement, individuals are increasingly looking for flexible, on-demand learning solutions to remain competitive in the job market.

EdTech companies are responding by offering micro-learning opportunities, short courses, and skill-based training that cater to adult learners. Moreover, the expansion of virtual reality (VR) and augmented reality (AR) in EdTech is creating immersive learning environments that engage students in new and exciting ways.

Business Benefits

One of the key business benefits is the ability to tap into a global market. With education becoming more accessible through online platforms, businesses have the potential to reach millions of learners across different geographies.

Another significant benefit is that EdTech solutions can foster better engagement and retention in educational settings. By leveraging AI and adaptive learning systems, companies can provide personalized learning experiences that improve student outcomes.

Investing in EdTech also promotes innovation within the education sector. As educational tools become more advanced, businesses that develop these tools can revolutionize how learning is delivered, making it more accessible, inclusive, and effective.

Moreover, investing in EdTech aligns businesses with broader trends in corporate social responsibility (CSR). By supporting education, companies can position themselves as ethical investors, reinforcing their reputation as forward-thinking and socially responsible entities.

Key Player Analysis

The EdTech venture capital market is experiencing rapid growth, with several key players driving innovation and investments in education technology startups.

Learn Capital is one of the leading EdTech venture capital firms. Known for its deep expertise in education, Learn Capital invests in companies that leverage technology to transform the education system. They focus on supporting startups that can scale and bring about systemic change, helping improve accessibility and learning outcomes for students globally.

Owl Ventures is another major player in the EdTech VC space. This firm focuses on high-growth education technology companies, especially those that are changing the way people learn. Owl Ventures has a strong track record of investing in businesses that use technology to enhance student engagement, improve education delivery, and increase learning outcomes.

Reach Capital is also a significant investor in the EdTech market. Reach Capital emphasizes supporting startups that use technology to create equitable access to quality education. They focus on early-stage companies that address unmet needs in education, particularly in underserved communities.

Top Key Players in the Market

- Learn Capital

- Owl Ventures

- Reach Capital

- GSV Ventures

- Rethink Capital Partners

- Sequoia Capital Operations, LLC

- Accel Partners

- Andreessen Horowitz

- Kleiner Perkins

- Lightspeed Venture Partners

- Others

Top Opportunities Awaiting for Players

- AI-Driven Personalized Learning: AI in education offers EdTech companies the chance to provide personalized learning, adapting lessons to individual paces and styles. This boosts understanding and skill development. Investors should focus on platforms using AI for real-time feedback and learning path optimization, as demand for personalized education continues to rise.

- Hybrid and Remote Learning Solutions: The pandemic changed the way education is delivered, with hybrid and remote learning becoming the norm for many institutions. EdTech companies that focus on tools for online assessments, collaboration, and virtual campus solutions are well-positioned for growth in a market where remote learning is now mainstream.

- Skill Development and Lifelong Learning: As the job market evolves, there is a growing emphasis on upskilling and reskilling.Investors should look at platforms that offer flexible, accessible learning options to help individuals transition into new careers or enhance their existing skills. This market offers immense growth potential, particularly in areas like tech, healthcare, and digital marketing.

- Global EdTech Expansion: Companies that can offer affordable, scalable solutions tailored to local needs are well-positioned to capture these untapped markets. From mobile learning apps to low-cost digital classrooms, investors should explore opportunities in regions like Southeast Asia, Africa, and Latin America, where demand for online learning tools is expected to soar.

- Education for Special Needs: EdTech solutions that focus on helping students with learning disabilities, autism, or physical impairments are gaining traction. Investors should look for opportunities to support companies that design adaptive learning tools, assistive technologies, and inclusive platforms that empower these students to succeed in education.

Recent Developments

- In April 2024, The ex-COO of Unacademy has successfully raised $11 million for his new edtech venture, securing backing from prominent investors Matrix Partners and Lightspeed. This funding marks a significant step in the launch of his next venture in the education technology space.

- In November 2024, Bhanzu, the math learning startup backed by Lightspeed, is now in advanced talks to raise approximately Rs 130-140 crore (around $16-$17 million) in a fresh funding round.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 12.6 Bn |

| Forecast Revenue (2034) | USD 67 Bn |

| CAGR (2025-2034) | 18.20% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Stage of Investment (Seed Stage, Series A, Series B and Beyond, Growth Capital), By Education Sector (Early Childhood Education, K-12 Education, Higher Education, Others), By EdTech Vertical (Content Delivery Platforms, Test Preparation, Language Learning, STEM Learning, Lifelong Learning, Edutainment, Others), |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Learn Capital, Owl Ventures, Reach Capital, GSV Ventures, Rethink Capital Partners, Sequoia Capital Operations, LLC, Accel Partners, Andreessen Horowitz, Kleiner Perkins, Lightspeed Venture Partners, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |