Quick Navigation

Market Overview

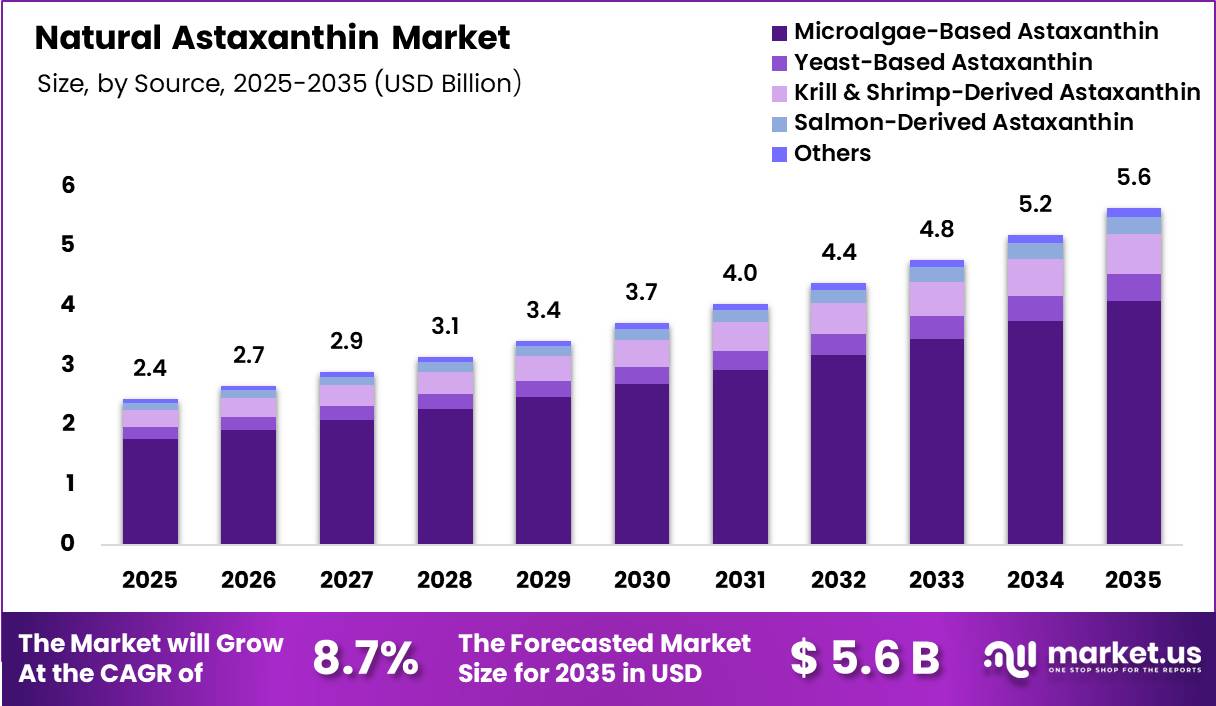

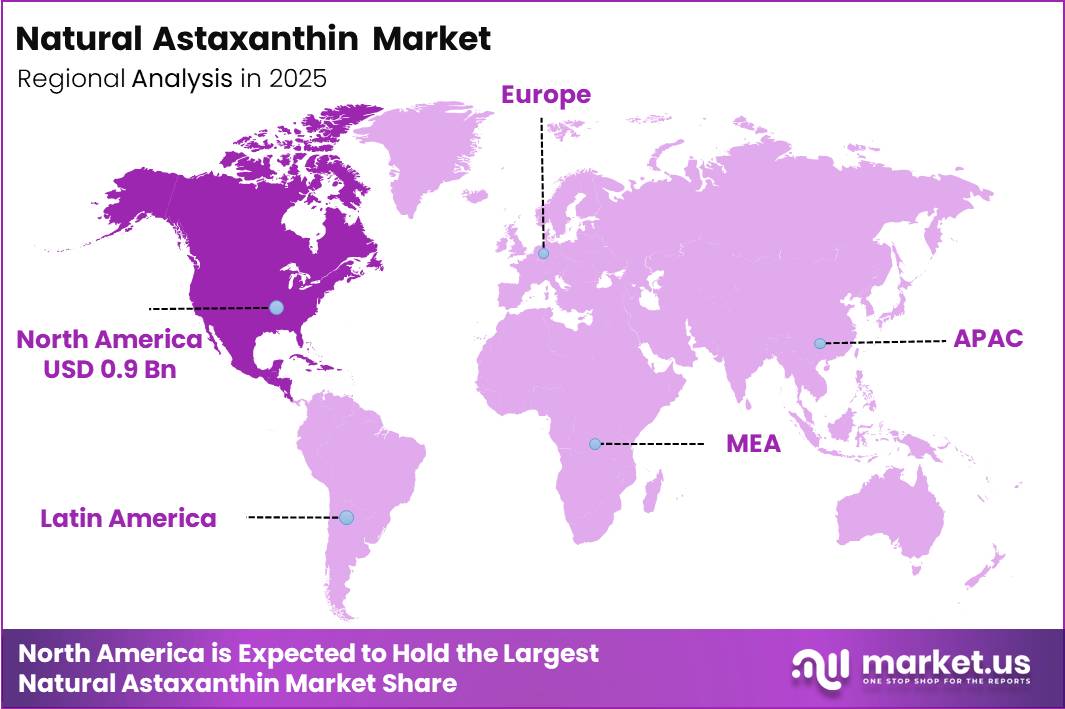

Global Natural Astaxanthin Market size is expected to be worth around US$ 5.6 Billion by 2035 from US$ 2.4 Billion in 2025, growing at a CAGR of 8.7% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 35.6% share with a revenue of US$ 0.9 Billion.

The global Natural Astaxanthin market is witnessing steady expansion driven by rising consumer awareness of preventive healthcare and increasing demand for natural antioxidants. Astaxanthin is a red carotenoid primarily derived from the microalgae Haematococcus pluvialis, widely recognized for its strong antioxidant potential and bioavailability.

According to biomedical literature indexed by the National Library of Medicine (NIH), astaxanthin exhibits antioxidant activity significantly higher than many common carotenoids, making it highly relevant in nutraceutical and functional food applications.

The compound is increasingly used in dietary supplements, cosmetics, and aquaculture feed due to its reported role in supporting skin health, eye function, cardiovascular wellness, and immune balance. Clinical studies indicate typical supplementation ranges between 4 mg to 12 mg per day in adults, with research showing potential benefits in reducing oxidative stress and inflammation biomarkers.

Government and academic health sources highlight that oxidative stress is a key contributor to chronic diseases, including cardiovascular and metabolic disorders, strengthening the demand for antioxidant-based preventive nutrition strategies. Natural astaxanthin is also valued for its stability and lipid-soluble structure, which enhances absorption when consumed with dietary fats.

Growing consumer shift toward plant-based and algae-derived ingredients is further accelerating market adoption. In addition, increasing use in skincare formulations is supported by evidence suggesting improved skin elasticity and UV protection properties.

With expanding applications across nutraceutical, pharmaceutical, and cosmetic industries, natural astaxanthin is positioned as a high-value bioactive ingredient in the global health and wellness market landscape.

Key Takeaways

- Market Size: Global Natural Astaxanthin Market size is expected to be worth around US$ 5.6 Billion by 2035 from US$ 2.4 Billion in 2025.

- Market Share: The market is growing at a CAGR of 8.7% during the forecast period from 2026 to 2035.

- Source: Microalgae-Based Astaxanthin dominates the source segment with a 72.3% market share in 2025.

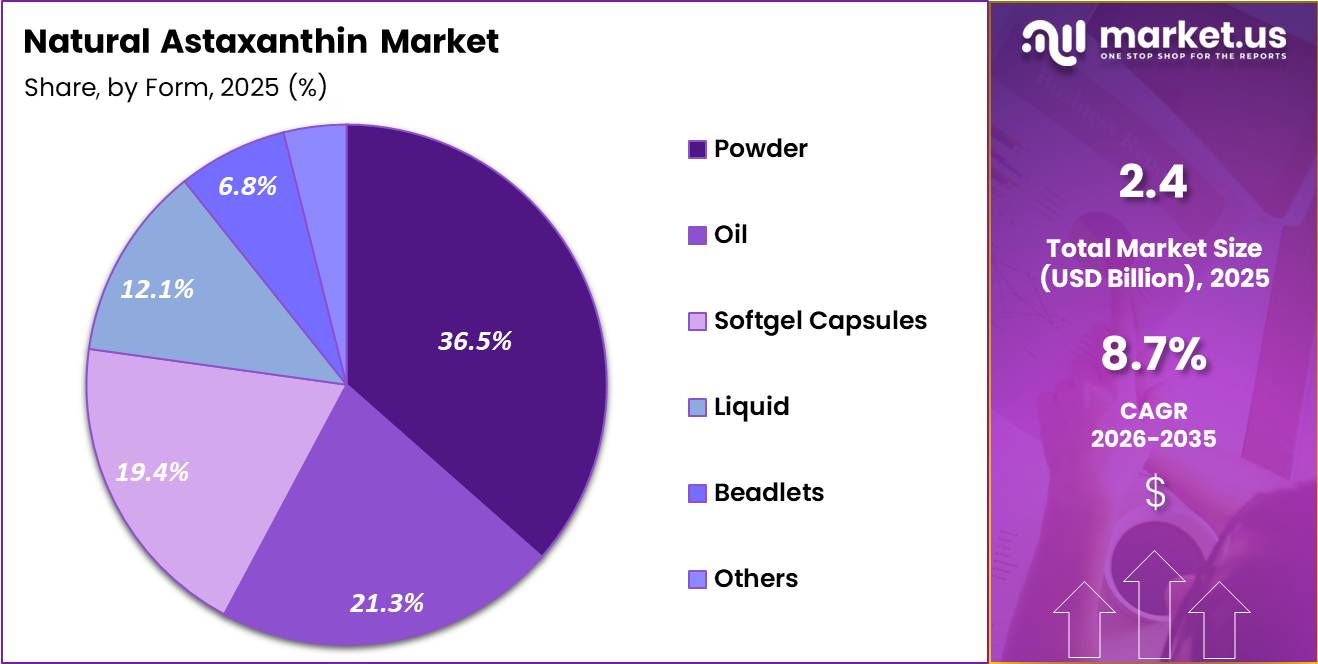

- Form: The Powder segment dominated the Natural Astaxanthin Market, accounting for 36.5% of total market revenue in 2025.

- Application: Nutraceuticals & Dietary Supplements dominate the application segment with a 44.5% market share in 2025.

- Distribution Channel: Business-to-Business (B2B) dominates the distribution channel segment with a 68.7% share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 35.6% share with a revenue of US$ 0.9 Billion.

Source Analysis

Microalgae-Based Production Leads Due to High Purity, Scalability, and Strong Nutraceutical Demand.

The Natural Astaxanthin Market is primarily segmented by source into Microalgae-Based Astaxanthin, Yeast-Based Astaxanthin, Krill & Shrimp-Derived Astaxanthin, Salmon-Derived Astaxanthin, and Others. Microalgae-Based Astaxanthin dominates the market with a 72.3% share in 2025, owing to its status as the most sustainable, pure, and commercially scalable source of natural astaxanthin.

Derived mainly from Haematococcus pluvialis, it is widely preferred in nutraceuticals and dietary supplements due to its high antioxidant potency and clean-label positioning. Increasing consumer preference for plant-based and vegan ingredients further strengthens its dominance.

Yeast-Based Astaxanthin holds an 8.0% share, supported by its controlled fermentation process and consistent quality output, while Krill & Shrimp-Derived Astaxanthin accounts for 12.0%, driven by its utilization in marine-based extraction processes.

Salmon-Derived Astaxanthin represents 5.0%, mainly used in niche applications linked to aquaculture and animal nutrition. The Others category holds 2.7%, covering emerging synthetic-free and hybrid extraction sources. Growing regulatory preference for natural and non-GMO ingredients continues to reinforce microalgae’s leadership in this segment.

Powder Form Dominates Owing to Stability, Versatility, and Wide Nutraceutical Integration.

The Natural Astaxanthin Market by form is segmented into Powder, Oil, Softgel Capsules, Liquid, Beadlets, and Others. Powder dominates the segment with a 36.5% market share in 2025, driven by its versatility, long shelf life, and ease of blending into dietary supplements, functional foods, and beverage formulations.

Its stability and cost-effectiveness make it the preferred choice for large-scale manufacturers. Oil-based astaxanthin is widely used due to its high bioavailability and compatibility with softgel encapsulation processes, especially in nutraceutical applications.

Softgel Capsules continue to grow steadily, supported by rising consumer demand for convenient dosage formats and premium supplement products. Liquid formulations are gaining traction in functional beverages and cosmetic applications due to fast absorption properties.

Beadlets are increasingly adopted in controlled-release formulations, improving stability and targeted delivery. The Others category includes emerging formats used in experimental and specialty applications. Overall, innovation in delivery systems and rising demand for convenient, bioavailable formats are shaping the evolution of this segment.

Application Analysis

Nutraceuticals Lead Market Growth on Strong Antioxidant Demand and Preventive Healthcare Trends.

The Natural Astaxanthin Market by application is segmented into Nutraceuticals & Dietary Supplements, Food & Beverages (Animal Feed, Aquaculture Feed, Poultry Feed, Pet Food), Livestock Feed, Cosmetics & Personal Care, Pharmaceuticals, and Others.

Nutraceuticals & Dietary Supplements dominate the market with a 44.5% share in 2025, driven by rising consumer awareness of antioxidant benefits, immune support, and anti-aging properties. Increasing health consciousness and preventive healthcare trends continue to support strong demand.

Food & Beverages applications, particularly in aquaculture and animal feed, represent a significant growth area due to astaxanthin’s role in enhancing pigmentation, growth, and overall animal health. Livestock feed applications are expanding steadily with rising demand for natural feed additives.

Cosmetics & Personal Care segments are gaining momentum due to astaxanthin’s anti-aging and skin-protective properties, especially in premium skincare formulations. Pharmaceutical usage remains niche but growing, supported by ongoing research into therapeutic benefits. The Others category includes emerging industrial and specialty applications. Overall, health-driven consumption trends are shaping market expansion.

Distribution Channel Analysis

B2B Channel Dominates Due to Bulk Supply, Industrial Demand, and Long-Term Supply Agreements.

The Natural Astaxanthin Market by distribution channel is segmented into Business-to-Business (B2B) and Business-to-Consumer (B2C), with B2B dominating at 68.7% share in 2025. This dominance is attributed to strong bulk procurement by nutraceutical manufacturers, food and beverage companies, cosmetics producers, and animal feed industries.

B2B channels ensure consistent supply chains, cost efficiency, and large-scale formulation integration, making them the backbone of the market. Direct contracts with ingredient suppliers and long-term partnerships further strengthen this segment’s leadership.

B2C channels, including Online Retail, Supermarkets & Hypermarkets, Specialty Health Stores, Pharmacies & Drug Stores, and Others, are steadily expanding due to rising consumer preference for direct supplement purchases and e-commerce-driven health product accessibility.

Online retail is particularly growing due to convenience and wider product availability. Specialty health stores and pharmacies continue to play an important role in trust-based purchasing of nutraceutical products. Overall, while B2C is gaining momentum, B2B remains the dominant distribution channel due to industrial-scale demand and structured procurement systems.

Key Market Segments

Source

- Microalgae-Based Astaxanthin

- Yeast-Based Astaxanthin

- Krill & Shrimp-Derived Astaxanthin

- Salmon-Derived Astaxanthin

- Others

Form

- Powder

- Oil

- Softgel Capsules

- Liquid

- Beadlets

- Others

Application

- Nutraceuticals & Dietary Supplements

- Food & Beverages

- Animal Feed

- Aquaculture Feed

- Poultry Feed

- Pet Food

- Livestock Feed

- Cosmetics & Personal Care

- Pharmaceuticals

- Others

Distribution Channel

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- Online Retail

- Supermarkets & Hypermarkets

- Specialty Health Stores

- Pharmacies & Drug Stores

- Others

Opportunity

Natural aquafeed substitution is a significant opportunity because naturally derived astaxanthin is increasingly being used as an alternative to synthetic pigmentation ingredients in salmonid aquaculture.

Regulatory frameworks permit astaxanthin inclusion at up to 80 mg/kg of finished salmonid feed, supporting its commercial adoption. Research has shown that Haematococcus pluvialis-derived astaxanthin can deliver strong pigmentation performance and enhanced coloration in fish.

Beyond pigmentation, natural astaxanthin offers benefits related to antioxidant status and feed utilization, strengthening its value proposition in premium aquafeed formulations. Demand is particularly strong in salmon and trout production, where flesh color is a critical quality attribute.

Even modest improvements in coloration and product quality can enhance market acceptance and downstream value realization. As a result, natural astaxanthin is emerging as a premium ingredient in high-value aquaculture nutrition programs.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Functional food fortification | +2.0% | North America, EU, Japan, South Korea | Short term |

| Premium skin-health nutricosmetics | +1.8% | Japan, South Korea, EU, North America | Short term |

| Natural aquafeed substitution | +2.3% | Norway, Chile, Scotland, Japan, China | Medium term |

| Supercritical extraction scale-up | +1.5% | EU, Israel, India, China | Medium term |

| Clinical-positioned eye health lines | +1.7% | Japan, EU, North America | Medium term |

| Algae-platform biorefinery models | +2.1% | APAC manufacturing hubs, EU, North America | Long term |

Drivers

Supplement safety framework expansion is a major market driver because increasing regulatory clarity is improving confidence in the use of natural astaxanthin for human consumption. Safety assessments have confirmed that adult intake of up to 8 mg/day from supplements remains within established safety limits when combined with normal dietary exposure.

This reduces uncertainty around dosage recommendations and product formulation strategies. Greater regulatory alignment also supports the use of astaxanthin-rich Haematococcus pluvialis ingredients in consumer health products.

As a result, manufacturers can develop more standardized supplement formats with stronger compliance support and clearer labeling. Improved safety recognition helps accelerate retailer acceptance and facilitates product launches across multiple markets. This regulatory foundation is enabling natural astaxanthin to move beyond niche antioxidant applications into broader wellness and nutrition categories.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supplement safety framework expansion | +1.8% | North America, EU, Japan | Short term |

| Human clinical validation in eye and skin health | +2.0% | Japan, South Korea, EU, North America | Medium term |

| Natural pigment demand in aquafeed | +2.2% | Norway, Chile, Scotland, Japan, China | Medium term |

| Extraction efficiency improvements | +1.4% | EU, India, China, Israel | Medium term |

| Microalgae platform scale-up | +1.6% | APAC manufacturing hubs, EU, North America | Long term |

| Premium clean-label antioxidant positioning | +1.5% | North America, EU, South Korea, Australia | Short term |

Challenges

Contamination-prone algae systems remain a major challenge because Haematococcus pluvialis grows relatively slowly, making it highly susceptible to contamination by bacteria, fungi, and faster-growing competing microorganisms.

Maintaining axenic (contamination-free) cultivation remains difficult across both open and closed production systems. The challenge becomes more severe in tropical and variable-climate environments where biological contamination pressure is higher.

Contamination can disrupt cultivation before the critical red-stage induction phase, reducing biomass quality and astaxanthin productivity. This increases batch failure risk and lowers effective production yields.

Producers also face higher sterilization, monitoring, and facility-maintenance requirements. Additional downtime between cultivation cycles further limits operational efficiency. As a result, contamination risks continue to constrain large-scale production reliability and consistent supply quality.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| High cultivation cost | -1.8% | Global, strongest in EU and APAC production hubs | Medium term |

| Contamination-prone algae systems | -1.3% | India, China, Southeast Asia, warm-climate sites | Medium term |

| Extraction and purification losses | -1.2% | Global processing centers | Short term |

| Stability and isomerization risk | -1.0% | Global, especially nutraceutical and food formats | Medium term |

| Regulatory dosage ceilings | -0.9% | EU, UK, export-oriented brands | Medium term |

| Bioavailability standardization gaps | -1.1% | North America, EU, Japan | Long term |

Restraints

Yield losses in processing remain a major restraint because astaxanthin recovery depends on multiple tightly controlled stages, including cell disruption, extraction, purification, and stabilization.

Scientific studies have shown that near-maximum recovery is achievable only under carefully optimized supercritical CO₂ extraction conditions, highlighting the narrow operating window required for efficient production. Small deviations in biomass quality, moisture content, pressure control, or solvent handling can reduce extractable astaxanthin and increase process waste.

Recovery losses at any stage directly lower the amount of commercially usable active ingredient obtained from each batch. This raises the cost of producing standardized astaxanthin ingredients and reduces overall manufacturing efficiency.

Processing variability also makes supply planning and quality consistency more difficult. As a result, yield losses continue to constrain scalable production and broader adoption in cost-sensitive application areas.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost base | -2.0% | Global, strongest in EU and APAC production hubs | Medium term |

| Dosage ceiling and age limits | -1.3% | EU, UK, export-oriented nutraceutical markets | Medium term |

| Feed-use concentration caps | -1.0% | North America, aquaculture export corridors | Short term |

| Yield losses in processing | -1.2% | Global processing centers | Short term |

| Formulation stability weakness | -1.1% | Global, especially food and beverage formats | Medium term |

| Narrow pediatric addressability | -0.8% | EU, UK, regulated supplement channels | Long term |

Regional Analysis

North America Leads While Asia Pacific Emerges as Fastest-Growing Region in Natural Astaxanthin Market.

In 2025, the regional landscape of the Natural Astaxanthin Market is characterized by strong concentration in developed economies alongside accelerating growth in emerging regions. North America dominates the global market, holding over 35.6% share and generating approximately US$ 0.9 Billion in revenue.

This leadership is driven by high consumer awareness of dietary supplements, widespread adoption of preventive healthcare practices, and strong demand for natural antioxidants in nutraceutical and functional food applications. Advanced distribution networks and strong presence of health-focused product manufacturers further reinforce regional dominance.

Europe follows as a mature and steady market, supported by increasing demand for natural ingredients in cosmetics, anti-aging skincare, and functional nutrition products. Strict regulatory frameworks promoting clean-label and natural formulations also contribute to consistent adoption.

Asia Pacific is emerging as the fastest-growing region, fueled by expanding aquaculture industries, rising disposable incomes, and growing awareness of health supplements in countries such as China, Japan, and India. Rapid urbanization and increasing focus on preventive healthcare further strengthen demand.

Meanwhile, Latin America and the Middle East & Africa are witnessing gradual uptake, primarily driven by aquaculture expansion and improving awareness of antioxidant benefits. Overall, the market reflects a dual structure where developed regions dominate revenue while emerging economies drive future growth momentum.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

The Natural Astaxanthin Market is moderately consolidated, with a mix of established global biotechnology firms and specialized algae-based producers competing in a highly innovation-driven environment. Competitive dynamics are shaped by strong emphasis on sustainable cultivation technologies, high-purity extraction processes, and expanding applications across nutraceuticals, cosmetics, and aquaculture.

Leading players continuously invest in R&D to improve bioavailability, scalability, and cost efficiency while strengthening their positions through strategic partnerships and integrated production ecosystems.

Key companies such as Cyanotech Corporation, Algatech Ltd., Fuji Chemical Industries Co., Ltd., and BASF SE focus heavily on large-scale microalgae cultivation systems and advanced extraction technologies to ensure consistent product quality.

Valensa International, AstaReal AB, and Beijing Ginko Group (BGG) emphasize clinical validation and branded ingredient development to differentiate in premium supplement segments. Meanwhile, Piveg, Inc., Algamo s.r.o., and Algalif Iceland are strengthening sustainability-led production models, leveraging closed-loop and environmentally controlled cultivation systems.

Fenchem Biotek Ltd., Divis Laboratories Ltd., and Parry Nutraceuticals focus on cost-efficient manufacturing and expansion into functional nutrition markets, while Heliae Development LLC and Igene Biotechnology, Inc. prioritize biotechnology innovation and downstream application development.

Across the ecosystem, companies are increasingly engaging in partnerships, contract manufacturing, and supply chain integration to enhance scalability and global reach. Overall, competition is defined by continuous innovation, sustainability alignment, and ecosystem-based collaboration rather than price-based rivalry alone.

Top Key Players

- Cyanotech Corporation

- Algatech Ltd.

- Fuji Chemical Industries Co., Ltd.

- BASF SE

- Valensa International

- AstaReal AB

- Beijing Ginko Group (BGG)

- Piveg, Inc.

- Algamo s.r.o.

- Algalif Iceland

- Fenchem Biotek Ltd.

- Divis Laboratories Ltd.

- Parry Nutraceuticals

- Heliae Development LLC

- Igene Biotechnology, Inc.

- Other Key Players

Recent Developments

- In May 2026, AstaReal AB (Market Expansion): AstaReal strengthened its international marketing and customer outreach by participating in Vitafoods Europe 2026, highlighting its latest natural astaxanthin innovations and expanding collaboration opportunities with global dietary supplement and functional food manufacturers.

- In August 2025, Algalif Iceland ehf. advanced its continuous cultivation footprint through its customized indoor photobioreactor and LED infrastructure to support global supply of its premium, carbon-neutral Haematococcus pluvialis microalgae biomass.

- In September 2025, Fuji Chemical Industries Co., Ltd. (AstaReal Group) was officially awarded the Editor’s Award for Infant and Child Nutrition Initiative at the NutraIngredients-Asia Awards 2025 for completing the world’s first pediatric clinical trial on astaxanthin for digital eye strain.

- In June 2025, Cyanotech Corporation announced in its fiscal year financial report that strategic operational optimizations at its Hawaii microalgae facility successfully reduced its annual operating loss to USD 2,508,000, down from USD 4,592,000 the previous year.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 2.4 Billion |

| Forecast Revenue (2035) | US$ 5.6 Billion |

| CAGR (2026-2035) | 8.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Microalgae-Based Astaxanthin, Yeast-Based Astaxanthin, Krill & Shrimp-Derived Astaxanthin, Salmon-Derived Astaxanthin, Others), By Form (Powder, Oil, Softgel Capsules, Liquid, Beadlets, Others), By Application (Nutraceuticals & Dietary Supplements, Food & Beverages, Livestock Feed, Cosmetics & Personal Care, Pharmaceuticals, Others), By Distribution Channel (Business-to-Business (B2B), Business-to-Consumer (B2C) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Cyanotech Corporation, Algatech Ltd., Fuji Chemical Industries Co., Ltd., BASF SE, Valensa International, AstaReal AB, Beijing Ginko Group (BGG), Piveg, Inc., Algamo s.r.o., Algalif Iceland, Fenchem Biotek Ltd., Divis Laboratories Ltd., Parry Nutraceuticals, Heliae Development LLC, Igene Biotechnology, Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |