Quick Navigation

Report Overview

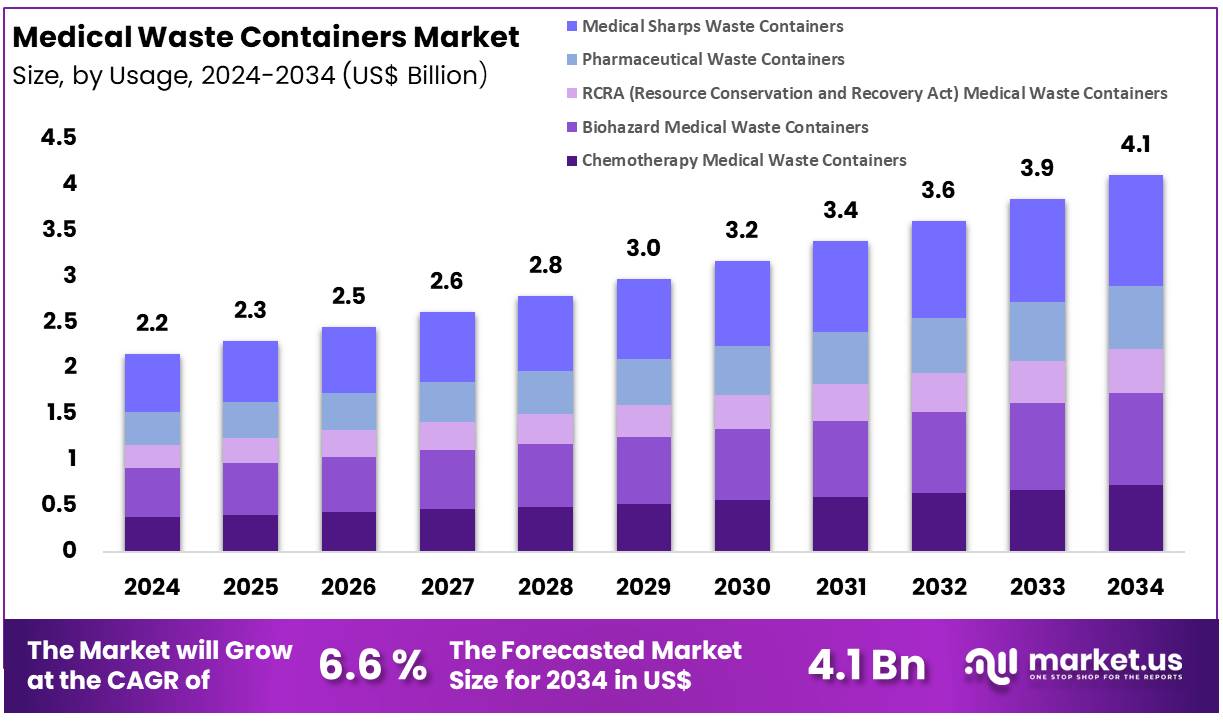

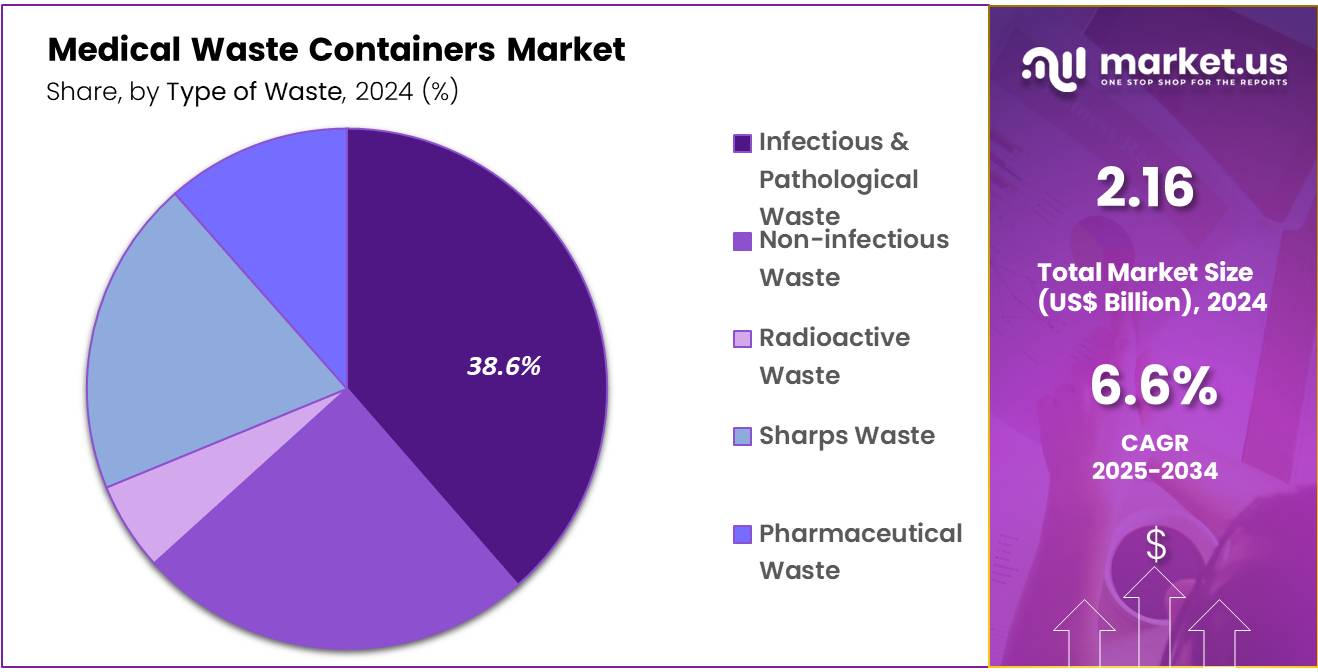

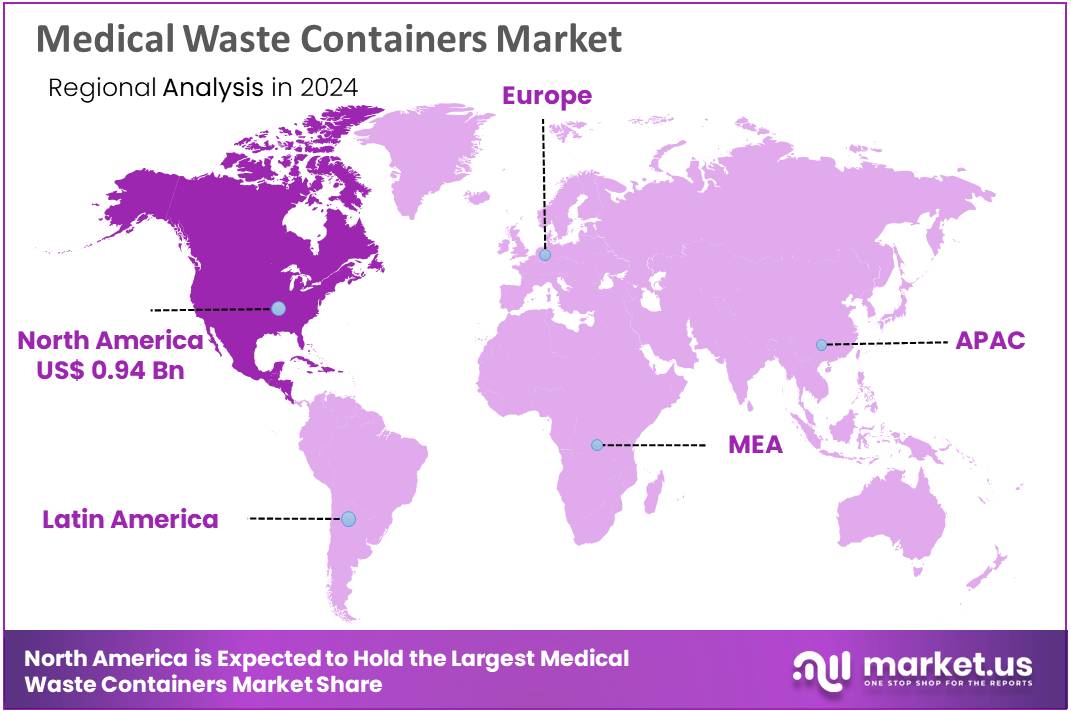

The Global Medical Waste Containers Market size is expected to be worth around US$ 4.1 Billion by 2033 from US$ 2.16 Billion in 2024, growing at a CAGR of 6.6% during the forecast period from 2024 to 2033. In 2023, North America led the market, achieving over 43.60% share with a revenue of US$ 0.94 Billion.

The surge in healthcare activities fueled by the aging population, rising prevalence of chronic diseases, and growing healthcare infrastructure is significantly driving the growth of medical waste container market. These factors contribute to the escalating volume of medical waste, necessitating the use of specialized containment solutions to ensure safe and compliant disposal.

- High-income countries produce an average of up to 0.5 kg of hazardous waste per hospital bed daily, whereas low-income countries generate approximately 0.2 kg per hospital bed each day.

- Healthcare activities generate waste that is roughly 85% general and non-hazardous, while the remaining 15% consists of hazardous materials. These hazardous materials may pose risks such as being infectious, toxic, carcinogenic, flammable, corrosive, reactive, explosive, or radioactive.

Stringent regulatory frameworks imposed by governments worldwide further propel market growth by compelling healthcare facilities to adopt approved medical waste containers. Additionally, increasing awareness of the environmental and public health risks associated with improper waste disposal has spurred the adoption of advanced and eco-friendly containment systems.

- The regulatory framework for environmental management in India’s healthcare sector is established by the Bio-Medical Waste Rules, initially drafted in 1998 and amended in 2000 and 2003. These rules apply to all individuals and institutions involved in the generation or handling of healthcare waste in any form.

The market presents significant opportunities, especially in emerging economies where rapid expansion of healthcare infrastructure is underway. Regions like Asia-Pacific and Latin America show substantial growth potential driven by increased investments in healthcare facilities and waste management systems.

Additionally, the escalating demand for sustainable solutions, including biodegradable and recyclable medical waste containers, creates a promising avenue for innovation. The incorporation of smart technologies, such as IoT-enabled waste management systems that track container usage and enhance disposal processes, is anticipated to further fuel market expansion.

- In India, government health expenditure increased to 1.9% of GDP in the fiscal year 2023-24. While China’s health expenditure has surged from less than 500 billion yuan in 2000 to over nine trillion yuan in 2023.

High costs associated with advanced medical waste containers can limit adoption, particularly among small-scale healthcare providers in resource-constrained settings. A lack of awareness about proper waste management practices in some low-income regions further hinders market expansion. Moreover, the complex regulatory landscape, with varying requirements across countries, poses challenges for manufacturers seeking to ensure compliance and streamline operations globally.

Key Takeaways

- The Medical Waste Containers Market generated a revenue of US$ 2.16 Billion in 2024 and is predicted to reach US$ 3.85 Billion, with a CAGR of 6.6%.

- Based on the Usage, the Medical Sharps Waste Containers segment generated the most revenue for the market with a market share of 29.3%.

- Based on the Type of Waste, the Infectious & Pathological Waste segment generated the most revenue for the market with a market share of 38.6%.

- By Product, the Disposable Medical Waste Containers segment contributed the most to the market and secured a market share of 72.6%.

- Region-wise North America remained the lead contributor to the market, by claiming the highest market share, amounting to 43.60%.

By Usage Analysis

In 2024, Medical Sharps Waste Containers dominated the usage segment of the Medical Waste Containers Market, accounting for 29.3% of the share. The high demand for these containers is driven by the growing healthcare sector and the increasing volume of medical procedures involving needles, syringes, and other sharp objects.

These containers are specifically designed to safely contain hazardous sharp waste, preventing injuries and contamination. Stringent regulations and heightened awareness about the risks associated with improper disposal further boost their adoption across hospitals, clinics, and healthcare facilities, ensuring compliance with safety and environmental standards.

RCRA containers are anticipated to witness the fastest growth, with a CAGR of 8.1% during the forecast period. This growth is primarily driven by stringent regulations governing the safe disposal of hazardous medical waste. Healthcare facilities are required to use RCRA-compliant containers for the entire waste management process, ensuring adherence to safety standards and legal requirements.

As a result, there is a rising demand for RCRA-certified solutions to minimize legal risks and enhance safety. This regulatory pressure is prompting healthcare providers to invest in compliant containers, ensuring proper waste disposal and reducing potential liabilities.

By Type of Waste Analysis

Infectious and pathological waste led the type of waste segment in the medical waste containers market. This type of waste includes materials contaminated with pathogens, such as blood-soaked bandages, surgical waste, and other potentially harmful biological substances. The dominance of infectious and pathological waste is attributed to the growing number of medical procedures and healthcare activities that generate hazardous biological materials.

Strict regulations and safety standards require proper disposal to prevent the spread of infections and protect public health, which drives the demand for specialized containers designed to safely manage and contain this high-risk waste.

By Product Analysis

Disposable medical waste containers dominated the product segment of the Medical Waste Containers Market, driven by their convenience, cost-effectiveness, and compliance with stringent safety regulations. These single-use containers are designed to safely handle and dispose of various types of medical waste, including sharps, infectious materials, and hazardous substances, minimizing the risk of contamination and injuries. Their widespread adoption is attributed to the growing demand for efficient waste management solutions in healthcare facilities, which prioritize hygiene and regulatory compliance.

The increasing volume of medical procedures, along with the rising awareness of proper waste disposal practices, has further bolstered the use of disposable containers. Healthcare providers favor these products due to their ease of use and ability to meet strict disposal standards set by regulatory bodies. Additionally, advancements in material technologies and the availability of eco-friendly options enhance their appeal, ensuring the safe and sustainable management of medical waste across the industry.

By End Use Analysis

Hospitals, clinics & physicians’ offices, pharmaceutical companies, long term care & urgent care centers, pharmacies and others are few end-users in the medical waste containers market. Hospitals lead the end-user segment of the Medical Waste Containers Market, reflecting their critical role in generating and managing significant volumes of medical waste.

As primary hubs for patient care, hospitals produce diverse waste types, including sharps, infectious materials, and hazardous substances, necessitating efficient waste management solutions. Their dominance is driven by the high frequency of medical procedures, diagnostic activities, and surgical interventions, all of which contribute to substantial waste generation.

Regulatory requirements mandating the proper disposal of medical waste further emphasize the need for specialized containers in hospital settings. Hospitals prioritize compliance with these standards to safeguard public health and minimize environmental impact. The adoption of advanced and compliant medical waste containers supports streamlined waste segregation, handling, and disposal processes.

Additionally, the growing focus on infection control and workplace safety has accelerated hospitals’ investment in high-quality medical waste containers, reinforcing their position as the leading end-user in this market segment.

Key Market Segments

By Usage

- Chemotherapy Medical Waste Containers

- Biohazard Medical Waste Containers

- RCRA (Resource Conservation and Recovery Act) Medical Waste Containers

- Pharmaceutical Waste Containers

- Medical Sharps Waste Containers

By Type of Waste

- Infectious & Pathological Waste

- Non-infectious Waste

- Radioactive Waste

- Sharps Waste

- Pharmaceutical Waste

By Product

- Disposable Medical Waste Containers

- Reusable Medical Waste Containers

By End Use

- Hospitals

- Clinics & Physicians’ Offices

- Pharmaceutical Companies

- Long Term Care & Urgent Care Centers

- Pharmacies

- Other Generators

Drivers

Advancements in Healthcare Infrastructure

The rapid expansion of healthcare facilities in emerging economies is significantly driving the adoption of medical waste containers. Countries in regions like Asia-Pacific, Latin America, and Africa are experiencing robust growth in their healthcare sectors due to increased government investments, rising medical tourism, and improving access to healthcare services. This development has led to higher volumes of medical waste, necessitating efficient and compliant waste management solutions.

The growing number of hospitals, clinics, and diagnostic centers in these regions requires specialized containers for the safe handling and disposal of hazardous and non-hazardous medical waste. Furthermore, stricter regulatory frameworks in emerging economies are pushing healthcare providers to adopt certified waste containers to ensure compliance and reduce risks associated with improper waste disposal.

Additionally, increasing awareness of infection control and environmental sustainability is further promoting the use of advanced medical waste containers, positioning these markets as key growth drivers in the global medical waste containers industry.

Restrains

High Costs of Advanced Containers

The high costs of biodegradable and technologically advanced medical waste containers present a significant challenge, particularly for smaller healthcare facilities. These containers, designed with sustainable materials or integrated with smart technologies like IoT, offer superior waste management solutions by enhancing safety, compliance, and environmental benefits. However, their premium pricing often deters adoption in cost-sensitive settings.

Smaller healthcare facilities, especially in developing regions, operate on limited budgets and prioritize essential medical equipment and services over high-cost waste management solutions. The upfront expense of advanced containers, coupled with potential maintenance costs for smart features, creates financial barriers.

Additionally, many facilities lack awareness of the long-term benefits, such as reduced liability risks and improved operational efficiency, which could offset initial costs. Bridging this gap requires targeted subsidies, affordable innovations, and education initiatives to encourage broader adoption. Addressing cost-related challenges is crucial for expanding the market reach of advanced medical waste containers.

Opportunities

Supportive Policies and Programs Promoting Proper Medical Waste Disposal

Government initiatives promoting proper medical waste disposal are opening new opportunities for market players to expand their presence. Regulatory frameworks, such as the Bio-Medical Waste Management Rules in India and the Resource Conservation and Recovery Act (RCRA) in the U.S., mandate the safe segregation, transportation, and disposal of medical waste. These regulations drive the adoption of compliant waste containers across healthcare facilities, fostering demand for innovative solutions.

In addition to regulations, governments are launching awareness campaigns and funding programs to enhance waste management infrastructure, particularly in emerging economies. Investments in training healthcare workers and upgrading waste disposal systems further support market growth.

These initiatives not only encourage the use of certified medical waste containers but also push manufacturers to innovate, offering eco-friendly and cost-effective solutions. By addressing compliance and environmental concerns, supportive policies enable market players to strengthen their foothold and cater to the growing demand for advanced waste management systems..

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the medical waste containers market. Economic growth in emerging regions drives healthcare infrastructure expansion, boosting demand for medical waste management solutions. Conversely, economic slowdowns or inflation can limit investments in advanced waste containers, particularly in cost-sensitive markets.

Geopolitical factors, such as trade policies and international regulations, impact supply chains and raw material availability, potentially increasing production costs. Additionally, pandemics or global health crises amplify medical waste generation, accelerating container demand. Conversely, political instability or conflicts in certain regions may disrupt market activities and infrastructure development, hindering the adoption of medical waste containers.

Latest Trends

The medical waste containers market is experiencing notable trends driven by technological advancements and sustainability demands. Increasing adoption of eco-friendly, biodegradable, and recyclable containers reflects the industry’s shift towards environmental responsibility. Integration of smart technologies, such as IoT-enabled containers, enhances waste tracking and disposal efficiency, optimizing healthcare operations.

Stringent regulatory requirements worldwide are pushing manufacturers to innovate compliant, high-quality solutions. Additionally, the rising focus on infection control and workplace safety is encouraging the adoption of specialized containers for hazardous and non-hazardous waste. Emerging economies present growth opportunities, fueled by healthcare infrastructure expansion and heightened awareness of proper waste management practices.

Regional Analysis

North America Dominated the Global Medical Waste Containers Market

North America emerged as the dominant region in the global medical waste containers market, driven by advanced healthcare infrastructure and stringent regulatory frameworks. The region’s well-established healthcare sector generates substantial medical waste, necessitating efficient waste management solutions. Regulatory bodies, such as the Environmental Protection Agency (EPA) in the U.S. and Health Canada, enforce strict guidelines for medical waste segregation, storage, and disposal, encouraging the widespread adoption of compliant containers.

Additionally, the high prevalence of chronic diseases and the growing volume of surgical and diagnostic procedures further fuel the demand for specialized waste containers in hospitals, clinics, and diagnostic centers. The focus on infection control and workplace safety also contributes to the increasing use of advanced waste management solutions.

Moreover, technological advancements and the availability of eco-friendly options are gaining traction in North America, aligning with sustainability goals. This combination of factors ensures the region’s leadership in the global medical waste containers market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, North America led the market, achieving over 43.60% share with a revenue of US$ 0.94 Billion. Leading companies such as Stericycle, BD, Stryker, and Thermo Fisher Scientific dominate the market, offering a wide range of products, including sharps containers, chemotherapy waste containers, and biodegradable solutions. These companies emphasize compliance with stringent regulations like OSHA and EPA standards to ensure safety and proper waste disposal.

Emerging players are also making significant strides by introducing eco-friendly and technologically advanced solutions. For example, companies are increasingly adopting recyclable, biodegradable, and IoT-enabled containers to meet growing demand for sustainable waste management practices and improve operational efficiency.

Additionally, acquisitions and partnerships are common strategies for expanding geographic presence and enhancing service offerings. As healthcare facilities and regulatory bodies push for better waste management practices, innovation, product quality, and adherence to regulations remain key competitive differentiators in the market.

Top Key Players in the Medical Waste Containers Market

- BD

- Bemis Manufacturing Company

- BWAY Corporation

- Bondtech Corporation

- Daniels Sharpsmart Inc.

- EnviroTain, LLC.

- Thermo Fisher Scientific Inc.

- Cardinal Health

- Henry Schein, Inc.

- Sharps Medical Waste Services

Recent Developments

- In October 2024, Mun Australia introduced innovative Sharps Containers crafted from up to 75% recycled plastic, enhancing healthcare safety and sustainability while reducing environmental impact and ensuring regulatory compliance.

- In October 2024, Urbaser announced the acquisition of Stericycle’s assets in Spain and Portugal, strengthening its biomedical waste services portfolio. Meanwhile, Waste Management’s acquisition of Stericycle in Canada faced delays due to an ongoing antitrust review.

- In June 2024, Thermo Fisher Scientific Inc. launched bio-based films for bioprocessing containers, significantly reducing carbon emissions from plastic resin production. These sustainable solutions also earned the ISCC PLUS certification for circular products.

- In March 2024, BD, in partnership with a Danish healthcare consortium, developed a recycling method for used blood collection tubes, preventing 33 tonnes of plastic waste from incineration annually while maintaining hygiene and quality standards..

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 2.16 Billion |

| Forecast Revenue (2034) | US$ 3.85 Billion |

| CAGR (2024-2033) | 6.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Usage- Chemotherapy Medical Waste Containers, Biohazard Medical Waste Containers, RCRA (Resource Conservation and Recovery Act) Medical Waste Containers, Pharmaceutical Waste Containers and Medical Sharps Waste Containers, Type of Waste- Infectious & Pathological Waste, Non-infectious Waste, Radioactive Waste, Sharps Waste and Pharmaceutical Waste, By Product- Disposable Medical Waste Containers and Reusable Medical Waste Containers, By End Use- Hospitals, Clinics & Physicians’ Offices, Pharmaceutical Companies, Long Term Care & Urgent Care Centers, Pharmacies and Others. |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | BD, Bemis Manufacturing Company, BWAY Corporation, Bondtech Corporation, Daniels Sharpsmart Inc., EnviroTain, LLC., Thermo Fisher Scientific Inc., Cardinal Health, Henry Schein, Inc. and Sharps Medical Waste Services |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |