Quick Navigation

Report Overview

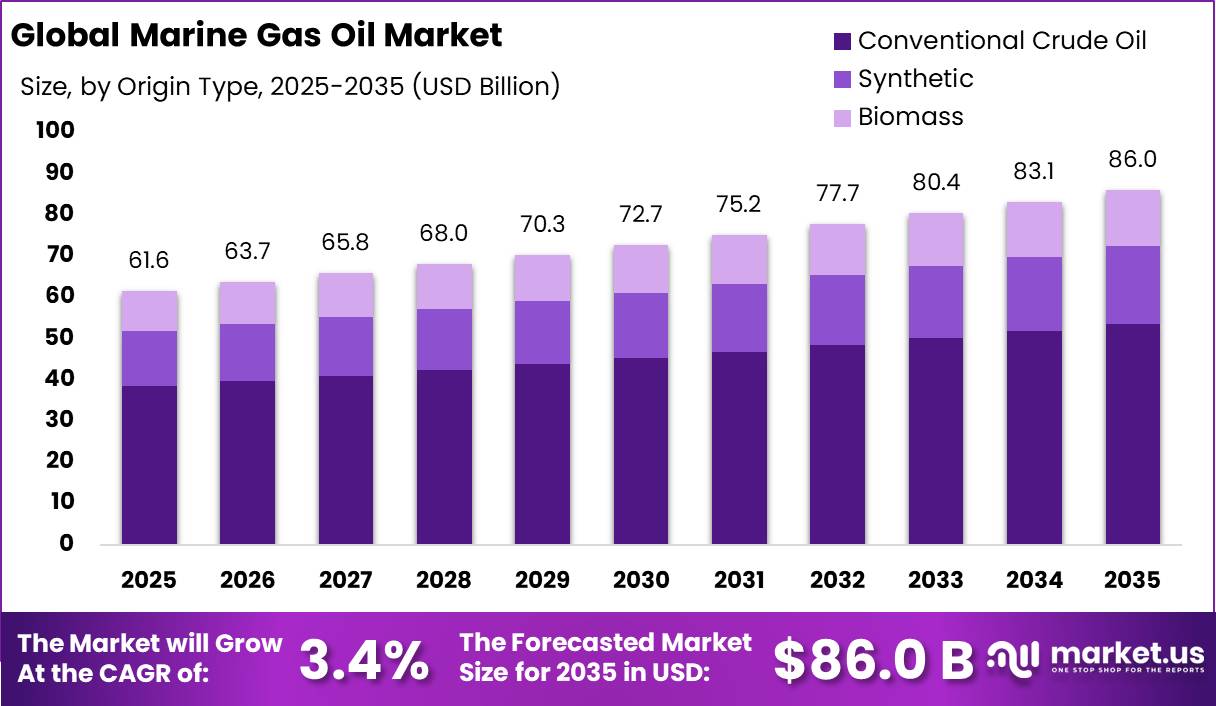

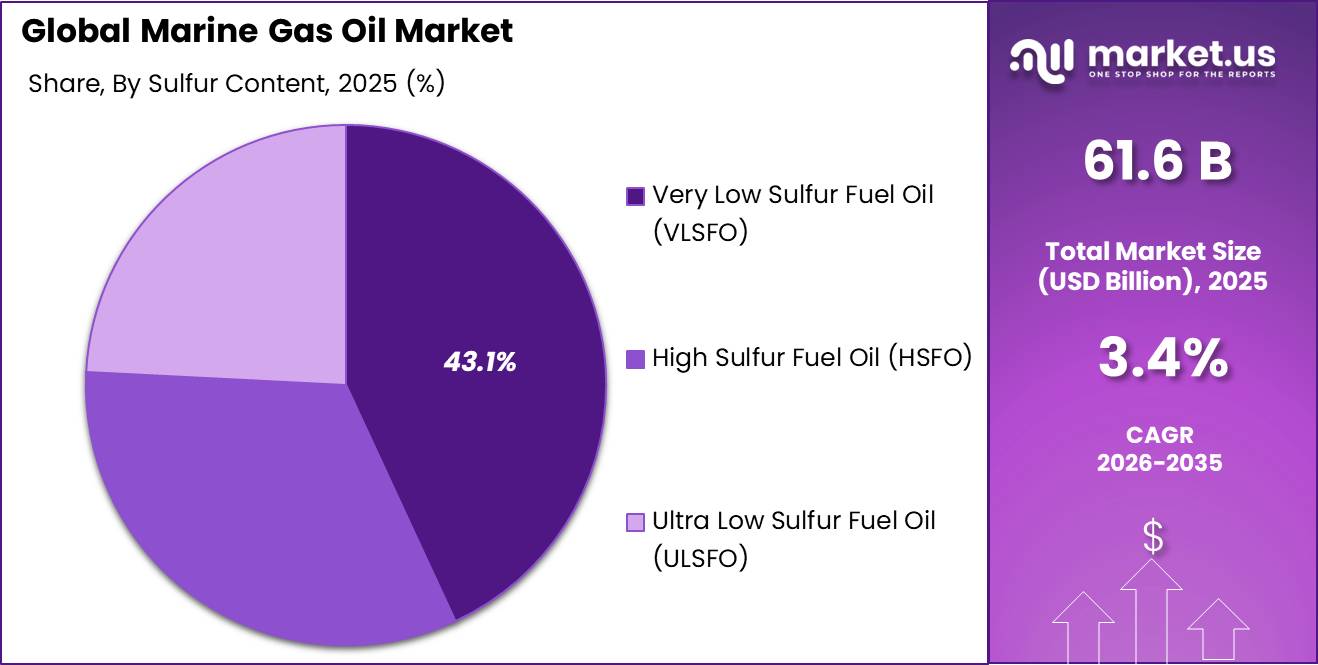

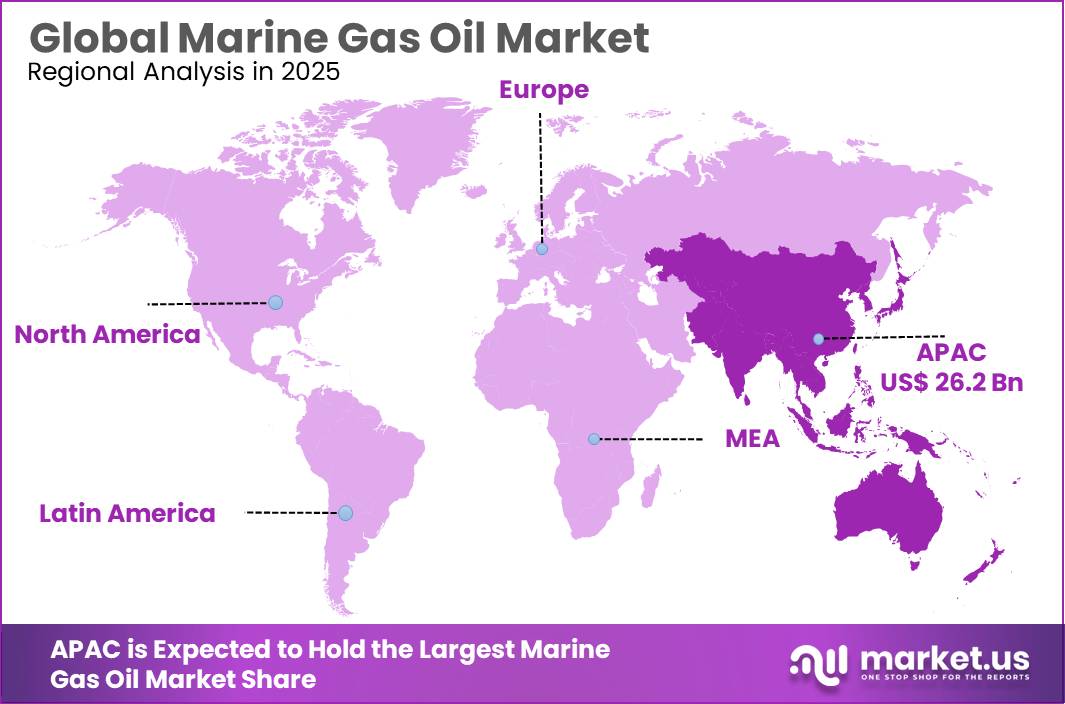

The Global Marine Gas Oil Market size is expected to be worth around USD 86.0 Billion by 2035, from USD 61.6 Billion in 2025, growing at a CAGR of 3.4% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 42.6% share, holding USD 26.2 Billion revenue.

Marine Gas Oil (MGO) remains a key distillate marine fuel used by ships operating in emission-controlled areas, ports, offshore support, ferries and auxiliary engines because it offers lower sulphur and cleaner combustion than residual bunker fuel. The industrial base is supported by maritime trade, as over 80% of global goods trade by volume moves by sea, while UNCTAD reported maritime trade growth of 2.2% in 2024, slowing to 0.5% in 2025 and averaging 2% annually during 2026–2030.

Key Takeaways

- Marine Gas Oil Market size is expected to be worth around USD 86.0 Billion by 2035, from USD 61.6 Billion in 2025, growing at a CAGR of 3.4%.

- Conventional Crude Oil held a dominant market position, capturing more than a 62.3% share in the Marine Gas Oil market.

- Distillate held a dominant market position, capturing more than a 59.6% share in the Marine Gas Oil market.

- Direct Sales held a dominant market position, capturing more than a 45.7% share in the Marine Gas Oil market.

- Very Low Sulfur Fuel Oil (VLSFO) held a dominant market position, capturing more than a 43.1% share in the Marine Gas Oil market.

- Marine held a dominant market position, capturing more than a 51.3% share in the Marine Gas Oil market.

- Asia-Pacific held the dominant position in the Marine Gas Oil market, accounting for 42.6% of the global market and reaching a value of USD 26.2 Billion.

The industrial scenario remains regulation-led but volume-sensitive. UNCTAD reported global seaborne trade growth of 2.2% in 2024, slowing to 0.5% in 2025, before averaging about 2% later in the decade, indicating that MGO demand is supported more by compliance, fleet operations and route disruption than by rapid cargo growth. The IEA also indicated that marine bunker demand may remain near 5 million barrels per day from 2024 to 2030, as efficiency rules, carbon pricing and weaker trade growth restrain fuel expansion.

Driving factors include port emission rules, low-sulphur compliance, offshore activity, naval and short-sea shipping demand, and route disruptions that increase voyage distance and bunker consumption. IEA indicated global oil demand growth of 680 kb/d in 2025 and 700 kb/d in 2026, reaching 104.4 mb/d, supporting refined product demand including marine distillates. However, IEA also noted bunker demand may remain around 5 million barrels per day from 2024 to 2030, reflecting regulation and slower trade growth.

Government and regulatory initiatives are strengthening the transition. The EU FuelEU Maritime framework applies from 2025, requiring a 2% cut in yearly average GHG intensity for ships above 5,000 gross tonnage, rising toward 80% by 2050. The IMO also approved a 2025 net-zero framework combining mandatory fuel-emission limits and GHG pricing, targeting net-zero shipping by or around 2050.

ExxonMobil Corporation continued to strengthen downstream and marine-related fuel capability. In September 2025, ExxonMobil started new Singapore technology to convert fuel oil and bottom-of-the-barrel crude products into higher-value base stocks and distillates, adding 20,000 barrels per day of Group II base-stock capacity, including up to 6,000 barrels per day of EHC 340 MAX.

By Origin Type Analysis

Conventional Crude Oil dominates with 62.3% share due to its established supply chain and broad compatibility with marine fuel requirements

In 2025, Conventional Crude Oil held a dominant market position, capturing more than a 62.3% share in the Marine Gas Oil market by origin type. This leading position was mainly supported by its long-established production network, stable availability across major oil-producing regions, and continued preference among marine fuel suppliers. Conventional crude remains widely used because it offers a reliable feedstock for refining marine gas oil and supports consistent fuel quality needed for commercial shipping operations.

By Viscosity Type Analysis

Distillate dominates with 59.6% share driven by cleaner fuel characteristics and strong adoption across marine operations

In 2025, Distillate held a dominant market position, capturing more than a 59.6% share in the Marine Gas Oil market by viscosity type. This leadership was supported by its cleaner combustion profile, lower sulfur content alignment, and suitability for a wide range of marine vessels operating under evolving environmental requirements. Marine operators continued to prefer distillate fuels because they offer reliable engine performance while helping meet operational and emissions expectations across regional and international routes.

By Sales Channel Analysis

Direct Sales dominates with 45.7% share supported by stronger customer relationships and efficient fuel procurement

In 2025, Direct Sales held a dominant market position, capturing more than a 45.7% share in the Marine Gas Oil market by sales channel. This leading position was mainly driven by the growing preference of shipping companies and fleet operators to purchase fuel directly from suppliers for better pricing transparency, reliable supply agreements, and improved operational planning. Direct sales channels continued to gain attention as buyers focused on maintaining fuel availability and reducing dependency on multiple intermediaries.

By Sulfur Content Analysis

Very Low Sulfur Fuel Oil (VLSFO) dominates with 43.1% share driven by compliance needs and cleaner marine fuel demand

In 2025, Very Low Sulfur Fuel Oil (VLSFO) held a dominant market position, capturing more than a 43.1% share in the Marine Gas Oil market by sulfur content. Its strong market presence was supported by the continued shift toward cleaner marine fuels and the growing focus on meeting environmental standards across global shipping operations. Vessel operators increasingly selected VLSFO as a practical option to reduce sulfur emissions while maintaining operational efficiency without major engine modifications.

By Application Analysis

Marine dominates with 51.3% share supported by strong vessel fuel demand and continuous shipping activity

In 2025, Marine held a dominant market position, capturing more than a 51.3% share in the Marine Gas Oil market by application. This leading position was largely driven by the continuous demand for fuel across commercial shipping operations, cargo transportation, offshore activities, and vessel movement across international trade routes. Marine gas oil remained an important fuel choice because of its dependable performance and suitability for a broad range of marine engines.

Key Market Segments

By Origin Type

- Conventional Crude Oil

- Synthetic

- Biomass

By Viscosity Type

- Distillate

- Residual

By Sales Channel

- Direct Sales

- Distributors

- Online Marketplaces

By Sulfur Content

- Very Low Sulfur Fuel Oil (VLSFO)

- High Sulfur Fuel Oil (HSFO)

- Ultra Low Sulfur Fuel Oil (ULSFO)

By Application

- Marine

- Industrial

- Power Generation

- Others

Emerging Trends

Low-Sulphur Marine Gas Oil Is Becoming the Safer Compliance Choice

A major latest trend in Marine Gas Oil is the steady shift toward cleaner, low-sulphur fuel for ships operating in stricter emission zones. Shipowners are using MGO because it is easier to handle than heavy fuel oil and helps vessels meet sulphur rules without major engine changes. The IMO’s global sulphur rule limits marine fuel sulphur to 0.50%, down from the earlier 3.50%, while ships in Emission Control Areas must use fuel with only 0.10% sulphur.

This has made MGO more important for ferries, offshore vessels, cruise ships and ships calling at regulated ports. The trend is also linked to the shipping sector’s wider climate target, as IMO aims for net-zero greenhouse gas emissions from international shipping by around 2050.

Bio-MGO Blends Are Opening a Cleaner Fuel Path

Another important part of this trend is the rise of bio-blended marine fuels, including bio-MGO. ExxonMobil has expanded marine biofuel options, including 0.10% sulphur bio MGO and blends available up to B30 in selected UK South Coast ports. This shows that large energy suppliers are not only selling conventional MGO but also preparing lower-carbon versions for shipowners that need practical fuel options today.

The opportunity is strong because shipping still depends heavily on liquid fuels; the IEA reported that global bunker demand is expected to stay near 5 million barrels per day from 2024 to 2030. At the same time, IMO’s 2030 checkpoint targets at least 20% GHG reduction, striving for 30%, which is pushing suppliers and ship operators toward cleaner MGO blends.

Drivers

Rising Global Seaborne Trade is Creating Strong Demand for Marine Gas Oil

One of the major driving factors for the Marine Gas Oil market is the continued growth of global seaborne trade and the increasing dependence of international supply chains on shipping activity. Marine gas oil remains an important fuel source for vessels because it supports reliable operations across cargo transport, commercial shipping, offshore movement, and regional marine logistics.

- According to the United Nations Conference on Trade and Development (UNCTAD), more than 80% of the volume of international trade in goods is transported by sea.

This shows how strongly the global economy depends on maritime transport to move raw materials, industrial products, and finished goods across regions. As shipping activity expands, fuel demand naturally increases, supporting steady consumption of marine gas oil across major ports and shipping corridors.

Higher Vessel Movement and Bunkering Activity Continue to Support Fuel Consumption

Another important factor supporting the Marine Gas Oil market is the rise in vessel movement and increasing bunkering volumes at major marine fuel hubs. Growth in ship traffic directly influences fuel requirements and creates stronger demand for marine fuel products across global trading routes.

Official data from the Maritime and Port Authority of Singapore showed that marine fuel sales reached a record 54.92 million metric tons in 2024, while container throughput climbed to 41.12 million TEUs and vessel arrival tonnage reached 3.11 billion gross tons. These figures reflect sustained shipping activity and demonstrate how active marine transport continues to support fuel demand.

Restraints

Tightening Emission Regulations and Decarbonization Targets Are Limiting Marine Gas Oil Growth

One of the major restraining factors for the Marine Gas Oil market is the increasing pressure from international emission regulations and long-term shipping decarbonization targets. Marine gas oil has traditionally been a dependable fuel for shipping operations, but environmental policies are gradually pushing the industry toward lower-emission and alternative fuel options.

- According to the International Maritime Organization (IMO), the revised 2023 greenhouse gas strategy targets a reduction in carbon intensity of international shipping by at least 40% by 2030 compared with 2008 levels.

The strategy also introduced a target for zero or near-zero emission fuels to account for at least 5% of total shipping energy use by 2030, with efforts toward 10%. In addition, the sector is working toward net-zero greenhouse gas emissions by or around 2050. These targets are encouraging shipping companies to reconsider long-term dependence on conventional marine fuels and increase investment in cleaner alternatives.

Rising Compliance Costs and Fuel Transition Investments Are Increasing Operational Pressure

Another factor restricting Marine Gas Oil market growth is the growing financial burden linked to compliance and fuel transition. Shipping companies are now balancing operational efficiency with environmental obligations, which increases costs across fleet management and fuel procurement.

The International Maritime Organization estimated in its Fourth GHG Study that shipping contributed approximately 2.89% of global anthropogenic greenhouse gas emissions in 2018. This figure continues to influence global policy discussions and stronger emission control measures across maritime transport. At the same time, regulators are introducing stricter frameworks that encourage lower-carbon fuel adoption and reduce reliance on conventional fuel pathways.

Opportunity

Expansion of Global Port Infrastructure and Maritime Trade Creates New Demand Opportunities

One of the major growth opportunities for the Marine Gas Oil market is the ongoing expansion of global port infrastructure and increasing maritime trade activity. As governments and port authorities continue investing in port modernization, vessel handling capacity, and marine logistics networks, fuel demand across shipping operations is expected to remain supported over the coming years.

According to the United Nations Conference on Trade and Development (UNCTAD), global maritime trade reached approximately 12.3 billion tons in 2023, showing the continued importance of sea transport in moving goods across international markets. At the same time, UNCTAD projects maritime trade volumes to grow by around 2.4% in 2024 and continue expanding at an average annual rate of about 2.1% through 2029. This steady increase in cargo movement creates long-term opportunities for marine fuel consumption, including marine gas oil.

Growing Investment in Modern Shipping Fleets Supports Marine Gas Oil Consumption

Another strong growth opportunity comes from continued investment in fleet modernization and rising commercial vessel activity. Shipping companies are expanding and upgrading fleets to improve operational performance, fuel efficiency, and compliance with evolving environmental standards while maintaining existing fuel compatibility.

According to the United Nations Conference on Trade and Development, the global commercial fleet reached more than 110,000 ships in operation worldwide in recent reporting periods, reflecting continued expansion in marine transportation capacity. Additionally, the International Energy Agency highlighted that shipping remains one of the most energy-efficient transport modes for large-volume cargo movement, reinforcing long-term demand for marine fuel infrastructure.

Regional Insights

Asia-Pacific dominated the Marine Gas Oil market with a 42.6% share, reaching USD 26.2 Billion through strong shipping activity and expanding marine trade infrastructure

In 2025, Asia-Pacific held the dominant position in the Marine Gas Oil market, accounting for 42.6% of the global market and reaching a value of USD 26.2 Billion. The region’s leadership was mainly supported by its strong maritime trade network, large commercial shipping fleet, expanding port infrastructure, and high concentration of global manufacturing and export activities.

Asia-Pacific remains home to some of the world’s busiest shipping corridors and major bunkering hubs, which strengthens fuel demand across marine operations. The region benefits from high container traffic, increasing vessel movement, and continuous investment in port modernization. Growing industrial production and export-oriented economies further contribute to consistent marine transportation requirements.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Shell PLC remains one of the leading participants in the Marine Gas Oil market through its broad marine fuel supply network and global bunkering operations. The company operates in more than 70 countries and supports marine customers across major international shipping routes. Shell reported revenue of approximately USD 284 billion in 2025, reflecting its large-scale energy operations.

ExxonMobil Corporation maintains a strong position in the Marine Gas Oil market through its refining capacity and international fuel supply network. The company generated around USD 339 billion in revenue in 2025 and continued expanding downstream operations to support marine fuel demand. ExxonMobil operates across more than 60 countries and supplies fuel solutions for commercial shipping customers globally.

BP PLC continues to serve the Marine Gas Oil market through marine fuel trading, bunkering services, and global energy operations. In 2025, the company reported revenue exceeding USD 190 billion and maintained operations across more than 70 countries. BP focuses on strengthening marine fuel accessibility and improving supply reliability across key shipping locations.

Top Key Players Outlook

- Shell PLC

- ExxonMobil Corporation

- BP PLC

- TotalEnergies SE

- Engen Petroleum

- Gazprom Neft PJSC

- Chevron Corporation

- Marathon Petroleum

- Valero Energy

- Petrobras

- Lubrizol (Berkshire Hathaway)

- Neste OYJ

- Bomin Bunker Fuel Holding GMBH & Co. KG

Recent Industry Developments

In 2025, Engen benefited from Vivo Energy’s wider African network, which included over 3,900 service stations, more than 2 billion litres of storage capacity, and operations across 28 African markets. For investment and expansion, Vivo Energy committed around USD 550.79 million, or nearly ZAR 10 billion, for South African operations after the Engen merger, with possible additional investment of ZAR 4 billion in biofuels and marine-related projects, depending on feasibility.

In July 2025, TotalEnergies signed a major partnership with CMA CGM to launch an LNG bunkering logistics joint venture in the ARA region, supported by a long-term supply deal of up to 360,000 tons of LNG per year until 2040 and a 20,000 m³ LNG bunker vessel planned for 2028. In 2025, TotalEnergies’ Downstream business reported USD 3.8 billion in adjusted net operating income and USD 6.2 billion in cash flow, supporting its refining, marketing, and marine fuel supply strength.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 61.6 Bn |

| Forecast Revenue (2035) | USD 86.0 Bn |

| CAGR (2026-2035) | 3.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Origin Type (Conventional Crude Oil, Synthetic, Biomass), By Viscosity Type (Distillate, Residual), By Sales Channel (Direct Sales, Distributors, Online Marketplaces), By Sulfur Content (Very Low Sulfur Fuel Oil (VLSFO), High Sulfur Fuel Oil (HSFO), Ultra Low Sulfur Fuel Oil (ULSFO)), By Application (Marine, Industrial, Power Generation, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Shell PLC, ExxonMobil Corporation, BP PLC, TotalEnergies SE, Engen Petroleum, Gazprom Neft PJSC, Chevron Corporation, Marathon Petroleum, Valero Energy, Petrobras, Lubrizol (Berkshire Hathaway), Neste OYJ, Bomin Bunker Fuel Holding GMBH & Co. KG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |