Quick Navigation

Report Overview

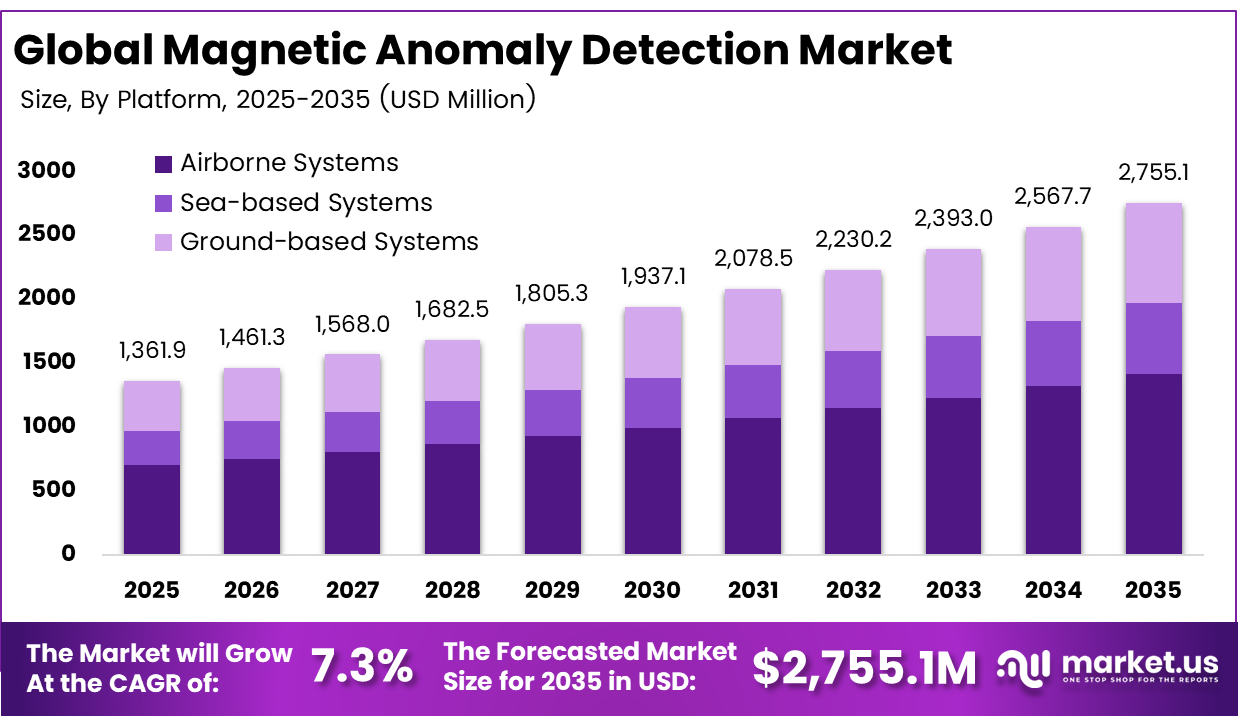

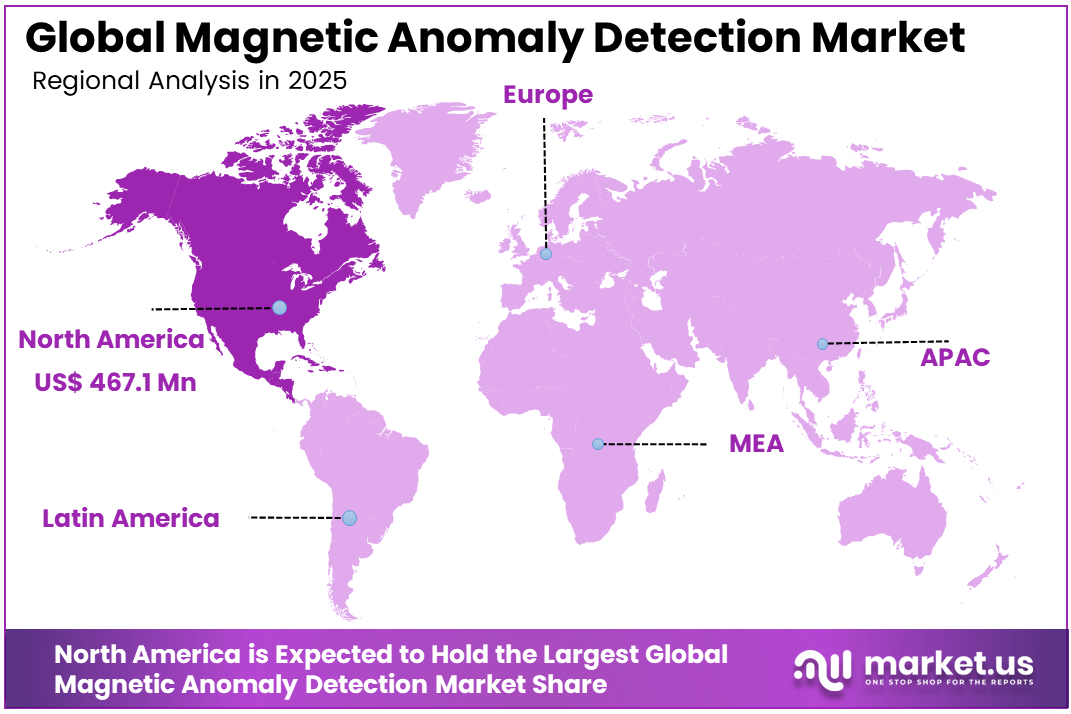

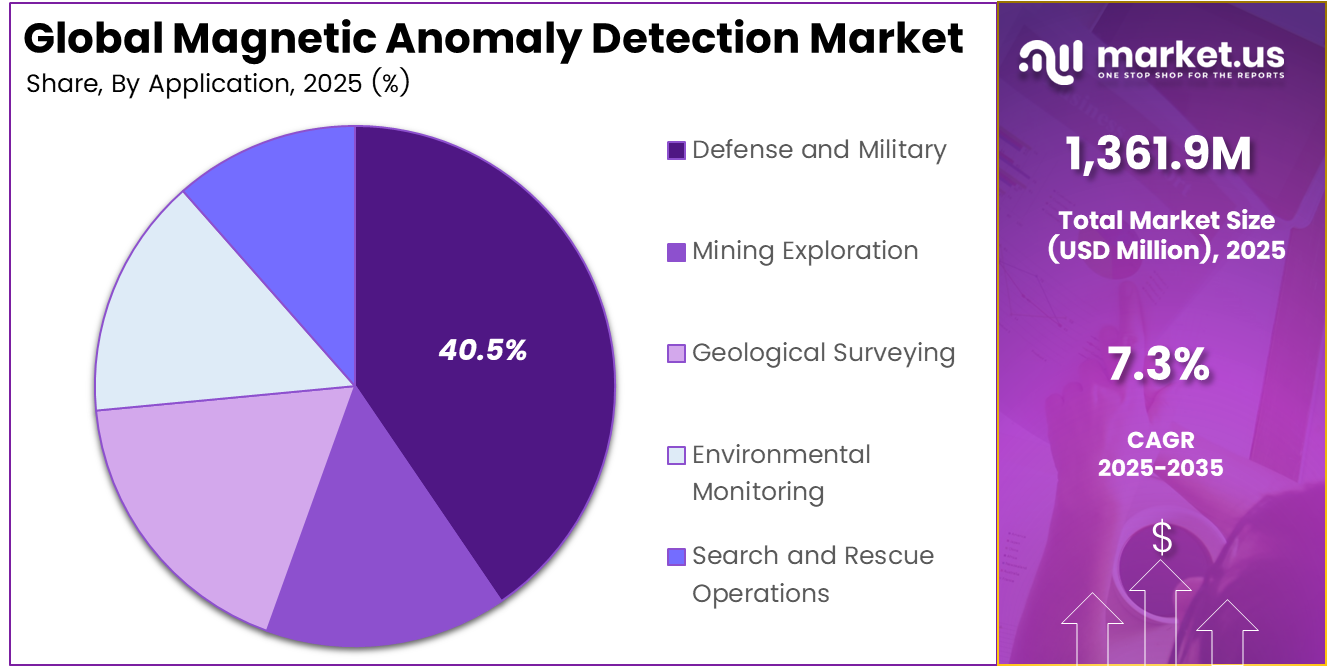

The Global Magnetic Anomaly Detection Market size is expected to be worth around USD 2,755.1 million by 2035, from USD 1,361.9 million in 2025, growing at a CAGR of 7.3% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than 34.3% share and generating USD 467.1 million in revenue.

Magnetic Anomaly Detection refers to the use of sensors that identify small changes in the Earth’s magnetic field caused by metallic objects or underground structures. It is widely used in submarine detection, mine identification, mineral exploration, and infrastructure surveys, helping users locate hidden targets without direct contact.

Top driving factors include rising focus on underwater security, resource exploration, and coastal infrastructure monitoring, especially as over 90% of global trade flows by sea. Magnetic detection methods are gaining use because magnetic fields remain stable over time and can pass through water or soil, unlike acoustic or optical signals that may face interference.

The market for Magnetic Anomaly Detection is driven by rising demand for underwater security, submarine detection, offshore asset monitoring, and mineral exploration. Its ability to identify hidden metallic objects without direct contact makes it valuable for defense, energy, and geophysical survey operations. Growing use of drones, autonomous underwater vehicles, and advanced magnetometers is further supporting wider market adoption.

Demand is growing as operators need non-contact detection tools for ferromagnetic targets at stand-off distances of several hundred meters. These systems help users monitor areas without exposing their own position. They also reduce site surveys and diver time, which is important as each offshore day can cost tens of thousands of dollars.

For instance, in August 2024, Quantum Magnetics advanced its high-sensitivity magnetic and electromagnetic sensing platforms for security screening and subsurface threat detection. The company is refining algorithms to pick out weak magnetic anomalies from noisy environments, supporting defense and homeland-security programs that require covert detection of metallic objects and buried infrastructure.

Key Takeaway

- In 2025, the Airborne Systems segment held a dominant market position, capturing a 51.4% share of the Global Magnetic Anomaly Detection Market.

- In 2025, the Fluxgate Magnetometers segment held a dominant market position, capturing a 35.6% share of the Global Magnetic Anomaly Detection Market.

- In 2025, the Defense & Military segment held a dominant market position, capturing a 40.5% share of the Global Magnetic Anomaly Detection Market.

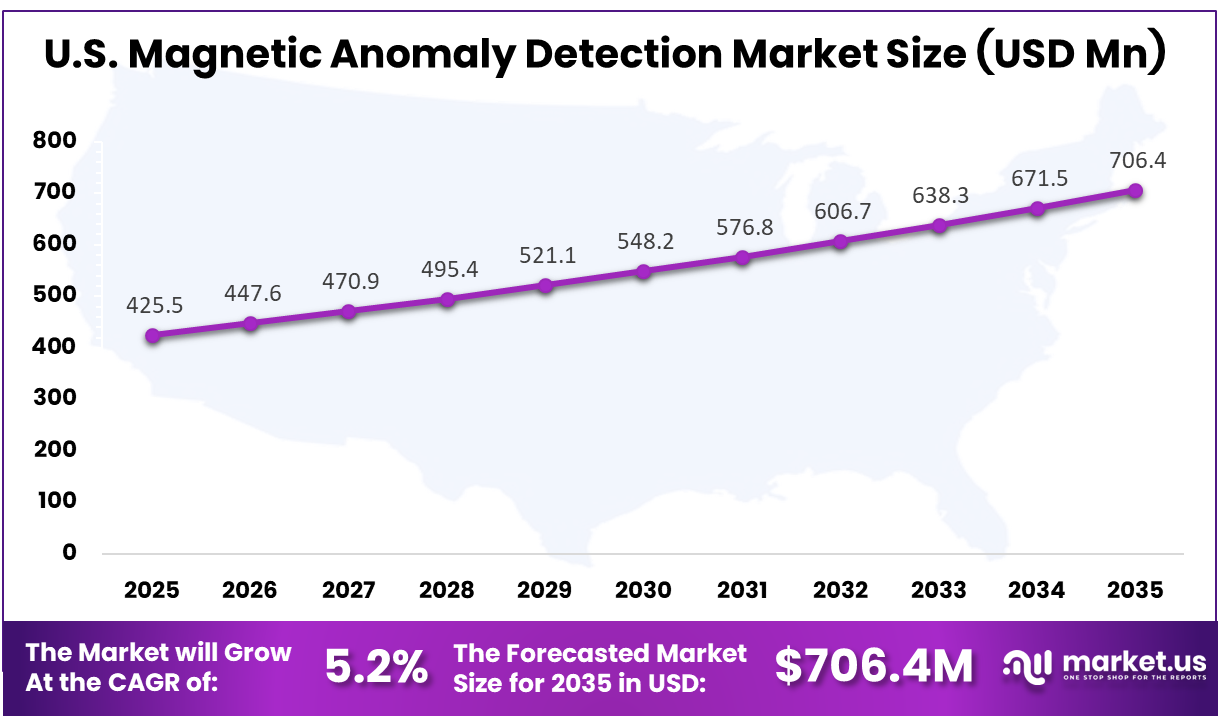

- The U.S. Magnetic Anomaly Detection Market was valued at USD 425.5 Million in 2025, with a robust CAGR of 5.2%.

- In 2025, North America held a dominant market position in the Global Magnetic Anomaly Detection Market, capturing more than a 34.3% share.

Role of Generative AI

Generative AI is improving the way magnetic anomaly detection data is processed by reducing noise and identifying weak signals that traditional systems may miss. AI-based methods have improved detection accuracy by close to 20% to 30% in complex geomagnetic conditions, especially when target signals are hidden under strong natural noise.

Generative AI also supports the creation of realistic target signatures, helping teams reduce dependence on long sea trials. Synthetic data and AI-assisted workflows can cut model training time by about 40% and increase usable training samples by more than 50%, which is valuable when real labeled MAD data is limited.

Investment and Business Benefits

Investment opportunities arise in compact and high-sensitivity sensors designed for drones, autonomous underwater vehicles, and towed arrays, where payload power limits are often below 100 watts. Strong scope is also seen in software platforms that combine magnetic data with sonar, lidar, and positioning feeds, while machine learning can cut false alarms by more than 50%.

Business benefits include faster surveys, smaller field teams, and fewer repeat passes, helping improve asset availability and reduce inspection campaigns by 20 to 30% over several years. In mining, oil, and gas operations, improved magnetic mapping also helps identify hidden anomalies early, lowering the risk of unplanned downtime and safety issues.

Regional Analysis

In 2025, North America held a dominant market position in the Global Magnetic Anomaly Detection Market, capturing more than 34.3% share and generating USD 467.1 million in revenue. This dominance is due to strong defense spending, advanced naval surveillance programs, and high adoption of airborne and unmanned detection platforms. The region has large coastal areas, active offshore energy operations, and a growing focus on undersea security. Continued investment in high-sensitivity magnetometers, maritime patrol aircraft, and infrastructure monitoring further supports its leadership in this market.

For instance, in March 2025, Lockheed Martin secured a U.S. Defense Innovation Unit contract to prototype its quantum-enabled Inertial Navigation System (QuINS), using ultra-precise quantum sensors to maintain navigation accuracy even when GPS is jammed. This next-generation sensing capability strengthens U.S. undersea and airborne anti-submarine warfare, reinforcing North America’s lead in advanced magnetic and anomaly-detection technologies for defense.

U.S. Magnetic Anomaly Detection Market Size

The market for Magnetic Anomaly Detection within the U.S. is growing tremendously and is currently valued at USD 425.5 million; the market has a projected CAGR of 5.2%. The market is growing due to rising investments in maritime security, submarine detection, offshore infrastructure monitoring, and advanced defense surveillance. The country’s large naval presence, expanding coastal protection needs, and use of unmanned platforms are supporting wider adoption. Demand is also increasing in mineral exploration and oil and gas activities, where accurate magnetic mapping helps reduce operational risks and improve field decisions.

For instance, in February 2025, Quantum Magnetics continued developing high-sensitivity magnetic and electromagnetic sensing platforms for U.S. security, counter-threat, and non-intrusive inspection programs. Its technologies help detect concealed metallic objects and subsurface anomalies with extremely low signal signatures. By supplying such advanced sensors to federal security and defense projects, the company reinforces U.S. leadership in precision magnetic detection and anomaly-sensing solutions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Platform Analysis

In 2025, the Airborne Systems segment held a dominant market position, capturing a 51.4% share of the Global Magnetic Anomaly Detection Market. This dominance is due to the strong use of airborne systems in maritime patrol, undersea surveillance, and large area monitoring. Aircraft can cover wide ocean zones faster than surface platforms, making them suitable for defense missions, offshore inspections, and rapid detection of magnetic disturbances linked to submerged metallic objects.

Airborne systems are also preferred because they can operate from a safer distance while supporting quick response missions. Their ability to carry advanced sensors, collect data over broad routes, and support real-time decision making makes them important for naval forces, border security agencies, and coastal infrastructure monitoring teams.

For instance, in June 2025, Sikorsky, a Lockheed Martin company, partnered with CAE to integrate the MAD XR digital magnetic anomaly detection system on MH-60R maritime helicopters for the US and Australian navies. The compact sensor gives airborne crews a new way to confirm submerged threats during anti-submarine missions, strengthening the role of aircraft in magnetic detection.

Technology Analysis

In 2025, the Fluxgate Magnetometers segment held a dominant market position, capturing a 35.6% share of the Global Magnetic Anomaly Detection Market. This dominance is due to the practical performance of fluxgate magnetometers in detecting small changes in magnetic fields. These sensors are widely valued for their stability, compact design, and suitability for field operations. They are used in aircraft, underwater vehicles, and portable systems where reliable magnetic readings are required.

Fluxgate magnetometers also offer a balanced mix of sensitivity, cost efficiency, and operational durability. Their ability to work in difficult environments makes them useful for defense, mineral exploration, and infrastructure surveys. As users seek dependable detection tools, this technology continues to remain a preferred choice across several MAD applications.

For instance, in February 2025, PNI Sensor highlighted advances in fluxgate-based magnetometer technology for navigation, security, and geophysical exploration. Improvements in sensor accuracy, miniaturization, and power efficiency make fluxgate designs more attractive for mobile platforms and portable systems, which indirectly supports the adoption of similar fluxgate solutions across magnetic anomaly detection projects.

Application Analysis

In 2025, the Defense & Military segment held a dominant market position, capturing a 40.5% share of the Global Magnetic Anomaly Detection Market. This dominance is due to the strong role of magnetic anomaly detection in defense and military operations. MAD systems help identify submarines, underwater mines, and other metallic targets by detecting changes in the Earth’s magnetic field. This makes them useful in naval surveillance, maritime security, and strategic undersea monitoring.

Defense users rely on MAD because it supports covert and non-contact detection in complex marine environments. It is often used with sonar and other sensing tools to improve target confirmation. Growing attention on underwater security, naval modernization, and coastal protection continues to support its wider military adoption.

For instance, in June 2025, the MAD XR upgrade for MH-60R helicopters was presented as a way to sharpen anti-submarine warfare performance for US and Australian forces. By adding a non-acoustic magnetic sensor to existing sonar and radar suites, navies gain another option to locate quiet submarines, which keeps defense applications at the center of magnetic anomaly detection demand.

Key Market Segments

By Platform

- Airborne Systems

- Sea-based Systems

- Ground-based Systems

By Technology

- Optically Pumped Magnetometers (OPM)

- Nuclear Precession Magnetometers

- Fluxgate Magnetometers

- SQUID (Superconducting Quantum Interference Device) Magnetometers

- Others

By Application

- Defense and Military

- Mining Exploration

- Geological Surveying

- Environmental Monitoring

- Search and Rescue Operations

Emerging Trends

Emerging trends in MAD show a growing shift toward distributed sensor networks supported by advanced signal processing and AI. Multi-sensor or multi-platform layouts can extend effective detection ranges by roughly 15% to 25% compared with single sensor systems, while also improving localization accuracy for small or deep targets.

Miniaturization is also becoming important as lightweight magnetometers are added to unmanned aerial and underwater platforms. Trials using micro aerial vehicles and autonomous underwater vehicles indicate up to 30% lower operational costs, while enabling more frequent survey missions when supported by strong detection algorithms.

Growth Factors

Growth in MAD is supported by rising undersea activity, including naval modernization and subsea infrastructure monitoring. More than 60% of new undersea surveillance concepts now evaluate magnetic sensing in some form, often as an added layer beside sonar and optical systems for stronger maritime awareness.

Another growth factor is the advancement of high-sensitivity magnetometers, including optically pumped and fluxgate sensors. Technical evaluations show next-generation sensors can deliver around 10% to 20% better signal-to-noise ratios than older tools, helping improve deeper detection and more reliable classification of ferromagnetic targets.

Market Dynamics

Drivers - Stronger Underwater Security Needs

Stronger underwater security needs are driving the Magnetic Anomaly Detection Market as defense agencies focus on submarine tracking, mine detection, and coastal protection. MAD systems help detect metallic objects below the surface without relying only on sonar, making them useful in complex marine areas.

The growth of naval modernization and undersea surveillance programs is also supporting adoption. These systems are valued because they can strengthen maritime awareness, support patrol missions, and improve detection confidence in areas where traditional sensing methods may face environmental or operational limits.

For instance, in June 2025, Lockheed Martin’s Sikorsky unit and CAE began delivering the MAD-XR digital magnetic anomaly detection system for MH-60R Seahawk helicopters used by the US and Royal Australian Navies, giving crews an additional non-acoustic tool to strengthen close-in submarine detection and overall underwater security.

Restraint - High Cost and Technical Complexity

High cost and technical complexity remain key restraints for the Magnetic Anomaly Detection Market. Advanced sensors, calibration tools, data processing systems, and platform integration require skilled teams and careful testing, which can raise the overall cost of deployment for many users.

The technology also needs proper filtering to separate real target signals from background magnetic noise. This makes system setup and interpretation more difficult, especially in cluttered or deepwater environments. Smaller operators may delay adoption due to limited budgets and a lack of technical expertise.

For instance, in January 2024, EMCORE’s precision navigation sensors for demanding defense missions highlighted how performance gains come with complex calibration and integration requirements, a pattern that is similar for high-grade magnetic sensing equipment when it is embedded in tightly coupled mission systems.

Opportunities - Expansion into Commercial and Niche Applications

Expansion into commercial and niche applications is creating new opportunities for Magnetic Anomaly Detection systems. Beyond defense, these tools are being used in offshore energy, mineral exploration, marine archaeology, pipeline inspection, and unexploded object detection, where accurate magnetic mapping supports safer field decisions.

Growing use of drones, autonomous underwater vehicles, and compact sensors is also widening the commercial scope. These platforms can reduce manual survey work, improve access to difficult locations, and help operators collect magnetic data with lower field risk and better operational flexibility.

For instance, in March 2026, Leonardo’s updated industrial plan emphasized multi-domain security and advanced sensing architectures, creating a framework where technologies proven in defense could later be adapted for civil protection roles, including coastal monitoring and critical infrastructure surveillance.

Challenges - Regulatory Constraints

Regulatory constraints are a major challenge for the Magnetic Anomaly Detection Market, especially in defense, offshore, and coastal survey activities. Operators often need approvals related to maritime zones, airspace use, environmental protection, and data handling before deploying aircraft, drones, or underwater systems.

These requirements can slow project timelines and increase compliance work. In sensitive defense or energy areas, data security rules may also limit the sharing, storage, and analysis of survey results. This creates additional pressure on vendors to design systems that meet both technical and regulatory expectations.

For instance, in December 2025, Thales’ onboard cyber and anomaly detection work for satellites ran under European space and cybersecurity regulations, echoing how underwater and magnetic detection solutions must also navigate strict rules on security-sensitive technologies and data.

Key Players Analysis

One of the leading players in August 2025, EMCORE completed the acquisition of L3Harris’ Space & Navigation business for about $5 million in an all-cash deal, adding strategic-grade gyros and IMUs to its portfolio. This strengthens EMCORE’s position in high-precision navigation, a core enabler for next-generation magnetic anomaly detection systems used on aircraft and unmanned platforms.

Top Key Players in the Market

- Lockheed Martin Corporation

- Geonics Limited

- Leonardo

- EMCORE Corporation

- Geospace Technologies

- CETC

- Quantum Magnetics

- Magellan Aerospace

- Mistras Group

- Terra Exploration

- Thales Group

- Northrop Grumman Corporation

- L3Harris Technologies Inc.

- Others

Recent Developments

- In March 2025, Lockheed Martin advanced its underwater surveillance portfolio by investing in next-generation MAD payloads optimized for anti-submarine warfare aircraft and unmanned platforms. The company is focusing on miniaturized, high-sensitivity sensors and digital signal processing, reinforcing its position as a leading supplier of MAD solutions to U.S. and allied naval forces.

- In February 2025, Geonics Limited expanded deliveries of high-resolution electromagnetic and magnetometer systems to North American mining and environmental clients. The company is enhancing instruments used for subsurface anomaly mapping and UXO detection, aligning its roadmap with growing demand for portable, field-proven MAD-style technologies in resource exploration and remediation projects.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1,361.9 Million |

| Forecast Revenue (2035) | USD 2,755.1 Million |

| CAGR (2026-2035) | 7.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Platform (Airborne Systems, Sea-based Systems, Ground-based Systems), By Technology (Optically Pumped Magnetometers (OPM), Nuclear Precession Magnetometers, Fluxgate Magnetometers, SQUID (Superconducting Quantum Interference Device) Magnetometers, Others), By Application (Mining Exploration, Geological Surveying, Environmental Monitoring, Defense and Military, Search and Rescue Operations) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Lockheed Martin Corporation, Geonics Limited, Leonardo, EMCORE Corporation, Geospace Technologies, CETC, Quantum Magnetics, Magellan Aerospace, Mistras Group, Terra Exploration, Thales Group, Northrop Grumman Corporation, L3Harris Technologies Inc., Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |