Quick Navigation

Report Overview

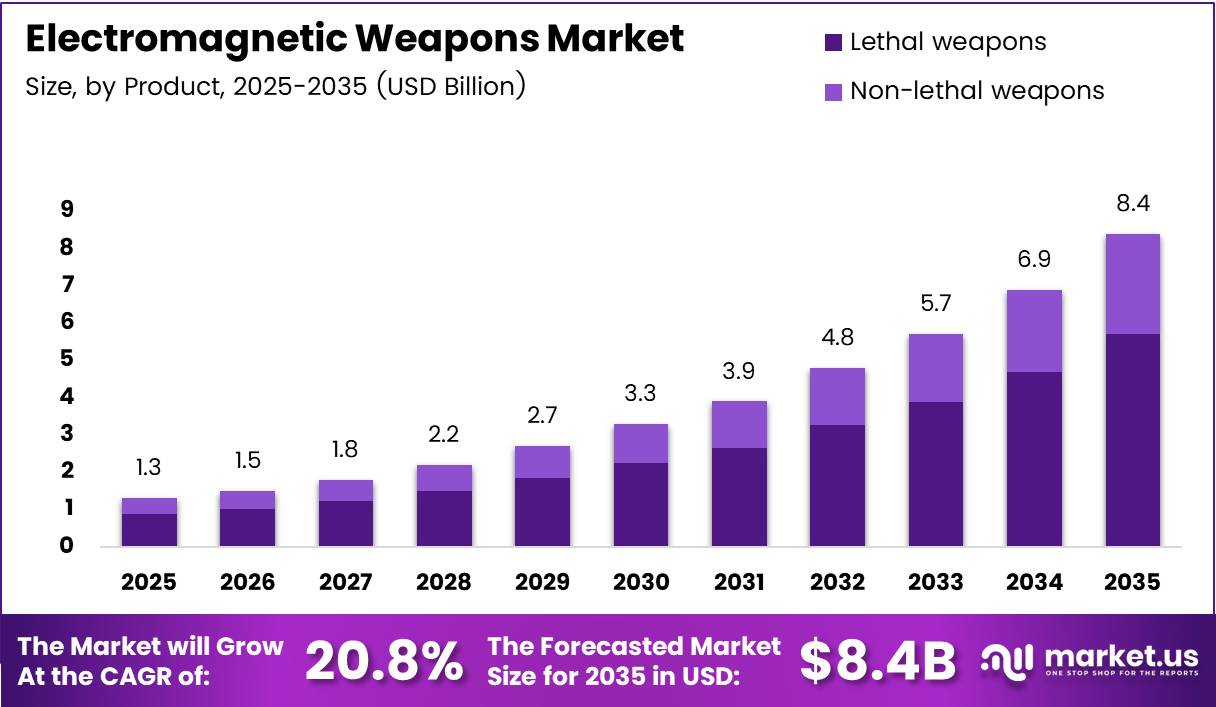

Global Electromagnetic Weapons Market size is expected to be worth around USD 8.4 Billion by 2035 from USD 1.3 Billion in 2025, growing at a CAGR of 20.8% during the forecast period 2026 to 2035.

The electromagnetic weapons market covers directed-energy systems, railguns, high-power microwave devices, and laser-induced plasma channel weapons used by military and homeland security forces. Defense agencies worldwide treat these systems as strategic alternatives to conventional munitions, particularly for precision engagements where minimizing collateral damage is operationally critical.

Lethal and non-lethal electromagnetic platforms serve distinct mission profiles. Lethal systems target high-value hardware — aircraft, missiles, and armored vehicles — while non-lethal variants disable electronic infrastructure or crowd-control targets without permanent physical destruction. This dual-use structure broadens addressable procurement budgets across multiple defense departments simultaneously.

Military applications drive the bulk of procurement activity, with land-based platforms accounting for the largest platform share. However, naval integration is accelerating as major navies recognize the cost-per-engagement advantage of directed-energy systems over conventional interceptor missiles, particularly for layered defense against drone swarms and hypersonic threats.

Government R&D investments are escalating at a measurable pace. In 2025, Japan’s Acquisition, Technology and Logistics Agency allocated 800 million yen (approximately 5.2 million USD) specifically for high-power microwave device development to counter drone swarms. This level of dedicated annual R&D spend signals that electromagnetic counter-UAS capability has moved from experimental to priority acquisition status across Pacific defense agencies.

Innovation concentration reveals a structural competitive dynamic. According to a 2025 analysis, approximately 90 percent of global HPM-related patents are owned by China-affiliated organizations. This patent dominance positions China as the lead innovator in electromagnetic pulse and HPM weapon technologies — a reality that is reshaping U.S. and allied procurement strategies toward accelerated domestic development programs.

The convergence of power storage improvements, compact form factors, and counter-drone mission urgency creates conditions where procurement timelines are compressing. Defense budgets in North America, Europe, and Asia Pacific are allocating dedicated electromagnetic weapon line items — a structural shift from discretionary R&D spending toward operational acquisition funding that validates long-term market expansion.

Key Takeaways

- The global Electromagnetic Weapons Market was valued at USD 1.3 Billion in 2025 and is forecast to reach USD 8.4 Billion by 2035.

- The market advances at a CAGR of 20.8% during the forecast period 2026 to 2035.

- By Product, Lethal Weapons held the dominant share at 67.4% in 2025.

- By Technology, High Laser-Induced Plasma Channel (LIPC) led with a 61.3% share in 2025.

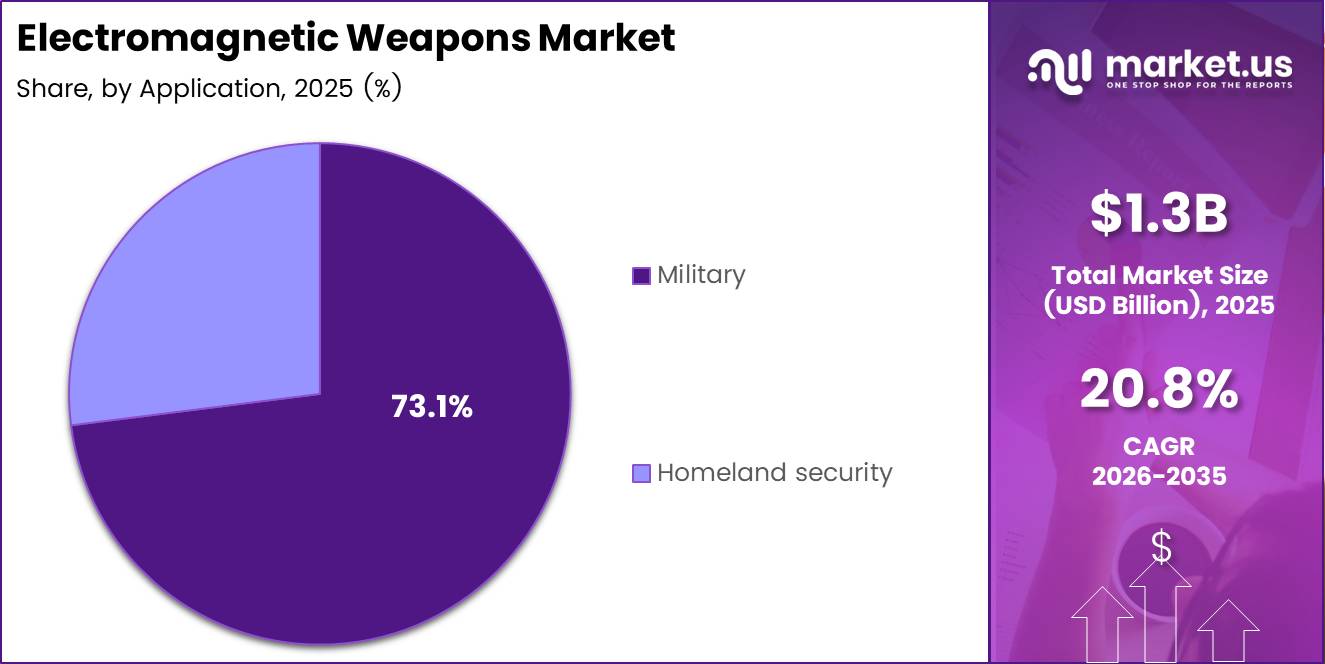

- By Application, Military accounted for the largest share at 73.1% in 2025.

- By Platform, Land-based systems dominated with a 51.2% share in 2025.

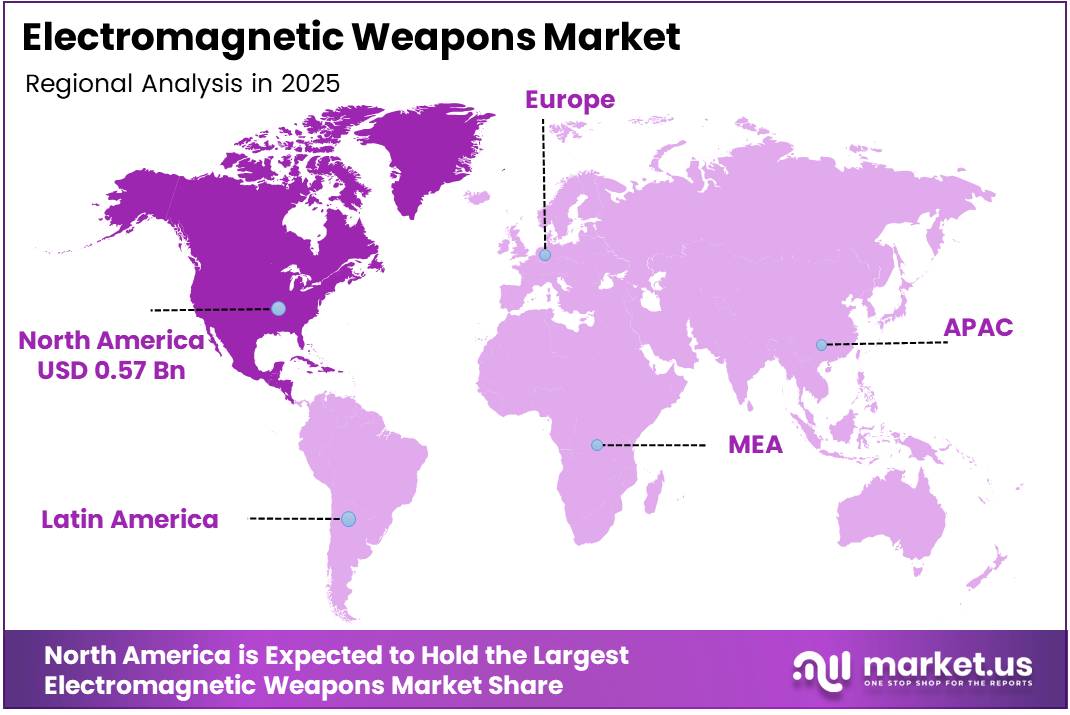

- North America led all regions with a 43.90% share, valued at USD 0.57 Billion in 2025.

Product Analysis

Lethal Weapons dominate with 67.4% due to high-value hardware destruction requirements.

In 2025, Lethal Weapons held a dominant market position in the By Product segment of the Electromagnetic Weapons Market, with a 67.4% share. Defense agencies prioritize lethal systems because they permanently neutralize high-value targets — missiles, UAVs, and armored platforms — at a fraction of the per-engagement cost of conventional munitions. This cost structure compels procurement officers to reallocate capital toward directed-energy alternatives.

Non-Lethal Weapons serve a distinct and strategically important procurement tier. These systems disable electronic infrastructure, disrupt communications, or incapacitate personnel without inflicting permanent physical damage — making them viable for homeland security, crowd control, and urban warfare scenarios where rules of engagement restrict lethal force. Consequently, non-lethal electromagnetic systems access a separate budget channel beyond conventional defense procurement.

Technology Analysis

High Laser-Induced Plasma Channel (LIPC) dominates with 61.3% due to precision long-range engagement capability.

In 2025, High Laser-Induced Plasma Channel (LIPC) held a dominant market position in the By Technology segment of the Electromagnetic Weapons Market, with a 61.3% share. LIPC systems create a conductive plasma channel through the atmosphere, enabling directed electrical discharges at distant targets with high accuracy. This precision advantage over area-effect alternatives makes LIPC the preferred technology for engagements requiring minimal collateral impact. In 2025, Japan’s railgun sea trials on the JMSDF test ship Asuka demonstrated muzzle velocities above 2,300 m/s with barrel life exceeding 200 shots, validating that electromagnetic acceleration technology is crossing operational durability thresholds.

Particle Beam Weapons (PBW) operate on a fundamentally different physical mechanism — accelerating charged particles to near-relativistic velocities to deliver kinetic and ionizing energy simultaneously. PBW systems carry higher infrastructure requirements than LIPC alternatives, which currently limits their deployment to fixed installations and large naval platforms. However, as power generation systems become more compact, PBW technology is positioned to expand beyond stationary applications into mobile defense platforms.

Application Analysis

Military dominates with 73.1% due to precision strike and anti-drone mission priority.

In 2025, Military held a dominant market position in the By Application segment of the Electromagnetic Weapons Market, with a 73.1% share. Military procurement commands this share because electromagnetic weapons address capability gaps that conventional munitions cannot fill cost-effectively — particularly counter-drone, missile defense, and electronic attack missions. The cost-per-intercept advantage over kinetic systems is compelling enough that military buyers are accelerating procurement timelines.

Homeland Security represents a structurally distinct application that is expanding as the threat profile of civilian airspace evolves. Unauthorized drone incursions near critical infrastructure, airports, and public events have prompted homeland security agencies to evaluate electromagnetic non-lethal systems for area denial. This application tier operates under different acquisition frameworks and legal constraints than military procurement, creating a separate but additive demand channel.

Platform Analysis

Land dominates with 51.2% due to established ground defense infrastructure.

In 2025, Land held a dominant market position in the By Platform segment of the Electromagnetic Weapons Market, with a 51.2% share. Ground-based platforms benefit from existing power infrastructure, easier maintenance access, and fewer weight and size constraints than airborne or naval alternatives. This integration advantage accelerates deployment cycles and reduces per-unit system cost for land-based electromagnetic installations.

Airborne platforms introduce the most demanding engineering constraints in electromagnetic weapon integration. Power generation limits, weight budgets, and aerodynamic heat management create technical barriers that are narrowing but not yet eliminated. However, airborne electromagnetic systems offer unmatched engagement geometry — particularly for targeting ground-based electronics and communications — making continued R&D investment commercially justified despite deployment complexity.

Naval platforms are emerging as the highest-growth deployment environment for electromagnetic weapons. Shipboard power generation capacity supports high-energy railgun and HPM systems that land or airborne platforms cannot sustain. Additionally, naval electromagnetic systems address layered fleet defense requirements — intercepting missiles, drones, and small surface threats — at a cost-per-engagement that extends the operational life of surface combatants in contested maritime environments.

Key Market Segments

By Product

- Lethal Weapons

- Non-Lethal Weapons

By Technology

- Particle Beam Weapons (PBW)

- High Laser-Induced Plasma Channel (LIPC)

By Application

- Military

- Homeland Security

By Platform

- Land

- Airborne

- Naval

Drivers

Defense Agencies Accelerate Directed Energy Investment to Close Non-Kinetic Warfare Gaps

Defense budgets worldwide are shifting from evaluation-phase allocations to operational acquisition funding for directed-energy and electromagnetic systems. This shift reflects military doctrine evolution — modern conflict increasingly involves electronic attack, drone swarm suppression, and precision strike requirements where conventional munitions are cost-prohibitive. Electromagnetic weapons address all three simultaneously, compelling budget reallocation across major defense agencies.

The demand for non-kinetic warfare capability is structural, not cyclical. Adversaries increasingly rely on drone swarms, electronic jamming, and hypersonic delivery vehicles — all of which require electromagnetic countermeasures that kinetic systems cannot intercept cost-effectively. A U.S. Navy electromagnetic railgun test demonstrated a 10.64 megajoule shot that accelerated a 3.2 kg projectile to 2,520 m/s — a performance metric that illustrates the kinetic energy delivery achievable without explosive warheads, reducing per-round logistics cost substantially.

Precision strike requirements further reinforce this driver. Modern warfare demands engagement accuracy that limits collateral damage — a mission parameter that electromagnetic systems fulfill through directed, controllable energy delivery. In October 2024, Epirus received a nearly 17 million USD contract modification from the U.S. Army Rapid Capabilities and Critical Technologies Office to upgrade its Integrated Fires Protection Capability High-Power Microwave systems. This contract demonstrates that military buyers are now funding performance enhancements — not just prototypes — confirming the transition to operational procurement.

Restraints

High Energy Requirements and Operational Reliability Challenges Limit Deployment Scalability

Electromagnetic weapon systems require power generation infrastructure that current mobile platforms cannot consistently supply. Railguns and high-power microwave systems demand megajoule-scale energy per shot — far exceeding what conventional vehicle or aircraft power systems generate. This energy gap forces electromagnetic systems into fixed installations or large naval vessels, restricting deployment flexibility across rapid-response military scenarios.

Development costs compound the infrastructure barrier. Engineering directed-energy systems to operational reliability standards requires iterative prototype testing, advanced materials, and precision manufacturing — all carrying significant per-unit cost. The consequence is that smaller defense budgets and allied nations find full acquisition prohibitively expensive, limiting the addressable customer base to a narrow tier of well-funded military establishments.

Operational reliability under real-world conditions remains an unresolved technical challenge. The same 2025 analysis that identified continental-scale impact from a high-altitude electromagnetic pulse weapon also highlights that the electronics within EMP-generating systems face the same susceptibility risks they are designed to exploit — creating a systems hardening requirement that raises both development cost and deployment timelines. This circular technical challenge slows procurement confidence among operational commanders who require proven uptime in contested environments.

Growth Factors

Naval Expansion, Missile Defense Integration, and Counter-Drone Applications Unlock New Procurement Tiers

Integration of electromagnetic weapons into missile defense architectures creates a structurally new procurement category. Unlike standalone directed-energy systems, missile defense integration requires electromagnetic weapons to operate within multi-domain command networks — a capability requirement that raises contract value, extends program lifecycles, and deepens vendor lock-in. Defense agencies pursuing layered missile defense are therefore creating durable, high-value contracts for electromagnetic system integrators.

Naval platform expansion amplifies this opportunity. Shipboard power generation capacity makes large surface combatants the most viable deployment environment for high-energy electromagnetic systems. The U.S. Navy’s newer railgun launcher under development is designed for shots approaching 30 megajoules — nearly triple the 10.64 MJ demonstrated in earlier tests — a planned performance step-change that drives procurement of next-generation shipboard power and thermal management systems alongside the weapon itself. In November 2024, Verus Research secured a 1.8 million USD DARPA contract to develop agile high-power microwave waveforms for operational naval use, validating active investment in this platform tier.

Counter-drone applications represent the most immediately scalable growth channel. Drone proliferation across conflict zones, border regions, and civilian airspace creates sustained demand for cost-effective electromagnetic interdiction systems. Compact and mobile electromagnetic platforms — designed specifically for counter-drone missions — address procurement requirements of both military field units and homeland security agencies, effectively doubling the addressable buyer base without requiring full-scale defense infrastructure.

Emerging Trends

Railgun Maturation, Electronic Warfare Integration, and Hypersonic Directed-Energy Research Define the Next Capability Wave

Railgun technology is crossing from experimental to operationally relevant status. The combination of hypersonic muzzle velocities and extended barrel life — demonstrated in 2025 trials — signals that railguns will enter active naval inventories within this forecast decade. Microwave weapons operating in the 300 MHz to 300,000 MHz range, with pulse durations of 100 nanoseconds to 1 microsecond, define a proven technical envelope that manufacturers are now industrializing rather than still researching.

Electronic warfare system integration is reshaping how defense forces structure electromagnetic weapon procurement. Rather than treating directed-energy systems as standalone platforms, military planners now embed them within broader electronic warfare architectures — combining jamming, sensing, and directed-energy functions into unified engagement systems. In November 2024, Thales Australia and the University of Adelaide announced a partnership to develop an ultra-short pulse laser directed-energy weapon for extended-range counter-UAS missions, illustrating this integration-first approach at the program level.

Hypersonic and directed-energy integration research is intensifying across allied defense agencies. Strategic defense collaborations and joint development programs between NATO members and Pacific allies are compressing individual R&D timelines by pooling technical expertise. This collaborative model accelerates time-to-deployment for electromagnetic systems while distributing development cost — structurally advantaging established prime contractors with existing alliance relationships over new market entrants.

Regional Analysis

North America Dominates the Electromagnetic Weapons Market with a Market Share of 43.90%, Valued at USD 0.57 Billion

North America holds 43.90% of the global electromagnetic weapons market, valued at USD 0.57 Billion in 2025. The U.S. Department of Defense drives this position through sustained directed-energy procurement programs, active railgun and HPM development contracts, and operational integration across Army, Navy, and Air Force platforms. This institutional depth creates procurement advantages that allied suppliers are structured to serve exclusively.

Europe Electromagnetic Weapons Market Trends

European defense agencies are expanding electromagnetic weapon investment as NATO commitments and Russia-Ukraine conflict lessons reshape procurement priorities. Germany, France, and the UK lead regional allocation toward directed-energy systems, particularly for counter-drone and electronic warfare applications. Joint development programs between European prime contractors and allied research institutions are compressing regional capability gaps relative to North American counterparts.

Asia Pacific Electromagnetic Weapons Market Trends

Asia Pacific commands the most dynamic electromagnetic weapon development pipeline outside North America. Japan’s dedicated HPM and railgun programs, combined with China’s dominant patent position in HPM technologies, establish the region as the primary competitive arena for next-generation electromagnetic weapon development. India and South Korea are also scaling directed-energy R&D allocations as regional threat environments intensify.

Middle East and Africa Electromagnetic Weapons Market Trends

Middle East defense agencies — particularly GCC nations — are integrating electromagnetic weapon systems as part of layered air defense upgrades against drone and missile threats. Procurement activity concentrates on counter-UAS and base protection applications. Sustained defense budget allocations across Gulf states provide a commercially accessible procurement tier for established electromagnetic weapon vendors with existing regional relationships.

Latin America Electromagnetic Weapons Market Trends

Latin American electromagnetic weapon procurement remains nascent, constrained by defense budget limitations and the region’s lower threat exposure to advanced aerial systems. However, border security and counter-narcotics drone operations are generating initial demand for compact, cost-effective electromagnetic interdiction systems. Brazil and Mexico represent the primary early-adopter markets within this region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

BAE Systems positions itself as an integrated directed-energy and railgun systems provider across land and naval platforms. The company’s strategic advantage lies in its ability to bridge R&D output from national defense laboratories into production-ready hardware — a capability that defense agencies prioritize when selecting prime contractors for long-cycle electromagnetic weapon programs. This integration depth reduces program risk for procurement offices managing complex multi-domain deployment requirements.

Boeing leverages its aerospace and systems engineering infrastructure to develop high-energy laser and electromagnetic weapon platforms optimized for airborne deployment. The airborne electromagnetic weapon segment carries the highest technical barriers in the market — power management, weight constraints, and aerodynamic integration — creating a natural competitive moat for contractors with established aircraft integration experience. Boeing’s position in this technically demanding tier insulates it from lower-cost competitors entering ground-based segments.

Elbit Systems concentrates its electromagnetic weapon portfolio on exportable, compact directed-energy and electronic warfare systems. This market positioning targets allied defense agencies with smaller procurement budgets that cannot absorb the acquisition cost of large-scale U.S. or European prime contractor systems. By focusing on modular, cost-contained platforms, Elbit accesses a customer tier that larger competitors structurally underserve — a defensible market position that scales with global counter-drone demand growth.

General Atomics leads in electromagnetic launch system development, most notably through its railgun and electromagnetic aircraft launch system programs. Its technical specialization in pulsed-power systems — the core enabling technology for railguns and high-energy microwave weapons — positions it as an essential component supplier even to competitors developing competing platform architectures. In July 2025, Epirus secured a 43,551,060 USD Army contract to deliver two IFPC High-Power Microwave Generation II systems, illustrating the scale of contracts now flowing to specialized HPM system developers in this market.

Key Players

- BAE Systems

- Boeing

- Elbit Systems

- General Atomics

- Honeywell

- L3Harris Technologies

- Lockheed Martin

- Northrop Grumman

- QinetiQ

- Rafael Advanced Defense Systems

- Raytheon Technologies

- Rheinmetall

- Thales

Recent Developments

- October 2024 — Epirus received a nearly 17 million USD contract modification from the U.S. Army Rapid Capabilities and Critical Technologies Office to develop and integrate an upgraded sensor suite for its Integrated Fires Protection Capability High-Power Microwave systems. This contract enhancement targeted counter-drone and counter-electronics performance improvements for operationally deployed HPM platforms.

- November 2024 — Verus Research secured a one-year 1.8 million USD contract from the U.S. Defense Advanced Research Projects Agency to continue work with the U.S. Naval Research Laboratory on the Waveform Agile RF Directed Energy program. The program focuses on developing and experimentally validating agile high-power microwave waveforms for operational naval deployment.

- November 2024 — Thales Australia and the University of Adelaide announced a partnership to develop an ultra-short pulse laser directed energy weapon for extended-range counter-UAS missions. The collaboration explores ultra-short pulse laser technology as a replacement for long-range continuous-wave directed-energy systems in counter-drone applications.

- July 2025 — Epirus announced a 43,551,060 USD contract from the U.S. Army Rapid Capabilities and Critical Technologies Office to deliver two Integrated Fires Protection Capability High-Power Microwave Generation II systems, including test events, support equipment, and spares. This contract builds on four IFPC-HPM systems delivered in May 2024, expanding the Army’s operational HPM counter-drone capability.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.3 Billion |

| Forecast Revenue (2035) | USD 8.4 Billion |

| CAGR (2026-2035) | 20.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Lethal Weapons, Non-Lethal Weapons), By Technology (Particle Beam Weapons, High Laser-Induced Plasma Channel), By Application (Military, Homeland Security), By Platform (Land, Airborne, Naval) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | BAE Systems, Boeing, Elbit Systems, General Atomics, Honeywell, L3Harris Technologies, Lockheed Martin, Northrop Grumman, QinetiQ, Rafael Advanced Defense Systems, Raytheon Technologies, Rheinmetall, Thales |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |