Quick Navigation

Report Overview

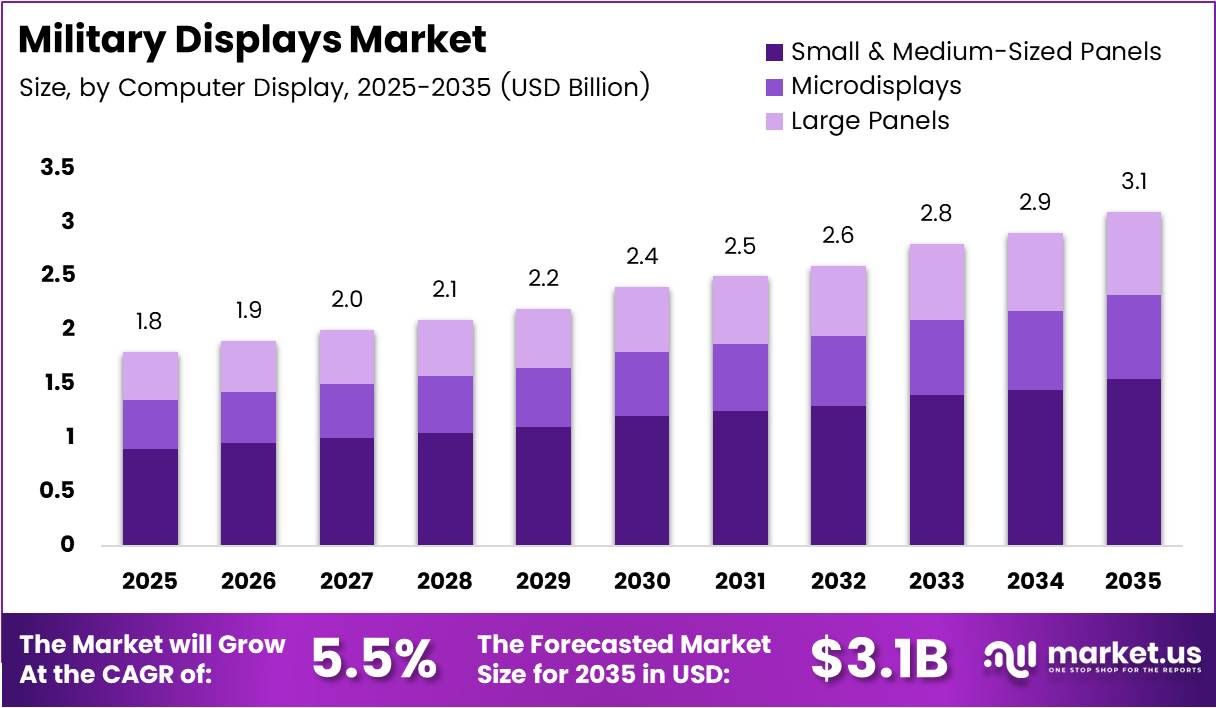

Global Military Displays Market size is expected to be worth around USD 3.1 Billion by 2035 from USD 1.8 Billion in 2025, growing at a CAGR of 5.5% during the forecast period 2026 to 2035.

The military displays market covers specialized visual interface systems built for defense operations across land, naval, and airborne environments. These systems include vehicle-mounted screens, handheld units, wearables, simulators, and ruggedized computer displays. Unlike commercial display markets, procurement here flows through defense budgets, long approval cycles, and strict military qualification standards.

Defense forces worldwide are replacing legacy display systems with higher-performance units that meet modern battlefield requirements. Smart displays now account for the dominant share within the technology mix, reflecting a shift toward integrated, software-driven visual platforms. This shift directly benefits vendors with established MIL-STD qualification experience and certified supply chains.

Land-based applications command the largest share of end-use demand, followed by airborne and naval segments. Vehicle-mounted displays hold the top position within product categories, reflecting the scale of armored vehicle modernization programs running across NATO members and allied nations. These programs create recurring procurement cycles, not one-time equipment buys.

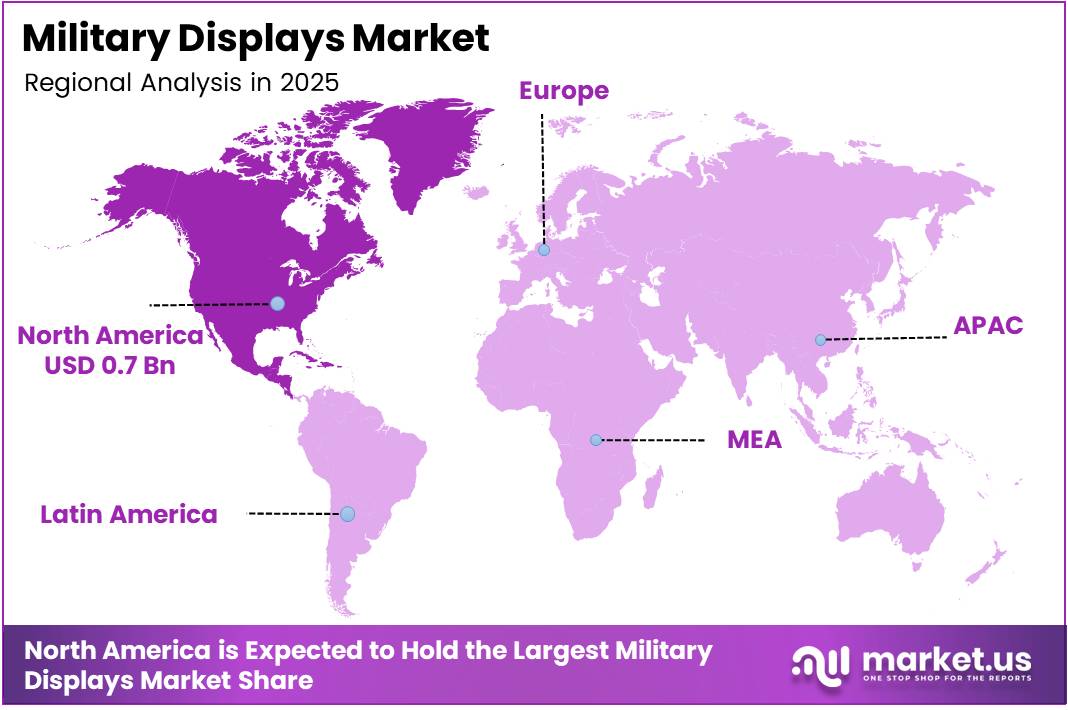

North America leads all regions with a 43.1% share, valued at approximately USD 0.7 Billion, anchored by sustained U.S. Department of Defense modernization budgets and a deep defense industrial base. In April 2024, EIZO Rugged Solutions launched the Talon RGD2443W, a 24-inch 4K ruggedized LCD monitor from its Orlando facility, targeting naval, ground control, and airborne applications — illustrating how new product activity continues to track closely with active procurement programs.

According to Cevians, sunlight-readable military displays deliver 1,000–2,500 nits luminance, compared with only 400–700 nits for standard daylight-readable units. This gap matters because field operators depend on screen legibility in direct sunlight — meaning procurement officers cannot substitute commercial-grade displays without accepting operational risk.

According to oled-info.com, Lumicore’s 2025 revision of its 0.71-inch FHD OLED microdisplay achieves 3,000 nits brightness with more than 92% luminance uniformity across the panel. This performance threshold signals that OLED microdisplays have crossed the viability line for helmet-mounted and near-eye military optics — a segment that previously relied on older display technologies with lower output and heavier form factors.

Vendors that invest now in OLED and MicroLED qualification for defense use cases position themselves ahead of the next procurement wave. The combination of brightness, power efficiency, and resolution improvements removes the last major technical objections to adoption in high-stakes airborne and soldier-worn applications.

Key Takeaways

- The Global Military Displays Market is valued at USD 1.8 Billion in 2025 and is forecast to reach USD 3.1 Billion by 2035, at a CAGR of 5.5%.

- By Product Type, Vehicle Mounted displays dominate with a 37.9% share in 2025.

- By Type, Smart Displays lead with a 58.3% share, reflecting strong adoption of integrated, software-driven display platforms.

- By Computer Display, Small and Medium-Sized Panels hold the largest share at 46.8%.

- By Technology, LCD holds the top position with a 38.5% share in the military displays technology mix.

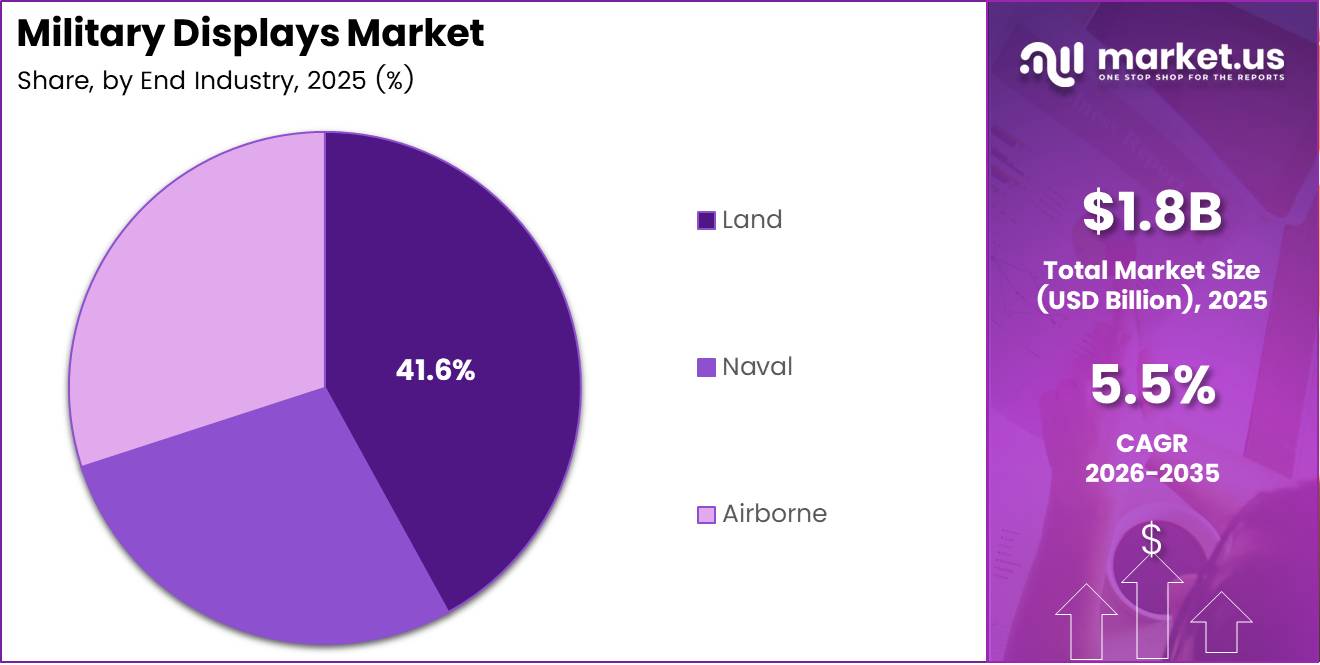

- By End Industry, Land applications account for the dominant share at 41.6%, driven by armored vehicle modernization programs.

- North America dominates regional demand with a 43.1% market share, valued at approximately USD 0.7 Billion.

Product Analysis

Vehicle Mounted displays dominate with 37.9% due to large-scale armored vehicle modernization programs.

In 2025, Vehicle Mounted displays held a dominant market position in the By Product Type segment of the Military Displays Market, with a 37.9% share. Armored vehicle upgrade programs across NATO members and allied forces create multi-year, high-volume procurement contracts. This gives vehicle-mounted display vendors a structural revenue advantage over segments tied to smaller-unit or individual-soldier equipment.

Handheld displays serve dismounted infantry and forward operating units requiring portable visual interfaces in the field. Their procurement scales with infantry modernization budgets, which tend to move in smaller tranches than platform-level vehicle programs. However, handheld units increasingly require the same ruggedization and sunlight-readability standards as vehicle systems, narrowing the cost gap between both segments.

Wearables represent the fastest-moving form factor within the military displays product mix. Helmet-mounted displays and soldier-worn visual systems are gaining traction in airborne and special operations applications. The technical barrier remains high, as wearable displays must balance brightness, weight, and battery life — all within MIL-STD qualification constraints that commercial wearables do not face.

Simulators serve training commands that require high-fidelity visual environments without deploying live equipment. Defense agencies invest in simulation to reduce operational wear on costly hardware and to train personnel on threat scenarios that cannot be replicated in field exercises. Simulator displays demand extremely high resolution and refresh rates to maintain training realism.

Computer Displays cover command-and-control workstations, intelligence analysis terminals, and operations center infrastructure. These units operate in more controlled environments than field equipment but still require MIL-STD compliance for shock, vibration, and electromagnetic compatibility. Demand tracks closely with network-centric warfare infrastructure investments.

Type Analysis

Smart Displays dominate with 58.3% due to integrated software capability for modern tactical operations.

In 2025, Smart Displays held a dominant market position in the By Type segment of the Military Displays Market, with a 58.3% share. Smart displays combine processing capability, multi-source data visualization, and network connectivity in a single unit. Defense buyers now treat this integration as a baseline requirement, not an upgrade — which locks out conventional alternatives from most new procurement programs.

Conventional Displays retain a role in cost-constrained applications and legacy platform maintenance programs. Older naval vessels, ground vehicles still mid-lifecycle, and training facilities operate conventional units that procurement managers extend rather than replace. However, each new platform generation shifts the default specification toward smart displays, compressing the long-term addressable base for conventional units.

Computer Display Analysis

Small and Medium-Sized Panels dominate with 46.8% due to versatile fit across vehicle and portable systems.

In 2025, Small and Medium-Sized Panels held a dominant market position in the By Computer Display segment of the Military Displays Market, with a 46.8% share. These panels fit vehicle consoles, portable command terminals, and cockpit instrument clusters — spanning the widest range of platform types within the military display ecosystem. Their cross-platform applicability creates higher unit volumes than any other size category.

Microdisplays serve helmet-mounted sights, rifle-mounted systems, and night-vision-integrated eyepieces. Their adoption is constrained by the technical difficulty of achieving the brightness and resolution required for military optics within an extremely compact form factor. Advances in OLED microdisplay technology in 2025 have begun removing this constraint, positioning microdisplays for wider integration into soldier-worn platforms.

Large Panels equip operations centers, naval combat management systems, and ground-based command infrastructure. Their use cases are fewer but carry high contract values, as large-format rugged display systems require custom integration, high-grade EMI shielding, and multi-signal input management. Procurement volume is lower, but per-unit revenue contribution is disproportionately high.

Technology Analysis

LCD dominates with 38.5% due to proven qualification record and cost-effective production base.

In 2025, LCD held a dominant market position in the By Technology segment of the Military Displays Market, with a 38.5% share. LCD technology benefits from decades of MIL-STD qualification history, an established supply chain, and lower production costs relative to OLED or AMOLED alternatives. Defense procurement offices favor proven technologies for mission-critical applications where supply continuity matters as much as performance.

LED technology provides the backlighting infrastructure for a significant portion of current military display installations. LED backlights deliver the high luminance levels required for sunlight-readable panels while offering longer operational lifespans than fluorescent predecessors. Their embedded role across vehicle and shipborne systems ensures sustained demand even as frontline display technologies evolve.

AMOLED displays offer superior contrast ratios and faster response times than LCD, making them better suited for low-light tactical environments where image clarity at night matters. Defense buyers evaluating AMOLED weigh these performance advantages against higher unit costs and a less extensive MIL-STD qualification track record compared to incumbent LCD systems.

OLED technology is moving toward broader adoption in helmet-mounted and near-eye military optics. Its ability to deliver high brightness, deep blacks, and thin form factors addresses the core requirements of wearable defense applications. Qualification investment by display manufacturers in 2024 and 2025 is building the compliance evidence base that defense procurement officers require before standardizing on new display technology.

End Industry Analysis

Land dominates with 41.6% due to high-volume armored vehicle and soldier systems procurement.

In 2025, Land applications held a dominant market position in the By End Industry segment of the Military Displays Market, with a 41.6% share. Ground forces operate the largest and most diverse equipment fleet within any national military, creating sustained demand across vehicle-mounted, handheld, and wearable display categories. Land program modernization cycles run on predictable multi-year budgets, giving display suppliers stable revenue visibility.

Naval applications require displays that withstand saltwater corrosion, shipboard vibration, and electromagnetic interference from onboard systems. Combat management consoles, bridge navigation displays, and below-deck tactical terminals all carry high per-unit specifications. Naval programs tend to run on longer replacement cycles than land vehicles, but contract values are substantially larger given the complexity of shipboard integration requirements.

Airborne applications place the most demanding weight, power, and reliability requirements on display systems. Cockpit multifunction displays, helmet-mounted sights for fighter pilots, and mission system terminals must all operate across extreme temperature and vibration profiles while maintaining zero tolerance for failure. In September 2024, Thales Defense and Security received a USD 1.6 million contract from the U.S. Defense Innovation Unit to develop F-22-specific upgrades for its Scorpion helmet-mounted display — illustrating the precision engineering investment that airborne display development demands.

Key Market Segments

By Product Type

- Vehicle Mounted

- Handheld

- Wearables

- Simulators

- Computer Displays

By Type

- Smart Displays

- Conventional Displays

By Computer Display

- Small and Medium-Sized Panels

- Micro-displays

- Large Panels

By Technology

- LCD

- LED

- AMOLED

- OLED

By End Industry

- Land

- Naval

- Airborne

Drivers

Defense Modernization and Situational Awareness Requirements Force Display Upgrades Across All Platforms

Armed forces worldwide are replacing aging display systems as part of broad modernization programs that span ground vehicles, aircraft, and naval platforms. These programs mandate higher-resolution, networked, and environmentally hardened display units. The result is a replacement cycle that does not depend on discretionary budget flexibility — it is built into multi-year platform upgrade contracts.

Situational awareness has become a core operational requirement across land, naval, and airborne missions. Modern display systems must aggregate data from sensors, mapping systems, and communications networks into a single readable interface. According to AGDisplays, a 2026 case study found that ruggedized LCD upgrades reduced field display failure rates by an estimated 40% — directly cutting mission downtime from display malfunction and making the operational case for premium display procurement undeniable.

Unmanned systems add a parallel layer of display demand. Drone operators and autonomous vehicle controllers require high-performance remote display interfaces that replicate real-time sensor feeds without latency or degradation. Augmented reality integration in military training further extends the requirement into wearable and near-eye displays. Each new platform category adds a distinct procurement stream to the overall demand base.

Restraints

High Development Costs and Stringent Military Qualification Standards Slow Market Access for New Entrants

Advanced military display technologies — particularly OLED, AMOLED, and MicroLED — carry development costs that far exceed commercial display programs. Defense buyers also require extensive qualification testing under MIL-STD-810, covering temperature, vibration, shock, humidity, and electromagnetic compatibility. These requirements add years and millions in cost before any unit reaches procurement consideration.

In December 2024, BAE Systems received a 133 million GBP (approximately 168 million USD) contract from the Eurofighter Typhoon consortium to further develop and flight-test the Striker II helmet-mounted display. This contract scale illustrates why advanced military display development remains restricted to large, well-capitalized defense primes — smaller vendors cannot sustain the R&D investment required to compete for flagship programs.

Procurement timelines compound the cost problem. Military display programs move through requirement definition, prototyping, testing, and full-rate production over periods that can span a decade. During that window, a vendor must maintain a qualified supply chain, absorb engineering change orders, and hold prices within contracted ranges. These structural barriers protect incumbents but effectively cap the number of credible market participants.

Growth Factors

OLED and MicroLED Advances, Wearable Displays, and Network-Centric Warfare Create New Revenue Segments

OLED and MicroLED technology improvements are opening display segments that were previously inaccessible for defense use. According to oled-info.com, Lumicore’s 2025 revision of its 0.71-inch FHD OLED microdisplay cuts power consumption by 50% compared with the prior generation while maintaining 3,000-nit brightness. A 50% power reduction at constant optical output directly addresses the battery endurance constraints that previously limited OLED adoption in soldier-worn military systems.

Wearable and head-mounted displays represent a high-value segment that defense agencies are actively expanding. Helmet-mounted displays for fighter pilots and ground soldiers require a combination of brightness, low weight, and night-vision compatibility that only advanced display technologies can meet. In April 2024, Industrial Electronic Engineers showcased its latest cockpit and mission displays for rotary-wing platforms at the Army Aviation Mission Solutions Summit, signaling active industry investment in airborne wearable display solutions.

Network-centric warfare expansion creates structural demand for displays across command, control, and intelligence systems. As military forces integrate more data sources into battlefield decision-making, the display interface becomes a critical chokepoint in the information chain. Simulation and training systems require the same high-fidelity visualization as operational platforms, adding a parallel procurement stream that runs independently of operational equipment replacement cycles.

Emerging Trends

Touchscreen Interfaces, AI-Driven Visualization, and Ruggedized Lightweight Designs Reshape Military Display Standards

Touchscreen and gesture-based interfaces are displacing traditional button-and-dial control systems across military platforms. Defense procurement specifications now routinely include touch capability, which shifts display design requirements toward chemically strengthened glass, gloved-touch sensitivity, and surface coatings that maintain optical clarity in field conditions. Vendors without touch-certified ruggedized displays face an expanding specification gap against program requirements.

AI-driven data visualization is changing how operators interact with display systems in combat environments. Rather than raw sensor feeds, AI-processed displays present prioritized threat assessments and mission-relevant data overlays. According to notebookcheck.net, Lumicore’s upgraded OLED microdisplay integrates image-enhancement processing and MIPI interface support at 1,920 × 1,080 resolution, specifically targeting near-eye AR/VR and military optics — showing that display hardware is being co-developed with AI visualization capability from the component level upward.

Ruggedization for extreme environments and energy efficiency are converging into a single design mandate. Military operators deploy display systems across arctic cold, desert heat, high-humidity maritime conditions, and high-altitude airborne platforms — often within a single equipment program. At the same time, soldier-worn and vehicle systems face tightening power budgets. Vendors that achieve both environmental resilience and low power draw in the same qualified unit carry a decisive competitive advantage in future procurement competitions.

Regional Analysis

North America Dominates the Military Displays Market with a Market Share of 43.1%, Valued at USD 0.7 Billion

North America holds a 43.1% share of the global military displays market, valued at approximately USD 0.7 Billion. The United States Department of Defense drives this position through sustained multi-year modernization budgets covering ground vehicles, aircraft, and naval vessels. A mature domestic defense industrial base, strong certification infrastructure, and established procurement relationships with qualified display vendors reinforce this regional lead.

Europe Military Displays Market Trends

Europe maintains a substantial share of global military display demand, supported by NATO-driven equipment standardization requirements and active national defense upgrade programs. The United Kingdom, Germany, and France operate some of the most technically demanding military display programs on the continent. BAE Systems’ December 2024 Striker II helmet-mounted display contract with the Eurofighter Typhoon consortium confirms that European defense programs continue to fund high-specification display development at scale.

Asia Pacific Military Displays Market Trends

Asia Pacific defense spending has risen consistently across the region’s largest military powers. China, India, South Korea, and Japan each operate active modernization programs covering land, naval, and airborne platforms. These programs increasingly specify advanced display technology as a baseline requirement rather than an optional upgrade, creating a procurement environment that favors vendors with qualified OLED, LCD, and ruggedized display portfolios adapted to regional platform specifications.

Middle East and Africa Military Displays Market Trends

Middle East defense procurement concentrates in Gulf Cooperation Council nations, which import advanced military systems including display-equipped platforms from North American and European suppliers. Domestic defense manufacturing capacity in the region remains limited, meaning display technology typically enters through system-level platform contracts rather than direct component procurement. Africa’s military display demand remains modest and project-driven, tied largely to peacekeeping and border security equipment programs.

Latin America Military Displays Market Trends

Latin America represents the smallest regional share of military display demand. Brazil and Mexico operate the region’s largest defense forces, with procurement focused on maintaining existing platform fleets rather than large-scale modernization. Budget constraints limit access to premium display technologies, and most advanced display-equipped systems enter the region through foreign military sales programs rather than direct procurement from display manufacturers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Aselsan, Turkey’s largest defense electronics company, has built a strategic advantage in military displays through vertical integration — designing display controllers, signal processing, and ruggedized enclosures within a single domestic supply chain. This self-sufficiency reduces exposure to export control restrictions that constrain foreign suppliers and positions Aselsan as the preferred source for Turkish Armed Forces platform modernization programs requiring MIL-STD-qualified display systems.

BAE Systems occupies a dominant position in high-specification airborne display systems, anchored by its Striker II helmet-mounted display program. The December 2024 award of a 133 million GBP Eurofighter Typhoon contract validates BAE’s long-cycle investment in helmet-mounted display technology. This program positions BAE as the benchmark vendor for next-generation pilot display systems across NATO air forces, a position that is structurally difficult for competitors to displace without equivalent flight-test certification history.

CMC Electronics focuses on avionics display systems for fixed-wing and rotary-wing military platforms. Its strength lies in cockpit display integration — combining flight data, navigation, and mission system feeds into certified multifunction display architectures. CMC’s deep qualification experience within transport and patrol aircraft programs gives it a defensible position in the mid-tier airborne display segment, where procurement officers favor vendors with existing platform certification rather than new entrants.

Crystal Group specializes in ruggedized computing and display systems for ground-based military applications. Its market position centers on delivering MIL-STD-810-qualified systems that consolidate multiple electronic functions into space-constrained vehicle installations. Crystal Group’s focus on purpose-built hardware for extreme environments, rather than adapted commercial products, addresses the reliability requirements of land forces operating in high-shock, high-temperature deployment conditions.

Key Players

- Aselsan

- BAE Systems

- CMC Electronics

- Crystal Group

- Curtiss-Wright

- Elbit Systems

- General Digital

- General Dynamics

- Hatteland Technology

- L3Harris

- Leonardo

- Milcots

- Saab

- Thales

Recent Developments

- December 2024 — BAE Systems received a 133 million GBP (approximately 168 million USD) contract from the Eurofighter Typhoon consortium to further develop and flight-test the Striker II helmet-mounted display, advancing this advanced fighter-pilot helmet toward production readiness.

- September 2024 — Thales Defense and Security Inc. was awarded an initial 1.6 million USD Other Transaction Authority contract by the U.S. Defense Innovation Unit to develop F-22-specific upgrades for its Scorpion helmet-mounted display interface under the Raptor Open System Tactical-Helmet Display program.

- April 2024 — EIZO Rugged Solutions introduced the Talon RGD2443W, a 24-inch 4K ruggedized LCD monitor from its Orlando, Florida facility, targeting naval displays, ground control, and airborne operations, with the unit weighing under 10 pounds.

- April 2024 — Industrial Electronic Engineers announced it would exhibit its rugged military avionics display lineup at the Army Aviation Mission Solutions Summit in Denver, showcasing its latest cockpit and mission displays for rotary-wing platforms.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.8 Billion |

| Forecast Revenue (2035) | USD 3.1 Billion |

| CAGR (2026-2035) | 5.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Vehicle Mounted, Handheld, Wearables, Simulators, Computer Displays), By Type (Smart Displays, Conventional Displays), By Computer Display (Small and Medium-Sized Panels, Microdisplays, Large Panels), By Technology (LCD, LED, AMOLED, OLED), By End Industry (Land, Naval, Airborne) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Aselsan, BAE Systems, CMC Electronics, Crystal Group, Curtiss-Wright, Elbit Systems, General Digital, General Dynamics, Hatteland Technology, L3Harris, Leonardo, Milcots, Saab, Thales |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |