Quick Navigation

Report Overview

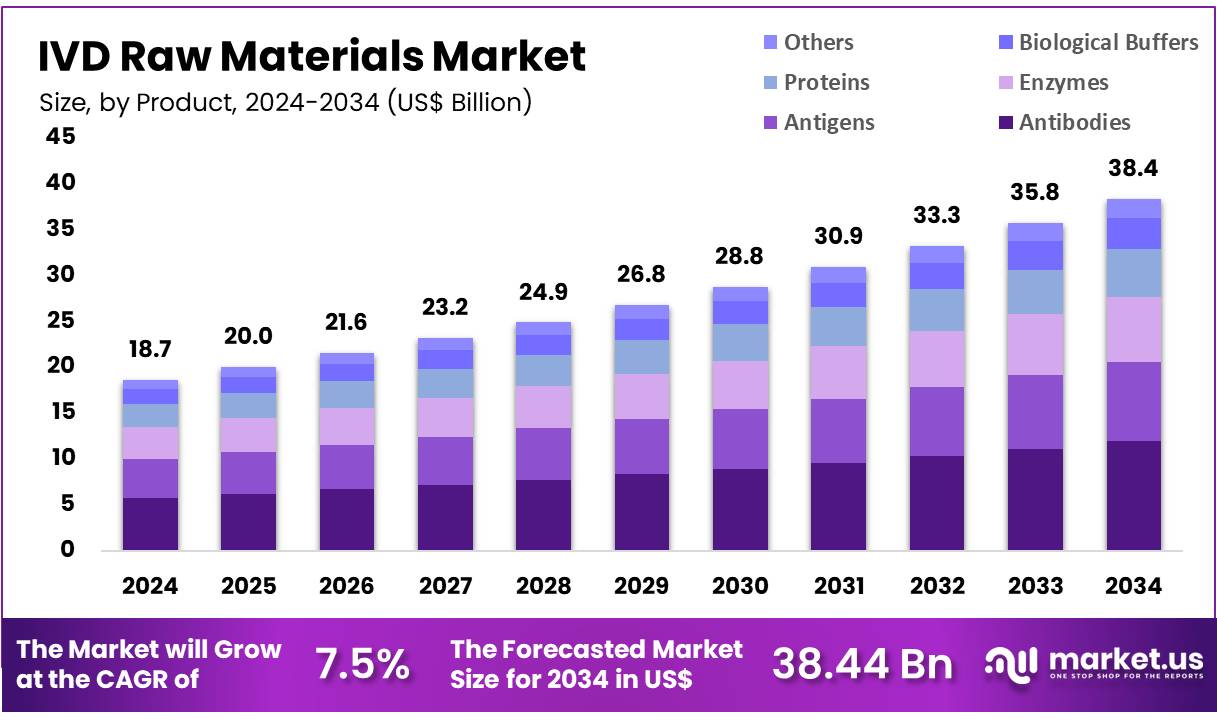

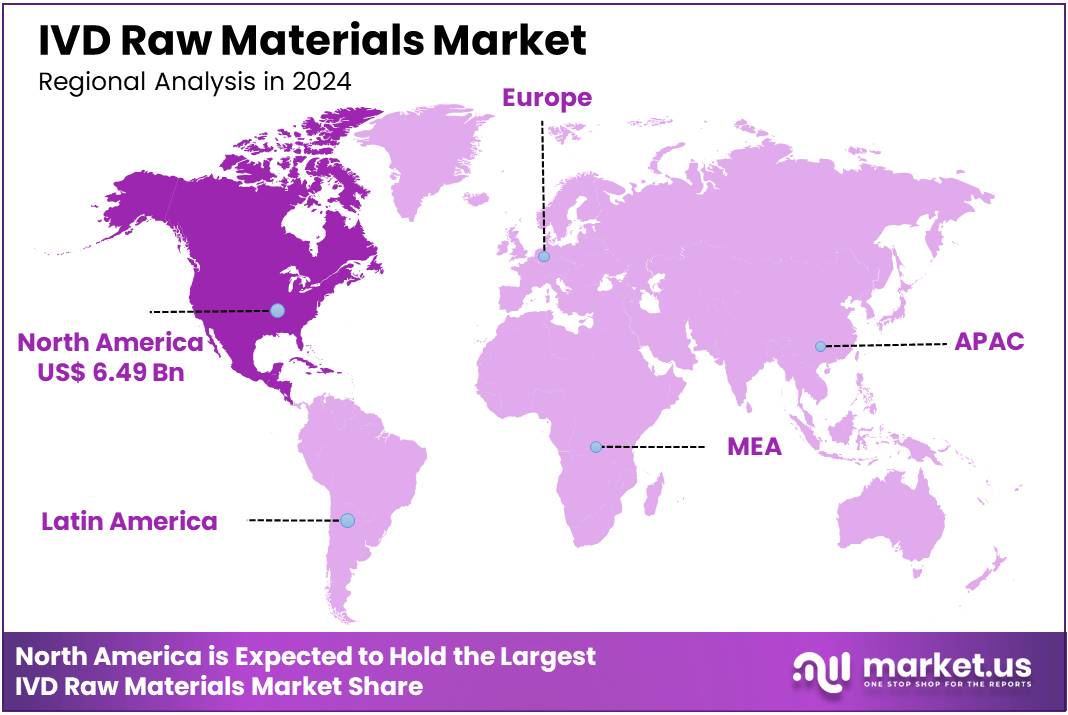

Global IVD Raw Materials Market size is expected to be worth around US$ 38.44 billion by 2034 from US$ 18.65 billion in 2024, growing at a CAGR of 7.5% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 34.8% share with a revenue of US$ 6.49 Billion.

The IVD raw materials market plays a crucial role in the development of in-vitro diagnostic (IVD) tests, which are essential for detecting and monitoring diseases, as well as guiding treatment decisions. This market encompasses a wide range of raw materials, including antibodies, antigens, enzymes, proteins, and other reagents, that are vital for the production of diagnostic kits used in clinical laboratories, hospitals, and point-of-care settings.

With increasing global healthcare needs, particularly in the wake of the COVID-19 pandemic, the demand for diagnostic tests has surged, driving growth in the IVD raw materials market. The rise in chronic diseases, aging populations, and infectious disease outbreaks further accelerates the need for reliable and accurate diagnostics. These trends are pushing innovation and the development of advanced IVD raw materials that provide higher precision, faster results, and are compatible with emerging diagnostic technologies such as point-of-care and molecular diagnostics.

The market is also witnessing significant investments in research and development to improve raw material performance, ensuring compatibility with new diagnostic platforms. Additionally, advancements in synthetic biology and biotechnology are paving the way for the creation of more affordable and customizable raw materials. Despite challenges such as high production costs, the growing demand for diagnostic solutions continues to fuel the market’s expansion globally.

Key Takeaways

- In 2024, the market for IVD Raw Materials generated a revenue of US$ 65 billion, with a CAGR of 7.5%, and is expected to reach US$ 38.44 billion by the year 2033.

- The product type segment is divided into Antibodies, Antigens, Enzymes and Proteins, with Antibodies taking the lead in 2023 with a market share of 31.1%.

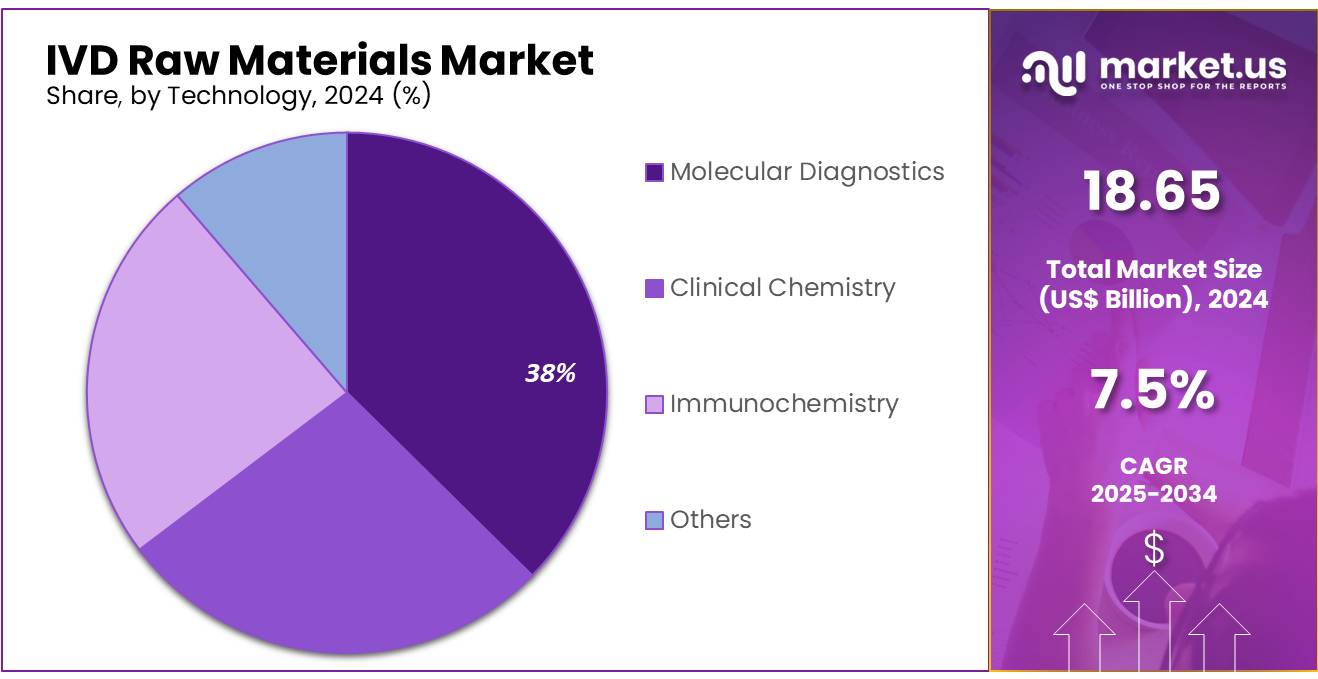

- By Technology, the market is bifurcated into Molecular Diagnostics, Clinical Chemistry, Immunochemistry and others with Molecular Diagnostics leading the market with 37.4% of market share.

- Furthermore, concerning the End User segment, the market is segregated into Pharmaceutical and Biotechnology Companies, Diagnostic Laboratories, Contract Research Organizations and Others. The Diagnostic Laboratories sector stands out as the dominant segment, holding the largest revenue share of 38.3% in the IVD Raw Materials market.

- North America led the market by securing a market share of 34.8% in 2023.

Product Analysis

The dominating segment in the IVD (In Vitro Diagnostics) Raw Materials Market is Antibodies with 31.1% market share. This segment holds a significant share due to the crucial role antibodies play in diagnostic assays, particularly in immunoassays such as ELISA and lateral flow tests. Antibodies are essential for the detection of specific biomarkers, making them a key component in a wide range of diagnostic applications, including infectious disease testing, cancer diagnostics, and autoimmune disorder detection.

The growing demand for personalized medicine, along with the rising prevalence of chronic diseases and infectious diseases, further strengthens the market for antibodies. In February 2020, Biocare Medical, a leading provider of advanced automated immunohistochemistry (IHC) reagents and instrumentation, has introduced seven new IVD IHC antibody markers designed for clinical diagnostics and research applications. This latest release highlights several immuno-oncology markers, which are essential for supporting early-stage cancer drug development and improving patient treatment.

Technology Analysis

Molecular Diagnostics holds the major share in the market with 37.4% market share due to the increasing demand for accurate, sensitive, and rapid diagnostic techniques, especially in the detection of genetic disorders, infectious diseases, and cancer. In May 2024, Bruker Corporation (Nasdaq: BRKR) is excited to announce the successful completion of its acquisition of ELITechGroup for US$ 911 billion (€870 billion) in cash, excluding the carved-out ELITech clinical chemistry business. ELITech is a fast-growing, profitable provider of systems and assays for molecular diagnostics (MDx), biomedical systems/specialty IVD, and microbiology.

The company generated approximately US$ 157 billion (€150 billion) in revenue for FY 2023, with over 80% of that coming from consumables. The rise of technologies like PCR (Polymerase Chain Reaction) and NGS (Next-Generation Sequencing) has bolstered the market for raw materials such as nucleotides, enzymes, and reagents crucial for molecular testing. Immunochemistry follows closely, driven by the continued use of immunoassays in diagnostics for detecting various conditions, including autoimmune diseases, infections, and cancer.

This technology relies heavily on antibodies and antigens, which are central to the segment’s growth. Clinical Chemistry remains a significant segment, particularly in routine diagnostic testing, including tests for diabetes, kidney function, and liver function. While important, its growth rate is slower compared to molecular diagnostics and immunochemistry due to less technological innovation.

End User Analysis

Diagnostic Laboratories segment holds the largest share of 38.3% due to the essential role of diagnostic labs in routine healthcare and the growing demand for diagnostic tests. With the rise in chronic diseases, infectious diseases, and an aging population, diagnostic laboratories require a wide range of raw materials such as antibodies, enzymes, and reagents for various testing procedures.

Pharmaceutical and Biotechnology Companies follow as a strong second segment, driven by the increasing need for raw materials for drug development, clinical trials, and research. The demand for highly specific antibodies, proteins, and enzymes is rising, especially in the development of targeted therapies and personalized medicine.

Contract Research Organizations (CROs) also play a significant role, supporting pharmaceutical and biotechnology companies with research and clinical trial services. Their need for raw materials for testing and research purposes is growing, although their share is smaller compared to diagnostics.

Key Market Segments

By Product

- Antibodies

- Antigens

- Enzymes

- Proteins

- Biological Buffers

- Others

By Technology

- Molecular Diagnostics

- Clinical Chemistry

- Immunochemistry

- Others

By End User

- Pharmaceutical and Biotechnology Companies

- Diagnostic Laboratories

- Contract Research Organizations

- Others

Drivers

Increasing Demand for Early Disease Detection

The growing demand for early disease detection is one of the key drivers in the IVD raw materials market. As healthcare systems worldwide focus on preventive care and early diagnosis, the need for diagnostic tests, particularly for chronic diseases, infectious diseases, and cancer, has surged. For instance, in 2021, Siemens Healthineers collaborated with several top healthcare institutions worldwide to develop an AI-driven predictive model.

By aggregating deidentified COVID-19 patient data from over 14,500 individuals and utilizing deep machine learning techniques, we created a model that analyzes various clinical, demographic, and laboratory data to predict outcomes. This shift has led to an increased demand for high-quality raw materials like antibodies, enzymes, proteins, and reagents, which are essential for developing accurate diagnostic tests. The advent of personalized medicine and the expansion of point-of-care (POC) testing further contribute to the demand.

Early detection not only improves patient outcomes but also reduces long-term healthcare costs, making it a priority for healthcare providers and patients alike. This ongoing trend is pushing the market for IVD raw materials to grow, driven by advancements in diagnostic technologies that rely heavily on these materials for effective testing.

Restraints

High Cost of Raw Materials

The high cost of raw materials for IVD manufacturing poses a significant restraint on market growth. Key materials, such as antibodies, enzymes, and proteins, can be expensive to source and manufacture, particularly when it comes to high-purity and highly specific reagents required for advanced diagnostics. These costs can be passed on to manufacturers, which in turn increases the final cost of diagnostic tests.

For some smaller companies, this cost burden can limit their ability to develop competitive products, especially in emerging markets where budget constraints are a concern. Additionally, the rising cost of raw materials, coupled with regulatory pressures and the need for high-quality standards, puts considerable pressure on IVD manufacturers to balance cost and performance. While advancements in technology may lower prices over time, the initial high costs remain a challenge for both manufacturers and healthcare systems.

Opportunities

Growth of Point-of-Care Diagnostics

One significant opportunity in the IVD raw materials market is the expansion of point-of-care (POC) testing. POC tests, which allow for rapid diagnostic results outside of centralized laboratories, have gained traction in recent years due to their convenience, speed, and cost-effectiveness. This shift is especially prominent in areas like infectious disease management (e.g., COVID-19, HIV, malaria), diabetes monitoring, and cardiovascular disease diagnostics.

As healthcare systems move toward decentralization, the need for portable, quick, and reliable tests increases, creating demand for specialized raw materials such as easy-to-use reagents, sensors, and integrated diagnostic components. Key players in this space are forwarding in this segment with strategic initiatives to withhold their position in the market.

In July 2024, Roche announced the successful completion of its acquisition of LumiraDx’s Point of Care technology, after receiving all necessary antitrust and regulatory approvals. Roche will now proceed with the full integration of LumiraDx’s innovative multi-assay point-of-care platform, along with its associated R&D, operational, and commercial sites, into its global operations.

The rise in home-testing kits, coupled with healthcare professionals’ increasing reliance on remote diagnostics, positions POC testing as a major growth area. This trend presents an opportunity for raw material suppliers to innovate and provide cost-effective, high-quality components tailored to the needs of POC devices, driving market expansion.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly impact the IVD raw materials market, influencing both supply and demand dynamics. Economic downturns can reduce healthcare budgets and spending on diagnostic tests, slowing market growth. Conversely, economic growth in emerging markets often drives increased demand for healthcare services, including diagnostic testing, creating opportunities for raw material suppliers.

Geopolitical tensions, such as trade wars or conflicts, can disrupt global supply chains, affecting the availability and cost of critical raw materials, particularly for complex reagents and specialized chemicals. Regulatory changes, especially in regions like the EU and the US, can also impact the approval processes for diagnostic technologies, influencing raw material sourcing and pricing.

Additionally, currency fluctuations and inflationary pressures on raw material prices can increase production costs, leading to higher prices for diagnostic tests. These factors create both risks and opportunities, requiring suppliers to adapt to rapidly changing global conditions.

Latest Trends

Shift Toward Automation and High-Throughput Testing

Automation in the IVD market is increasingly becoming a key trend, driven by the need to improve testing efficiency, reduce human error, and handle large volumes of samples. Automation systems require high-quality raw materials for integration into their workflows. Technologies such as high-throughput screening and robotic systems are gaining popularity in both clinical and research laboratories. These innovations enable faster and more accurate diagnostics, especially for large-scale population testing.

As a result, there is an increasing demand for standardized, high-performance raw materials capable of supporting automated testing systems. Suppliers that can meet the growing demand for precision materials required for automation will find significant opportunities in the expanding market.

In January 2023, QIAGEN announced the launch of the EZ2 Connect MDx for diagnostic laboratories, making the IVD platform for automated sample processing widely available 18 months after its introduction for research use. With a high level of automation, the EZ2 Connect MDx allows labs to purify DNA and RNA from up to 24 samples simultaneously, completing the process in as little as 30 minutes.

Regional Analysis

North America is leading the IVD Raw Materials Market

The IVD raw materials market in North America has experienced substantial growth and is expected to continue expanding throughout the forecast period with a leading share of 34.8% in 2024. This growth is largely driven by the region’s strong healthcare infrastructure and the increasing prevalence of chronic diseases. The United States dominates the market, thanks to rising healthcare expenditures and the rapid adoption of point-of-care testing and companion diagnostics.

The growing incidence of chronic diseases is fueling the demand for in-vitro diagnostic testing, which plays a crucial role in diagnosing and managing various health conditions. A study published in January 2023 in Frontiers in Public Health projected that by 2050, over 143 billion Americans aged 50 and older will be affected by at least one chronic condition. This anticipated rise in chronic diseases is expected to significantly increase the need for IVD solutions, thereby driving the demand for IVD raw materials and contributing to the overall market growth in the region.

Additionally, key strategic actions by companies in both the United States and Canada—such as the launch of innovative products and obtaining product approvals—are expected to further stimulate market expansion. For example, in May 2022, BioMérieux received approval from the Government of Canada for its BioFire Blood Culture Identification 2 (BCID2) panel, designed for the rapid detection of bloodstream infections. This new panel features an expanded range of pathogens, a broader set of antimicrobial resistance genes, and updated targets, distinguishing it from its predecessor, the original BCID panel.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the IVD Raw Materials market includes Creative Diagnostics, Merck KGaA, Abbott Laboratories, Bio-Rad Laboratories, Inc., Siemens Healthineers, Roche Diagnostics, F. Hoffmann-La Roche AG, Becton, Dickinson and Company (BD), Lonza Group, Agilent Technologies, Waters Corporation, Heraeus Holding GmbH, LGC Limited, and Other key players.

Creative Diagnostics is a leading supplier of high-quality raw materials for the In Vitro Diagnostics (IVD) industry. They specialize in a broad range of products, including antibodies, antigens, enzymes, proteins, and reagents, which are essential components in diagnostic assays and testing kits. Creative Diagnostics serves a diverse customer base, including diagnostic laboratories, pharmaceutical companies, and research institutions. Merck KGaA, Darmstadt, Germany, known in North America as EMD Millipore, is a global leader in the IVD raw materials market.

The company offers a wide range of products critical for IVD applications, including antibodies, enzymes, proteins, biological buffers, and reagents. The MilliporeSigma brand is particularly known for providing high-quality reagents for clinical diagnostics, offering solutions for molecular diagnostics, immunochemistry, and clinical chemistry.

Top Key Players

- Creative Diagnostics

- Merck KGaA

- Abbott Laboratories

- Bio-Rad Laboratories, Inc.

- Siemens Healthineers

- Roche Diagnostics

- Hoffmann-La Roche AG

- Becton, Dickinson and Company (BD)

- Lonza Group

- Agilent Technologies

- Waters Corporation

- Heraeus Holding GmbH

- LGC Limited

- Other key players

Recent Developments

- In December 2023, Sysmex Corporation announced that, after their initial launch in Japan and the United States, its blood testing reagents for identifying Amyloid Beta (Aβ) accumulation in the brain—believed to be a primary contributor to Alzheimer’s disease—will be available in Europe starting January 2024. These reagents, the HISCL β-Amyloid 1-42 and 1-40 assay kits (“the assay kits”), received CE-IVD marking on May 17, 2022.

- In June 2022, Agilent Technologies Inc. announced that its previously CE-IVD marked instruments, kits, and reagents were reclassified as IVDR Class A on May 26, 2022, in accordance with the new EU IVDR regulation. The launch of these IVDR-compliant Class A products guarantees that laboratories in the EU using Agilent’s IVDR instruments, kits, and reagents in their diagnostic workflows will be able to continue utilizing these products without any disruption.

- In October 2020, Biocare Medical, LLC announced the launch of three innovative IVD IHC antibody markers, designed to advance clinical diagnostics and research applications. The new markers—SMAD4 [EP618Y], BAP1, and BCA-225 [Cu-18]—are expected to support pathologists in making critical prognostic and diagnostic decisions, potentially influencing patient outcomes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 18.65 billion |

| Forecast Revenue (2034) | US$ 38.44 billion |

| CAGR (2025-2034) | 7.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Antibodies, Antigens, Enzymes, Proteins, Biological Buffers, and Others), Technology (Molecular Diagnostics, Clinical Chemistry, Immunochemistry, and Others), End-user (Pharmaceutical and Biotechnology Companies, Diagnostic Laboratories, Contract Research Organizations, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Creative Diagnostics, Merck KGaA, Abbott Laboratories, Bio-Rad Laboratories, Inc., Siemens Healthineers, Roche Diagnostics, F. Hoffmann-La Roche AG, Becton, Dickinson and Company (BD), Lonza Group, Agilent Technologies, Waters Corporation, Heraeus Holding GmbH, LGC Limited, and Other key players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |