Global Integration Platform as a Service Market Size, Share, Growth Analysis By Component (Software/Solutions, Services), By Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Service Type (Data Integration and Migration, API Integration and Management, Application Integration, Cloud Integration, B2B and Event-Driven Integration, Others), By End-User Industry (Banking, Financial Services, and Insurance, IT and Telecommunications, Retail and E-commerce, Healthcare and Life Sciences, Government and Public Sector, Manufacturing, Consumer Goods and Retail, Education, Media and Entertainment, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2035

- Published date: Feb 2026

- Report ID: 179322

- Number of Pages: 335

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Effective Takeaways

- Future Predictions

- Market Growth

- By Component

- By Deployment Mode

- By Organization Size

- By Service Type

- By End-User Industry

- Key Market Segments

- Regional Analysis

- US Market Size

- Driving Factors

- Restraint factors

- Growth Opportunities

- Trending factors

- Competitive Analysis

- Recent Developments

- Report Scope

Report Overview

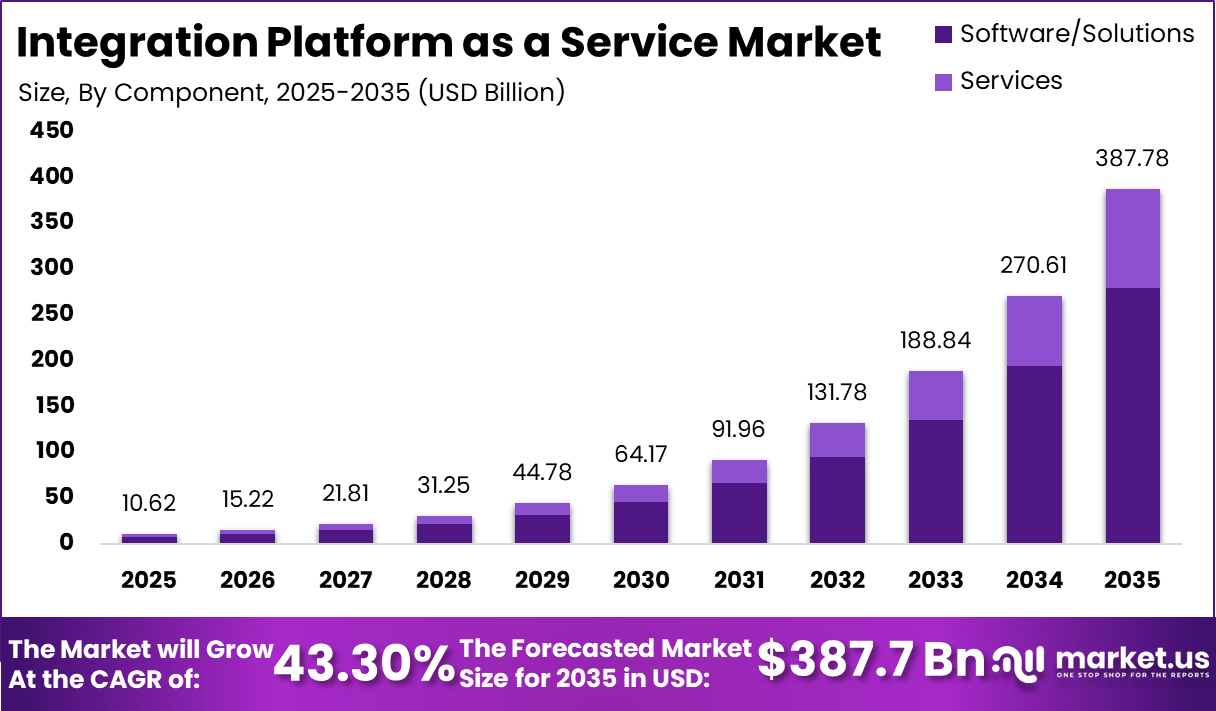

The Integration Platform as a Service (iPaaS) market presents a compelling growth opportunity for businesses seeking to leverage seamless cloud integration and digital transformation. With a projected market value of USD 387.7 billion by 2035 from USD 10.62 billion in 2025, growing at an exceptional CAGR of 43.3%, the iPaaS landscape is expanding rapidly across industries. Investing in insights from this report allows organizations to identify high-potential regions, understand adoption drivers, and optimize technology strategies to stay ahead of competitors in an increasingly connected digital ecosystem.

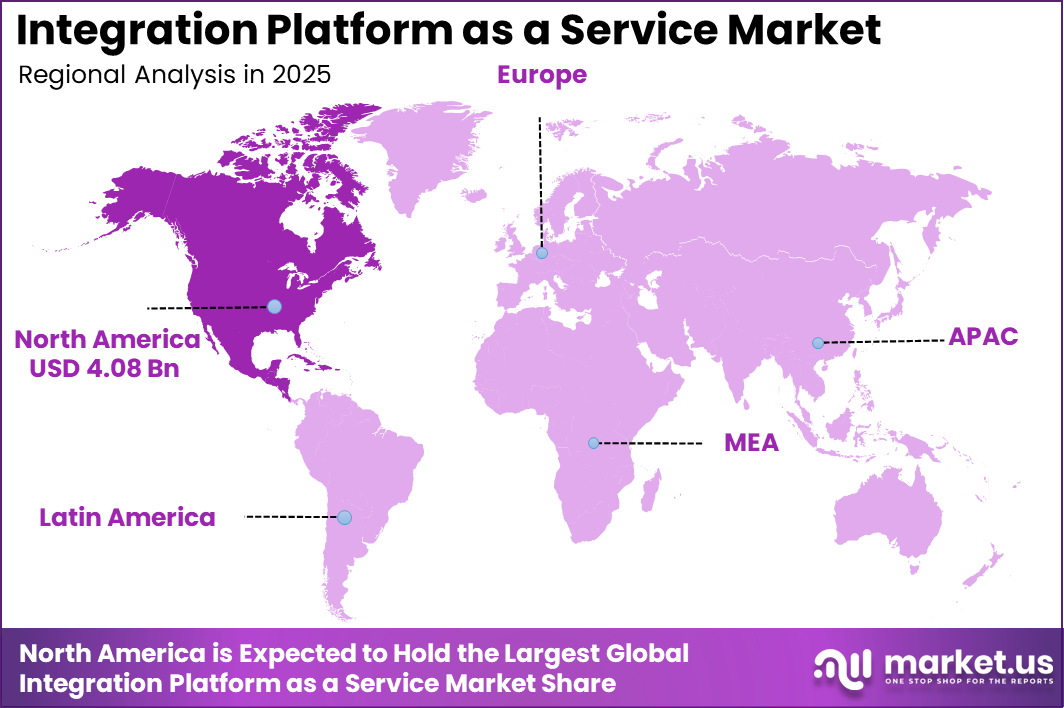

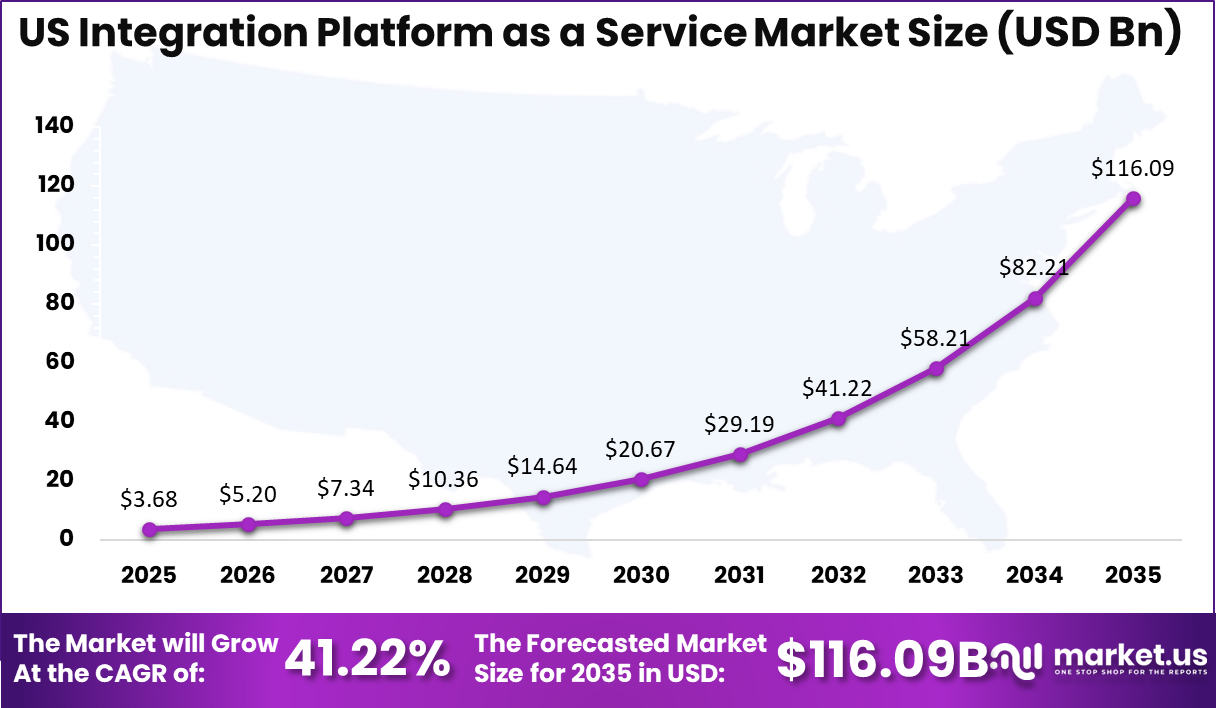

North America holds a dominant 38.5% share of the market, with a 2025 size of USD 4.08 billion, and the US alone accounts for USD 3.68 billion. The US market is expected to continue a robust growth trajectory, driven by enterprises prioritizing hybrid cloud strategies, API management, and real-time data integration, at a CAGR of 41.2%. These trends underscore the urgency for businesses to capitalize on integration solutions that enhance operational efficiency and accelerate innovation.

This report delivers a comprehensive analysis of market size, growth drivers, regional dynamics, and competitive landscape, offering actionable insights for strategic decision-making. Leveraging this research equips your organization with the intelligence needed to identify investment opportunities, forecast market trends, and achieve a competitive advantage in the fast-evolving iPaaS market.

Global cloud adoption rates exceed 85% among enterprises, creating a vast addressable market for integration solutions that connect SaaS, legacy systems, and data sources. Higher cloud usage directly fuels iPaaS demand as businesses seek scalable, real‑time integration strategies. Across enterprise environments, API usage has grown strongly.

API‑first strategies are increasing by 61%, and organizations are managing more than 900 APIs on average, underlining the critical role of API integration in modern digital ecosystems. Hybrid and multi‑cloud strategies are now the norm, with 75% of organizations expected to use hybrid or multi‑cloud architectures by 2026, which drives demand for platforms capable of orchestrating data and workflows across diverse environments.

In digital transformation initiatives, 63% of companies report data integration as critical to business success, reflecting the strategic importance of iPaaS for operational efficiency and analytics. Cloud infrastructure spending reached USD 102.6 billion in Q3 2025, growing over 25% year‑over‑year, highlighting the intense investment environment in which iPaaS solutions operate.

These authentic statistics reinforce the rapid growth of cloud‑integrated technologies, the foundational role of APIs, and enterprise commitment to integrated digital workflows, all directly linked to accelerating iPaaS adoption and market expansion.

Effective Takeaways

- The Integration Platform as a Service market is projected to grow from USD 10.62 Billion in 2025 to USD 387.7 billion by 2035, reflecting a CAGR of 43.30%.

- North America accounts for 38.5% of the market, with a 2025 size of USD 4.08 billion.

- The US contributes USD 3.68 billion in 2025, with a strong growth trajectory at a CAGR of 41.22%.

- By Component, Software/Solutions dominate with 72.0% share, indicating high demand for scalable integration platforms.

- By Deployment Mode, Public Cloud adoption leads at 58.0%, reflecting enterprises’ preference for flexible, cloud-based integration solutions.

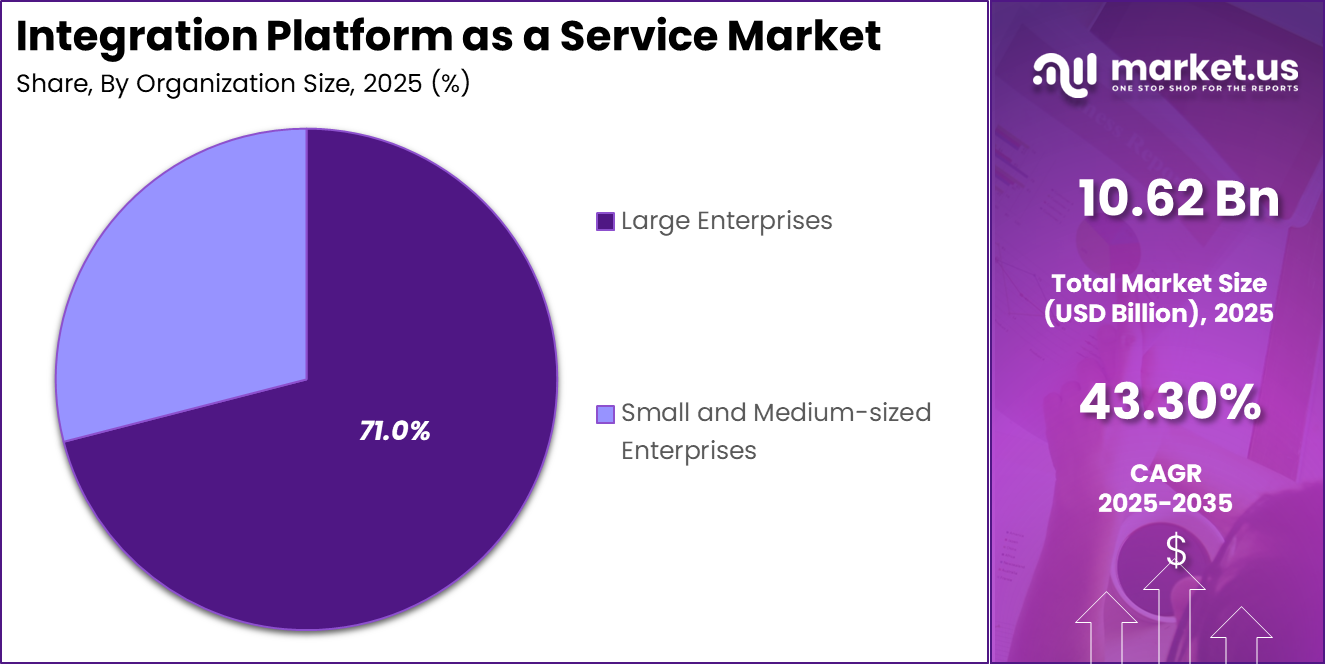

- By Organization Size, Large Enterprises hold 71.0% share, emphasizing that iPaaS adoption is primarily driven by complex, high-volume operations.

- By Service Type, Data Integration and Migration represents 35.0% of the market, showing that managing and transferring enterprise data is a key use case.

- By End-User Industry, Banking, Financial Services, and Insurance lead with 32.0% share, underlining the critical need for secure, efficient, and compliant data integration in highly regulated sectors.

Future Predictions

The future of the iPaaS market is strongly anchored in accelerating cloud adoption, API‑centric connectivity, and digital transformation initiatives across global enterprises. Multiple industry forecasts indicate that the iPaaS market will continue its substantial expansion through 2035, with projections ranging from USD ~292.9 billion to USD ~351.5 billion globally, driven by scalable cloud solutions and real‑time integration demands.

Hybrid and multi‑cloud architectures will become foundational to enterprise IT strategies, with analysts predicting that 75 % of organizations will employ hybrid or multi‑cloud approaches by 2026, fueling demand for flexible, secure integration platforms that connect disparate systems seamlessly. Advancements in embedded intelligence and automation will reshape how iPaaS solutions deliver value.

Investment in AI‑powered integration capabilities is projected to rise sharply, with AI‑enabled data integration reducing manual effort by up to 55 % and improving accuracy by approximately 40 % compared to legacy integration methods.

SME adoption of cloud integration tools is also set to accelerate, reflecting broader cloud infrastructure investment trends, and creating new growth vectors beyond large enterprises. Overall, enterprises seeking to optimize agility, operational efficiency, and real‑time data flows will continue to prioritize iPaaS solutions, making them core components of future digital strategy frameworks.

Market Growth

The Integration Platform as a Service (iPaaS) market is experiencing rapid growth, driven by enterprises’ increasing demand for seamless data connectivity and digital transformation. Adoption of cloud technologies, along with the rise of hybrid and multi-cloud infrastructures, is creating a strong need for platforms that can integrate complex IT environments in real time.

North America remains the leading region, reflecting early adoption of cloud-based solutions and advanced IT infrastructure. Large enterprises are at the forefront of iPaaS implementation, leveraging scalable and secure integration platforms to streamline operations, improve efficiency, and enhance digital workflows. Software and solutions dominate the market as the primary component, while public cloud deployment is preferred for its flexibility and cost-effectiveness.

Services focusing on data integration and migration continue to be critical, helping organizations manage, transfer, and harmonize enterprise data across multiple systems. The Banking, Financial Services, and Insurance sector is a key driver, emphasizing the importance of secure, compliant, and efficient integration solutions. Overall, the market trajectory indicates strong momentum, with increasing adoption across industries positioning iPaaS as a cornerstone of modern enterprise IT strategy and digital transformation initiatives.

By Component

The Software/Solutions segment dominates the Integration Platform as a Service (iPaaS) market, capturing 72.0% of the overall share, reflecting its essential role in enabling seamless connectivity across enterprise systems. This segment provides organizations with tools to integrate applications, manage workflows, and orchestrate data in real time, which is increasingly critical as businesses adopt cloud-based and hybrid IT environments.

Software solutions offer flexibility, scalability, and automation capabilities, allowing enterprises to optimize operations, reduce manual intervention, and accelerate digital transformation initiatives. Enterprises prioritize these solutions to streamline complex processes, ensure data consistency, and enhance collaboration across departments.

Services complement the Software/Solutions segment by providing implementation, customization, and ongoing support, ensuring integration platforms deliver maximum value. These services include system integration, data migration, API management, and technical support, helping organizations overcome deployment and maintenance challenges. Managed services enable enterprises to focus on core operations while ensuring their integration platforms operate efficiently and securely.

The combination of Software/Solutions and Services drives strong market adoption, particularly among large enterprises and industries with complex IT requirements. The 72.0% share of Software/Solutions highlights the continued reliance on integrated software and service offerings as organizations pursue operational efficiency and seamless digital workflows in the rapidly growing iPaaS market.

By Deployment Mode

The Public Cloud deployment mode leads the Integration Platform as a Service (iPaaS) market, capturing 58.0% of the overall share, reflecting enterprises’ preference for flexible, scalable, and cost-effective integration solutions.

Public cloud platforms enable organizations to connect applications, manage workflows, and orchestrate data across multiple systems without the need for extensive on-premises infrastructure. This deployment model supports rapid implementation, automatic updates, and seamless scalability, allowing enterprises to respond quickly to evolving business needs and digital transformation initiatives.

Private Cloud deployment offers organizations enhanced control, security, and compliance, making it a preferred choice for industries with strict regulatory requirements or sensitive data. It allows enterprises to customize integration platforms according to internal policies while maintaining dedicated resources for mission-critical operations.

Hybrid Cloud deployment combines the advantages of both public and private clouds, enabling enterprises to balance cost efficiency with security and control. Organizations leverage hybrid deployments to manage workloads across different environments, ensuring flexibility and optimizing performance for complex IT ecosystems.

By Organization Size

Large Enterprises dominate the Integration Platform as a Service (iPaaS) market, accounting for 71.0% of the overall share, highlighting their significant role in driving adoption. These organizations typically operate complex IT environments with multiple applications, cloud systems, and data sources that require seamless integration.

iPaaS solutions help large enterprises streamline workflows, automate processes, and ensure real-time data connectivity across departments and regions. The scalability, flexibility, and advanced features offered by these platforms make them particularly suitable for organizations with high-volume operations and extensive digital transformation initiatives.

Small and Medium-sized Enterprises (SMEs) are gradually increasing their adoption of iPaaS solutions, driven by the need to optimize operations and remain competitive in a digital-first landscape. While SMEs have comparatively simpler IT environments, integration platforms help them unify applications, improve efficiency, and support business growth without large upfront infrastructure investments.

The dominance of Large Enterprises at 71.0% demonstrates that complex, resource-intensive organizations are the primary drivers of market growth. However, the growing interest from SMEs indicates an expanding market opportunity, as integration solutions become more accessible, cost-effective, and tailored to meet the unique needs of smaller organizations alongside large-scale enterprise deployments.

By Service Type

Data Integration and Migration leads the Integration Platform as a Service (iPaaS) market with a 35.0% share, reflecting its critical importance for organizations managing complex and distributed data environments. This service type enables enterprises to efficiently consolidate, transfer, and harmonize data across applications, cloud platforms, and legacy systems.

It ensures data consistency, accessibility, and accuracy, which are essential for analytics, reporting, and operational decision-making. The growing volume of enterprise data and the shift toward cloud-first strategies have made data integration and migration a primary focus for organizations seeking streamlined workflows and enhanced digital transformation outcomes.

API Integration and Management facilitates connectivity between applications and services, supporting real-time data exchange and automating workflows. Application Integration ensures that enterprise systems, including ERP, CRM, and other core platforms, operate cohesively. Cloud Integration enables seamless interaction between on-premises and cloud environments, while B2B and Event-Driven Integration focus on external partner networks and real-time event processing. Other specialized services address niche integration requirements, supporting industry-specific or highly customized workflows.

The dominance of Data Integration and Migration at 35.0% underscores its role as the foundation for effective iPaaS deployment. Organizations increasingly prioritize this service to unify data, optimize operational efficiency, and enable informed decision-making across diverse enterprise ecosystems.

By End-User Industry

Banking, Financial Services, and Insurance (BFSI) lead the Integration Platform as a Service (iPaaS) market with a 32.0% share, reflecting the sector’s critical need for secure, efficient, and compliant data integration. BFSI organizations manage vast volumes of sensitive data across multiple applications and platforms, making seamless integration essential for real-time transaction processing, regulatory compliance, risk management, and customer experience. The growing adoption of digital banking, mobile payments, and advanced analytics further drives demand for robust iPaaS solutions in this sector.

IT and Telecommunications organizations rely on iPaaS to connect complex networks of software applications, cloud services, and customer management systems. Retail and E-commerce enterprises leverage integration platforms to unify sales, inventory, and customer data, enabling personalized experiences and efficient supply chain operations. Healthcare and Life Sciences prioritize secure integration for electronic health records, clinical systems, and research databases, while Government and Public Sector agencies use iPaaS to streamline services, enhance citizen engagement, and ensure data compliance.

Manufacturing, Consumer Goods, Education, Media and Entertainment, and other sectors are increasingly adopting integration solutions to optimize workflows, automate processes, and enhance operational efficiency. The 32.0% share of BFSI underscores the high dependence on reliable integration platforms, establishing this industry as a primary driver of iPaaS market growth.

Key Market Segments

By Component

- Software/Solutions

- Services

By Deployment Mode

- Public Cloud

- Private Cloud

- Hybrid Cloud

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

By Service Type

- Data Integration and Migration

- API Integration and Management

- Application Integration

- Cloud Integration

- B2B and Event-Driven Integration

- Others

By End-User Industry

- Banking, Financial Services, and Insurance

- IT and Telecommunications

- Retail and E-commerce

- Healthcare and Life Sciences

- Government and Public Sector

- Manufacturing

- Consumer Goods and Retail

- Education

- Media and Entertainment

- Others

Regional Analysis

North America holds a dominant position in the Integration Platform as a Service (iPaaS) market, accounting for 38.5% of the global share, with a market size of USD 4.08 billion in 2025. The region’s strong presence is driven by high cloud adoption rates, advanced IT infrastructure, and a large base of technology-savvy enterprises.

Organizations across industries in North America are increasingly leveraging iPaaS solutions to integrate multiple applications, manage data flows, and streamline complex workflows, supporting both operational efficiency and digital transformation initiatives.

The United States plays a central role in this regional dominance, reflecting early adoption of public and hybrid cloud models and the presence of major technology providers offering scalable integration solutions. Enterprises prioritize iPaaS to ensure seamless connectivity between legacy systems and modern cloud applications, optimize business processes, and enable real-time data-driven decision-making.

Factors such as strong government support for digital infrastructure, significant investment in cloud technologies, and growing emphasis on automation and analytics further reinforce North America’s leadership in the iPaaS market.

Additionally, the presence of large enterprises across sectors like Banking, Financial Services, Insurance, IT, and Telecommunications fuels sustained demand. The region is expected to continue serving as a strategic growth hub, setting trends in adoption, deployment models, and advanced integration technologies that influence global market dynamics.

US Market Size

The US market is a major contributor to the Integration Platform as a Service (iPaaS) sector, with a market size of USD 3.68 billion in 2025. The country is projected to reach USD 116.09 billion by 2035, growing at a robust CAGR of 41.22%. This rapid growth reflects the strong demand for seamless integration solutions across enterprise IT environments, driven by digital transformation initiatives, cloud adoption, and the need for real-time data connectivity.

Large enterprises in the US are the primary adopters of iPaaS solutions, leveraging these platforms to connect legacy systems with modern cloud applications, automate workflows, and optimize operations. Key industries such as Banking, Financial Services, Insurance, IT, and Telecommunications are leading adoption due to their reliance on secure, compliant, and efficient integration tools. Public cloud deployment and software/solutions components remain preferred, emphasizing scalability, flexibility, and cost-effectiveness.

The growth trajectory is also supported by increasing enterprise investment in API management, data integration, and workflow orchestration solutions, enabling faster decision-making and improved operational efficiency. With continued innovation in cloud and integration technologies, the US market is expected to remain a central hub for iPaaS adoption, setting global standards for integration practices and enterprise connectivity solutions.

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driving Factors

The growth of the Integration Platform as a Service (iPaaS) market is primarily driven by the increasing adoption of cloud technologies and digital transformation initiatives across industries. Enterprises are prioritizing seamless connectivity between applications, legacy systems, and cloud platforms to ensure real-time data access and operational efficiency.

The rise of hybrid and multi-cloud environments further fuels demand, as organizations require flexible platforms that can orchestrate workflows across diverse infrastructures. Additionally, the growing emphasis on automation, API management, and analytics encourages the adoption of iPaaS solutions, enabling businesses to reduce manual intervention, streamline processes, and accelerate decision-making.

Regulatory compliance and data security requirements also push enterprises toward integrated solutions that can standardize and secure data across systems. Large-scale enterprises and industries such as Banking, Financial Services, Insurance, IT, and Telecommunications are leading the adoption, highlighting the critical role of iPaaS in enhancing scalability, performance, and business agility.

Restraint factors

The iPaaS market faces certain challenges that may constrain growth. High implementation costs, particularly for large-scale enterprise deployments, can deter smaller organizations from adopting comprehensive integration solutions. Complexity in integrating legacy systems with modern cloud applications often requires specialized skills, creating dependence on external service providers and increasing operational overhead.

Security and data privacy concerns, especially in highly regulated industries, pose additional challenges, as organizations must ensure that sensitive information remains protected during integration processes. Integration platform downtime or system failures can disrupt critical business operations, affecting trust in iPaaS solutions.

Furthermore, the lack of standardized protocols and varying integration requirements across organizations can complicate deployment. Limited awareness among small and medium-sized enterprises about the benefits of iPaaS also slows adoption in this segment. These factors highlight the need for cost-effective, user-friendly, and secure integration solutions to overcome existing market barriers.

Growth Opportunities

The iPaaS market presents significant growth opportunities as enterprises increasingly adopt cloud-first strategies and digital workflows. Rising demand for hybrid and multi-cloud environments enables vendors to offer advanced integration solutions tailored to diverse IT infrastructures.

AI-powered and automated integration capabilities are emerging as key growth drivers, helping organizations reduce manual intervention, improve accuracy, and accelerate data-driven decision-making. Expansion into small and medium-sized enterprises represents another opportunity, as affordable, scalable platforms allow these businesses to adopt advanced integration tools previously reserved for large enterprises.

Industry-specific solutions, particularly for Banking, Financial Services, Insurance, Healthcare, and Retail, can address unique compliance, workflow, and data requirements, further expanding market potential. Geographic expansion in emerging regions with growing cloud adoption also offers substantial prospects. Vendors that provide comprehensive services, including implementation, migration, and support, are well-positioned to capitalize on these opportunities and drive sustained market growth.

Trending factors

Several trends are shaping the current iPaaS landscape. Public cloud deployment remains the most preferred model, reflecting enterprise preference for scalability, flexibility, and cost efficiency. Software/Solutions continue to dominate as the leading component, with platforms increasingly incorporating AI and machine learning to automate data integration and workflow orchestration.

API-first strategies are becoming standard, enabling real-time connectivity across applications and services. The rise of industry-specific solutions, particularly for BFSI, Healthcare, and IT sectors, highlights the focus on tailored integration offerings. Hybrid cloud adoption is gaining momentum, allowing organizations to balance security and performance with cost efficiency.

Additionally, services such as data migration, API management, and application integration are trending as enterprises seek end-to-end support for complex IT ecosystems. These factors collectively indicate that iPaaS adoption is evolving toward intelligent, automated, and industry-aligned solutions.

Competitive Analysis

The Integration Platform as a Service (iPaaS) market is highly competitive, driven by the presence of established global technology providers and emerging specialized vendors. Key players focus on enhancing platform capabilities through advanced features such as AI-powered automation, API management, cloud orchestration, and real-time data integration.

Companies are also investing in research and development to provide scalable, flexible, and secure solutions tailored to diverse enterprise requirements across industries such as Banking, Financial Services, Insurance, IT, and Telecommunications. Strategic initiatives such as mergers, acquisitions, and partnerships are common, enabling vendors to expand their geographic presence, strengthen service offerings, and accelerate technology adoption.

Product innovation remains a major differentiator, with providers integrating analytics, machine learning, and workflow automation to deliver enhanced operational efficiency and improve user experience. Additionally, companies are focusing on offering end-to-end services, including implementation, customization, and support, to help enterprises optimize platform performance and reduce integration complexity.

The competitive landscape is also shaped by the growing adoption of public and hybrid cloud deployments, prompting vendors to offer flexible pricing models, subscription-based services, and industry-specific solutions. Overall, the iPaaS market is characterized by continuous innovation, aggressive expansion strategies, and customer-centric solutions, positioning leading providers to capture a larger share of the rapidly growing integration market.

Top Key Players in the Market

- Dell Boomi Inc.

- Informatica Inc.

- MuleSoft LLC (Salesforce, Inc.)

- Microsoft Corporation

- International Business Machines Corporation

- Oracle Corporation

- SAP SE

- SnapLogic Inc.

- Workato Inc.

- Jitterbit Inc.

- TIBCO Software Inc.

- Celigo Inc.

- Zapier Inc.

- Software AG

- Amazon Web Services, Inc.

- Others

Recent Developments

- In 2025, SAP Integration Suite was recognized as a Leader for the fifth consecutive time in the 2025 Gartner Magic Quadrant for iPaaS. The platform introduced AI‑assisted features that automate workflows, detect API anomalies, and enhance data validation across hybrid environments.

- In 2025, SnapLogic launched AI‑enabled connectors for faster real-time data integration. Microsoft added low-code automation tools to its integration offerings, and Dell Boomi expanded cloud connectors to support more SaaS applications, boosting adoption across industries.

- In 2024, Boomi acquired APIIDA AG’s federated API management business, enhancing API security and scalability. The platform also added AI-driven automation and managed file transfer features to support complex, regulation-sensitive integrations.

Report Scope

Report Features Description Market Value (2025) USD 10.62 Billion Forecast Revenue (2035) USD 387.7 Billion CAGR(2025-2035) 43.30% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics, and Emerging Trends Segments Covered By Component (Software/Solutions, Services), By Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Service Type (Data Integration and Migration, API Integration and Management, Application Integration, Cloud Integration, B2B and Event-Driven Integration, Others), By End-User Industry (Banking, Financial Services, and Insurance, IT and Telecommunications, Retail and E-commerce, Healthcare and Life Sciences, Government and Public Sector, Manufacturing, Consumer Goods and Retail, Education, Media and Entertainment, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Dell Boomi Inc., Informatica Inc., MuleSoft LLC (Salesforce, Inc.), Microsoft Corporation, International Business Machines Corporation, Oracle Corporation, SAP SE, SnapLogic Inc., Workato Inc., Jitterbit Inc., TIBCO Software Inc., Celigo Inc., Zapier Inc., Software AG, Amazon Web Services, Inc., Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Integration Platform as a Service MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Integration Platform as a Service MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Dell Boomi Inc.

- Informatica Inc.

- MuleSoft LLC (Salesforce, Inc.)

- Microsoft Corporation

- International Business Machines Corporation

- Oracle Corporation

- SAP SE

- SnapLogic Inc.

- Workato Inc.

- Jitterbit Inc.

- TIBCO Software Inc.

- Celigo Inc.

- Zapier Inc.

- Software AG

- Amazon Web Services, Inc.

- Others

Our Clients

- 179322

- Feb 2026