Quick Navigation

Report Overview

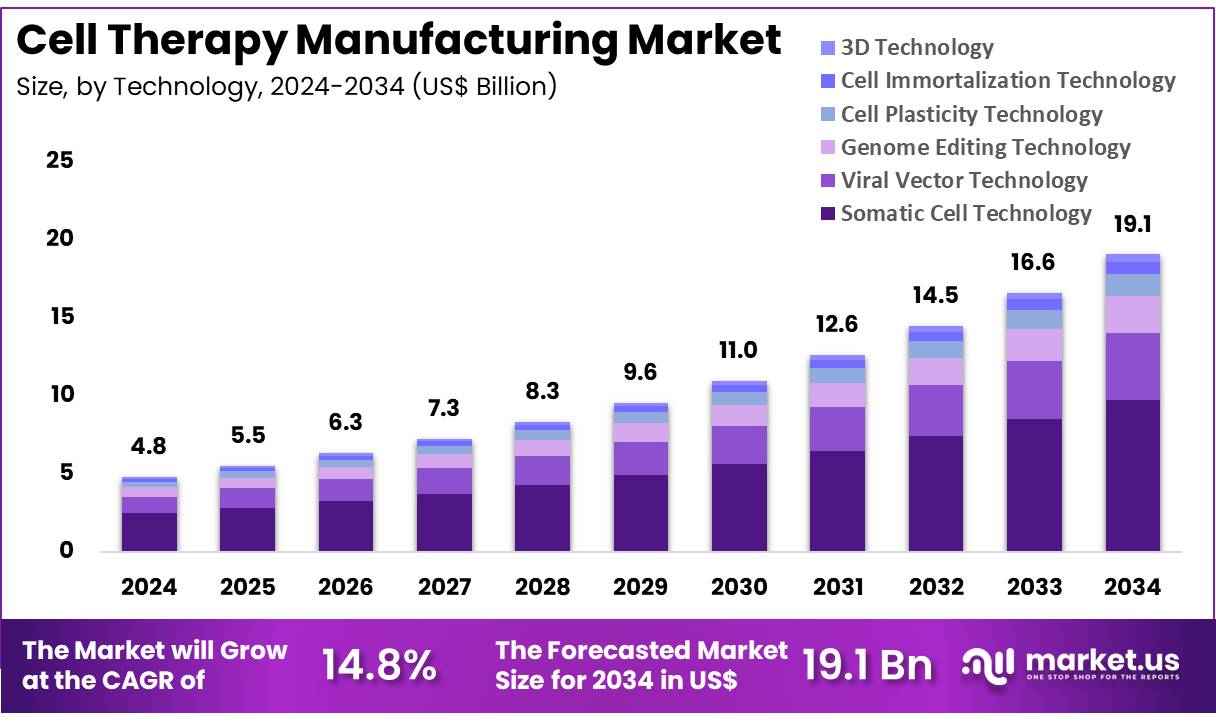

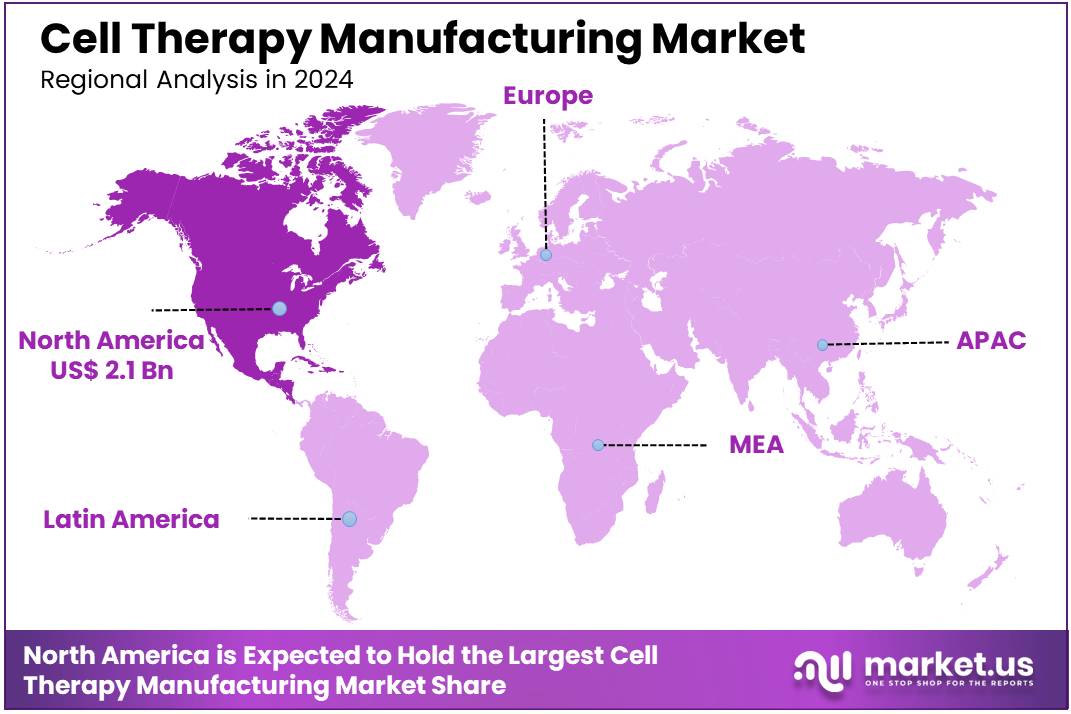

Global Cell Therapy Manufacturing Market size is expected to be worth around US$ 19.1 billion by 2034 from US$ 4.8 billion in 2024, growing at a CAGR of 14.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 42.8% share with a revenue of US$ 2.1 Billion.

Increasing demand for personalized medicine and advancements in regenerative therapies are driving the growth of the cell therapy manufacturing market. As more cell-based treatments, including immunotherapies, stem cell therapies, and gene therapies, gain prominence, the need for scalable, efficient, and cost-effective manufacturing solutions grows. Companies are increasingly focused on improving the quality and consistency of cell products, while also reducing costs to make treatments more accessible.

In March 2024, Cellars unveiled its first Cell Shuttle, an advanced automated platform designed to support the global cell therapy market. This platform operates under cGMP standards and is expected to reduce manufacturing costs and improve process efficiency, ultimately addressing the rising demand for cell-based treatments. The integration of automation and advanced technologies in manufacturing processes accelerates production timelines and enhances the reproducibility of therapies.

Additionally, the increasing regulatory support and advancements in biomanufacturing techniques, such as closed systems and 3D culture models, present significant opportunities for market expansion. The rising focus on personalized treatments and the growing potential of cell therapies for a variety of diseases, including cancer, autoimmune disorders, and genetic conditions, continue to fuel the market’s growth.

Key Takeaways

- In 2024, the market for cell therapy manufacturing generated a revenue of US$ 4.8 billion, with a CAGR of 14.8%, and is expected to reach US$ 19.1 billion by the year 2033.

- The therapy type segment is divided into allogenic cell therapy and autologous cell therapy, with autologous cell therapy taking the lead in 2024 with a market share of 58.3%.

- Considering technology, the market is divided into somatic cell technology, viral vector technology, genome editing technology, cell plasticity technology, cell immortalization technology, and 3D technology. Among these, somatic cell technology held a significant share of 51.2%.

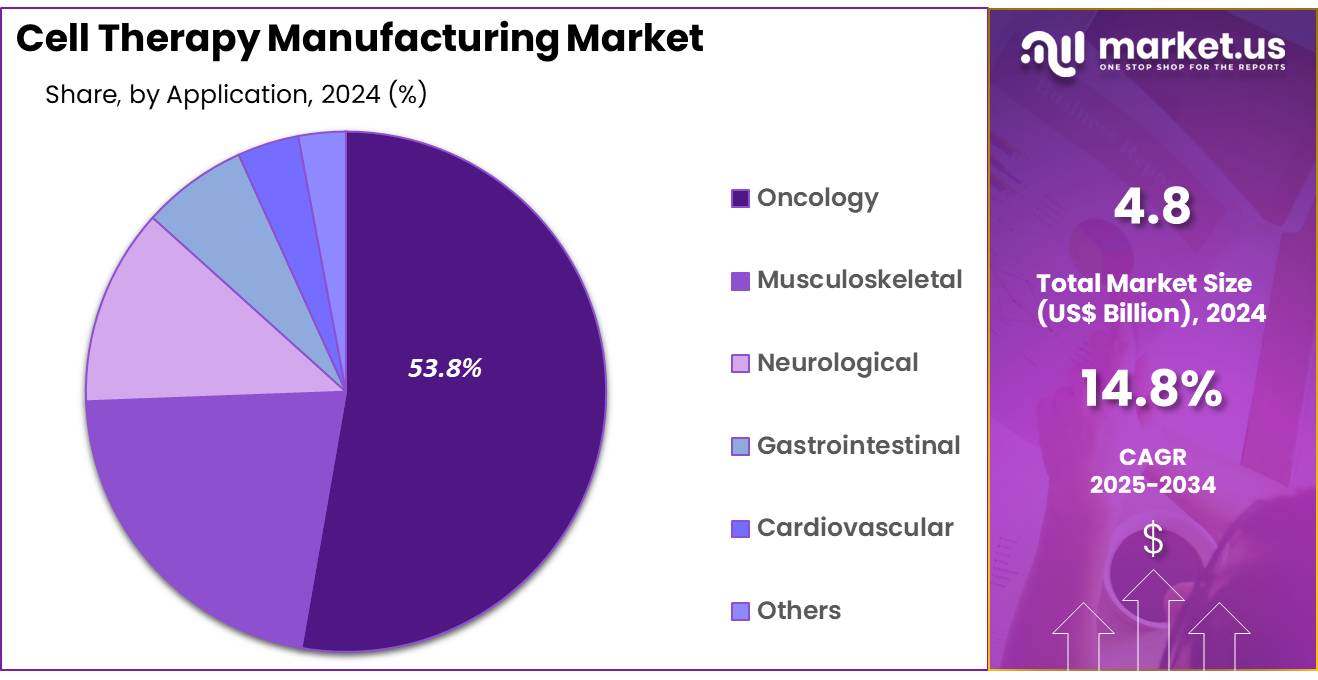

- Furthermore, concerning the application segment, the market is segregated into musculoskeletal, oncology, neurological, gastrointestinal, cardiovascular, and others. The oncology sector stands out as the dominant player, holding the largest revenue share of 53.8% in the cell therapy manufacturing market.

- The source segment is segregated into induced pluripotent stem cell, umbilical cord, neural stem, bone marrow, and adipose tissues, with the induced pluripotent stem cell segment leading the market, holding a revenue share of 54.7%.

- North America led the market by securing a market share of 42.8% in 2024.

Therapy Type Analysis

The autologous cell therapy segment led in 2024, claiming a market share of b owing to the clinical success and regulatory approvals of several autologous CAR T-cell therapies for hematological malignancies. Autologous therapies, derived from the patient’s own cells, eliminate the risk of graft-versus-host disease, contributing to their clinical efficacy.

The increasing number of clinical trials and approvals for autologous cell therapies across various cancer types and other indications is further driving the demand for manufacturing solutions tailored to these personalized treatments. The logistical complexities and costs associated with autologous manufacturing are also significant factors shaping the market landscape within this segment.

Technology Analysis

The somatic cell technology held a significant share of 51.2%. Somatic cell therapies, involving non-germline cells, encompass a wide range of therapeutic approaches, including CAR T-cells, mesenchymal stromal cells, and other adult stem cell-derived therapies.

The established clinical applications and the relatively mature manufacturing processes for many somatic cell therapies have contributed to the dominance of this segment. The ongoing advancements in somatic cell engineering and expansion technologies are further enhancing their therapeutic potential and driving the demand for efficient manufacturing solutions.

Application Analysis

The oncology segment had a tremendous growth rate, with a revenue share of 53.8% owing to the significant clinical success of cell therapies, particularly CAR T-cell therapies, in treating various hematological malignancies, including lymphoma and leukemia.

The high unmet medical need in certain cancer types and the breakthrough therapeutic potential of cell therapies have led to substantial investment and rapid adoption in this application area. The increasing research and development efforts focused on expanding the application of cell therapies to solid tumors are expected to further drive the growth of the oncology segment in cell therapy manufacturing.

Source Analysis

The induced pluripotent stem cell segment grew at a substantial rate, generating a revenue portion of 54.7% and is expected to exhibit substantial growth. iPSCs offer a versatile source of cells for various therapeutic applications, including both autologous and allogeneic therapies.

Their ability to differentiate into a wide range of cell types and their potential for large-scale, standardized manufacturing make them an attractive source for cell therapy development. Ongoing research and advancements in iPSC derivation, differentiation, and genetic engineering are driving increased adoption and investment in manufacturing platforms utilizing iPSCs.

Key Market Segments

Therapy Type

- Allogenic Cell Therapy

- Autologous Cell Therapy

Technology

- Somatic Cell Technology

- Viral Vector Technology

- Genome Editing Technology

- Cell Plasticity Technology

- Cell Immortalization Technology

- 3D Technology

Application

- Musculoskeletal

- Oncology

- Neurological

- Gastrointestinal

- Cardiovascular

- Others

Source

- Induced Pluripotent Stem Cell

- Umbilical Cord

- Neural Stem

- Bone Marrow

- Adipose Tissues

Drivers

Increasing Clinical Success and Regulatory Approvals of Cell Therapies is Driving the Market

The growing number of cell therapies demonstrating significant clinical efficacy and receiving regulatory approvals is a major driver for the Cell Therapy Manufacturing Market. As per recent reports, the number of approved cell and gene therapies has seen a significant uptick, with over 20 approvals granted by the FDA alone since 2017, and a notable portion of these occurring after 2021.

For instance, the FDA approved several new CAR T-cell therapies for various hematological cancers in 2022 and 2023, as detailed on the FDA’s website. This increasing validation of cell therapies is creating strong demand for robust and scalable manufacturing processes to support both clinical trials and commercial supply.

The positive clinical outcomes, such as the high remission rates observed in certain lymphoma patients treated with CAR T-cell therapies (studies published in the New England Journal of Medicine in 2021 and 2022 reported remission rates exceeding 70% in some patient cohorts), are also attracting further investment into the development and manufacturing of these advanced therapies.

Restraints

Complexity of Cell Therapy Manufacturing and Regulatory Hurdles May Restrain Market Growth

The inherent complexity of cell therapy manufacturing processes and the stringent regulatory requirements pose potential restraints on market growth. Cell therapies often involve intricate and sensitive biological materials and processes, requiring specialized expertise and infrastructure.

Navigating the complex regulatory landscape, which can involve over 18-24 months for clinical trial approvals and market authorization (as per industry timelines discussed at regulatory affairs conferences in 2023 and 2024), and ensuring compliance with quality control and safety standards, which can account for up to 30% of manufacturing costs (according to industry cost analyses), can be challenging and time-consuming for cell therapy developers and manufacturers.

Opportunities

Need for Scalable and Cost-Effective Manufacturing Solutions is Creating Growth Opportunity

The critical need for scalable and cost-effective manufacturing solutions is a significant driver for the adoption of advanced manufacturing technologies in the cell therapy market. Traditional manual and open processing methods can cost upwards of US$100,000 per patient dose for autologous CAR T-cell therapies (as per industry reports on cost of goods for cell therapies in 2023), hindering large-scale production and accessibility.

Automated and closed systems have the potential to reduce these costs by an estimated 20-30% and increase throughput by a factor of 5-10 compared to manual methods (according to various presentations at the International Society for Cell & Gene Therapy (ISCT) annual meetings in 2023 and 2024). This potential for cost reduction and scalability is crucial for the widespread clinical use and commercial success of cell therapies.

Impact of Macroeconomic / Geopolitical Factors

The Cell Therapy Manufacturing Market in 2025 is influenced by macroeconomic factors affecting investment in biotechnology and healthcare infrastructure. Global investment in biotechnology research and development remains high, with estimates suggesting over US$400 billion in 2023 (as per recent reports on global biotech investment).

Government initiatives and funding programs supporting regenerative medicine and advanced biomanufacturing, such as the US National Institutes of Health (NIH) allocating over US$6 billion to cell and gene therapy research in fiscal year 2024, and similar initiatives in Europe (e.g., Horizon Europe) and Asia (e.g., Japan’s AMED), are also playing a crucial role in market growth.

However, economic uncertainties and potential recessions could impact investment flows into the biotech sector, which saw a period of adjustment in public market valuations in 2022-2023 (as per recent financial market analyses), potentially affecting the capital available for establishing and expanding cell therapy manufacturing facilities.

Geopolitical factors, including trade policies, intellectual property rights related to cell therapy technologies (with over 20,000 patents filed in cell and gene therapy globally as of 2023, according to recent IP landscape reports), and international collaborations in research and development, can also influence the market. Disruptions in global supply chains for specialized equipment and critical raw materials used in cell therapy manufacturing can lead to increased costs and production delays, with some critical components experiencing lead times of over 6-9 months in recent years (as per recent reports on biomanufacturing supply chains).

The recent US tariff policies implemented in April 2025 could have specific implications for the Cell Therapy Manufacturing Market. The US imports various specialized equipment and consumables used in cell therapy manufacturing. Tariffs on these imports could increase the operational costs for cell therapy manufacturers in the US by an estimated 5-10%, as per recent reports.

Furthermore, retaliatory tariffs from other countries on US-made cell therapy manufacturing technologies or therapies could impact export opportunities, which accounted for approximately US$1.5 billion in 2024 (as per recent trade data on biopharmaceuticals). The long-term effects will depend on the specifics of the tariff policies and the adaptability of the global cell therapy manufacturing supply chain.

Latest Trends

Recent Technological Advancements in Cell Processing and Automation are Driving Adoption

Continuous technological advancements in cell processing, automation, and bioprinting are creating significant growth opportunities in cell therapy manufacturing. Innovations such as closed system processing, which reduced contamination rates in cell culture by over 90% in some studies (as presented at ISCT 2022), advanced cell separation and expansion technologies that can increase cell yields by 2-3 fold (according to technology showcases at industry conferences in 2023).

Gene editing tools like CRISPR-Cas9 that allow for more precise and efficient cell engineering (with over US$5 billion invested in gene editing companies in 2023, as per recent reports), and 3D bioprinting for tissue engineering are improving manufacturing efficiency, reducing contamination risks, and enabling the production of more complex and sophisticated cell-based therapies.

Regional Analysis

North America is leading the Cell Therapy Manufacturing Market

North America dominated the market with the highest revenue share of 42.8% owing to owing to its strong research base in cell therapy, a well-established biopharmaceutical industry, and significant venture capital investments in the sector (with over US$20 billion invested in cell and gene therapy companies in North America between 2021 and 2023, as per recent reports). The US National Institutes of Health (NIH) invested over US$6 billion in cell and gene therapy research in fiscal year 2024, fostering innovation and the development of new therapies requiring advanced manufacturing.

The FDA has approved over 20 cell and gene therapies since 2017, with a significant number of these approvals occurring since 2021, driving the demand for scalable manufacturing solutions. The presence of numerous leading academic institutions and biotech companies at the forefront of cell therapy development further solidifies North America’s leading position in manufacturing.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to increasing healthcare investments, a growing focus on regenerative medicine, and a rising number of cell therapy research initiatives. Countries like China, which increased its R&D spending in the biopharmaceutical sector by over 15% annually between 2021 and 2024 (as per recent national statistics), and Japan, with its strong government support for regenerative medicine (as outlined in Japan’s Agency for Medical Research and Development (AMED) initiatives, which allocated over US$1 billion to regenerative medicine research in 2023), are rapidly expanding their capabilities in cell therapy research and manufacturing.

The number of cell therapy clinical trials in the Asia Pacific region has increased by over 40% since 2021 (as per recent analyses of global clinical trial databases). The large patient pool in the region and the growing adoption of innovative therapies are driving the demand for robust cell therapy manufacturing infrastructure.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the Cell Therapy Manufacturing Market are characterized by their focus on providing comprehensive solutions for cell therapy production, including equipment, consumables, and services. These companies are continuously innovating to develop more efficient, scalable, and cost-effective manufacturing technologies.

Strategic collaborations with cell therapy developers, contract manufacturing organizations (CMOs), and research institutions are crucial for understanding specific manufacturing needs and developing tailored solutions. Expanding their global presence to support the growing cell therapy market worldwide is also a key strategy for market leaders.

Lonza Group AG is a leading global CDMO that provides cell therapy manufacturing services, as well as offering cell therapy manufacturing platforms and technologies. Their expertise in GMP manufacturing and their established infrastructure make them a crucial partner for companies looking to scale up cell therapy production.

Top Key Players

- Thermo Fisher Scientific

- The Discovery Labs

- Ori Bio

- Novartis AG

- Merck KGaA

- Lonza

- Cytiva

- Cell One Partners

Recent Developments

- In March 2023, Cell One Partners partnered with the Center for Breakthrough Medicines (CBM) to accelerate the development and commercialization of cutting-edge cell and gene therapies. The alliance combines both organizations’ strengths to foster innovation in regenerative medicine, driving the next generation of transformative treatments.

- In September 2022, Ori Bio joined forces with the Cell Therapy Manufacturing Center (CTMC) to fast-track the commercialization and clinical integration of cell therapies. This collaboration focuses on optimizing the process of bringing cell-based treatments to market, aiming to improve patient outcomes by shortening development timelines.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 4.8 billion |

| Forecast Revenue (2034) | US$ 19.1 billion |

| CAGR (2025-2034) | 14.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Therapy Type (Allogenic Cell Therapy and Autologous Cell Therapy), By Technology (Somatic Cell Technology, Viral Vector Technology, Genome Editing Technology, Cell Plasticity Technology, Cell Immortalization Technology, and 3D Technology), By Application (Musculoskeletal, Oncology, Neurological, Gastrointestinal, Cardiovascular, and Others), By Source (Induced Pluripotent Stem Cell, Umbilical Cord, Neural Stem, Bone Marrow, and Adipose Tissues) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Thermo Fisher Scientific, The Discovery Labs, Ori Bio, Novartis AG, Merck KGaA, Lonza, Cytiva, and Cell One Partners. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |