Quick Navigation

- Report Overview

- Key Takeaways

- Service Type Segment Analysis

- End-User Segment Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Challenging Factors

- Emerging Trends

- Top Use Cases

- Regional Analysis

- Key Regions and Countries

- Key Players Analysis

- Top Key Players in the Market

- Recent Developments

- Report Scope

Report Overview

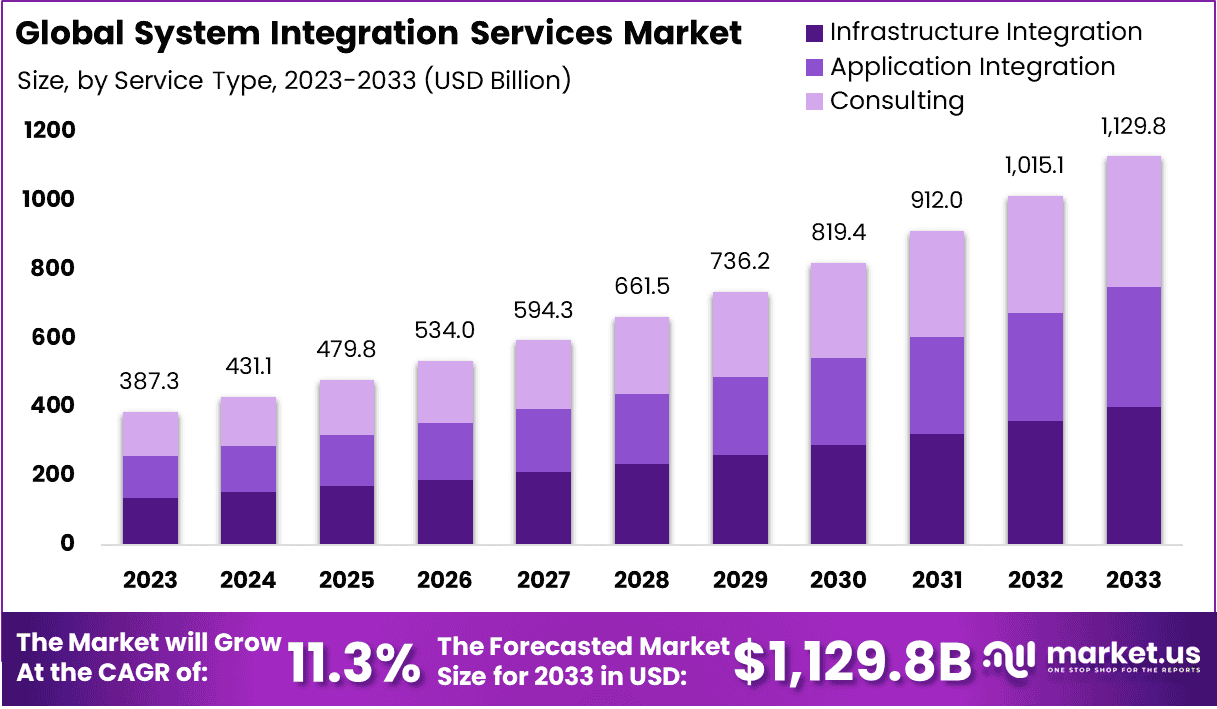

The global system integration services market size is expected to be worth around USD 1,129.8 billion by 2033, from USD 387.3 billion in 2023, growing at a CAGR of 11.3% during the forecast period from 2024 to 2033.

System integration services involve combining different technological components into a cohesive system that functions as intended. This process includes linking various IT systems, services, and software to enable them to work together efficiently. Companies use system integration to ensure that their computing systems and software applications can communicate and operate on a unified platform, which enhances business processes and information flow across the organization.

The market for system integration services is expanding as businesses increasingly rely on complex, interconnected systems that require seamless integration to function effectively. This growth is driven by the need for integrated information analysis, system efficiency, and streamlined operations across various industries. Companies that provide system integration services are crucial in helping businesses modernize their IT infrastructures, implement new technologies, and ensure compatibility across diverse systems.

Rising awareness about the advantages of system integration services is significantly influencing the market. Businesses are becoming more cognizant of the benefits such as increased efficiency, reduced operational costs, and improved information flow across different platforms. This understanding is driving the adoption of integration services, as organizations seek to leverage fully integrated systems to gain a competitive edge. Enhanced system interoperability not only streamlines operations but also supports better decision-making by consolidating data insights from multiple sources.

As digital transformation initiatives increase, the demand for skilled system integrators also rises, indicating a robust market outlook. Several key factors contribute to the growth of the system integration services market. The rapid pace of technological advancements necessitates continual updates and integration of software and hardware systems within organizations.

The increasing emphasis on customer relationship management (CRM) and enterprise resource planning (ERP) systems also drives the need for integration services to provide a unified view of business operations. Furthermore, regulatory compliance across various industries mandates reliable and secure data management practices, which system integration services facilitate.

The demand for system integration services is primarily driven by the growing need for efficient business processes and the integration of new technologies into existing infrastructures. As organizations expand and diversify, the complexity of their IT systems increases, necessitating sophisticated integration solutions to manage data flow and system functionality effectively.

Additionally, the rise in adoption of cloud computing, big data analytics, and IoT (Internet of Things) technologies has further fueled the demand for robust system integration services to ensure these technologies work harmoniously within corporate ecosystems. The system integration services market presents significant opportunities for service providers. There is a continual need for integration capabilities that encompass emerging technologies such as artificial intelligence (AI), machine learning, and blockchain.

The system integration services industry is witnessing a substantial expansion, currently valued at over $500 billion and is projected to reach $1 trillion by 2030. This significant growth trajectory is propelled by an escalating demand for integrated solutions that bolster operational efficiency and enhance data accessibility across diverse organizational landscapes. Specifically, the enterprise integration sector is experiencing a robust annual growth rate of 30 to 40%.

According to data from Partner Fleet, 84% of businesses acknowledge the importance of integrations, classifying them as “very important” or a “key requirement” for ensuring customer satisfaction and retention. This underscores the pivotal role that system integration plays in maintaining competitive edges and fostering customer loyalty. Moreover, 90% of B2B buyers assert that a vendor’s capability to seamlessly integrate with existing technologies is a critical factor influencing their purchasing decisions.

The complexity within the system integration landscape is also intensifying, with 50% of enterprise companies reporting more than 50 integrations. This trend highlights the shift towards more complex integration environments as businesses expand and scale. Furthermore, companies with as few as five integrations demonstrate a willingness to pay 20% more for the same core product, emphasizing the perceived added value of robust integrated solutions.

Key Takeaways

- The global system integration services market size is expected to be worth around USD 1,129.8 billion by 2033, from USD 387.3 billion in 2023, growing at a CAGR of 11.3% during the forecast period from 2024 to 2033.

- In 2023, the infrastructure integration segment held a dominant market position, capturing more than a 35.4% share of the system integration services market.

- In 2023, the BFSI segment held a dominant market position, capturing more than a 54.7% share of the system integration services market.

- In 2023, North America held a dominant market position in the system integration service market, capturing more than a 35.6% share.

Service Type Segment Analysis

In 2023, the Infrastructure Integration segment held a dominant market position, capturing more than a 35.4% share of the system integration services market. This segment includes the integration of core physical and IT infrastructures, such as networking equipment, storage systems, and computing resources.

The prominence of this segment stems primarily from the critical need for robust, scalable, and secure infrastructure that can handle vast amounts of data and support complex applications and systems. As businesses increasingly move towards digitization, the demand for seamless infrastructure integration that supports digital processes and services has become essential.

The leadership of the Infrastructure Integration segment is further reinforced by the rapid expansion of cloud technologies and data centers. Companies are continually upgrading their infrastructure to leverage cloud solutions, requiring sophisticated integration services to ensure these technologies work seamlessly with existing systems. This need for integration has become more acute as organizations adopt multi-cloud environments and hybrid systems that combine on-premises and cloud-based resources.

The ability of infrastructure integration services to provide a smooth transition and operation across these varied environments enhances its importance and contribution to the market’s growth. Additionally, the surge in data-driven decision-making processes has necessitated the integration of advanced infrastructure capable of supporting big data analytics and IoT applications.

This scenario calls for high-performance, highly available, and secure infrastructure, which is only possible through effective integration services. As businesses look to harness the power of data analytics and real-time data processing, the infrastructure integration segment is positioned to remain at the forefront, providing the essential services that enable these technologies to function optimally within the broader IT ecosystem

End-User Segment Analysis

In 2023, the BFSI segment held a dominant market position, capturing more than a 54.7% share of the system integration services market. This leadership is largely attributed to the significant transformation that the banking, financial services, and insurance sectors are undergoing, driven by digital innovation.

Financial institutions are heavily investing in integrating their legacy systems with new digital solutions to improve operational efficiency, enhance security, and meet evolving customer expectations. This need for robust, seamless integration is critical in facilitating real-time banking services, secure transactions, and multi-channel customer support.

Additionally, the BFSI sector faces stringent regulatory requirements that mandate high levels of data protection, financial reporting, and operational resilience. System integration services play a crucial role in ensuring compliance by linking various technologies and platforms to create a unified system that adheres to these regulations.

As the BFSI sector continues to adopt technologies such as cloud computing and big data analytics, the complexity of maintaining compliance increases, further driving the demand for sophisticated system integration services that can adeptly manage these complexities. Moreover, the push towards personalized financial services has necessitated the integration of advanced analytics and customer relationship management (CRM) systems within the BFSI infrastructure.

These integrations help financial institutions leverage customer data to tailor products and services, predict trends, and make informed decisions. The ability of system integration services to enable these functionalities by seamlessly connecting disparate systems and data sources has been pivotal in driving the BFSI segment’s dominance in the system integration services market.

Key Market Segments

By Service Type

- Infrastructure Integration

- Application Integration

- Consulting

By End-User

- IT & Telecom

- Defense & Security

- BFSI

- Oil & Gas

- Healthcare

- Transportation

- Retail

Driving Factors

Increased need for integrating legacy systems with new digital platforms

The increased need for integrating legacy systems with the new digital platform is a significant driver for the system integration services market. Different organizations rely on legacy systems that are crucial for their daily operations. However, these systems often lack compatibility with new or modern digital technologies such as cloud computing, IoT, and big data analytics.

To stay competitive, businesses must be able to adopt these modern technologies, necessitating the integration of their old systems with the new digital platforms. This integration ensures seamless data flow, improved operational efficiency, and enhanced customer experience.

Additionally, it helps organizations leverage existing investments in legacy systems while gaining the benefit of modern technologies. The complexities of this process create a substantial demand for specialized system integration services, driving the market growth as businesses seek expert solutions.

Restraining Factors

Inadequate skilled professional

The shortage of skilled professionals poses a significant restraint on the system integration service market. System integration requires experts in various technologies including legacy systems, cloud computing, IoT, cybersecurity, and data analytics. The rapid evolution of these technologies demands continuous learning and adaptation, making it challenging for professionals to keep up.

This skill gap leads to a limited pool of qualified experts who can handle the complexities of integrating diverse systems. Consequently, service providers face difficulties in delivering high-quality solutions on time, leading to project delays, increased costs, and customer dissatisfaction.

Furthermore, the competition for skilled professionals drives up labor costs, making integration services more expensive and less accessible, especially for small and medium-sized enterprises. The inability to find and retail talents hinders the market’s growth potential, as organizations struggle to implement effective integration strategies without the necessary expertise.

Growth Opportunities

Integration of AI and Automation

Integrating AI and automation presents a significant opportunity for the system integration services market. AI and automation technologies offer substantial benefits, such as enhanced operational efficiency, reduced human error, and improved decision-making capabilities.

As organizations increasingly adopt these technologies to stay competitive, there is a growing need to integrate them seamlessly with existing IT infrastructure. This integration involves connecting AI and automation tools with legacy systems, databases, and other digital platforms to ensure smooth operations and data flow.

Service providers specializing in system integration can capitalize on this trend by offering expertise in blending these advanced technologies into established workflows. By enabling businesses to leverage AI and automation effectively, system integrators can help clients achieve greater productivity, scalability, and innovation.

Challenging Factors

Complexity in integration

The complexities in integration are a crucial challenge for the integration services market. integrating diverse systems, technologies, and applications involves navigating numerous technical, organizational, and operational intricacies. Legacy systems are often incompatible with modern platforms, requiring extensive customization and careful planning to ensure seamless integration.

Additionally, the need to align different data formats, protocols, and security measures further complicates the process. This complexity can lead to prolonged project timelines and increased costs, making it difficult for service providers to deliver efficient and cost-effective solutions.

Misaligned integration efforts can lead to data silos, operational disruptions, and suboptimal performance, impacting overall business productivity. Moreover, managing these intricate integration processes requires highly skilled professionals, who are already in short supply.

Emerging Trends

System integration services are evolving rapidly, propelled by advancements in technology and shifting market needs. Some of the most notable emerging trends include:

- IoT Integration: The Internet of Things (IoT) continues to be a significant driver for system integration, enhancing operational efficiency and enabling new data insights and revenue streams.

- Cloud-Based Solutions: There is an increasing shift towards cloud-based solutions for system integration, which offer enhanced scalability, cost-effectiveness, and flexibility. This trend is largely driven by the need for more agile and adaptable IT infrastructures.

- Enhanced Cybersecurity: As digital systems become more integrated, cybersecurity is becoming a critical component. Businesses are investing in stronger security measures to protect sensitive data and maintain trust.

- AI and Automation: Artificial intelligence and automation are playing crucial roles in optimizing system integration processes, reducing errors, and freeing up human resources for more strategic tasks.

- Sustainability Initiatives: With a growing emphasis on environmental impact, sustainability is becoming a key consideration in system integration projects, influencing how technologies are selected and implemented.

Top Use Cases

System integration finds application across various scenarios, demonstrating its versatility and critical role in modern IT strategies:

- Business Continuity and Disaster Recovery: System integration services are vital in designing and implementing robust business continuity plans (BCP) and disaster recovery processes (DRP), ensuring minimal downtime and sustained productivity.

- Banking and Financial Services: In the banking sector, system integration is crucial for creating efficient, secure, and resilient IT infrastructures that support everything from everyday banking operations to innovative financial services.

- Telecommunications: For telecom companies, system integration helps manage complex IT ecosystems, integrating various hardware and software solutions to improve service delivery and operational efficiency.

- Retail Customer Experience: In retail, integrated systems enable a more personalized customer experience by consolidating data from multiple touchpoints, which helps in understanding customer preferences and enhancing service delivery.

- Healthcare Efficiency: In healthcare, system integration facilitates better data management and interoperability among diverse healthcare systems, improving patient care outcomes and operational efficiencies.

Regional Analysis

In 2023, North America held a dominant market position in the system integration services market, capturing more than a 35.6% share with revenues amounting to USD 137.8 billion. This substantial market share can be attributed to several factors, including the rapid adoption of advanced technologies across various sectors and a robust technological infrastructure.

The region is home to numerous technology giants and innovative startups constantly pushing for digital transformations, thereby driving the demand for system integration services to manage and streamline the new technologies with existing systems.

The leadership of North America in this market is also supported by significant investments in cloud computing, big data, and IoT technologies by enterprises aiming to enhance their operational efficiencies and competitive edge. These technologies require complex system integration to ensure they work seamlessly with legacy systems, pushing companies in the region to adopt these services extensively.

Moreover, the presence of a stringent regulatory environment, particularly in sectors such as healthcare, finance, and government, necessitates reliable system integration to ensure compliance with data protection, privacy laws, and other regulations. Additionally, North America’s market dominance is reinforced by its advanced IT infrastructure, which is capable of supporting large-scale integrations and innovations.

The ongoing trends of remote work, e-commerce, and mobile applications have further amplified the need for scalable and secure system integration solutions that can support an increasingly distributed and mobile workforce. The focus on customer-centric approaches and personalized services in industries like retail and banking also drives the integration of CRM and ERP systems, thereby supporting the market’s growth in this region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Analyzing the key players in the system integration services market including looking at the major companies that tend to provide a comprehensive integration solution, their market strategies, strengths, and recent developments.

Accenture is one of the leading players in the market that focuses on digital transformation, cloud integration, and cybersecurity. It has a global presence with extensive industry expertise and a strong partnership with leading technology providers.

Further, IBM is another key player in the market that emphasizes hybrid cloud integration, AI-driven solutions, and blockchain. It has advanced technological infrastructure, robust research and development, and extensive experience in large-scale integration projects.

Top Key Players in the Market

- Accenture

- NEC Corporation

- Capgemini

- Cisco Systems, Inc.

- Cognizant

- Deloitte Touche Tohmatsu Limited

- HCL Technologies Limited

- IBM Corporation

- Infosys Limited

- Oracle Corporation

- Tata Consultancy Services Limited

- Tech Mahindra Limited

- Wipro

- Other Key Players

Recent Developments

- Acquisition Insights: In November 2023, Accenture strategically expanded its capabilities in data analytics by acquiring ALBERT, a company at the forefront of AI-driven big data solutions. This acquisition is pivotal for Accenture, as it significantly enhances its system integration services, positioning the company to leverage advanced data analytics more effectively across various industries.

- New Product Development: Cognizant introduced innovative cloud-based solutions in the first quarter of 2024, focusing on sectors such as healthcare and finance. These solutions are designed to enhance IT infrastructure integration and automation, underscoring Cognizant’s commitment to improving operational efficiency and client service through cutting-edge technology.

- Acquisition Performance: Capgemini’s acquisition of Quantmetry in 2023 has been instrumental in boosting its performance. Quantmetry, known for its expertise in AI and data science, complements Capgemini’s existing system integration services, enriching its offerings particularly in sectors that demand sophisticated analytics and AI-driven strategies.

- Strategic Expansion: In May 2023, Infosys demonstrated its strategic intent to bolster its European operations by inaugurating new delivery centers in Germany and Ireland. This expansion is aimed at augmenting its onshore capabilities, enhancing service delivery in cloud and AI integration, and meeting the localized demands of European clients more effectively.

- Partnership Development: Cisco, in a significant move in January 2024, entered into a partnership with NetApp. This collaboration is focused on enhancing the FlexPod XCS, a hybrid cloud service that integrates automation and data services. The partnership is particularly tailored to advance system integration solutions across the retail and banking, financial services, and insurance (BFSI) sectors, showcasing a targeted approach to sector-specific challenges.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 387.3 billion |

| Forecast Revenue (2033) | USD 1,129.7 billion |

| CAGR (2024-2033) | 11.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Infrastructure Integration, Application Integration, Consulting) by End-User (IT & Telecom, Defense & Security, BFSI, Oil & Gas, Healthcare, Transportation, Retail, Others) Region |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Accenture; NEC Corporation; Capgemini; Cisco Systems, Inc.; Cognizant; Deloitte Touche Tohmatsu Limited; HCL Technologies Limited; IBM Corporation; Infosys Limited; Oracle Corporation; Tata Consultancy Services Limited; Tech Mahindra Limited; Wipro, Other Key Players. |

| Customization Scope | Customization for segments at the regional/country level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

System integration refers to the process of joining together various IT systems and applications so they function together seamlessly, whether this means connecting new or existing ones or systems from various vendors. System integration has the power to both enhance business efficiency and productivity while improving their customer service levels.

System Integration Services are integral for businesses as they allow for streamlining processes, improved data flow, lower operating costs and an overall increase in productivity. Furthermore, system Integration services promote greater decision-making through providing integrated data insights.

System Integration Services have many applications in various industries, such as healthcare, finance, manufacturing and telecommunications. Any sector which utilizes multiple software applications and hardware systems could gain from them.

System integration presents several challenges, including compatibility issues between various systems, data security concerns, scaling restrictions and needing experienced professionals to oversee and direct the integration process effectively.

The global system integration services market size is expected to be worth around USD 1,129.8 billion by 2033, from USD 387.3 billion in 2023, growing at a CAGR of 11.3% during the forecast period from 2024 to 2033.

The leading players in the System Integration Services Market are as follows:

- Accenture

- NEC Corporation

- Capgemini

- Cisco Systems, Inc.

- Cognizant

- Deloitte Touche Tohmatsu Limited

- HCL Technologies Limited

- IBM Corporation

- Infosys Limited

- Oracle Corporation

- Tata Consultancy Services Limited

- Tech Mahindra Limited

- Wipro

- Other Key Players