Global Induced Pluripotent Stem Cells Market By Derived Cell Type (Fibroblasts, Hepatocytes, Keratinocytes, Amniotic Cells, and Others), By Application (Drug Development, Disease Modeling, Toxicology Research, and Tissue Engineering & Regenerative Medicine (Orthopedics, Oncology, Neurology, Diabetes, Cardiovascular and Myocardial Infarction, and Others)), By End-user (Academic & Research Institutes, Pharmaceutical & Biotechnology Companies, and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: June 2025

- Report ID: 151546

- Number of Pages: 221

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

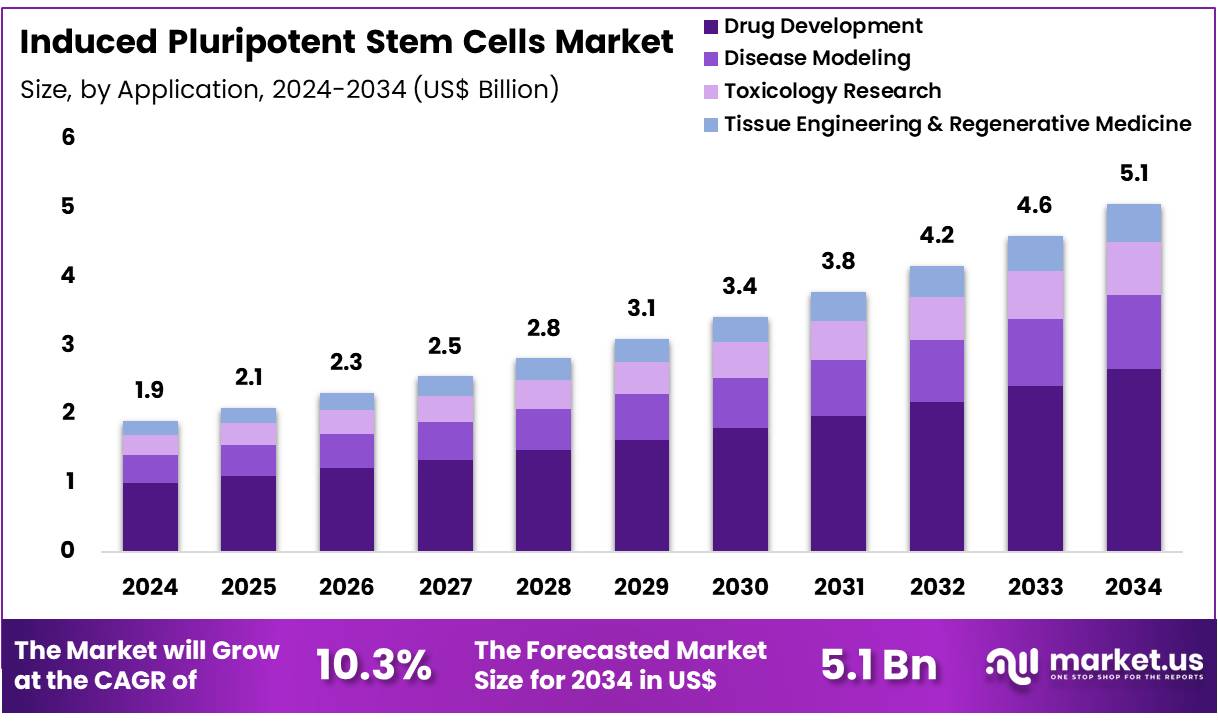

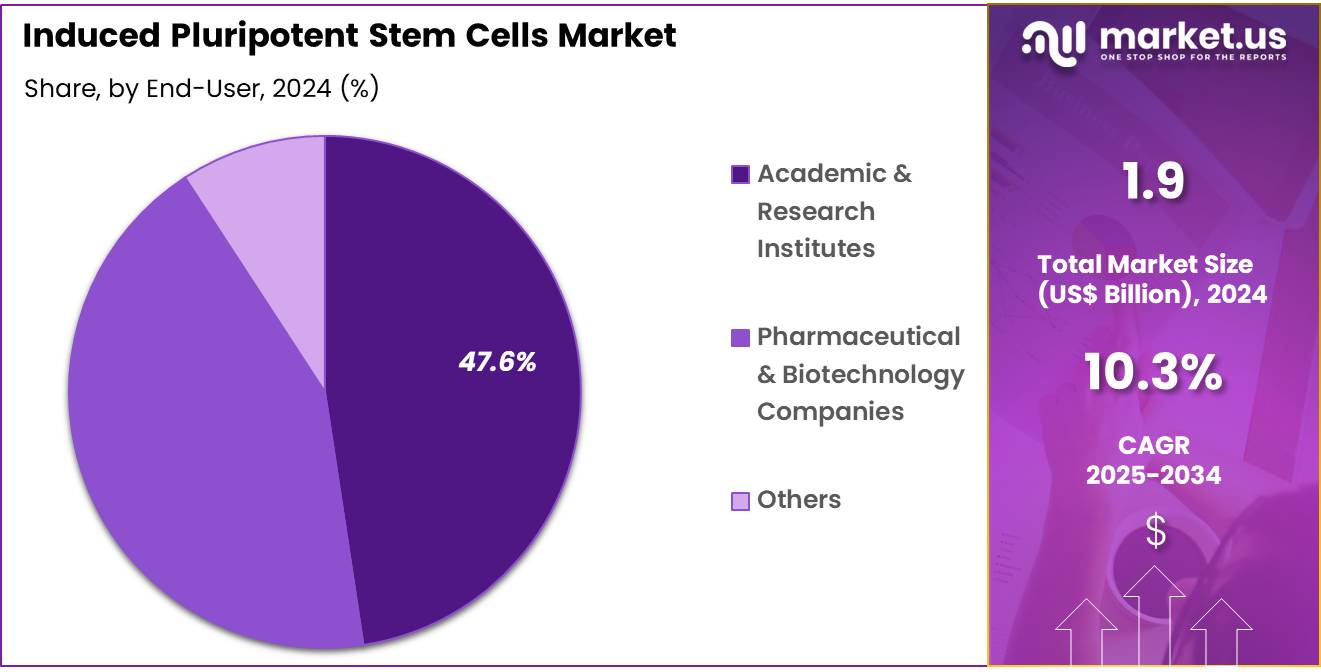

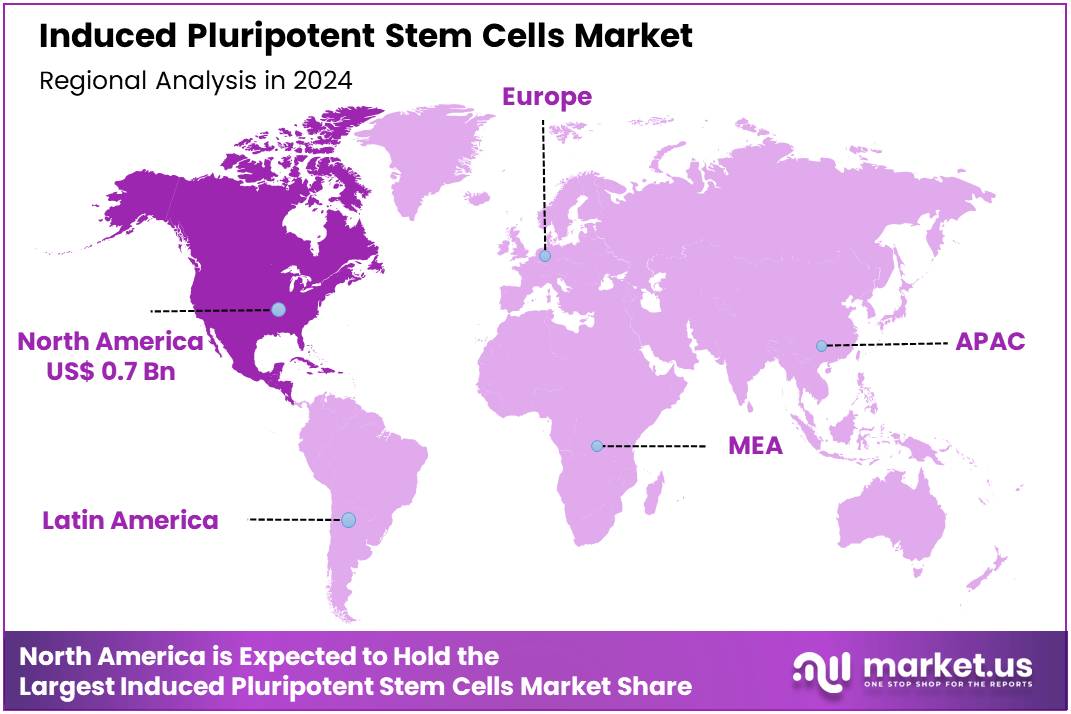

Global Induced Pluripotent Stem Cells Market size is expected to be worth around US$ 5.1 Billion by 2034 from US$ 1.9 Billion in 2024, growing at a CAGR of 10.3% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 37.2% share with a revenue of US$ 0.7 Billion.

Increasing advancements in stem cell research and the rising potential of regenerative medicine are fueling significant growth in the induced pluripotent stem cells (iPSC) market. iPSCs, derived from adult somatic cells and reprogrammed into a pluripotent state, offer immense promise in disease modeling, drug discovery, and personalized medicine. These cells can differentiate into various cell types, making them a powerful tool for treating a range of diseases, including neurodegenerative disorders, heart disease, and diabetes.

The market is benefiting from improvements in iPSC generation techniques and their application in drug testing, allowing for more accurate predictions of drug efficacy and safety. Additionally, iPSCs play a key role in developing cell-based therapies, including tissue regeneration and organ transplantation, offering long-term solutions for patients with chronic conditions. Recent trends highlight the growing focus on scaling up iPSC production for clinical applications, driven by advances in culture systems and bioprocessing technologies.

In January 2024, the Abu Dhabi Stem Cells Centre (ADSCC) and Kyoto University, Japan, joined forces to develop a new therapy for diabetes, utilizing pancreatic beta cells derived from human iPSCs. This collaboration underscores the increasing interest in utilizing iPSCs for therapeutic interventions, particularly in regenerative medicine. As technology advances, the iPSC market presents significant opportunities for breakthroughs in both research and clinical applications, accelerating the development of personalized treatments for a wide range of diseases.

Key Takeaways

- In 2024, the market for induced pluripotent stem cells generated a revenue of US$ 1.9 Billion, with a CAGR of 10.3%, and is expected to reach US$ 5.1 Billion by the year 2034.

- The derived cell type segment is divided into fibroblasts, hepatocytes, keratinocytes, amniotic cells, and others, with fibroblasts taking the lead in 2023 with a market share of 41.2%.

- Considering application, the market is divided into drug development, disease modeling, toxicology research, and tissue engineering & regenerative medicine. Among these, drug development held a significant share of 52.4%.

- Furthermore, concerning the end-user segment, the market is segregated into academic & research institutes, pharmaceutical & biotechnology companies, and others. The academic & research institutes sector stands out as the dominant player, holding the largest revenue share of 47.6% in the induced pluripotent stem cells market.

- North America led the market by securing a market share of 37.2% in 2023.

Derived Cell Type Analysis

Fibroblasts are expected to be the dominant derived cell type in the iPSC market, accounting for 41.2% of the share. Fibroblasts, being one of the most versatile cell types, are widely used in research and drug development. Their ability to generate a variety of cell types through reprogramming makes them a preferred choice for disease modeling and therapeutic development. The growth of this segment is anticipated to be driven by the increasing demand for fibroblast-derived cells in regenerative medicine, where they are used to generate tissues for transplants and wound healing.

Furthermore, fibroblasts are expected to play a crucial role in drug testing, enabling researchers to model diseases and test treatments more effectively. As advances in cell culture techniques improve the efficiency of fibroblast-derived iPSCs, the segment’s growth is likely to continue expanding.

Application Analysis

Drug development is projected to be the largest application segment in the iPSC market, holding 52.4% of the share. iPSCs are anticipated to revolutionize drug development by providing human-based models for drug testing, thereby improving the accuracy and efficiency of preclinical testing. This application is particularly valuable in screening for toxicity, efficacy, and potential side effects in a human context, reducing the need for animal testing. The rising emphasis on personalized medicine, which requires patient-specific models, is likely to drive the demand for iPSCs in drug development.

Additionally, the continuous improvements in the scalability and reliability of iPSC technologies for high-throughput drug screening will likely fuel the expansion of this segment. As pharmaceutical companies seek more effective and safer drug candidates, iPSCs are expected to become an integral tool in the drug development process.

End-User Analysis

Academic and research institutes are projected to remain the dominant end-users of iPSCs, comprising 47.6% of the market share. These institutions are at the forefront of iPSC research, driving innovations in stem cell biology, regenerative medicine, and genetic engineering. Research institutes are expected to continue their pivotal role in advancing iPSC technologies, exploring new applications in disease modeling, regenerative medicine, and drug discovery.

The growing focus on human-based models for studying disease mechanisms and developing novel therapies is likely to fuel the demand for iPSCs in these settings. As governments and private organizations increase funding for stem cell research, academic and research institutes are expected to see continued growth in the use of iPSCs for scientific breakthroughs. The development of new methodologies and discoveries in the stem cell field will contribute to the sustained growth of this segment in the iPSC market.

Key Market Segments

By Derived Cell Type

- Fibroblasts

- Hepatocytes

- Keratinocytes

- Amniotic Cells

- Others

By Application

- Drug Development

- Disease Modeling

- Toxicology Research

- Tissue Engineering & Regenerative Medicine

- Orthopedics

- Oncology

- Neurology

- Diabetes

- Cardiovascular and Myocardial Infarction

- Others

By End-use

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Others

Drivers

Expanding Applications in Drug Discovery and Regenerative Medicine Fueling Growth

The growing adoption of induced pluripotent stem cells (iPSCs) in drug discovery, disease modeling, and regenerative medicine is a major factor propelling the market. iPSCs offer a valuable tool for generating patient-specific cell lines, allowing researchers to better understand disease mechanisms in vitro, screen for new drug candidates with greater precision, and develop personalized therapies.Research organizations, such as the National Institutes of Health (NIH), continue to provide substantial funding for iPSC-based projects. For instance, the NIH RePORTER database reflects numerous active grants involving iPSCs in 2023-2024, underlining their pivotal role in advancing biomedical research. Additionally, iPSCs are being explored for producing various cell types, such as neurons for treating Parkinson’s disease or cardiomyocytes for heart repair, further boosting their demand in regenerative medicine.

Restraints

High Costs and Complexities in Reprogramming and Culturing Cells

The market faces challenges due to the high costs and technical complexities involved in reprogramming, expanding, and maintaining iPSCs. Developing and sustaining high-quality iPSC lines requires specialized knowledge, advanced laboratory equipment, and costly reagents, making the process resource-intensive.A report by the National Academies of Sciences, Engineering, and Medicine in 2024 noted that manufacturing hurdles, particularly the complexities of cell culture, remain substantial barriers within the broader fields of regenerative medicine and cell therapy. Moreover, ensuring the genetic stability and pluripotency of iPSCs across several passages adds further challenges and costs. These factors limit the accessibility of iPSCs for smaller research teams and increase the overall expenses of developing therapeutic applications.

Opportunities

Advancements in Automation and Gene Editing Open New Growth Prospects

Innovations in automation and gene-editing technologies, particularly CRISPR-Cas9, offer significant growth opportunities in the iPSC market. Automation systems, such as robotic cell culture platforms, allow for high-throughput iPSC generation, which reduces manual labor and improves consistency while expanding production capacity.At the same time, gene-editing tools enable the precise correction of genetic mutations in patient-derived iPSCs or the introduction of specific reporters, enhancing their applications for disease modeling and drug discovery. Research published in 2024 in Cell Stem Cell highlights advancements in automated stem cell manufacturing, suggesting these technologies will overcome scalability challenges. These breakthroughs are driving efficiencies, making iPSC research more cost-effective and reproducible, broadening their use in both research and clinical applications.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic factors significantly impact the iPSC market, particularly in relation to global research and development (R&D) funding, venture capital in biotechnology, and government healthcare initiatives. Economic prosperity typically leads to increased investment in advanced biomedical research, including stem cell technologies, fostering innovation and expanding iPSC production capabilities. However, economic downturns and high inflation can reduce research budgets and venture capital funding, potentially slowing the development of iPSC therapies.

According to the National Science Foundation, total US R&D expenditure was projected to reach US$940 billion in 2023, showing a generally positive investment environment despite slower growth. Additionally, geopolitical factors like international collaborations, intellectual property protections, and global supply chain disruptions can also impact iPSC research.

For example, trade tensions can raise costs for critical reagents and equipment, which may affect the efficiency and cost-effectiveness of iPSC-based research. However, the promising potential of iPSCs for disease modeling and regenerative medicine ensures that strategic investments continue, ensuring long-term market growth despite economic and political uncertainties.

The current US tariff policies can directly influence the iPSC market by raising the costs of importing essential reagents, cell culture components, and advanced laboratory equipment. Many critical materials for iPSC research and production are sourced globally, and tariffs could increase the operational expenses for US-based academic and biotech institutions.

According to the US International Trade Commission, the US imported over US$4 billion worth of cell culture media and reagents in 2023, much of which could be subject to new tariffs. These tariffs could drive up costs for iPSC research and therapy development, potentially slowing down progress. On the other hand, tariffs might incentivize the growth of domestic production capabilities for iPSC-related materials, ultimately leading to more resilient and secure supply chains for iPSC research and therapeutic development in the US

Latest Trends

Surge in Investment in Regenerative Medicine and iPSC-Based Startups

A recent trend in the market is the increased investment in regenerative medicine and cell therapy startups that heavily rely on iPSCs. This reflects growing confidence in the potential of iPSCs for therapeutic applications.The Alliance for Regenerative Medicine (ARM) reported that global funding for cell and gene therapy, a field central to iPSC technology, reached US$13.7 billion in 2023, demonstrating continued significant investment. This influx of capital supports the establishment of new iPSC production facilities, accelerates the development of iPSC-derived therapies, and fosters collaborations to bring these treatments to patients, further driving the demand for high-quality iPSC lines.

Regional Analysis

North America is leading the Induced Pluripotent Stem Cells Market

North America holds the dominant share of the induced pluripotent stem cells (iPSC) market, with a revenue share of 37.2%. This leadership position is largely attributed to substantial government support for regenerative medicine and a significant increase in iPSC-based clinical trials. The National Institutes of Health (NIH), a major funding body, allocated approximately US$48.6 billion for biomedical research in 2024, with a dedicated portion directed towards stem cell research and advancements.

This funding underscores the critical role iPSCs play in transforming healthcare through their potential applications in disease modeling, regenerative therapies, and drug development. The increasing number of iPSC-related clinical trials, as demonstrated by data from ClinicalTrials.gov, highlights the rising demand for high-quality iPSCs, making the market a vital component of future therapeutic development.

Furthermore, key industry players, such as Thermo Fisher Scientific, which supply reagents and tools crucial for iPSC research, have witnessed considerable growth. These developments contribute to the rising demand for scalable, reliable production systems in the region, positioning North America as a key player in driving the iPSC market’s growth.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Asia Pacific region is projected to witness the highest compound annual growth rate (CAGR) during the forecast period, driven by increasing governmental investments in regenerative medicine, a growing number of iPSC-related clinical trials, and expanding biopharmaceutical manufacturing capabilities. Governments in countries like Japan, China, and South Korea are prioritizing stem cell research as part of their broader healthcare and biotechnology initiatives.

Japan, for example, has made significant strides in stem cell science through its Agency for Medical Research and Development (AMED), which allocated JPY 211.7 billion (approximately US$1.35 billion) in 2024 for medical R&D, much of which is earmarked for stem cell applications. This funding is fueling advancements in iPSC technology, particularly for the treatment of diseases such as Parkinson’s, Alzheimer’s, and heart disease. The growing number of iPSC-related clinical trials in these countries signals an expanding research pipeline, which is expected to increase the demand for advanced research services and iPSC-derived therapies.

Moreover, China’s significant investments in biopharmaceutical manufacturing have created a favorable environment for iPSC research and application, enhancing the region’s capabilities to generate and scale up iPSC-based treatments. As these countries continue to expand their research infrastructure and push forward the clinical translation of iPSC therapies, the demand for cutting-edge stem cell technology and related services will continue to surge, making Asia Pacific a crucial region for the growth of the iPSC market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the induced pluripotent stem cell (iPSC) market employ several strategies to drive growth. They focus on expanding their product portfolios by developing novel iPSC lines and enhancing differentiation protocols to cater to diverse research and therapeutic needs. Companies invest in automation and high-throughput technologies to improve scalability and reproducibility in cell production processes.

Strategic partnerships with academic institutions and biotechnology firms facilitate innovation and accelerate the translation of iPSC-based therapies into clinical applications. Additionally, players aim to strengthen their market presence by establishing manufacturing facilities and distribution networks in key regions, ensuring timely and efficient delivery of products to support the growing demand for iPSC-based solutions.

FUJIFILM Cellular Dynamics, Inc., headquartered in Madison, Wisconsin, is a prominent player in the iPSC market. The company specializes in developing and manufacturing human iPSC-derived cells for use in drug discovery, toxicology testing, and regenerative medicine. FUJIFILM Cellular Dynamics offers a comprehensive portfolio of products, including iCell and MyCell lines, which are utilized by researchers and pharmaceutical companies worldwide.

The company emphasizes innovation and quality, providing high-quality, reproducible cell models that enable more accurate and efficient drug development processes. Through its integration with FUJIFILM Holdings, the company leverages advanced technologies and global resources to advance the field of iPSC-based applications.

Top Key Players

- Takara Bio, Inc

- STEMCELL Technologies Inc

- REPROCELL Inc

- Fate Therapeutics, Inc

- Evotec SE

- Cynata Therapeutics Limited

- Shinobi

- Axol Bioscience Ltd

Recent Developments

- In April 2024, Shinobi, a manufacturer of iPSC-derived cell therapies, formed a collaboration with Panasonic and Kyoto University, Japan, to create a platform for iPS-T cell therapies. This partnership aims to accelerate the development of innovative therapies using induced pluripotent stem cells (iPSCs) for targeted treatments.

- In October 2023, STEMCELLS Technologies, Inc. opened a new facility in Ontario, enhancing its presence in the North American market. This expansion is expected to strengthen the company’s capabilities in stem cell research and its ability to meet the growing demand for advanced cell therapies in the region.

Report Scope

Report Features Description Market Value (2024) US$ 1.9 Billion Forecast Revenue (2034) US$ 5.1 Billion CAGR (2025-2034) 10.3% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Derived Cell Type (Fibroblasts, Hepatocytes, Keratinocytes, Amniotic Cells, and Others), By Application (Drug Development, Disease Modeling, Toxicology Research, and Tissue Engineering & Regenerative Medicine (Orthopedics, Oncology, Neurology, Diabetes, Cardiovascular and Myocardial Infarction, and Others)), By End-user (Academic & Research Institutes, Pharmaceutical & Biotechnology Companies, and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Takara Bio, Inc, STEMCELL Technologies Inc, REPROCELL Inc, Fate Therapeutics, Inc, Evotec SE, Cynata Therapeutics Limited, Shinobi, Axol Bioscience Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Induced Pluripotent Stem Cells MarketPublished date: June 2025add_shopping_cartBuy Now get_appDownload Sample

Induced Pluripotent Stem Cells MarketPublished date: June 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Takara Bio, Inc

- STEMCELL Technologies Inc

- REPROCELL Inc

- Fate Therapeutics, Inc

- Evotec SE

- Cynata Therapeutics Limited

- Shinobi

- Axol Bioscience Ltd

Our Clients

- 151546

- June 2025