Quick Navigation

Report Overview

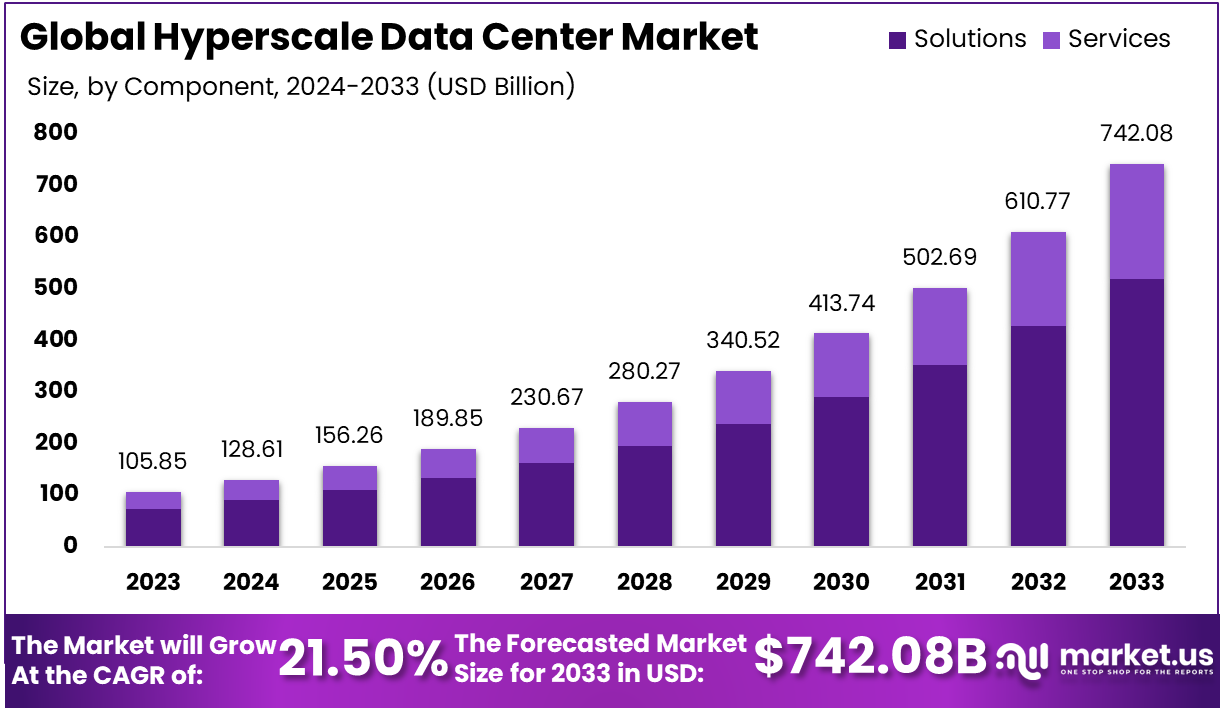

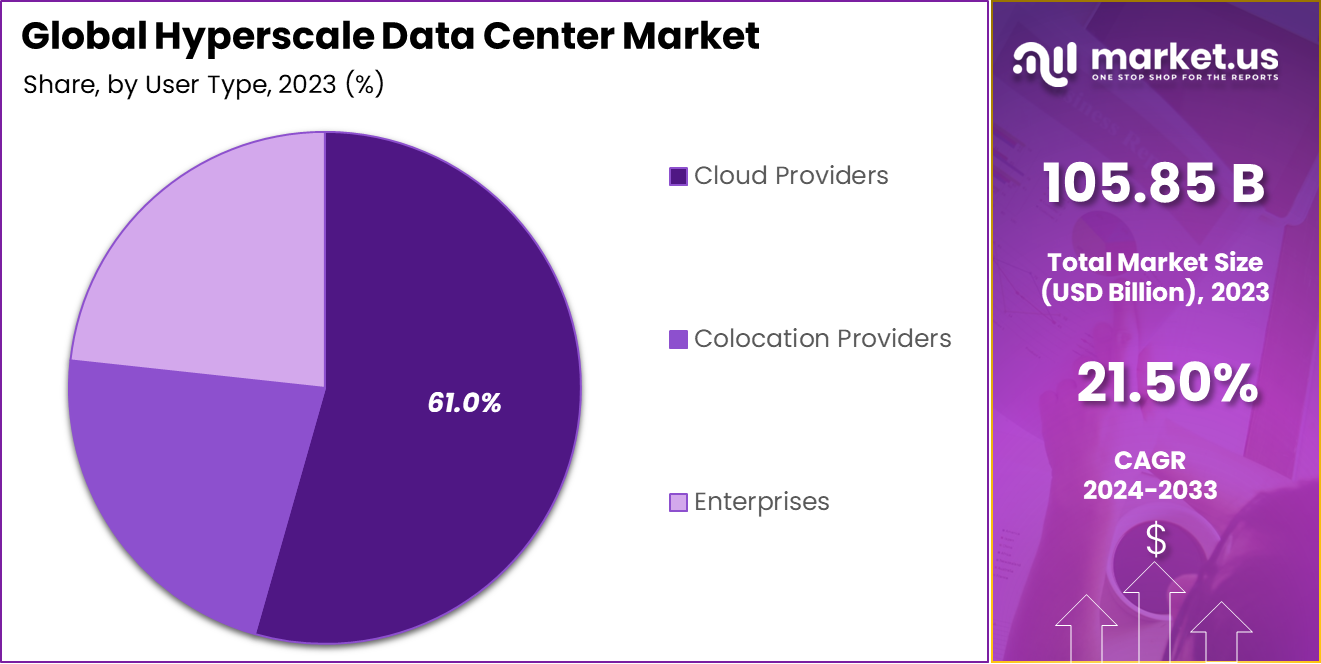

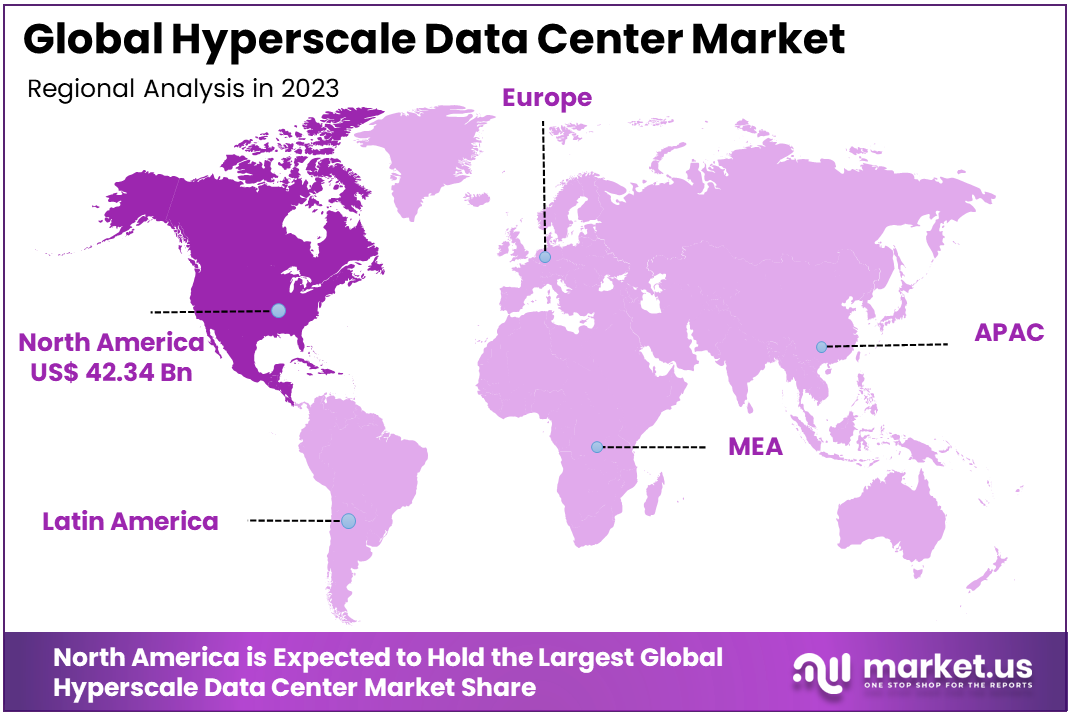

The Global Hyperscale Data Center Market size is expected to be worth around USD 742.08 Billion By 2033, from USD 105.85 Billion in 2023, growing at a CAGR of 21.50% during the forecast period from 2024 to 2033. In 2023, North America held a dominant market position, capturing more than a 40% share, holding USD 42.34 Billion in revenue.

A hyperscale data center refers to a large-scale facility designed to accommodate the massive computing and storage needs of companies, particularly those in cloud computing, e-commerce, and tech industries. These data centers are typically built to scale, meaning they can easily expand their capacity to handle increasing data and traffic demands.

Hyperscale data centers are characterized by their ability to support a high number of servers, interconnected systems, and powerful storage solutions. They are engineered for efficiency, reliability, and scalability, allowing businesses to process vast amounts of data quickly and securely. These data centers are often owned by major tech giants like Amazon, Google, and Microsoft, which require enormous amounts of computing power to run their services on a global scale.

The hyperscale data center market has been experiencing rapid growth, driven by the increasing adoption of cloud services, the expansion of internet traffic, and the proliferation of data-intensive applications like AI, big data analytics, and IoT.

With businesses and industries shifting to cloud-based models, hyperscale data centers are becoming the backbone of modern data infrastructure, enabling faster, more efficient processing of vast amounts of data. According to market reports, the hyperscale data center market is projected to grow significantly in the coming years, fueled by continuous advancements in technology and increasing demand for cloud storage and computing services.

The primary driving factors behind the growth of the hyperscale data center market include the explosive rise in data generation, the increasing reliance on cloud computing, and the need for enhanced processing capabilities. As more organizations move to cloud-first strategies, hyperscale data centers are in high demand for their ability to scale and provide reliable services across multiple regions.

Additionally, the ongoing push toward digitization in industries such as healthcare, finance, and retail is further accelerating the market’s growth. The adoption of advanced technologies like 5G, artificial intelligence, and machine learning is also creating a significant need for large, powerful data storage and processing capabilities that hyperscale data centers offer.

Demand for hyperscale data centers is being driven by the increasing number of consumers and businesses that rely on cloud-based services. With the rapid adoption of digital services across industries, the need for vast amounts of data storage and computational power is surging.

Hyperscale data centers offer businesses an efficient, scalable way to manage and process these ever-growing data requirements. Additionally, the trend of digital transformation, including the shift to e-commerce, smart cities, and autonomous vehicles, is further fueling demand for large-scale, high-performance computing infrastructure.

The hyperscale data center market presents several growth opportunities, particularly in emerging markets and industries that are in the early stages of digital transformation. As cloud adoption continues to rise in regions like Asia-Pacific and Latin America, companies investing in hyperscale data centers stand to benefit from this untapped potential.

Moreover, technological innovations such as the integration of renewable energy sources and advanced cooling systems are creating new opportunities for data center operators to reduce costs and enhance environmental sustainability. These advancements not only improve operational efficiency but also align with global trends toward more sustainable and energy-efficient practices in the tech industry.

Technological advancements play a pivotal role in shaping the future of hyperscale data centers. Innovations such as AI-powered data management, edge computing, and 5G connectivity are expected to revolutionize the way data is processed and stored. Hyperscale data centers are increasingly leveraging these technologies to enhance speed, scalability, and reliability.

Furthermore, the adoption of advanced cooling techniques, including liquid cooling and AI-driven thermal management, is addressing the growing concerns around energy efficiency and sustainability in the data center sector. These developments are pushing the boundaries of what hyperscale data centers can achieve, making them a critical component of modern IT infrastructure.

Hyperscale data centers are characterized by their vast size and capacity, designed to support the immense data processing needs of large organizations. As of 2024, there are over 1,000 hyperscale data centers globally, with the United States hosting approximately 51% of this capacity. These facilities typically exceed 10,000 square feet, house more than 5,000 servers, and provide a minimum of 40 megawatts (MW) of IT capacity.

Currently, hyperscale data centers account for about 41% of the total worldwide data center capacity. The average power density in these facilities has risen significantly; for instance, it has increased from 8 kilowatts (kW) per rack to an average of 17 kW, with projections indicating it could reach up to 30 kW by 2027. This increase is largely driven by the growing demand for AI workloads, which require substantial computational power. Training advanced AI models can demand over 80 kW per rack.

The growth trajectory of hyperscale data centers is notable; their total capacity is expected to double approximately every four years. In the next few years, around 120 to 130 new hyperscale data centers are anticipated to come online annually, further expanding their footprint and capabilities to meet rising data demands.

Key Takeaways

- Market Size and Growth: The global hyperscale data center market is valued at USD 105.85 Billion in 2023 and is expected to reach USD 742.08 Billion by 2033, growing at a CAGR of 21.50% during the forecast period.

- Dominant Component: The solutions segment is the dominant market component, accounting for 70% of the market share in 2023. This reflects the increasing demand for integrated hardware and software solutions to optimize the efficiency of hyperscale data centers.

- Leading User Type: Cloud providers represent the largest user group, holding 61% of the market share. This is driven by the continued growth of cloud infrastructure and the need for scalable, high-performance computing environments.

- End-User Industry: The IT & telecom sector is the largest end-user industry, comprising 42% of the total market share. This industry continues to expand its demand for hyperscale data centers due to the surge in internet traffic, cloud applications, and telecommunication services.

- Data Center Size: The large data centers (above 20MW) segment leads the market with a 65% share. These large-scale data centers are ideal for handling the increasing need for capacity and performance in a variety of industries.

- Regional Dominance: North America is the leading region in the hyperscale data center market, accounting for 40% of the total market value in 2023. The region’s strong tech infrastructure, the presence of major cloud providers, and the growing demand for data storage and computing are key factors contributing to this dominance.

By Component

In 2023, the Solutions segment held a dominant market position, capturing more than a 70% share of the global hyperscale data center market. This leadership can be attributed to the increasing demand for integrated systems that include both hardware and software solutions tailored to meet the complex needs of hyperscale environments. As businesses move towards cloud computing and large-scale data management, the need for solutions that can support high-density storage, virtualization, and computing power has surged.

Solutions in hyperscale data centers typically involve server racks, network infrastructure, storage systems, and software management platforms. These solutions are designed to optimize operational efficiency, reduce costs, and ensure scalability to handle ever-growing volumes of data.

In particular, cloud providers, telecom companies, and large enterprises are investing heavily in these integrated solutions to stay competitive in the digital transformation landscape. As the demand for high-performance, low-latency computing and storage grows, hyperscale solutions are becoming the go-to choice for organizations looking to manage their data-intensive workloads.

The shift toward automation and artificial intelligence (AI) in managing large data centers has further boosted the demand for solutions. Modern hyperscale data centers are equipped with advanced software for resource management, monitoring, and predictive analytics, allowing operators to enhance performance while reducing energy consumption. The growing reliance on AI and machine learning (ML) applications, which require massive computational power, is a key driver of this segment’s growth.

By User Type

In 2023, the Cloud Providers segment held a dominant market position, capturing more than a 61% share of the hyperscale data center market. This leadership is driven by the exponential growth in demand for cloud computing services, which require vast amounts of computational power and storage.

As more businesses and consumers migrate to cloud platforms, cloud providers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud are expanding their data center infrastructure to meet this demand.

Cloud providers are heavily investing in hyperscale data centers to ensure they can offer scalable, reliable, and high-performance cloud services. These data centers allow cloud providers to optimize server utilization, lower operational costs, and improve data accessibility across different geographic regions.

The need for on-demand computing resources, as well as cloud-native applications, has accelerated the expansion of these facilities, particularly as more enterprises transition to cloud-based IT models. In addition, the growing trend of multi-cloud and hybrid cloud environments has further cemented the role of cloud providers in the hyperscale data center market.

By leveraging a global network of hyperscale facilities, cloud providers can offer businesses greater flexibility, security, and redundancy in their operations. As industries continue to embrace digital transformation and the Internet of Things (IoT), cloud providers are expected to lead the charge in driving the expansion and innovation of hyperscale data centers.

By End-User Industry

In 2023, the IT & Telecom segment held a dominant market position, capturing more than a 42% share of the hyperscale data center market. This sector’s leadership is primarily attributed to the massive data and computing requirements of the telecommunications and IT industries.

With the rise in data traffic, cloud adoption, and demand for high-speed internet services, IT and telecom companies are significantly expanding their infrastructure to ensure scalability, reliability, and reduced latency for their customers.

Telecommunications companies, in particular, are heavily investing in hyperscale data centers to support the growing demand for 5G networks and the ongoing expansion of broadband services. The increase in mobile data consumption, streaming services, and IoT devices has created a need for more robust data center solutions.

Hyperscale data centers enable telecom providers to meet these demands by offering greater capacity, faster processing, and the ability to scale resources efficiently, making them an essential part of the sector’s digital transformation.

Additionally, the rapid growth of cloud services and enterprise IT systems has further fueled the adoption of hyperscale data centers in the IT and telecom industries. These facilities allow for centralized data management, disaster recovery, and improved security protocols.

As more businesses shift their operations to cloud platforms, telecom companies are focusing on enhancing their data storage and processing capabilities to remain competitive. This reliance on hyperscale data centers is expected to continue growing, driven by the expansion of 5G, cloud computing, and emerging technologies like artificial intelligence (AI) and big data analytics.

By Data Center Size

In 2023, the Large (Above 20MW) segment held a dominant market position, capturing more than a 65% share of the hyperscale data center market. The primary factor driving the growth of large-scale data centers is the increasing demand for massive data storage and processing capacity from cloud service providers, IT companies, and telecom firms.

Large hyperscale data centers are designed to support complex workloads, high data traffic, and rapid scaling, making them ideal for organizations handling large volumes of data in real-time. The rise in cloud computing, artificial intelligence (AI), and machine learning (ML) has further propelled the adoption of large hyperscale data centers.

These technologies require substantial computational power, low-latency networks, and high availability, which only large-scale facilities can effectively support. With the continuous growth of data-driven industries, the demand for large data centers to manage complex operations and provide seamless user experiences is expected to rise exponentially in the coming years. Large hyperscale data centers also offer significant advantages in terms of economies of scale.

They can leverage better energy efficiency, advanced cooling technologies, and automation, enabling cost savings while maintaining optimal performance levels. The need for efficient resource management and reduced operational costs is crucial for companies looking to scale their operations without compromising on quality, which is why large data centers are preferred.

Key Market Segments

By Component

- Solutions

- Services

By User Type

- Cloud Providers

- Colocation Providers

- Enterprises

By End-User Industry

- IT & Telecom

- BFSI

- Government

- Retail

- Healthcare

- Manufacturing

- Others

By Data Center Size

- Small & Medium (Up to 20MW)

- Large (Above 20MW)

Driving Factor

Increasing Demand for Cloud Services

The growing adoption of cloud computing services is one of the key drivers for the hyperscale data center market. As businesses increasingly shift towards cloud infrastructure for data storage, processing, and management, the demand for robust, scalable, and efficient data centers has skyrocketed.

Hyperscale data centers, which are designed to handle large-scale IT operations and vast amounts of data, are central to supporting the expansion of cloud service providers. This trend is being fueled by the rapid digital transformation across various sectors, including healthcare, finance, and retail, which rely heavily on cloud technologies for improved operational efficiency and cost-effectiveness.

Cloud adoption is accelerating as businesses seek more flexible, scalable, and cost-efficient solutions compared to traditional on-premises data management. In particular, the shift towards Software as a Service (SaaS), Infrastructure as a Service (IaaS), and Platform as a Service (PaaS) models is creating the need for hyperscale data centers that can accommodate high-capacity computing and storage demands.

With organizations opting to store and process data off-site, hyperscale data centers offer the necessary infrastructure, performance, and redundancy that ensure high availability and reliability. Additionally, major cloud providers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud continue to expand their hyperscale data center footprints globally to meet the surging demand.

These data centers offer high performance and lower latency, which are critical for supporting mission-critical applications and services. As digital transformation initiatives continue to grow, the adoption of hyperscale data centers will expand, further bolstering their role in the overall cloud ecosystem.

Restraining Factors

High Initial Capital Investment

While hyperscale data centers offer numerous advantages, their establishment requires significant capital investment, which can act as a restraint to market growth. Building and operating large-scale data centers involves substantial upfront costs, including land acquisition, construction, IT equipment, networking infrastructure, cooling systems, and staffing.

Furthermore, the operating expenses of hyperscale data centers, such as power consumption, maintenance, and cybersecurity, are also considerable, making it challenging for smaller organizations or new market entrants to compete.

Hyperscale data centers typically require hundreds of millions of dollars in investment. This level of capital outlay can pose a financial challenge, especially for companies that are not able to generate the necessary funds or secure financing. The cost of acquiring the right real estate in prime locations is another challenge, as the demand for suitable land in major metropolitan areas and tech hubs continues to rise.

In addition, the long-term operational costs associated with maintaining large data centers, such as energy consumption, can also pose a financial strain. Hyperscale data centers consume a massive amount of electricity to power their servers, cooling systems, and other infrastructure.

Although there are ongoing efforts to improve energy efficiency, the high costs of electricity and other resources remain a key concern. Companies must also invest in upgrading technology and infrastructure regularly to stay competitive, which adds to the ongoing expenses.

Growth Opportunities

Growing Demand for Edge Computing

The rise of edge computing presents a significant opportunity for the hyperscale data center market. Edge computing involves processing data closer to where it is generated (at the “edge” of the network), as opposed to sending it to a centralized data center. This trend is being driven by the increasing number of IoT devices, the need for low-latency services, and the exponential growth of data that requires real-time processing.

Edge computing reduces latency and bandwidth issues by enabling real-time data processing at the point of origin, making it ideal for applications such as autonomous vehicles, smart cities, healthcare monitoring, and industrial automation.

As businesses look to deploy edge computing networks to support these applications, hyperscale data centers play a crucial role in supporting the infrastructure for edge data processing and analytics. These data centers will need to develop more distributed architectures and offer regional services to meet the demands of edge computing.

This opportunity for hyperscale data centers arises as industries across various sectors need to move away from centralized data processing models and adopt decentralized, high-performance computing solutions at the network edge.

Many cloud providers are already investing in the expansion of edge data centers to deliver ultra-low latency services and improve the overall user experience. This expansion is expected to create significant growth opportunities for hyperscale data center providers, allowing them to diversify their offerings and enter new markets.

Challenging Factors

Environmental and Regulatory Pressures

One of the major challenges facing the hyperscale data center market is the growing environmental and regulatory pressures related to energy consumption and carbon emissions. As hyperscale data centers consume large amounts of electricity to power their servers, cooling systems, and other infrastructure, the environmental impact of these operations is a significant concern.

Governments and regulatory bodies are increasingly focusing on reducing the carbon footprints of data centers and promoting more sustainable practices across industries. The hyperscale data center industry faces growing pressure to adopt energy-efficient technologies, reduce waste, and comply with stricter environmental regulations.

Data centers must explore renewable energy sources, such as solar and wind power, to meet sustainability goals and comply with environmental standards. However, transitioning to renewable energy requires significant investment in infrastructure, which can be costly and time-consuming.

Moreover, data centers must also comply with local regulations regarding waste management, water usage, and emissions. Different regions may have different environmental regulations, making it challenging for global hyperscale data center operators to maintain consistent compliance across their operations. Regulatory changes can also lead to increased operational costs, which could affect profit margins and overall market growth.

Growth Factors

The hyperscale data center market is experiencing rapid growth, primarily driven by the increasing demand for cloud computing services. Cloud adoption is becoming widespread across various industries, fueling the need for large-scale data storage and computing facilities. As businesses continue their digital transformation journeys, they require infrastructure that can handle large volumes of data and support complex applications.

Hyperscale data centers, with their ability to scale resources quickly and efficiently, are perfectly positioned to meet this demand. Furthermore, the increasing number of internet-connected devices, particularly with the rise of the Internet of Things (IoT), is pushing data processing and storage requirements to new heights, driving the expansion of hyperscale data centers.

Emerging Trends

A key emerging trend in the hyperscale data center market is the growing focus on sustainability and energy efficiency. With the expansion of data centers worldwide, the environmental impact has come under increasing scrutiny.

As a result, companies are investing heavily in green technologies, such as renewable energy sources, energy-efficient cooling systems, and advanced power management techniques. Moreover, the development of edge computing is reshaping the market, as it brings computing closer to end-users, reducing latency and improving data processing speeds.

Business Benefits

Hyperscale data centers offer significant business benefits, especially for cloud service providers and large enterprises. By leveraging these centers, businesses can reduce their capital expenditures, scale operations rapidly, and increase operational efficiency.

The flexibility to scale infrastructure on demand enables organizations to stay competitive in the fast-paced digital economy. Additionally, hyperscale data centers offer improved reliability, high availability, and reduced downtime, which are critical for businesses reliant on continuous data access and real-time processing.

Regional Analysis

In 2023, North America held a dominant market position, capturing more than a 40% share, holding USD 42.34 Billion in revenue. North America continues to lead the hyperscale data center market due to its strong technological infrastructure and a highly developed cloud computing ecosystem.

The region’s dominance can be attributed to the high demand for data storage and processing from major cloud providers, such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud. These companies have been expanding their data center operations rapidly across the U.S. and Canada, capitalizing on the region’s mature IT ecosystem.

Additionally, the growing adoption of cloud-based services by enterprises, including those in sectors such as healthcare, retail, and finance, has further driven the expansion of hyperscale data centers in the region. The U.S. is the largest contributor to the region’s hyperscale data center market, owing to its position as a global technology hub.

The country is home to several of the world’s largest data center operators, and its robust digital infrastructure has enabled businesses to scale their operations efficiently. Moreover, the increasing demand for edge computing, combined with the push toward 5G networks and artificial intelligence (AI) technologies, is fueling the need for advanced data center solutions.

These factors have made North America the most significant market for hyperscale data centers. Another key factor propelling growth in North America is the availability of ample real estate and favorable regulatory conditions for data center construction.

The region benefits from a combination of vast land availability in suburban and rural areas, where large-scale facilities can be built to accommodate growing data traffic and a business-friendly regulatory environment. Additionally, North American data centers are increasingly shifting towards renewable energy sources, addressing sustainability concerns and making the region attractive to environmentally conscious investors.

Overall, North America’s leadership in the hyperscale data center market is supported by its advanced technological infrastructure, significant investment in cloud computing, and the growing need for large-scale data storage and processing capabilities across multiple industries. The region is expected to maintain its dominance over the forecast period, with continued innovation and expansion in the sector.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

Digital Realty Trust, a global leader in data center solutions, has made significant strides in the hyperscale data center market through strategic acquisitions and expansion. The company focuses on enhancing its global footprint by acquiring and developing facilities that cater to the growing demand for cloud, IT, and digital services.

In recent years, Digital Realty has acquired several companies, including the 2021 purchase of “Interxion,” a leader in data center solutions across Europe. This acquisition strengthened its position in the European market and expanded its reach to key cities across the continent.

Google LLC, a major player in the hyperscale data center market, has continuously expanded its data center capacity to support its vast cloud infrastructure and services. Google’s cloud platform, Google Cloud, has been one of the main drivers of its hyperscale data center growth.

Google focuses on sustainability by investing heavily in green energy and innovative cooling techniques, positioning itself as a leader in environmentally friendly data centers. Google also made a strategic move in 2022 by announcing plans to invest USD 9 billion in expanding its data center infrastructure across the U.S.

Equinix, one of the largest global data center providers, has consistently focused on expanding its hyperscale data center offerings to meet the demands of digital transformation. Equinix has expanded its footprint globally through both organic growth and acquisitions, acquiring companies like “TelecityGroup” and “Metronode” to increase its presence in Europe and Australia.

In 2023, Equinix announced new data center expansions in key markets like Dallas and Amsterdam to accommodate the growing demand for digital infrastructure. The company’s strategy also includes launching new products, such as its Equinix Fabric, a software-defined interconnection service, which enables seamless cloud connectivity and global business expansion.

Top Key Players in the Market

- Digital Realty Trust, Inc.

- Google LLC

- Equinix, Inc.

- CyrusOne, Inc.

- NTT Ltd

- Quality Technology Services

- Vantage Data Centers, LLC

- Amazon Web Services, Inc.

- Microsoft Corporation

- Alphabet Inc.

- Meta Platforms Inc.

- IBM Corporation

- Other Key Players

Recent Developments

- In April 2024: Amazon Web Services (AWS) Announced the Launch of New Hyperscale Data Centers in India. In a move to strengthen its presence in the Asia-Pacific region, AWS launched several new hyperscale data centers in India.

- In January 2024: Microsoft’s Azure Data Center Expansion in Europe. Microsoft announced the opening of three new hyperscale data centers in Europe as part of its global expansion strategy for the Azure cloud platform.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 105.85 Bn |

| Forecast Revenue (2033) | USD 742.08 Bn |

| CAGR (2024-2033) | 21.50% |

| Largest Market | North America |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Solutions, Services), By User Type (Cloud Providers, Colocation Providers, Enterprises), By End-User Industry (IT & Telecom, BFSI, Government, Retail, Healthcare, Manufacturing, Others), By Data Center Size (Small & Medium (Up to 20MW), Large (Above 20MW)) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Digital Realty Trust, Inc., Google LLC, Equinix, Inc., CyrusOne, Inc., NTT Ltd, Quality Technology Services, Vantage Data Centers, LLC, Amazon Web Services, Inc., Microsoft Corporation, Alphabet Inc., Meta Platforms Inc., IBM Corporation, Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |