Global Hospital Stretchers Market By Product Type (Wheeled/Trolley Stretchers, Scoop Stretchers, Spine Board Stretchers, Basket Stretchers, Stair/Evacuation Chair Stretchers and Others), By Mobility Type (Motorized and Non-Motorized), By Application (Daycare/Inpatient, Surgery, Emergency/Trauma and Ambulatory/Transport), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179678

- Number of Pages: 283

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

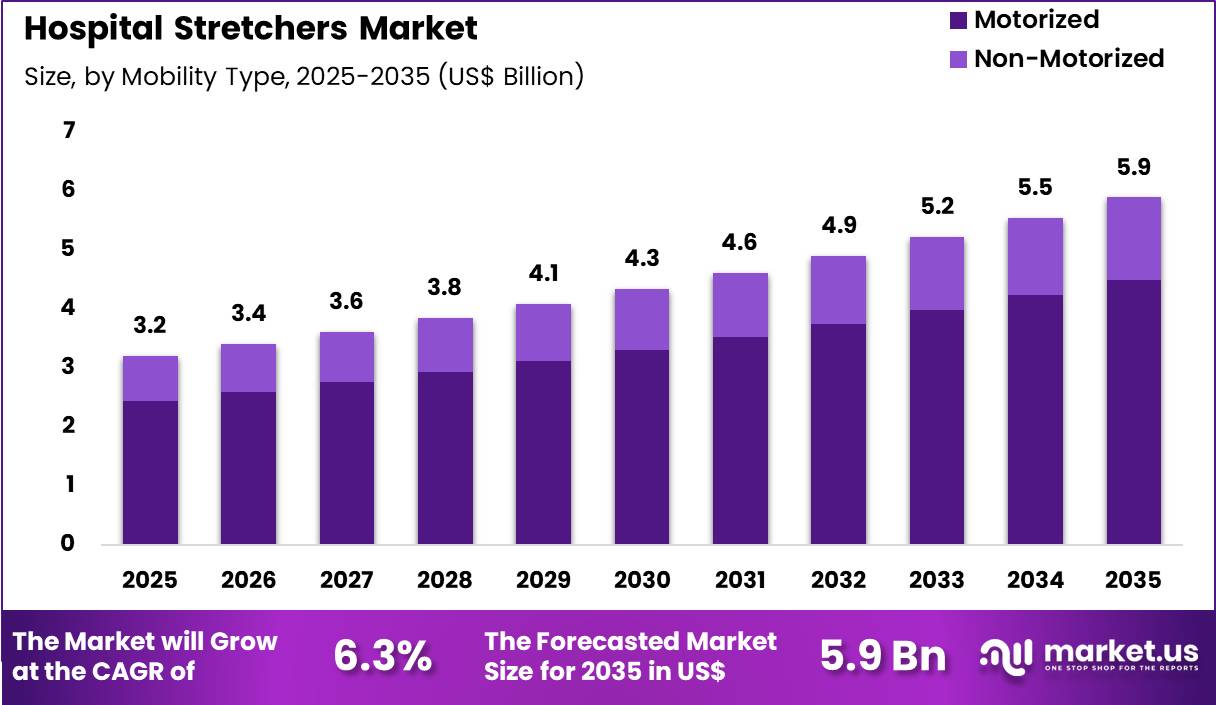

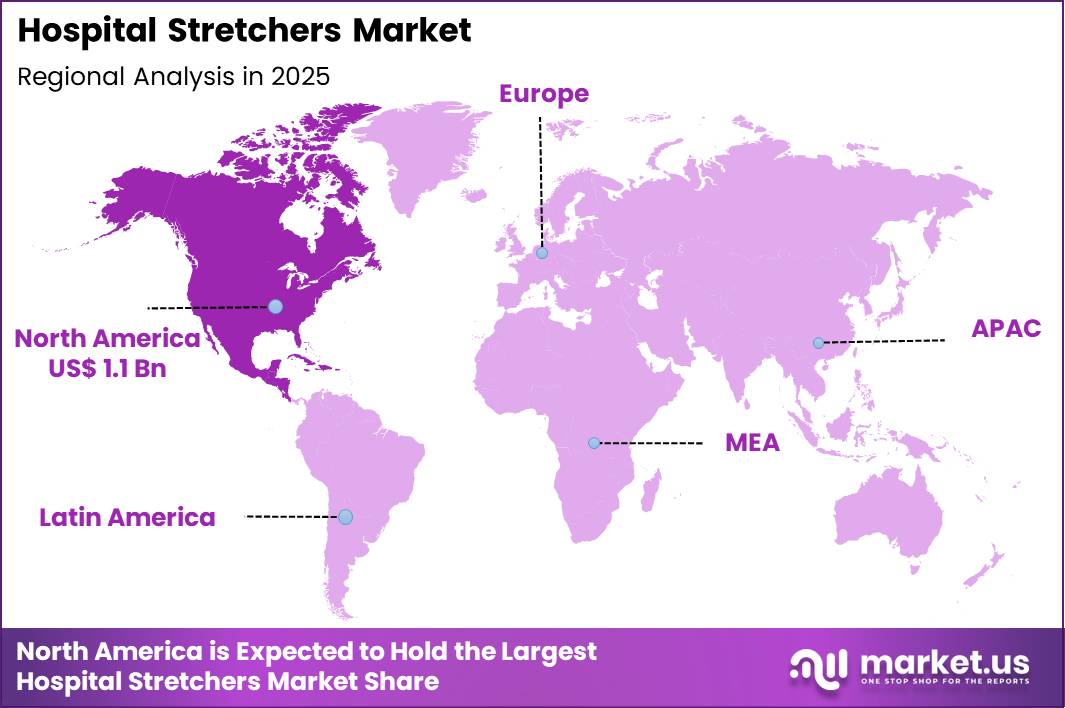

The Global Hospital Stretchers Market size is expected to be worth around US$ 5.9 Billion by 2035 from US$ 3.2 Billion in 2025, growing at a CAGR of 6.3% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 34.4% share with a revenue of US$ 1.1 Billion.

Increasing prevalence of emergency cases, surgical procedures, and chronic illnesses drives the hospital stretchers market as healthcare facilities require versatile, durable transport solutions that ensure patient safety and operational efficiency.

Emergency medical teams increasingly utilize trauma stretchers with spinal immobilization features to stabilize patients with suspected spinal injuries during pre-hospital transfer and emergency department intake. These devices support bariatric applications through reinforced frames and wider surfaces that accommodate higher weight capacities, facilitating secure transport for obese patients in acute care settings.

Operating room staff apply hydraulic stretchers with adjustable height and Trendelenburg positioning to optimize patient transfer and surgical access during orthopedic, cardiovascular, and general procedures. Critical care units deploy ICU stretchers equipped with integrated monitoring mounts and oxygen supply systems, enabling seamless movement of ventilated patients for imaging or interventions without interrupting life support.

Maternity wards use specialized obstetric stretchers with drop-down sides and lithotomy positioning for labor and delivery, enhancing maternal comfort and clinician access during childbirth. Manufacturers pursue opportunities to integrate smart features such as weight scales, pressure-relief mattresses, and battery-powered height adjustment, expanding applications in patient handling for high-acuity areas where frequent repositioning reduces staff injury risk.

Developers advance lightweight, collapsible designs with enhanced braking systems, broadening utility in ambulatory surgery centers and mobile emergency response units. These innovations facilitate modular accessories like IV poles and oxygen tank holders, improving adaptability across specialties.

Opportunities emerge in antimicrobial coatings and easy-clean surfaces that support infection control in post-pandemic environments. Companies invest in ergonomic push handles and side rails that enhance caregiver safety during transport. Recent trends emphasize value-based designs focused on durability, patient comfort, and workflow integration, positioning hospital stretchers as essential infrastructure for efficient, safe patient care delivery.

Key Takeaways

- In 2025, the market generated a revenue of US$ 3.2 Billion, with a CAGR of 6.3%, and is expected to reach US$ 5.9 Billion by the year 2035.

- The product type segment is divided into wheeled/trolley stretchers, scoop stretchers, spine board stretchers, basket stretchers, stair/evacuation chair stretchers and others, with wheeled/trolley stretchers taking the lead with a market share of 39.9%.

- Considering mobility type, the market is divided into motorized and non-motorized. Among these, motorized held a significant share of 76.3%.

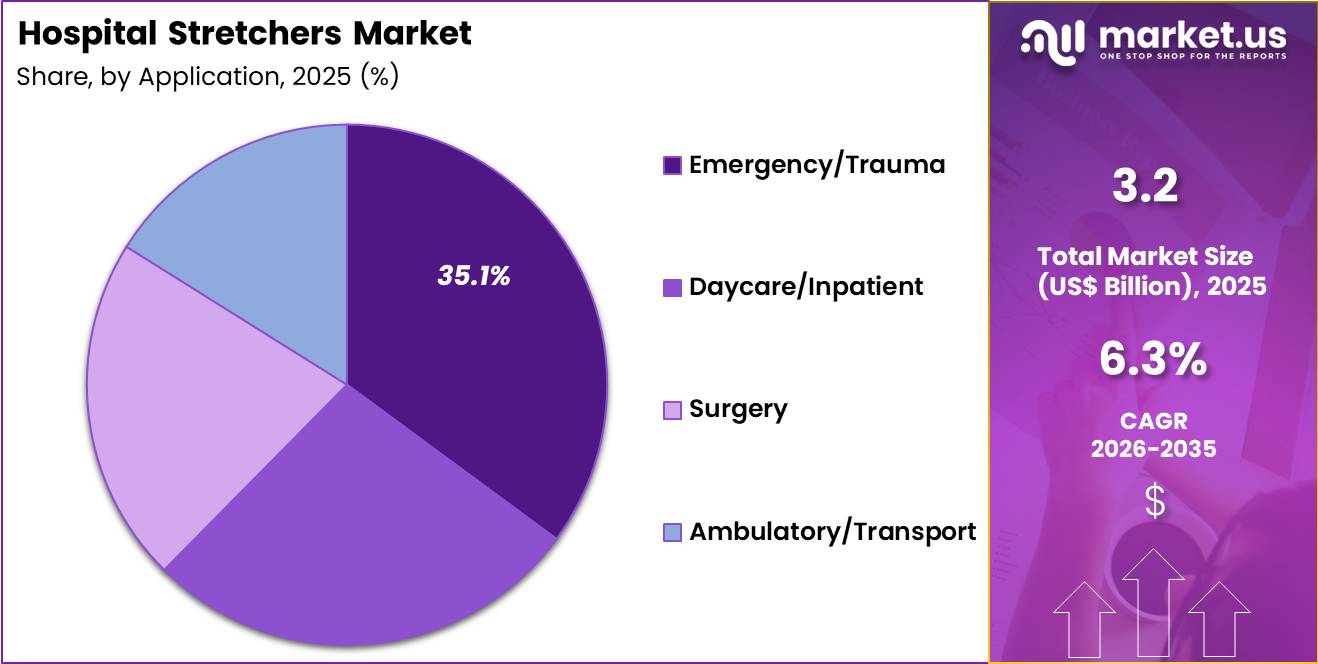

- Furthermore, concerning the application segment, the market is segregated into daycare/inpatient, surgery, emergency/trauma and ambulatory/transport. The emergency/trauma sector stands out as the dominant player, holding the largest revenue share of 35.1% in the market.

- North America led the market by securing a market share of 34.4%.

Product Type Analysis

Wheeled/trolley stretchers accounted for 39.9% of growth within product type and dominate the hospital stretchers market due to their versatility, ease of maneuverability, and suitability for high-volume patient movement.

Hospitals prioritize these stretchers for rapid transportation across departments and in emergency scenarios. The segment growth is projected to strengthen as ergonomic designs, improved load-bearing capacity, and enhanced safety features gain adoption. Rising patient influx and increasing hospital bed capacities drive higher demand.

Hospitals increasingly implement motorized and adjustable trolley stretchers to reduce staff fatigue. Integration of monitoring systems and foldable designs supports both surgical and emergency applications. Growing investments in healthcare infrastructure and trauma care facilities further fuel adoption.

Mobility Type Analysis

Motorized stretchers accounted for 76.3% of growth within mobility type and remain dominant due to automation, speed, and reduced physical effort for healthcare staff. Segment growth is anticipated to continue as hospitals and emergency centers adopt electric and battery-powered models for patient transfers.

Motorized stretchers ensure stable movement, improve safety in high-traffic environments, and reduce patient discomfort. Adoption increases in large hospitals and trauma centers managing critical cases. Technological advancements, including height adjustability, battery longevity, and remote control features, support expansion. Hospital administration prioritizes these stretchers for efficiency and compliance with ergonomic standards, reinforcing segment growth.

Application Analysis

Emergency/trauma accounted for 35.1% of growth within applications and dominates due to the critical need for rapid patient transfer in acute care scenarios. Hospitals and trauma centers rely on stretchers designed for quick access, stability, and adaptability in emergency departments.

Segment growth is projected to strengthen as the prevalence of accidents, cardiac events, and trauma cases increases globally. Emergency-ready stretchers with motorized functions and modular accessories enhance response time.

The segment benefits from growing investments in emergency care infrastructure and training for rapid patient handling. Adoption rises as hospitals implement standardized trauma protocols and advanced life support measures.

Key Market Segments

By Product Type

- Wheeled/Trolley Stretchers

- Scoop Stretchers

- Spine Board Stretchers

- Basket Stretchers

- Stair/Evacuation Chair Stretchers

- Others

By Mobility Type

- Motorized

- Non-Motorized

By Application

- Daycare/Inpatient

- Surgery

- Emergency/Trauma

- Ambulatory/Transport

Drivers

Increasing number of hospital admissions is driving the market.

The steady rise in hospital admissions worldwide has significantly increased the demand for hospital stretchers to facilitate patient transport, emergency care, and intra-facility movement. Greater access to healthcare services and population growth have contributed to higher patient volumes in both public and private hospitals.

Emergency departments require reliable stretchers for rapid triage and stabilization of critical cases. The correlation between hospital bed occupancy rates and the need for efficient patient handling equipment further amplifies procurement requirements. Government health reports document consistent increases in inpatient admissions, particularly for acute and chronic conditions.

Hospital stretchers with adjustable height and mobility features support safer transfers and reduced staff injury risks. National healthcare statistics highlight the growing strain on hospital resources, prompting investments in durable transport solutions.

Key manufacturers are scaling production of bariatric and specialty stretchers to meet this demand. This driver supports long-term expansion in both acute care and long-term facility settings. U.S. hospital admissions totaled approximately 34.7 million in 2023 according to the American Hospital Association.

Restraints

High cost of advanced hospital stretchers is restraining the market.

The substantial pricing of motorized and bariatric hospital stretchers restricts their adoption in facilities operating under tight capital budgets. Complex engineering for electric controls, X-ray compatibility, and high weight capacities contributes to elevated manufacturing expenses. Smaller hospitals and rural facilities often continue using manual or basic stretchers due to financial limitations.

Regulatory requirements for safety certification add further costs to procurement and maintenance. In public health systems, funding priorities favor essential medical supplies over premium transport equipment. Providers must balance patient safety features against economic feasibility when planning purchases. This restraint particularly affects replacement cycles in resource-limited settings.

Industry efforts to offer modular or refurbished options provide partial mitigation. Despite superior functionality, cost barriers slow the transition to advanced stretcher models. The high cost of advanced hospital stretchers remains a primary market restraint.

Opportunities

Expansion of emergency medical services infrastructure is creating growth opportunities.

The ongoing development of emergency medical services in urban and rural areas presents avenues for hospital stretchers to be deployed in ambulances, trauma centers, and field hospitals. Governmental investments in pre-hospital care support the procurement of specialized stretchers for emergency transport.

Increasing focus on rapid response capabilities amplifies demand for lightweight, foldable, and high-capacity models. Partnerships between EMS providers and stretcher manufacturers facilitate customized designs for ambulance integration.

The large volume of emergency transports in populated regions magnifies potential for durable, crash-tested stretchers. Training programs for paramedics promote standardized use of advanced transport equipment. This opportunity allows manufacturers to diversify beyond hospital placements into pre-hospital applications.

Leading companies are developing telescoping and pneumatic systems optimized for emergency use. Overall, EMS expansion aligns with efforts to improve trauma outcomes and reduce mortality. The number of emergency department visits in the United States reached 143 million in 2023 according to the Centers for Disease Control and Prevention.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic trends directly impact the hospital stretchers market through factors such as hospital budgets, investment in healthcare infrastructure, and workforce capacity. Rising inflation and higher interest rates drive up production and procurement costs, which can delay decisions to acquire new stretchers.

Geopolitical uncertainties disrupt the supply of critical metals, electronics, and hydraulic components, creating risks for manufacturing schedules. Current US tariffs on imported hospital equipment increase acquisition costs and extend approval timelines, particularly affecting smaller or financially constrained facilities.

On the upside, these tariffs encourage domestic assembly, local sourcing, and regional collaborations, enhancing supply chain resilience. Meanwhile, increasing hospital admissions and a growing focus on patient mobility maintain market demand. Continued innovation in ergonomic designs, operational efficiency, and maintenance support positions the market for sustained long-term growth.

Latest Trends

Introduction of electric-powered hospital stretchers is a recent trend in the market.

In 2024, manufacturers introduced electric-powered hospital stretchers with integrated battery systems to reduce physical strain on healthcare staff during patient transport. These stretchers feature powered height adjustment and drive systems for easier navigation in crowded corridors. Clinical evaluations in 2024 confirmed reduced musculoskeletal injuries among nursing and transport staff.

The trend emphasizes ergonomic design and battery life for extended use in large facilities. Stryker launched an updated electric-powered Prime Big Wheel stretcher series in 2024 with enhanced battery performance. This development addresses longstanding challenges in manual stretcher handling.

Regulatory clearances in 2024 for these powered models have accelerated clinical integration. Industry collaborations optimize control interfaces for intuitive operation. These innovations aim to improve staff safety while maintaining patient comfort during transfers. The introduction of electric-powered hospital stretchers represents a key trend in patient transport equipment.

Regional Analysis

North America is leading the Hospital Stretchers Market

North America accounted for 34.4% of the hospital stretchers market in 2024, underpinned by continued high demand for urgent and inpatient care equipment as emergency departments and acute care units handled record patient volumes.

In the United States alone there were approximately 155.4 million emergency department visits in 2023, a level that sustained intense utilization of patient transport infrastructure throughout 2024 and highlighted gaps in capacity that healthcare facilities sought to address through stretcher upgrades and additions.

Hospitals invested in adjustable, bariatric, and multi‑function stretchers to improve patient handling across triage, surgery prep, and transport corridors, reducing injuries to both patients and staff. Aging population trends elevated the number of complex admissions, prompting facilities to modernize equipment to support longer hospital stays and specialized care.

Healthcare networks allocated a larger share of capital expenditure toward upgrading emergency response assets, including ergonomically advanced stretchers that integrate with monitoring systems. Outpatient surgical centers and urgent care facilities expanded services, increasing purchases of compact, mobile stretcher models.

Training programs for clinical technicians emphasized safe patient movement, further reinforcing procurement decisions. Reimbursement frameworks in the U.S. and Canada supported acquisition of durable medical equipment, easing budget pressures on hospitals. Partnerships with major medical equipment providers facilitated rapid deployment of new stretcher models across facilities, strengthening response capacity during peak care periods.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Healthcare delivery in Asia Pacific is projected to expand markedly during the forecast period as governments and private providers accelerate hospital infrastructure development to meet rising demand from growing and aging populations.

Across the region, upper‑middle–income and lower‑middle–income countries averaged about 2.5–2.8 hospital beds per 1 000 population in 2023, a figure below many high‑income peers but indicative of rapid healthcare service scale‑up that supports broader use of patient transport and care equipment.

Expansion of hospital networks in China and India has driven new capital investment in emergency, surgical, and intensive care units, elevating requirements for versatile patient support equipment in addition to beds. Policymakers have increased funding for regional medical facilities, ensuring more equitable access to acute care services even in rural areas.

Rising prevalence of chronic diseases and higher rates of trauma and surgical interventions have pushed healthcare systems to procure equipment that can handle diverse clinical workflows. Private healthcare chains and international investors have contributed to construction and refurbishment of tertiary hospitals, boosting overall healthcare capacity and service delivery.

Clinicians and facility managers are emphasizing procurement of durable, easy‑to‑maneuver solutions to enhance safety and throughput in busy wards. Training programs and operational standards are harmonizing equipment usage across facilities, improving consistency of care. Collectively, these factors are expected to sustain strong growth in demand for patient handling and transport solutions throughout Asia Pacific.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the hospital stretchers market grow by refining ergonomic design, enhancing mobility features, and integrating patient safety technologies that improve caregiver efficiency and support smoother transfers across care areas.

They also strengthen value propositions by bundling service contracts, customizable accessories, and training programs that help facilities standardize handling protocols and reduce workplace injuries. Firms pursue strategic partnerships with large health systems, ambulatory surgical centers, and group purchasing organizations to secure preferred supplier agreements and larger order volumes.

Geographic expansion into North America, Europe, and high‑growth Asia Pacific broadens revenue streams and captures rising healthcare infrastructure investments tied to aging populations. Hill‑Rom Holdings, Inc., a subsidiary of Baxter International, exemplifies a diversified medical technology company with deep experience in patient care solutions, a broad range of stretcher and transport products, and coordinated commercial strategies that align innovation with hospital operational objectives.

The company advances its competitive agenda through disciplined investment in product development, targeted collaborations that extend clinical applicability, and a customer‑centric approach that translates practical enhancements into measurable clinical and operational benefits.

Top Key Players

- Hill-Rom Holdings, Inc. (Baxter)

- Stryker

- Narang Medical Limited

- FU SHUN HSING TECHNOLOGY CO., LTD

- MAC Medical, Inc.

- Royax

- Wy’East Medical

- Ferno-Washington, Inc.

- GF Health Products, Inc.

- TAYLOR HEALTHCARE PRODUCTS, INC.

Recent Developments

- In October 2024, Stryker introduced the ProCuity Wireless Bed, designed to support hospitals in lowering operational costs, minimizing patient fall incidents, and streamlining nurses’ workflow.

- In September 2024, a teenager in India developed a stretcher equipped with shock absorbers. This innovative design uses the patient’s own weight to balance their center of gravity, ensuring stability when moving over ramps, slopes, or uneven surfaces through a central wheel mechanism.

Report Scope

Report Features Description Market Value (2025) US$ 3.2 Billion Forecast Revenue (2035) US$ 5.9 Billion CAGR (2026-2035) 6.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Wheeled/Trolley Stretchers, Scoop Stretchers, Spine Board Stretchers, Basket Stretchers, Stair/Evacuation Chair Stretchers and Others), By Mobility Type (Motorized and Non-Motorized), By Application (Daycare/Inpatient, Surgery, Emergency/Trauma and Ambulatory/Transport) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Hill-Rom (Baxter), Stryker, Narang Medical, FU SHUN HSING, MAC Medical, Royax, Wy’East Medical, Ferno-Washington, GF Health, TAYLOR HEALTHCARE. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Hill-Rom Holdings, Inc. (Baxter)

- Stryker

- Narang Medical Limited

- FU SHUN HSING TECHNOLOGY CO., LTD

- MAC Medical, Inc.

- Royax

- Wy’East Medical

- Ferno-Washington, Inc.

- GF Health Products, Inc.

- TAYLOR HEALTHCARE PRODUCTS, INC.

Our Clients

- 179678

- Feb 2026