Quick Navigation

- Report Overview

- Key Takeaway

- Role of Generative AI

- Investment and Business Benefits

- Regional Analysis

- Product Type Analysis

- Material Type Analysis

- Manufacturing Technology Analysis

- End-user Industry Analysis

- Key Market Segments

- Emerging Trends

- Growth Factors

- Market Dynamics

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

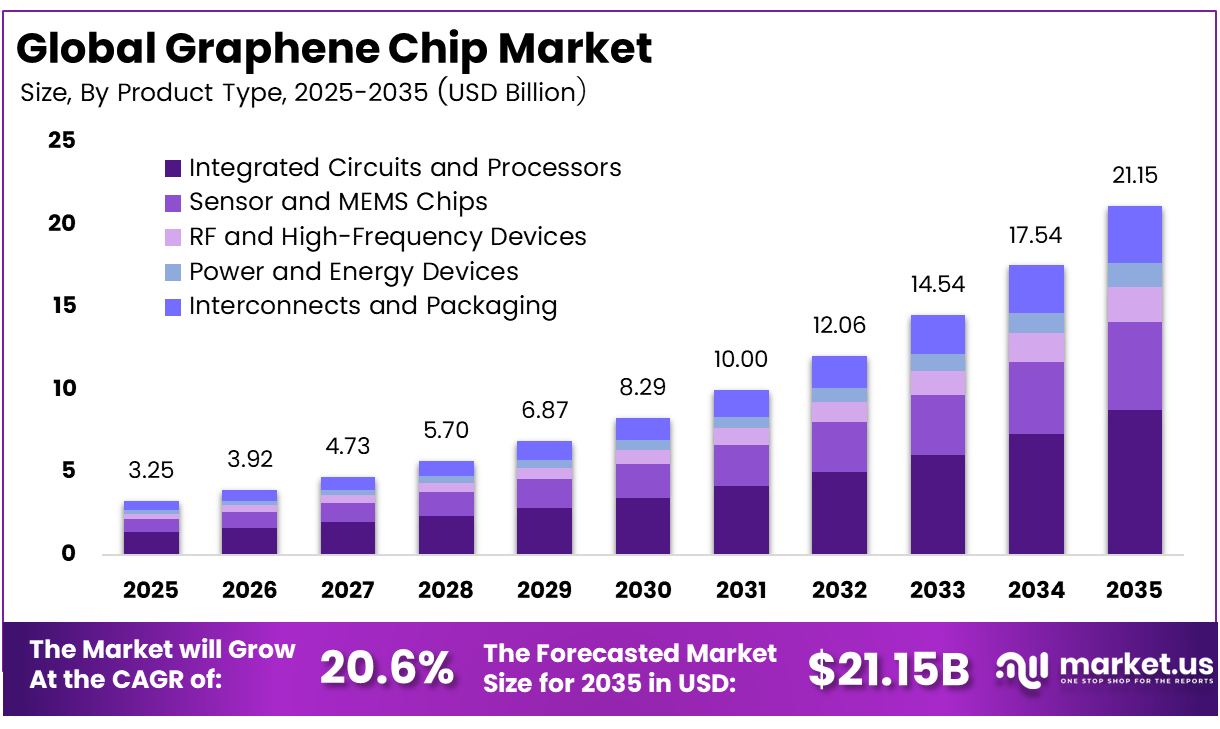

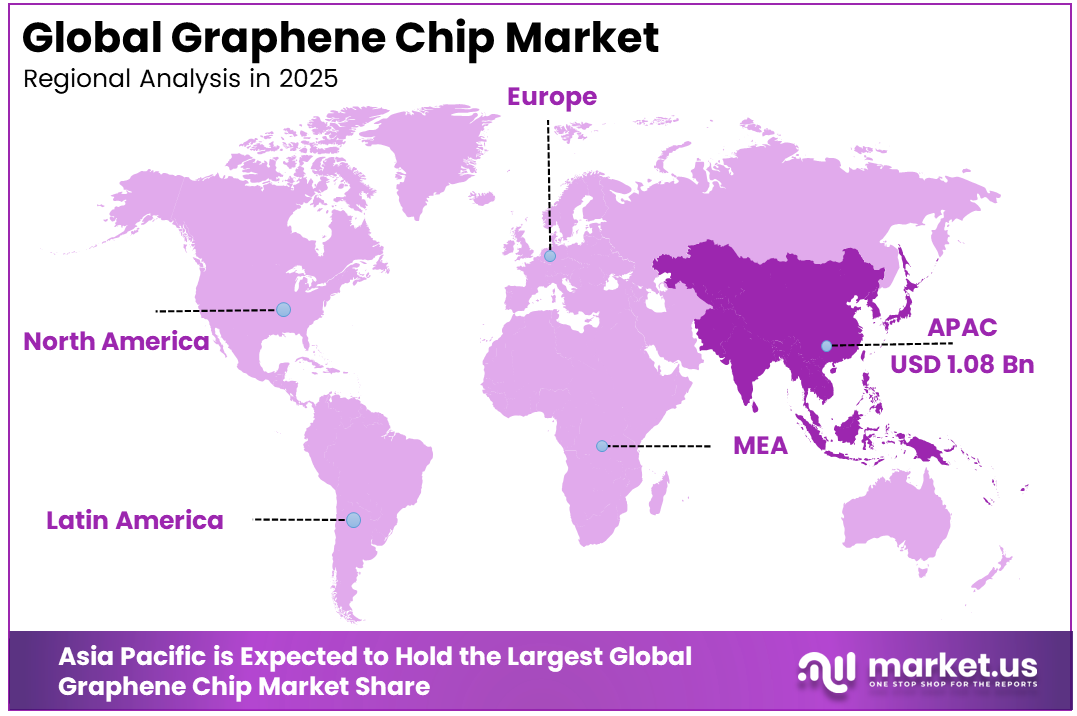

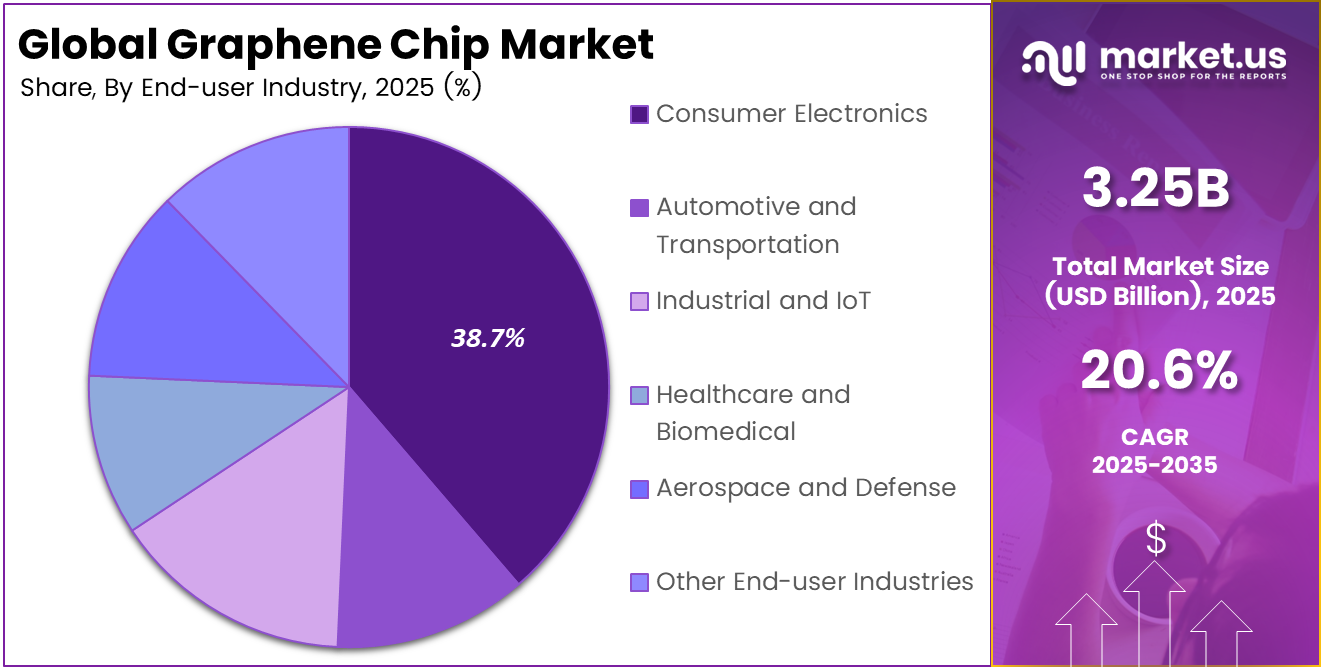

The Global Graphene Chip Market size is expected to be worth around USD 21.15 billion by 2035, from USD 3.25 billion in 2025, growing at a CAGR of 20.6% during the forecast period from 2025 to 2035. Asia Pacific held a dominant market position, capturing more than a 33.5% share, holding USD 1.08 billion in revenue.

A graphene chip refers to an electronic chip that uses graphene as a key material for conducting signals and improving performance. Graphene is a single layer of carbon atoms known for its high conductivity and strength. These chips are designed to deliver faster processing, lower power use, and better heat control in advanced electronics.

The need for faster switching, lower power use, and improved heat control is shaping material choices in modern electronics. Graphene transistors, reported to be up to 10 times faster than silicon in lab tests, are gaining attention. Demand is also supported by flexible displays, wearables, and advanced sensors that require thin, conductive, and bendable materials.

The market for Graphene Chip is driven by the need for faster data processing, lower energy use, and better heat control in modern electronics. Rising demand from AI systems, telecom networks, sensors, and edge devices is encouraging the use of advanced materials. Graphene’s high conductivity and thin structure support efficient chip performance in compact and high speed electronic applications.

Demand is rising across electronics, telecom, and computing, as these sectors need materials that support higher clock speeds, dense integration, and cooler operation. This is especially important for AI systems and high bandwidth networks. Government backed research lines and pilot lines in Europe and Asia also show movement from laboratory testing toward early industrial use.

For instance, in April 2026, Haydale was profiled among leading graphene semiconductor players, with its functionalized graphene additives feeding into inks, pastes, and composites for printed electronics. These materials are now being evaluated for antenna traces, interconnects, and thermal paths in emerging graphene chips and RF front-end designs.

Key Takeaway

- In 2025, the Integrated Circuits and Processors segment held a dominant market position, capturing a 41.6% share of the Global Graphene Chip Market.

- In 2025, the CVD Graphene Films segment held a dominant market position, capturing a 37.4% share of the Global Graphene Chip Market.

- In 2025, the Chemical Vapor Deposition segment held a dominant market position, capturing a 40.6% share of the Global Graphene Chip Market.

- In 2025, the Consumer Electronics segment held a dominant market position, capturing a 38.7% share of the Global Graphene Chip Market.

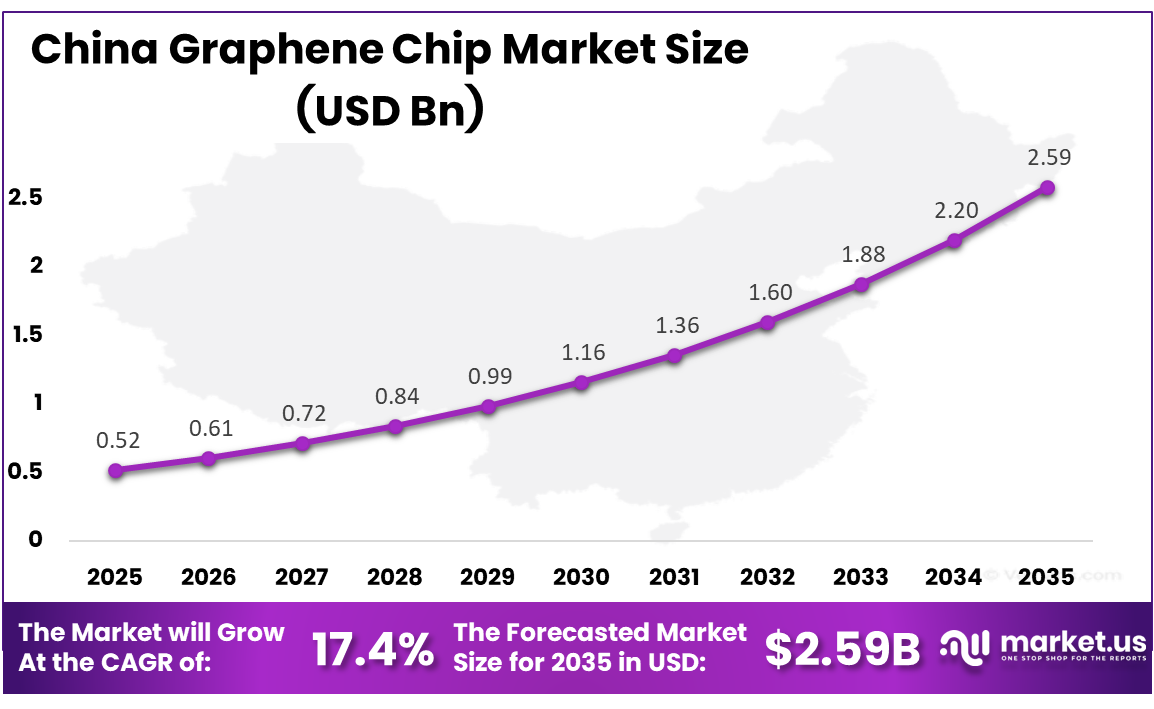

- The China Graphene Chip Market was valued at USD 0.52 Billion in 2025, with a robust CAGR of 17.4%.

- In 2025, the Asia Pacific held a dominant market position in the Global Graphene Chip Market, capturing more than a 33.5% share.

Role of Generative AI

Generative AI is influencing how graphene chips are discovered, designed, and tested before fabrication. In materials research, AI models help reduce billions of structure options to a few viable candidates. Some graphene production lines report AI-driven defect rates below 0.1% at the wafer level, supporting semiconductor grade quality improvements.

On the manufacturing side, more than 70% of new fabs are planning higher automation with AI integration. A major focus is on yield tuning, process control, and faster production ramp up. Generative AI is increasingly guiding decisions on process windows, device layouts, and reliability testing for emerging graphene based semiconductor platforms.

Investment and Business Benefits

Investment opportunities are centered on materials, device design, and production tools. Public and private programs are directing over 50 national and regional graphene projects into semiconductors, energy, and sensors. Early funding is largely focused on pilot lines that move production from grams to tons per year, with strong attention on yield, uniformity, and scale.

Business benefits include lower power use per operation, sometimes reduced by more than 30% in prototype logic compared with similar silicon circuits under the same workload. Companies may also gain from new product categories such as foldable devices and wearable health patches, where graphene’s ability to bend over 10,000 cycles without cracking adds strong value.

Regional Analysis

In 2025, the Asia Pacific held a dominant market position in the Global Graphene Chip Market, capturing more than a 33.5% share, holding USD 1.08 billion in revenue. This dominance is due to strong semiconductor manufacturing capacity, expanding electronics production, and active graphene research across China, Japan, South Korea, and Taiwan. The region benefits from mature supply chains, skilled fabrication capabilities, and rising demand for high-speed chips, sensors, wearables, and flexible devices. Government-backed material programs and industry partnerships also support faster movement from laboratory testing to pilot-scale graphene chip production.

For instance, in November 2025, graphene demand for high-performance electronics is surging as manufacturers adopt graphene in semiconductors, flexible displays, and sensor architectures. Graphene Platform and other domestic suppliers benefit from this ecosystem, reinforcing Asia Pacific’s role as a hub for graphene-enabled chip and device innovation.

China Graphene Chip Market Size

The market for Graphene Chip within China is growing tremendously and is currently valued at USD 0.52 billion; the market has a projected CAGR of 17.4%. The market is growing due to China’s strong push toward advanced semiconductors, high-speed electronics, and domestic material innovation. Rising investment in graphene research, chip design, sensors, and flexible electronics is supporting early commercialization. Demand is also increasing from telecom, consumer electronics, electric vehicles, and AI hardware, where low power use, faster switching, and better heat control are becoming important for next-generation device performance.

For instance, in March 2026, The Sixth Element was highlighted as one of China’s largest producers of graphene oxide and reduced graphene oxide, with industrial-scale capacity supporting graphene heat-dissipation films for advanced electronics. This production scale underpins China’s emerging dominance in graphene chips and thermal interface materials for high-performance devices.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Product Type Analysis

In 2025, the Integrated Circuits and Processors segment held a dominant market position, capturing a 41.6% share of the Global Graphene Chip Market. This dominance is due to the strong need for faster and energy-efficient computing systems. Graphene-based circuits are being explored for high-speed signal handling and low heat generation. Their use is increasing in advanced processors where traditional materials face limits in performance and power efficiency under demanding workloads.

Integrated circuits built with graphene offer improved electron mobility and support compact chip designs. This allows better performance in telecom, sensors, and computing systems. As industries focus on faster data processing and reduced energy use, graphene-based processors are gaining attention for next-generation electronic applications.

For instance, in November 2025, NanoXplore reported progress on a dry graphene manufacturing route that lowers production complexity and improves consistency of graphene additives. The development supports future use of graphene-enhanced materials in advanced integrated circuits where thermal and electrical performance need to improve together.

Material Type Analysis

In 2025, the CVD Graphene Films segment held a dominant market position, capturing a 37.4% share of the Global Graphene Chip Market. This dominance is due to the growing need for high-quality and large-area graphene materials that can be used in electronic device manufacturing. CVD graphene films provide consistent structure and conductivity, making them suitable for integration into semiconductor processes and supporting reliable device performance across applications.

These films are widely preferred for flexible electronics, transparent conductors, and sensor technologies. Their ability to be produced at wafer scale helps support industrial adoption, while maintaining material uniformity, which is important for ensuring consistent output in advanced electronic and optoelectronic devices.

For instance, in June 2025, at the Graphene 2025 conference in San Sebastian, Graphenea presented advances in CVD graphene film growth on 200 mm wafers. The work focused on improving uniformity and reproducibility, making these films more suitable for device grade chips and sensor arrays.

Manufacturing Technology Analysis

In 2025, the Chemical Vapor Deposition segment held a dominant market position, capturing a 40.6% share of the Global Graphene Chip Market. This dominance is due to the ability of chemical vapor deposition to produce graphene with controlled structure and high purity. This method supports repeatable production and aligns with semiconductor fabrication standards. It is considered a reliable approach for developing graphene materials suitable for integration into electronic and chip-level applications.

Chemical vapor deposition is gaining importance as industries move toward scalable graphene production. The method allows better control over film properties, which improves device performance. It also supports the transition from research scale to industrial scale manufacturing, making it a preferred technology for consistent and high-quality graphene output.

For instance, in March 2026, CVD Equipment Corporation reported new orders for deposition and gas delivery systems supporting semiconductor and advanced materials research. The company’s tools are used to refine chemical vapor deposition recipes for graphene and wide bandgap materials in university and industrial labs.

End-user Industry Analysis

In 2025, the Consumer Electronics segment held a dominant market position, capturing a 38.7% share of the Global Graphene Chip Market. This dominance is due to the rising need for flexible, lightweight, and energy-efficient electronic devices. Graphene supports thin and bendable components, which are ideal for wearables, displays, and compact gadgets. Its conductive properties enhance device performance while maintaining durability across different usage conditions.

Consumer electronics continue to adopt graphene as demand grows for innovative product designs. Flexible screens, smart wearables, and portable devices benefit from its strength and conductivity. The material enables new form factors while supporting long-term reliability, making it suitable for next-generation electronic products.

For instance, in October 2025, NanoXplore introduced new high surface area graphene grades designed for thermoplastics used in housings and components. These materials target improved durability and electrical properties in parts that go into everyday electronic devices and accessories.

Key Market Segments

By Product Type

- Integrated Circuits and Processors

- Sensor and MEMS Chips

- RF and High-Frequency Devices

- Power and Energy Devices

- Interconnects and Packaging

By Material Type

- CVD Graphene Films

- Graphene Nanoplatelets

- Graphene Oxide and rGO

- Graphene Nanoribbons and Quantum Dots

- Hybrid Metal-Graphene Structures

By Manufacturing Technology

- Chemical Vapor Deposition

- Epitaxial Growth on SiC

- Liquid Phase Exfoliation and Printing

- Plasma and Laser-Induced Growth

- Others

By End-user Industry

- Consumer Electronics

- Automotive and Transportation

- Industrial and IoT

- Healthcare and Biomedical

- Aerospace and Defense

- Other End-user Industries

Emerging Trends

A key trend is the use of graphene in areas where silicon interconnects face limits in heat and resistance. Applications include high-frequency RF systems, sensor front ends, and power-dense logic paths. Hybrid silicon graphene structures and controlled CVD methods are improving performance by nearly 30 to 50% in prototype FET designs.

Another trend is the shift toward flexible and wearable electronics using graphene. Its atom-thin structure allows integration into curved surfaces, textiles, and medical patches without losing conductivity. Flexible device adoption is increasing as manufacturing costs decline, with wearable electronics identified among the fastest-growing graphene-based application segments.

Growth Factors

Growth is driven by graphene’s high electrical conductivity, strong carrier mobility, and ultra-thin structure. These properties address challenges in high-performance computing, edge AI, and advanced sensors where heat and scaling limits restrict traditional materials. Graphene offers a path toward faster and more efficient chip performance in next-generation electronics.

The demand for ultra-fast and low-power processors in AI and edge devices is a major growth driver. Industry observations suggest this segment alone can contribute several percentage points to long-term growth. Graphene chips are gaining attention as a solution for energy-efficient computing and advanced sensing applications.

Market Dynamics

Drivers - Need for Faster Chips

The market is driven by the rising need for chips that can process data faster while using less energy. Graphene supports high electron mobility and strong heat movement, making it suitable for advanced processors, telecom systems, sensors, and compact devices that require quick response and stable performance.

This demand is increasing as AI, cloud computing, and edge devices place heavier pressure on existing chip materials. Graphene-based designs are being explored to reduce power loss and manage heat better in dense circuits. This makes the material attractive for next-generation computing and communication applications.

For instance, in July 2025, Graphenea showcased wafer-scale graphene foundry capabilities and graphene FET chips at a major graphene conference, stressing their relevance for next-generation high-speed biosensing and photonic applications that require rapid signal handling. Its foundry service aims to shorten development cycles for customers seeking faster chip prototypes on 200 mm wafers.

Restraint - High Manufacturing Cost

High manufacturing costs remain a major restraint for the graphene chip market. Producing uniform and high-quality graphene for semiconductor use requires advanced equipment, controlled processes, and skilled handling. These requirements increase production expenses and make large-scale adoption difficult for many electronics manufacturers.

Cost pressure also comes from wafer transfer, testing, defect control, and integration with existing chip lines. Even small material variations can affect device performance, which raises quality control needs. Until production becomes more repeatable and affordable, graphene chip commercialization may remain limited to selected high-value applications.

For instance, in December 2025, Paragraf reported progress on 6-inch graphene wafers with graphene grown directly on silicon, but also underlined the complexity of scaling such processes in a cost-effective way. Moving from smaller formats to larger wafers involves investment in new tools and yield optimisation, which keeps overall manufacturing costs high in the near term.

Opportunities - Flexible and Wearable Electronics

Flexible and wearable electronics create a strong opportunity for graphene chips. Graphene is thin, conductive, and bendable, which makes it suitable for smart watches, health patches, flexible displays, and sensor-based devices. These products need materials that can perform well on curved, moving, or lightweight surfaces.

The opportunity is also supported by rising interest in medical monitoring, connected clothing, and foldable consumer devices. Graphene can help improve comfort, durability, and signal performance in these applications. As device makers look beyond rigid electronics, graphene-based components can support new product formats and design flexibility.

For instance, in August 2025, Haydale reported work with HP1 Technologies on piezoresistive graphene inks used in flexible printed sensors, initially focused on safety helmets. The same technology is being adapted for aerospace, robotics, and utilities, showing how printed graphene sensors can fit into wearable or curved surfaces and extend electronic monitoring into places where rigid silicon devices are difficult to use.

Challenges - Competition with an Established Silicon Ecosystem

A major challenge is competition from the well-established silicon ecosystem. Silicon manufacturing has decades of process maturity, supplier networks, design tools, and fabrication standards. This makes it difficult for graphene chips to replace existing technologies, especially in applications where silicon already delivers reliable performance at scale.

Graphene adoption will depend on proving clear performance, cost, and reliability advantages over silicon-based solutions. Device makers may hesitate to shift unless production methods become stable and compatible with current chipmaking lines. This creates a long qualification cycle for graphene in mainstream semiconductor applications.

For instance, in September 2024, NanoXplore emphasized its role as a materials supplier across plastics and energy applications rather than a direct competitor to silicon chip vendors. The company’s strategy of embedding graphene into existing industrial products reflects a pragmatic recognition that penetrating the entrenched silicon-based electronics ecosystem is challenging and often requires indirect routes through supporting materials and components.

Key Players Analysis

One of the leading players in January 2026, Haydale completed the acquisition of SaveMoneyCutCarbon to build a broader graphene-enabled clean-tech platform. The deal strengthens Haydale’s downstream access to smart building and energy-efficiency projects, where graphene-based heating films and sensor chips can be embedded into connected devices rather than sold as raw materials alone.

Top Key Players in the Market

- Paragraf Limited

- Graphenea S.A.

- NanoXplore Inc.

- Graphene Square Inc.

- XG Sciences Inc.

- CVD Equipment Corporation

- Haydale Graphene Industries Plc

- First Graphene Limited

- Directa Plus S.p.A.

- Global Graphene Group Inc.

- Applied Graphene Materials Plc

- Versarien Plc

- Vorbeck Materials Corp.

- Grolltex Inc.

- The Sixth Element (Changzhou) Materials Technology Co., Ltd.

- Graphene Platform Corporation

- Thomas Swan and Co. Ltd.

- Angstron Materials Inc.

- Universal Matter Inc.

- Grafoid Inc.

- Skeleton Technologies Group OÜ

- Others

Recent Developments

- In April 2026, Paragraf secured $55 million in fresh funding to scale production of its wafer-level graphene chips and Hall-effect sensor devices. The company is ramping a dedicated graphene-on-wafer line aimed at high-sensitivity sensing and next-generation power electronics, signalling that graphene chips are moving from pilots to early commercial volumes.

- In March 2026, Graphene Square completed a new mass-production plant for CVD graphene films in Korea. The facility targets flexible electronics, transparent conductive layers, and early graphene chip stack concepts, giving device makers reliable access to industrial volumes of large-area graphene that can be integrated into sensors, RF components, and display-driven system-on-panel platforms.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.25 Billion |

| Forecast Revenue (2035) | USD 21.15 Billion |

| CAGR (2026-2035) | 20.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Integrated Circuits and Processors, Sensor and MEMS Chips, RF and High-Frequency Devices, Power and Energy Devices, Interconnects and Packaging), By Material Type (CVD Graphene Films, Graphene Nanoplatelets, Graphene Oxide and rGO, Graphene Nanoribbons and Quantum Dots, Hybrid Metal-Graphene Structures), By Manufacturing Technology (Chemical Vapor Deposition, Epitaxial Growth on SiC, Liquid Phase Exfoliation and Printing, Plasma and Laser Induced Growth, Others), By End-user Industry (Consumer Electronics, Automotive and Transportation, Industrial and IoT, Healthcare and Biomedical, Aerospace and Defense, Other End-user Industries) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Paragraf Limited, Graphenea S.A., NanoXplore Inc., Graphene Square Inc., XG Sciences Inc., CVD Equipment Corporation, Haydale Graphene Industries Plc, First Graphene Limited, Directa Plus S.p.A., Global Graphene Group Inc., Applied Graphene Materials Plc, Versarien Plc, Vorbeck Materials Corp., Grolltex Inc., The Sixth Element (Changzhou) Materials Technology Co. Ltd., Graphene Platform Corporation, Thomas Swan and Co. Ltd., Angstron Materials Inc., Universal Matter Inc., Grafoid Inc., Skeleton Technologies Group OÜ, Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |