Quick Navigation

Report Overview

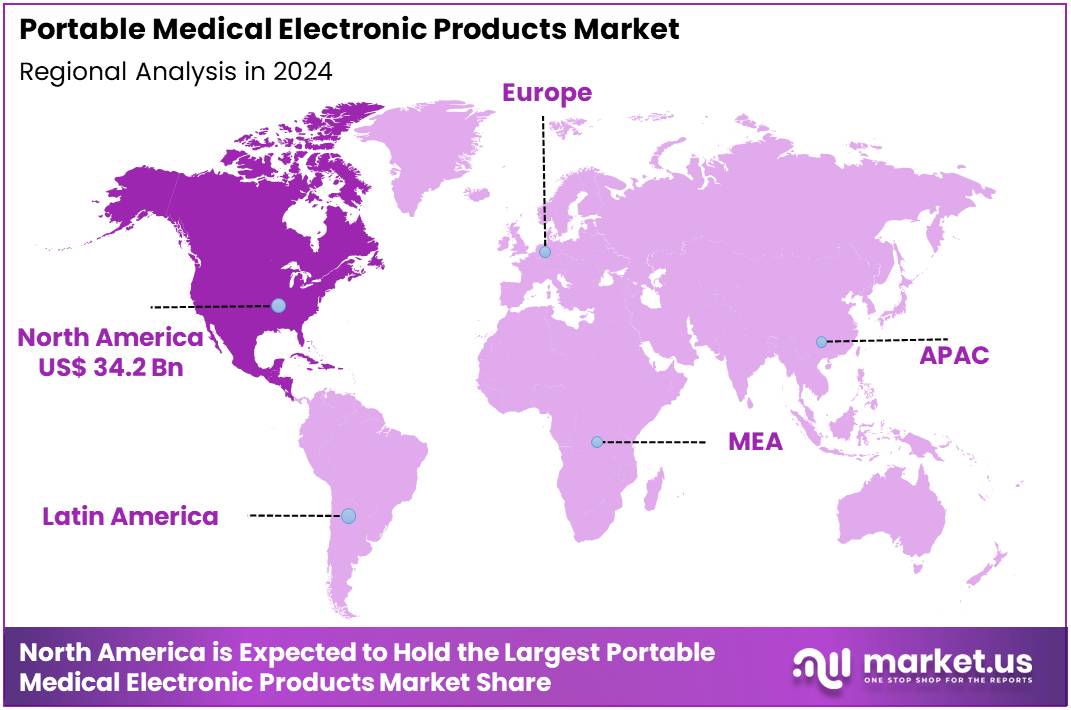

The Portable Medical Electronic Products Market size is expected to be worth around US$ 204.3 billion by 2034 from US$ 83.2 billion in 2024, growing at a CAGR of 9.4% during the forecast period 2025 to 2034. North America held a dominant market position, capturing more than a 41.1% share and holds US$ 34.2 Billion market value for the year.

Rising demand for convenient, on-the-go health monitoring is driving the growth of the portable medical electronic products market. These devices, which include portable diagnostic tools, wearables, and home healthcare equipment, provide individuals with the ability to monitor their health continuously and in real-time.

Applications of portable medical electronic products span a wide range of areas, such as heart rate monitoring, blood pressure tracking, glucose level measurement, and fitness tracking. The increasing prevalence of chronic diseases, including diabetes and cardiovascular conditions, is pushing healthcare providers and consumers toward more accessible and efficient diagnostic solutions.

In March 2022, Mobvoi Inc., in partnership with CardieX, launched the TicWatch GTH Pro, a smartwatch designed for heart health monitoring. This device, equipped with advanced sensors, offers detailed insights into both general and arterial health, capturing data from both the wrist and finger for improved accuracy and user experience.

Recent trends show a significant rise in the adoption of smartwatches and fitness trackers, integrating advanced sensors to track multiple health parameters. Additionally, the growing focus on preventive healthcare and the aging population present ample opportunities for the market. As technology continues to evolve, innovations in miniaturization, wireless connectivity, and AI integration will likely drive further expansion of the portable medical electronic products market.

Key Takeaways

- In 2024, the market for Portable Medical Electronic Products generated a revenue of US$ 83.2 billion, with a CAGR of 9.4%, and is expected to reach US$ 204.3 billion by the year 2033.

- The product type segment is divided into monitoring devices, diagnostic imaging, and others, with diagnostic imaging taking the lead in 2024 with a market share of 48.6%.

- Considering application, the market is divided into gynecology, gastrointestinal, cardiology, neurology, orthopedics, respiratory, and others. Among these, cardiology held a significant share of 32.8%.

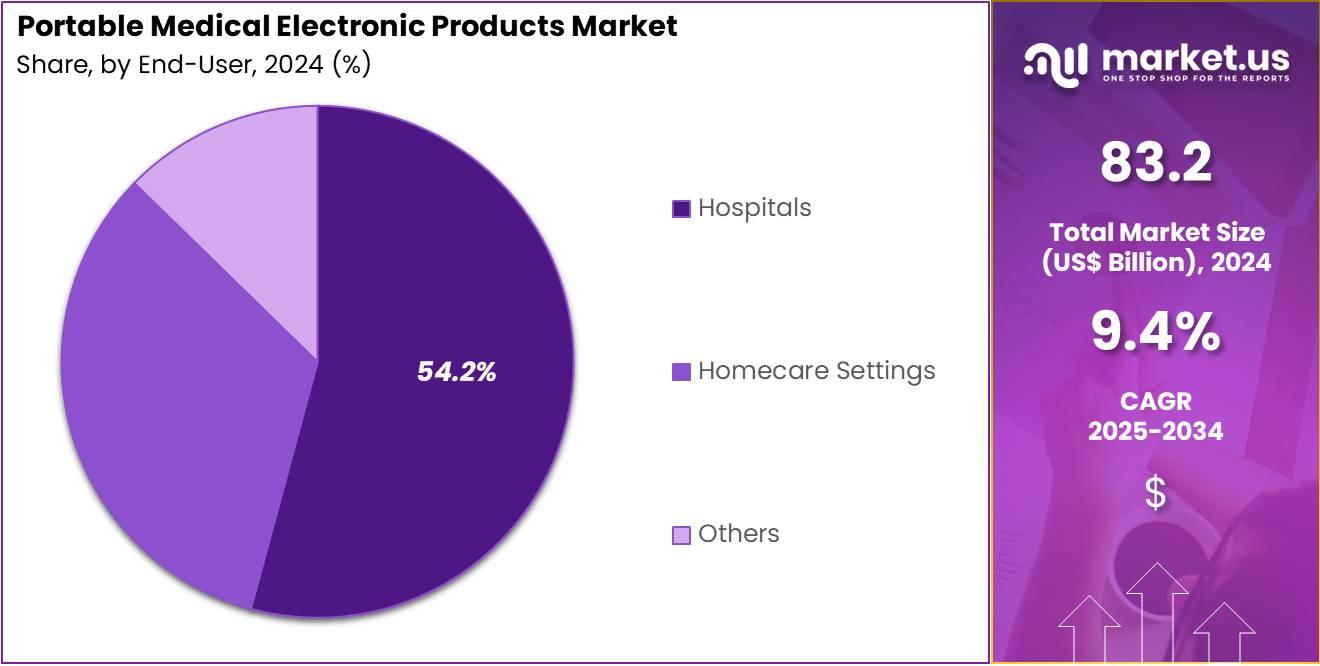

- Furthermore, concerning the end-user segment, the market is segregated into hospitals, homecare settings, and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 54.2% in the Portable Medical Electronic Products market.

- North America led the market by securing a market share of 41.1% in 2024.

Product Type Analysis

The diagnostic imaging segment led in 2024, claiming a market share of 48.6% owing to the increasing demand for portable imaging devices that offer flexibility and convenience in diagnosing patients. Portable diagnostic imaging devices, such as handheld ultrasound and portable X-ray machines, are anticipated to see greater adoption due to their ability to provide immediate, on-site results.

The rising need for emergency and point-of-care diagnostics, especially in remote or underserved areas, is likely to fuel demand for portable imaging solutions. Additionally, technological advancements that improve image quality and device portability are expected to further drive growth in this segment. As healthcare professionals increasingly rely on portable imaging for quick and accurate diagnosis, the demand for these devices will likely continue to rise.

Application Analysis

The cardiology held a significant share of 32.8% due to the increasing prevalence of cardiovascular diseases and the need for continuous monitoring. Portable devices for monitoring heart health, such as portable ECGs, heart rate monitors, and wearable defibrillators, are projected to see widespread adoption as patients seek to manage heart conditions outside of clinical settings.

The growing focus on preventive healthcare, early detection, and personalized treatment plans for cardiovascular diseases is expected to drive demand for these portable devices. Additionally, advancements in wireless technology and remote monitoring capabilities will likely enhance the adoption of portable cardiology products, allowing healthcare providers to monitor patients in real-time, improving patient outcomes and reducing hospital readmissions.

End-User Analysis

The hospitals segment had a tremendous growth rate, with a revenue share of 54.2% owing to the increasing need for flexible, space-saving, and cost-effective diagnostic solutions in healthcare facilities. Hospitals are likely to continue to be key end-users of portable medical electronic products, as they provide crucial diagnostic capabilities in emergency departments, intensive care units, and outpatient settings.

The rising demand for remote patient monitoring, coupled with the growing emphasis on reducing hospital stays and improving patient outcomes, is projected to contribute to the growth of this segment. Moreover, the adoption of portable medical devices in hospitals is expected to increase as hospitals focus on enhancing diagnostic accuracy, providing timely care, and reducing overall healthcare costs, further driving market expansion.

Key Market Segments

By Product Type

- Monitoring Devices

- Diagnostic Imaging

- Others

By Application

- Gynecology

- Gastrointestinal

- Cardiology

- Neurology

- Orthopedics

- Respiratory

- Others

By End-user

- Hospitals

- Homecare Settings

- Others

Drivers

Growing Prevalence of Non-Communicable Diseases

Growing prevalence of non-communicable diseases (NCDs) is anticipated to drive the portable medical electronic products market significantly. In May 2023, the World Health Organization reported that NCDs could account for 86% of global deaths by 2050 without effective preventative measures. This alarming statistic underscores the need for accessible, patient-centric solutions to monitor and manage chronic conditions such as diabetes, cardiovascular diseases, and respiratory disorders.

Portable medical devices offer real-time monitoring, enabling patients to track vital parameters like glucose levels, blood pressure, and oxygen saturation from the comfort of their homes. Increasing demand for compact and user-friendly products drives innovation in wearable technologies and handheld diagnostic tools. Healthcare providers recommend portable devices to improve patient engagement and adherence to treatment plans.

Expanding awareness about preventive healthcare solutions accelerates the adoption of these products globally. Technological advancements, including wireless connectivity and data integration, enhance device efficiency and functionality. Rising adoption of telemedicine further supports the use of portable devices, bridging healthcare access gaps in underserved regions. These trends position portable medical electronic products as essential tools in combating the growing burden of NCDs worldwide.

Restraints

High Costs Are Restraining the Portable Medical Electronic Products Market

High costs associated with portable medical electronic products are restraining the market. Advanced technologies, such as wireless connectivity and AI integration, require significant investment in research and manufacturing, increasing product prices. Patients in low- and middle-income countries often find these devices unaffordable, limiting market penetration.

Limited insurance coverage for portable diagnostic tools further discourages adoption in cost-sensitive regions. Healthcare providers face challenges in procuring and maintaining these devices due to budget constraints, particularly in public health systems. Training requirements for operating sophisticated devices add additional costs for hospitals and clinics.

Variability in global regulatory standards delays product launches and increases compliance expenses for manufacturers. Addressing these cost-related challenges requires innovations that reduce production costs and the implementation of financial support programs to improve affordability.

Opportunities

Development of Novel Technologies

Development of novel technologies is projected to create significant opportunities for the portable medical electronic products market. In May 2023, GenWorks introduced BrasterPro, a portable breast cancer screening device featuring radiation-free and contact-based technology. This innovation enhances accessibility to early detection, especially in resource-constrained healthcare settings. Advancements in sensor technologies and miniaturization enable the development of compact and efficient devices for a range of applications.

Integration of AI and machine learning algorithms improves diagnostic accuracy and supports personalized healthcare solutions. Increasing investment in research fosters breakthroughs in wearable and handheld technologies for continuous health monitoring. Collaborations between technology providers and healthcare institutions accelerate the commercialization of innovative devices.

Expanding government initiatives to promote healthcare digitization further boost the adoption of advanced portable solutions. These trends emphasize the transformative potential of novel technologies in advancing the portable medical electronic products market and addressing critical healthcare needs globally.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly impact the portable medical electronic products market. On the positive side, increasing healthcare investments and a growing focus on improving patient care globally fuel the demand for compact, easy-to-use medical devices. Rising healthcare awareness and the need for remote monitoring solutions also support market growth, particularly in emerging markets with limited access to traditional healthcare facilities.

However, economic recessions or budget cuts in healthcare spending can limit the affordability and availability of advanced portable devices, especially in low-income regions. Geopolitical factors such as trade restrictions and regulatory inconsistencies between countries may disrupt the supply chain and increase production costs for medical device manufacturers.

Moreover, political instability and shifting government policies could delay product approvals or hinder market access. Despite these challenges, the growing demand for healthcare solutions that offer convenience and accessibility continues to drive positive growth for portable medical products.

Trends

Surge in Mergers and Acquisitions Driving the Portable Medical Electronic Products Market

Rising mergers and acquisitions are driving the portable medical electronic products market. High levels of consolidation between medical device manufacturers, technology companies, and healthcare providers are expected to foster innovation, enhance product portfolios, and improve market competitiveness. These strategic partnerships allow for the integration of advanced technologies and broaden the reach of portable medical devices in different healthcare segments.

In February 2023, Sterling Medical Devices completed a merger with RBC Medical Innovations, facilitated by Ampersand Capital Partners, bringing together their expertise in medical device design and manufacturing. The merger aims to address evolving market needs more effectively. David Montecalvo, a Med Tech industry veteran with over 35 years of experience, was named CEO, while Sterling’s founder, Dan Sterling, and RBC’s founder, Carl Mayer, will continue in leadership roles to drive the company forward. As the trend of mergers and acquisitions continues, the market is expected to experience increased product development and expanded access, leading to significant growth in portable medical electronics.

Regional Analysis

North America is leading the Portable Medical Electronic Products Market

North America dominated the market with the highest revenue share of 41.1% owing to increasing demand for convenient, cost-effective, and patient-friendly healthcare solutions. The rise in chronic diseases, the aging population, and the growing need for home healthcare have all contributed to the market’s expansion.

Portable medical devices, such as monitors for blood pressure, glucose, and heart rate, have become essential for remote patient monitoring, especially in managing long-term conditions. A key development in the market was Trukera Medical’s rebranding and the introduction of the ScoutPro Osmolarity System in September 2022. This portable osmometer, the first of its kind in the U.S., was designed to help eye care professionals make more informed decisions regarding corneal health, particularly in cataract and refractive surgeries.

By enabling efficient osmolarity testing, this technology addresses the growing demand for portable solutions in specialized healthcare fields. As healthcare becomes more patient-centered, and the need for on-the-go diagnostics increases, the portable medical electronic products market in North America is expected to continue its growth, offering improved healthcare access and management.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to expanding healthcare access, rising consumer awareness, and the increasing adoption of home healthcare solutions. Countries such as India, China, and Japan are expected to see a surge in demand for portable medical devices as healthcare systems improve and more people seek to monitor their health at home.

In February 2022, Healthnet Global, a division of Apollo Hospitals, launched Automaid, a cutting-edge system designed to automate inpatient rooms for enhanced remote monitoring and triaging. This system is expected to improve the efficiency of patient care management by enabling real-time monitoring and data collection, which will likely contribute to the growth of the market.

The growing prevalence of chronic diseases, the rise in telemedicine adoption, and government initiatives to improve healthcare infrastructure will further accelerate demand for portable medical products. As the region continues to invest in healthcare technology and accessibility, the portable medical electronic products market in Asia Pacific is expected to expand significantly.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the portable medical electronic products market focus on developing compact, lightweight, and user-friendly devices that cater to both clinical and home healthcare needs. Companies invest in R&D to integrate advanced features such as wireless connectivity, real-time monitoring, and AI-driven analytics. Strategic collaborations with healthcare providers and technology firms drive innovation and expand application areas.

Geographic expansion into regions with increasing demand for remote patient monitoring and personalized healthcare solutions supports growth. Many players also emphasize affordability and regulatory compliance to ensure accessibility and trust. Philips Healthcare is a leading company in this market, offering a wide range of portable medical devices, including handheld diagnostic tools and patient monitoring systems. The company combines cutting-edge technology with ergonomic designs to deliver reliable and efficient solutions. Philips’ global reach and focus on advancing connected healthcare solidify its position as a leader in portable medical electronics.

Top Key Players in the Portable Medical Electronic Products Market

- VYAIRE

- Samsung

- OMRON Corporation

- Medtronic

- Koninklijke Philips N.V.

- General Electric Company

- Hoffmann-La Roche Ltd

- Biocorp

Recent Developments

- In October 2022, Biocorp, a French company renowned for its advanced medical device solutions, formed a partnership with Novo Nordisk to bring Mallya, a smart sensor, to market. This device attaches to Novo Nordisk’s FlexTouch insulin pens and enables enhanced blood glucose monitoring, with the initial launch focused on Japan.

- In September 2021, GE Healthcare unveiled the AMX Navigate, a cutting-edge portable digital X-ray system. Featuring a power-assisted Free Motion telescoping column, this system reduces lift force by up to 70%, enhancing technologist safety and improving operational efficiency by easing movement and setup.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 83.2 billion |

| Forecast Revenue (2034) | US$ 204.3 billion |

| CAGR (2025-2034) | 9.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Monitoring Devices, Diagnostic Imaging, and Others), By Application (Gynecology, Gastrointestinal, Cardiology, Neurology, Orthopedics, Respiratory, and Others), By End-user (Hospitals, Homecare Settings, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | VYAIRE, Samsung, OMRON Corporation, Medtronic, Koninklijke Philips N.V., General Electric Company, F. Hoffmann-La Roche Ltd, and Biocorp. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |