Global Oats Market Size, Share, And Industry Analysis Report By Type (Rolled Oats, Whole Oats, Steel Cut, Instant Oats, Others), By Application (Food and Beverage, Animal Feed, Personal Care and Cosmetics), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Grocery Stores, Online), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183737

- Number of Pages: 364

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

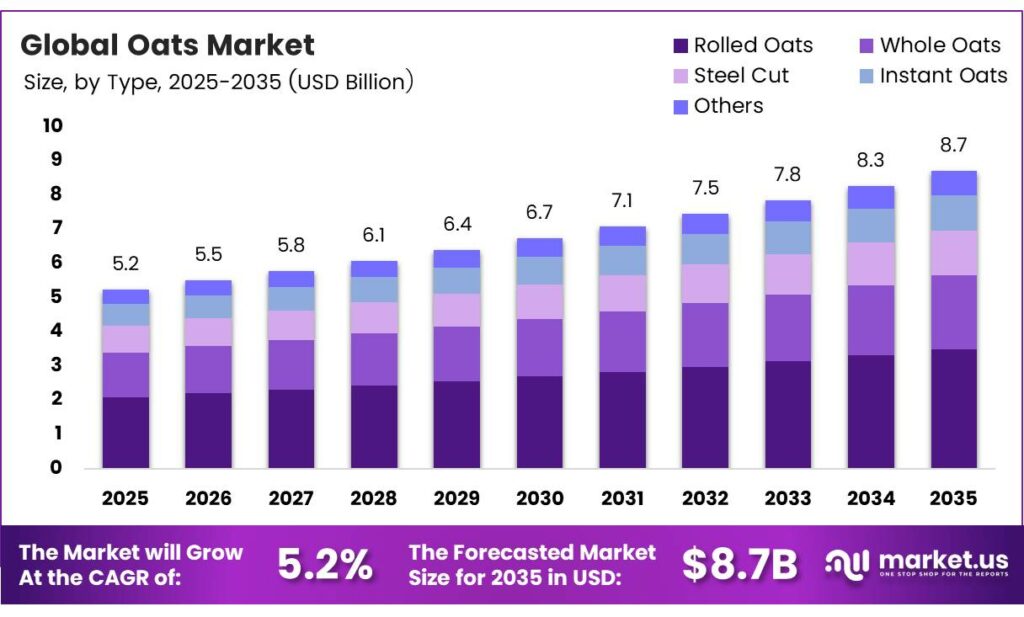

The Global Oats Market size is expected to be worth around USD 8.7 billion by 2035 from USD 5.2 billion in 2025, growing at a CAGR of 5.2% during the forecast period 2026 to 2035.

The oats market covers the production, processing, and distribution of oat-based products across food, beverage, animal feed, and personal care sectors. Oats serve as a versatile grain used in breakfast cereals, baked goods, dairy alternatives, and functional snacks. Moreover, growing health awareness continues to expand oat consumption globally.

Consumer demand for heart-healthy, high-fiber foods drives oat adoption across multiple product categories. Oats deliver beta-glucan, a soluble fiber clinically recognized for cholesterol reduction and cardiovascular support. Consequently, food manufacturers increasingly incorporate oats into fortified, functional, and clean-label product lines targeting health-conscious consumers.

Global oat production reached 24.65 million metric tons in MY 2025/2026, up 17% year over year from 19.44 million metric tons. This sharp production increase reflects expanded cultivated acreage and improved yield outcomes in key producing nations. The European Union oat production reached 8.0 million metric tons in MY 2025/2026, representing 32% of global output. This dominant EU share highlights Europe’s central role in shaping global oat supply dynamics and trade flows.

Oat-based dairy alternatives represent one of the fastest-growing segments within plant-based beverages. Coffee shops, foodservice operators, and retail brands actively expand their oat milk and oat cream offerings. Additionally, rising flexitarian and vegan consumer populations further accelerate demand for oat-derived milk substitutes across both developed and emerging markets.

Key Takeaways

- The Global Oats Market was valued at USD 5.2 billion in 2025 and is forecast to reach USD 8.7 billion by 2035 at a CAGR of 5.2% during the forecast period 2026 to 2035.

- Rolled Oats held the dominant share at 36.8% in 2025.

- The Food and Beverage segment led with a 74.6% market share in 2025.

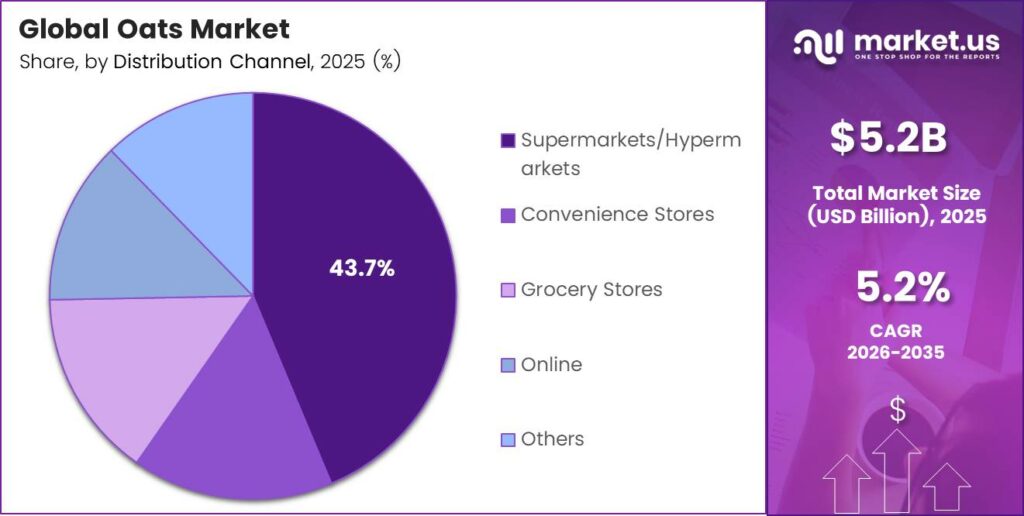

- Supermarkets and Hypermarkets captured 43.7% of the total market share in 2025.

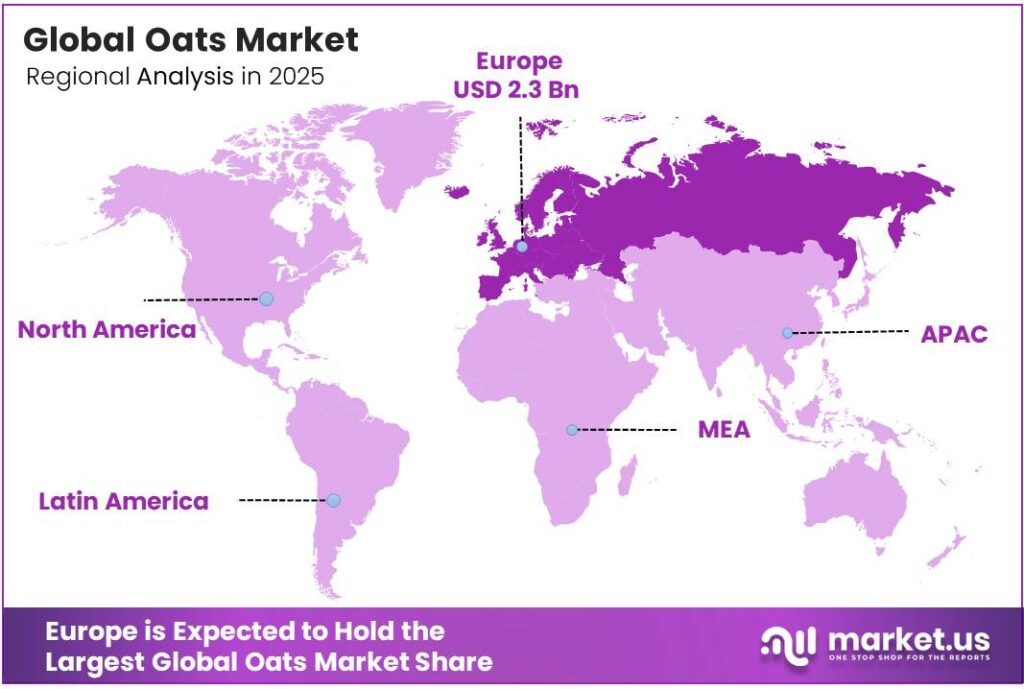

- Europe dominated the regional landscape with a 43.4% share, valued at USD 2.3 billion in 2025.

By Type Analysis

Rolled oats dominate with 36.8% due to widespread consumer preference for versatile, ready-to-cook oat formats.

In 2025, Rolled Oats held a dominant market position in the By Type segment of the Oats Market, with a 36.8% share. Rolled oats appeal to consumers seeking quick, nutritious breakfast options that require minimal preparation. Moreover, their compatibility with baked goods, granola bars, and overnight oats recipes drives consistent retail demand globally.

Whole Oats serve as the foundational raw form processed into downstream oat products. Grain processors and millers rely on whole oats for production inputs. Additionally, growing interest in minimally processed and clean-label foods encourages some consumers to purchase whole oat groats for home cooking and specialty applications.

Steel-cut oats attract health-focused consumers who prioritize lower glycemic index and richer nutritional density. This variety undergoes minimal processing, preserving more fiber and nutrients. Consequently, premium retail channels and specialty grocery stores increasingly stock steel-cut oats to meet demand from nutrition-aware adult consumers.

By Application Analysis

Food and Beverage dominates with 74.6% due to oats’ central role across breakfast, snack, and dairy alternative categories.

In 2025, the Food and Beverage segment held a dominant market position in the By Application segment of the Oats Market, with a 74.6% share. This dominance reflects oats’ deep integration across cereals, baked goods, beverages, and dairy alternatives. Moreover, oat milk’s rapid rise in coffee shops and supermarkets significantly contributes to this segment’s sustained leadership.

The Animal Feed segment represents a critical secondary application for oat by-products and lower-grade oat grades. Livestock producers value oats for their digestible fiber and energy content in equine and poultry nutrition. Consequently, feed mills and agricultural cooperatives maintain consistent procurement of feed-grade oats from regional grain suppliers throughout the year.

Personal Care and Cosmetics applications leverage colloidal oatmeal for its proven skin-soothing and anti-inflammatory properties. Dermatologist-recommended skincare brands incorporate oat extracts into creams, cleansers, and bath products. Additionally, rising consumer demand for natural and hypoallergenic formulations accelerates oat ingredient adoption within premium personal care product development pipelines.

By Distribution Channel Analysis

Supermarkets/Hypermarkets dominate with 43.7% due to high consumer footfall and a broad oat product variety on shelves.

In 2025, Supermarkets/Hypermarkets held a dominant market position in the By Distribution Channel segment of the Oats Market, with a 43.7% share. Large-format retail stores provide consumers with extensive oat product selections from multiple brands. Moreover, in-store promotions, loyalty programs, and health-focused product placement strategies effectively drive repeat oat purchases among mainstream shoppers.

Convenience Stores serve time-pressed consumers seeking quick single-serve oat snacks and instant breakfast options. Ready-to-eat oat cups and single-portion packs perform well in convenience retail formats. Additionally, urban commuter populations increasingly rely on convenience store channels to access nutritious on-the-go oat products without visiting larger grocery destinations.

Grocery Stores serve as community-level retail anchors for everyday household oat purchases. Independent and regional grocery operators stock both national brands and private-label oat products. Consequently, grocery retailers maintain a strong oat category presence by offering value-priced formats that appeal to budget-conscious family shoppers seeking weekly staple grain purchases.

Key Market Segments

By Type

- Rolled Oats

- Whole Oats

- Steel Cut

- Instant Oats

- Others

By Application

- Food and Beverage

- Animal Feed

- Personal Care and Cosmetics

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Grocery Stores

- Online

- Others

Emerging Trends

Plant-Based Diets and Multi-Use Oat Ingredients Redefine Product Innovation

The boom in plant-based and flexitarian diets accelerates multi-use oat ingredient innovation across food and beverage categories. Manufacturers develop oat-based milk, yogurt, and cheese alternatives to meet rising consumer demand. Canada oat production reached 3.92 million metric tons in MY 2025/2026, accounting for 16% of global supply, reflecting strong raw material availability supporting innovation pipelines.

E-Commerce Platforms and Clean-Label Products Reshape Oat Market Access

E-commerce and online grocery platforms significantly enhance consumer accessibility to specialty and organic oat offerings. Clean-label and minimally processed oat products gain strong momentum among wellness-focused shoppers globally. Moreover, integration of oats into personalized nutrition platforms and AI-driven meal planning solutions creates emerging opportunities for brands targeting data-informed, health-conscious consumer segments.

Drivers

Beta-Glucan Demand and Heart Health Awareness Fuel Oat Consumption Growth

Surging consumer demand for beta-glucan-rich foods targeting cholesterol management drives oat market expansion significantly. Health authorities globally recognize oat beta-glucan’s clinically validated cardiovascular benefits, prompting increased product launches. Canada’s oat exports reached $445.15 million and 1,524,070,000 kg in 2024, confirming Canada as the largest global oat exporter by both value and volume.

Oat-Based Dairy Alternatives and Convenient Formats Drive Broad Market Adoption

Rapid expansion of oat-based dairy alternatives in coffee shops and foodservice channels creates substantial new demand. Additionally, growing consumer preference for convenient on-the-go instant oat products accelerates retail category growth. Rising adoption of oats in functional snacks and fortified bakery items further broadens daily consumption occasions, reinforcing oats as a core ingredient in modern health-driven diet patterns.

Restraints

Grain Price Volatility Pressures Production Costs and Supply Chain Economics

Volatility in global grain prices creates significant challenges for oat producers managing raw material procurement and production costs. Price fluctuations reduce profit margins for smaller processors and limit their ability to offer competitive retail pricing. The 10-year average global oat production stood at 23.41 million metric tons across MY 2016–2025, indicating a stable long-term supply despite short-term price instability.

Climate Disruptions and Yield Variability Threaten Consistent Oat Market Supply

Climate-induced yield fluctuations pose a growing threat to consistent oat availability across key producing regions. Extreme weather events, including droughts and flooding, disrupt crop cycles and reduce harvest predictability. Consequently, supply chain disruptions create procurement challenges for food manufacturers dependent on stable, high-volume oat ingredient inputs to maintain continuous production and retail shelf availability.

Growth Factors

Organic Oat Varieties and Premium Fortified Products Open New Market Segments

Expansion of organic and certified gluten-free oat varieties in emerging urban markets presents strong growth opportunities for producers. Health-conscious millennials actively seek premium flavored and fortified oat products offering enhanced nutritional profiles. Finland’s oat exports reached $145.40 million and 506,437,000 kg in 2024, driven by robust EU food-grade oat demand reflecting a strong premium market pull.

Sustainable Farming Investment and Oat-Derived Cosmetics Expand Market Frontiers

Investment in sustainable farming technologies and resilient seed breeding programs strengthens long-term oat supply security. Australia’s oat exports reached $122.76 million and 324,519,000 kg in 2024, supported by Asia-Pacific cereal and feed trade flows. Furthermore, penetration into personal care and cosmetic applications using oat-derived ingredients creates diversified, high-margin revenue streams for oat ingredient suppliers.

Regional Analysis

Europe Dominates the Oats Market with a Market Share of 43.4%, Valued at USD 2.3 Billion

Europe leads the global oats market, commanding a dominant 43.4% share valued at USD 2.3 billion in 2025. Strong consumer preference for healthy breakfast cereals, oat milk, and clean-label food products drives regional demand. EU oat, reinforcing Central Europe’s vital processing and supply chain role.

North America represents a mature and innovation-driven oats market supported by strong brand heritage and consumer health awareness. The United States leads domestic consumption through established cereal, snack, and oat beverage categories. Canada’s leadership as the world’s largest oat exporter by value and volume anchors regional supply chain strength and global trade influence.

Asia Pacific demonstrates the fastest emerging growth trajectory within the global oats market landscape. Rising middle-class health awareness in China, India, and Southeast Asia accelerates oat product adoption. Additionally, expanding retail infrastructure and e-commerce platforms enable oat brands to reach previously underserved urban and semi-urban consumer populations across the region.

The Middle East and Africa region presents early-stage but expanding oat market potential driven by urbanization and diet diversification. Imported oat products from Europe and Australia meet rising consumer demand in GCC countries. Consequently, modern retail expansion and growing health consciousness among younger demographics support incremental oat category growth across this developing regional market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Quaker Oats Company stands as one of the most recognized oat brands globally, with a comprehensive product portfolio spanning breakfast cereals, instant oats, and oat-based snack bars. The company consistently drives innovation through new flavors and fortified product lines targeting health-conscious consumers. Moreover, its strong retail distribution network spans North America, Europe, and key Asia Pacific markets effectively.

Morning Foods operates as a leading European oat processing and brand management company with deep roots in the UK market. The company manages a broad range of oat products from traditional porridge oats to granola and specialty oat-based cereals. Additionally, Morning Foods leverages strong private-label manufacturing capabilities to supply major European grocery retailers across multiple product tiers.

General Mills participates actively in the oats market through its established cereal and snack food divisions with globally recognized product lines. The company integrates oats across multiple brand portfolios, targeting both mainstream and health-focused consumer segments simultaneously. Consequently, General Mills continues to invest in oat ingredient innovation and sustainable sourcing initiatives to strengthen its long-term competitive market position.

Richardson International represents a major North American agribusiness player with significant oat origination, processing, and export capabilities. The company operates an integrated grain supply chain from farm procurement through to finished product manufacturing and international trade. Therefore, Richardson’s scale and infrastructure position it as a critical supplier to both domestic food manufacturers and global commodity trading markets.

Top Key Players in the Market

- Quaker Oats Company

- Morning Foods

- General Mills

- Richardson International

- Grain Millers

- Avena Foods

- Blue Lake Milling

- B&G Foods, Inc.

- The Kellogg Company

- Marico Limited

Recent Developments

- In January 2025, Morning Foods highlighted local sourcing from British farmers, waste reduction in milling, promotion of sustainable farming practices, and reductions in supply-chain carbon footprint. Packaging is designed for recyclability or biodegradability.

- In 2025, Grain Millers has the most direct ties to oat by-product processing relevant to an “oats pulp” or fiber sector (via oat hull utilization). Oat milling achieves near-zero waste: 99% landfill diversion at the St. Ansgar facility, achieved by selling byproducts for animal feed and using oat hulls for fiber production or poultry bedding.

Report Scope

Report Features Description Market Value (2025) USD 5.2 Billion Forecast Revenue (2035) USD 8.7 Billion CAGR (2026-2035) 5.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Rolled Oats, Whole Oats, Steel Cut, Instant Oats, Others), By Application (Food and Beverage, Animal Feed, Personal Care and Cosmetics, Others), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Grocery Stores, Online, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Quaker Oats Company, Morning Foods, General Mills, Richardson International, Grain Millers, Avena Foods, Blue Lake Milling, B&G Foods, Inc., The Kellogg Company, Marico Limited Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Quaker Oats Company

- Morning Foods

- General Mills

- Richardson International

- Grain Millers

- Avena Foods

- Blue Lake Milling

- B&G Foods, Inc.

- The Kellogg Company

- Marico Limited

Our Clients

- 183737

- April 2026