Quick Navigation

Report Overview

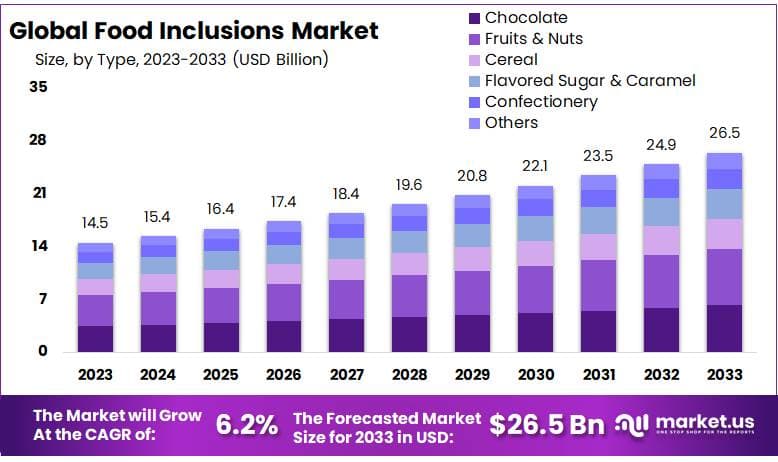

The global Food Inclusions Market size is expected to be worth around USD 26.5 billion by 2033, from USD 14.5 billion in 2023, growing at a CAGR of 6.2% during the forecast period from 2023 to 2033.

The food inclusions market represents a dynamic segment within the broader food industry, characterized by the integration of various edible elements into food products to improve their texture, flavor, appearance, and nutritional content. This market includes a diverse array of inclusions such as nuts, fruits, chocolates, flavored sugars, and spices, along with innovative additions like superfood grains and protein enhancers. These inclusions are commonly incorporated into bakery products, confectioneries, dairy items, snacks, and beverages.

Focusing on end-use industries, the bakery sector emerges as a significant contributor, accounting for roughly 30% of the overall market consumption of food inclusions. This reflects its central role in leveraging inclusions to enhance product appeal and meet consumer preferences. The dairy industry also shows promising growth prospects, with expectations of over 9% growth in the next five years. This surge is largely driven by increasing consumer demand for flavored dairy products such as milk and ice creams, which often feature a variety of flavorful and textural inclusions.

Regulatory considerations are critical in the food inclusion market, as they ensure the safety and integrity of food products. In the European Union, for instance, Regulation (EC) No 1169/2011 mandates the clear labeling of allergens in food inclusions, a practice mirrored by the U.S. FDA’s requirements for allergen disclosure on product labels. These regulations are crucial for protecting consumer health and making informed food choices, reinforcing the market’s commitment to compliance and safety.

Trade dynamics also play a crucial role in this market, influenced by international trade policies and tariffs, especially on key ingredients like cocoa, nuts, and exotic fruits. The U.S., for example, imported over $2 billion worth of processed fruits and nuts in 2022, highlighting the importance of these components in the food inclusions industry. Such trade activities underscore the interconnected nature of the global supply chain in supporting the market’s diverse product offerings.

Investment is another vital aspect of the food inclusion market, with significant contributions from both government and private sectors fostering innovation and infrastructure development. A notable instance is the USDA’s investment of approximately $50 million in 2021, aimed at advancing food processing technologies. This investment not only supports the existing market infrastructure but also catalyzes the development of new techniques and products within the food inclusions sector.

By Type

In 2023, Fruits & Nuts held a dominant market position, capturing more than a 28.4% share. This segment benefits greatly from consumer preferences for natural and healthy ingredients. Fruits and nuts are widely appreciated for their nutritional benefits and are often included in products targeting health-conscious consumers.

Chocolate is another significant category within the food inclusion market. It is favored for its universal appeal and versatility in a range of food products, from bakery items to snacks and dairy. Chocolate inclusions not only enhance flavor but also add a rich texture that is highly valued in confectionery and desserts.

The Cereal segment also plays a crucial role, particularly in breakfast foods and snack bars. Cereal inclusions offer functional benefits such as improved texture and added fiber, making them popular in products marketed as energy-boosting or fiber-rich.

The flavored Sugar & Caramel segment caters to the growing demand for indulgent, flavorful experiences in food consumption. These inclusions are key in sectors like bakery and confections, providing distinctive flavors and an enhanced sensory profile that attracts a broad consumer base.

Confectionery inclusions encompass a variety of candy and sweet particles that are integrated into food products for an added burst of flavor and texture. This segment thrives on innovation, with new flavors and colorful inclusions continually being developed to capture consumer interest and create visually appealing products.

By Form

In 2023, Solid & Semi-Solid forms held a dominant market position, capturing more than a 60.1% share. This segment’s popularity is driven by its versatility and ease of use in a wide array of food products. Solid and semi-solid inclusions like chunks, flakes, and granules are integral in providing texture and flavor enhancements in bakery products, snacks, and confectioneries. Their stability and ability to blend seamlessly with other ingredients make them a preferred choice in both industrial and artisanal food preparation.

The Liquid segment, while smaller, plays a crucial role in specific applications. Liquid inclusions such as syrups, purees, and flavored oils are favored for their ability to impart distinct flavors and moistness to products like cakes, beverages, and dairy items. Their ease of incorporation into various food matrices allows for innovative uses in culinary applications, especially in creating uniform flavor profiles and enhancing mouthfeel.

By Application

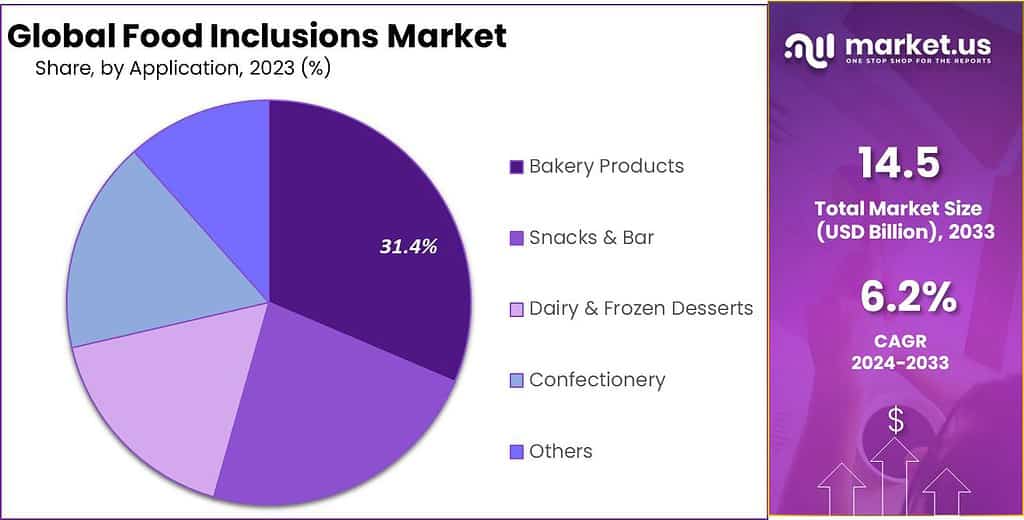

In 2023, Bakery Products held a dominant market position in the food inclusions market, capturing more than a 31.4% share. This segment benefits significantly from the diverse use of inclusions like fruits, nuts, and chocolate chips, which enhance taste and texture, making bakery items more appealing.

Snacks & Bars also represent a substantial portion of the market. These products often incorporate seeds, grains, and crunchy nuts to boost nutritional value and satisfy consumer demand for healthy, on-the-go eating options.

The Dairy & Frozen segment utilizes inclusions such as cookie dough pieces, fruit swirls, and candy bits to innovate and differentiate products like ice creams and flavored yogurts in a competitive market.

Desserts are another key area where food inclusions make a significant impact, adding both flavor and visual appeal to items such as puddings, mousses, and cakes. Here, the sensory experience is paramount, driving the demand for rich flavors and textures.

Confectionery uses inclusions to create fun and unique products, such as chocolates with caramel bits or gummies with fruit pieces. This segment thrives on constant innovation and the appeal of new taste sensations.

Key Market Segments

By Type

- Chocolate

- Fruits & Nuts

- Cereal

- Flavored Sugar & Caramel

- Confectionery

- Others

By Form

- Solid & Semi-Solid

- Liquid

By Application

- Bakery Products

- Snacks & Bar

- Dairy & Frozen Desserts

- Confectionery

- Others

Drivers

Increased Demand for Health-Conscious and Convenient Snack Options

One of the major driving factors for the food inclusion market is the rising consumer interest in health and wellness, which significantly influences their food choices. This trend is evident in the increasing demand for snack options that not only provide convenience but also offer health benefits. Food inclusions such as nuts, seeds, fruits, and whole grains are becoming popular additions in snacks and bars due to their nutritional profile, catering to health-conscious consumers seeking foods with added functional benefits.

This growth is supported by a shift towards snacks that not only satisfy hunger but also contribute to a healthy diet. Food inclusions play a crucial role in this sector by enhancing the taste, texture, and nutritional value of snacks, making them appealing to a broader demographic that prioritizes health alongside convenience.

Moreover, the demand for natural and clean label products is accelerating the growth of the food inclusions market. Consumers are increasingly looking for products with transparent ingredient lists that are free from artificial additives or preservatives. This preference drives the demand for natural food inclusions, which are perceived as healthier options. The market response includes a significant push towards innovations in natural food inclusions, aiming to meet the clean label standards demanded by today’s consumers.

The drive for healthier eating habits, combined with the need for convenient food options, significantly propels the food inclusions market forward. This trend is supported by the growing consumer preference for natural elements and clean-label products, highlighting a major opportunity area for manufacturers in the food industry.

Restraints

High Cost of Production and Raw Materials

A significant restraint in the food inclusions market is the high cost associated with producing and sourcing quality ingredients. This challenge is primarily driven by the expenses involved in procuring specialty items such as fruits, nuts, and high-quality chocolates, which are integral components of food inclusions. The cost factor extends not only to the acquisition of raw materials but also to the overall production process, impacting the final price of the food products. As a result, these higher costs can make the end products less accessible to budget-conscious consumers, potentially reducing market demand among this demographic.

Furthermore, fluctuations in the availability and price of these raw materials can exacerbate the issue. For instance, seasonal variations and geopolitical factors can lead to inconsistencies in supply chains, resulting in unstable pricing and availability of essential ingredients like nuts and fruits. Such volatility makes it challenging for food manufacturers to maintain consistent production costs and product pricing, ultimately affecting the market dynamics.

Additionally, the requirement to comply with stringent food safety and labeling regulations further adds to the production costs. Ensuring that food inclusions meet all regulatory standards for safety and transparency can require significant investment in both resources and time, which can be a substantial burden, particularly for smaller manufacturers.

These economic and regulatory challenges collectively act as a major restraint in the food inclusions market, influencing production strategies and pricing models, and potentially limiting the market’s growth in certain segments.

Opportunity

Growing Popularity of Functional and Nutrient-Dense Food Inclusions

A major growth opportunity in the food inclusions market is the rising consumer demand for functional foods that offer health benefits beyond basic nutrition. This trend is driving the incorporation of nutrient-dense ingredients such as proteins, fibers, vitamins, and minerals into various food products. Food inclusions like nuts, seeds, fruits, and grains are not only enhancing the flavor and texture of foods but are also providing essential nutrients, aligning with the consumer shift towards healthier eating habits.

The global food inclusions market is projected to expand significantly, with a forecasted market size of USD 23.84 billion by 2030, growing at a CAGR of 6.9% from 2024 to 2030. This growth is supported by innovations in food technology that allow for the development of new product lines with added health benefits. For instance, the incorporation of superfoods and antioxidant-rich ingredients caters to health-conscious consumers looking for snacks and meals that support a healthy lifestyle.

Moreover, the demand for clean label products—those made from natural ingredients and free of artificial additives—is also propelling the food inclusions market. Consumers are increasingly favoring products with transparent ingredient lists that are easy to understand and promise greater nutritional value. This shift is not only influencing consumer choices but also shaping product development strategies across the food industry.

The expanding range of applications of food inclusions across various segments like bakery products, dairy, snacks, and confections further underscores the versatility and potential for growth in this market. As manufacturers continue to innovate and cater to the evolving preferences of consumers, the food inclusions market is expected to witness robust growth and diversification in the coming years.

Trends

The Rise of Clean Label and Plant-Based Inclusions

A significant trend in the food inclusions market is the growing consumer demand for clean label and plant-based products. This trend is driven by increasing health consciousness among consumers and a desire for transparency in food labeling. Clean label products, which are free from artificial additives and chemicals, are becoming more popular, as consumers seek out food options that are both healthy and environmentally friendly.

The market is responding by incorporating more natural, organic, and plant-based ingredients into food products. These ingredients not only improve the nutritional profile of the foods but also align with consumer preferences towards sustainability and ethical sourcing. For instance, the use of plant-based proteins and natural sweeteners is on the rise, catering to the vegan and health-conscious markets.

This shift is also reflected in the industry’s innovation strategies, where there is an increased focus on developing new products that feature these clean and sustainable inclusions. These developments are not only seen in niche markets but are becoming mainstream as major players in the food industry adapt to these consumer demands.

Moreover, the market for these products is expected to continue growing, with significant expansions projected in the Asia-Pacific region, driven by both an increase in health awareness and economic growth which enable consumers to make more health-oriented food choices.

This trend towards clean label and plant-based food inclusions represents a pivotal shift in consumer preferences and is shaping the future of the food industry, offering opportunities for growth and innovation across global markets.

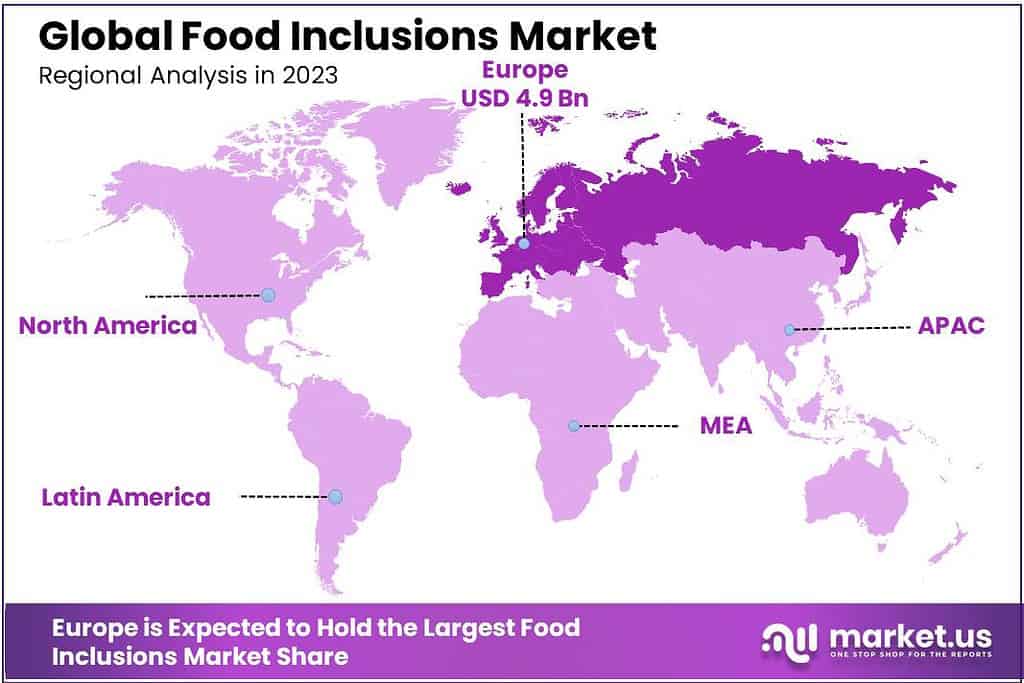

Regional Analysis

Europe leads the charge, commanding a 34.3% share of the global market, which translates to approximately USD 4.97 billion. This dominance is bolstered by strong demand for premium food products and the region’s stringent food quality and safety regulations, which encourage innovation in natural and clean label inclusions. European consumers are increasingly favoring gourmet food items with distinctive flavor profiles and high-quality ingredients, driving the market forward.

North America follows closely, characterized by a robust innovation pipeline and a high adoption rate of new food technologies. The market here is driven by consumers’ growing interest in health and wellness, which aligns with the rising demand for food products that contain natural and nutritional inclusions such as proteins and fibers.

In the Asia Pacific, the market is expanding rapidly, fueled by economic growth and an increasing middle-class population with disposable income to spend on enhanced food products. The region shows a strong inclination towards adopting Western eating habits, combined with a traditional preference for diverse flavors and textures, making it a dynamic area for the growth of food inclusions.

Middle East & Africa and Latin America are emerging markets with potential for growth due to changing consumer lifestyles and increased urbanization. These regions are experiencing a gradual shift towards convenience foods, which is expected to increase the demand for food inclusions that offer both convenience and nutrition.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Food Inclusions Market is characterized by the presence of several major players who are integral to its growth and innovation. Cargill, Incorporated and Archer Daniels Midland Company are two giants in the sector, widely recognized for their extensive product ranges that cater to varying consumer needs in the food and beverage industry. Both companies are pivotal in driving advancements in the market, particularly through their innovations in texture and flavor enhancement technologies.

Barry Callebaut AG and Tate & Lyle PLC are also key players, with Barry Callebaut leading in chocolate innovations and Tate & Lyle specializing in providing unique solutions that enhance taste and nutrition in food products. These companies, along with Agrana Beteiligungs-AG and Kerry Group plc, play significant roles in the market by focusing on the development of customized and specialty ingredients that respond to the clean label trend and consumer demand for natural products.

Other notable companies like Taura Natural Ingredients Limited, Nimbus Foods Ltd, and Sensient Technologies Corporation focus on niche markets and specific inclusion types, such as fruit pieces and flavor systems. Puratos Group NV and Inclusion Technologies LLC enhance the competitive landscape by offering unique bakery and confectionery solutions. Each of these companies contributes to the dynamism of the market, pushing forward with product innovations that meet evolving consumer preferences and regulatory standards in the food industry.

Market Key Players

- Cargill, Incorporated

- Archer Daniels Midland Company

- Barry Callebaut AG

- Tate & Lyle PLC

- Agrana Beteiligungs-AG

- Taura Natural Ingredients Limited

- Nimbus Foods Ltd

- SensoryEffects

- Kerry Group plc

- Sensient Technologies Corporation

- Puratos Group NV

- Inclusion Technologies LLC

Recent Development

In 2023 Cargill, Incorporated plays a significant role in the food inclusions market, especially in enhancing the nutritional and sensory qualities of food products.

In 2023, ADM demonstrated its commitment to strengthening its market position by targeting strategic areas of growth within the food inclusions sector, such as clean-label and plant-based products, aligning with global consumer trends towards healthier and more sustainable food options.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 14.5 Bn |

| Forecast Revenue (2033) | US$ 26.5 Bn |

| CAGR (2024-2033) | 6.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Chocolate, Fruits and Nuts, Cereal, Flavored Sugar and Caramel, Confectionery, Others), By Form(Solid and Semi-Solid, Liquid), By Application(Bakery Products, Snacks and Bar, Dairy and Frozen Desserts, Confectionery, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Cargill, Incorporated, Archer Daniels Midland Company, Barry Callebaut AG, Tate & Lyle PLC, Agrana Beteiligungs-AG, Taura Natural Ingredients Limited, Nimbus Foods Ltd, SensoryEffects, Kerry Group plc, Sensient Technologies Corporation, Puratos Group NV, Inclusion Technologies LLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

Food Inclusions Market size is expected to be worth around USD 26.5 billion by 2033, from USD 14.5 billion in 2023

Cargill, Incorporated, Archer Daniels Midland Company , Barry Callebaut AG, Tate & Lyle PLC, Agrana Beteiligungs-AG, Taura Natural Ingredients Limited, Nimbus Foods Ltd, SensoryEffects, Kerry Group plc, Sensient Technologies Corporation, Puratos Group NV, Inclusion Technologies LLC