Quick Navigation

Report Overview

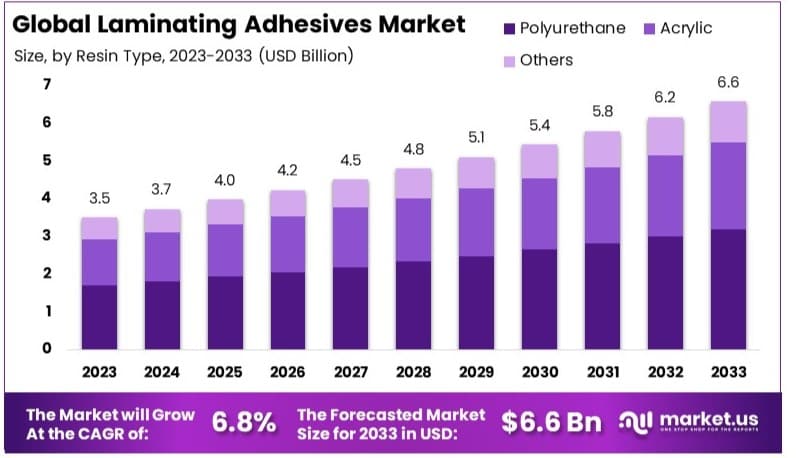

The Global Laminating Adhesives Market size is expected to be worth around USD 6.6 Billion by 2033, from USD 3.5 Billion in 2023, growing at a CAGR of 6.8% during the forecast period from 2024 to 2033.

The Laminating Adhesives Market refers to the industry involved in the production and sale of adhesives used for laminating applications. Laminating adhesives are critical in bonding multiple layers of materials to enhance strength, durability, and functionality. These adhesives are widely used in packaging, automotive, construction, and furniture industries.

The market includes various types of adhesives, such as solvent-based, water-based, and hot-melt adhesives. Innovations in adhesive technology are driven by the need for sustainable, eco-friendly solutions and the demand for high-performance adhesives.

The laminating adhesives market is experiencing robust growth, driven by rising demand in the packaging industry. Recent developments, such as Arkema’s acquisition of Dow’s flexible packaging laminating adhesives business for USD 150 million in May 2024, underscore the market’s expansion and increasing consolidation.

This strategic move allows Arkema to enhance its portfolio and strengthen its position in the flexible packaging market, which is witnessing significant growth due to the increasing use of flexible packaging solutions across various industries.

The growing popularity of flexible packaging is fueled by its advantages, such as lightweight, durability, and extended shelf life of products. Laminating adhesives play a crucial role in ensuring the performance and quality of these packaging solutions. As a result, the demand for high-performance laminating adhesives is on the rise.

Technological advancements in laminating adhesives are also contributing to market growth. Innovations aimed at improving adhesive properties, such as bond strength and resistance to environmental factors, are making laminating adhesives more effective and reliable. This, in turn, is driving their adoption in diverse applications, from food packaging to pharmaceuticals.

Environmental considerations are also shaping the laminating adhesives market. There is an increasing focus on developing eco-friendly adhesives that meet regulatory standards and consumer preferences for sustainable packaging solutions. Companies are investing in research and development to create products that reduce environmental impact while maintaining high performance.

The laminating adhesives market is poised for continued growth, supported by strategic acquisitions, technological advancements, and a shift towards sustainable packaging. As the demand for flexible packaging increases, the market for laminating adhesives is expected to expand, offering significant opportunities for industry stakeholders.

Key Takeaways

- Market Value: The Laminating Adhesives Market was valued at USD 3.5 billion in 2023, and is expected to reach USD 6.6 billion by 2033, with a CAGR of 6.8%.

- Resin Type Analysis: Polyurethane dominated with 48.6%; significant for its strong bonding and durability.

- Technology Analysis: Solvent-Based technology led with 51.6%; crucial for its wide applications and performance.

- End-Use Industry Analysis: Packaging dominated with 62.5%; essential for its extensive use in food, pharmaceuticals, and consumer products.

- Dominant Region: APAC held 41.2%; significant due to high manufacturing and packaging activities.

- Analyst Viewpoint: The laminating adhesives market is moderately competitive with strong growth potential. Future trends suggest increased demand in packaging and industrial applications.

- Growth Opportunities: Companies can leverage advancements in adhesive technologies and expand applications in emerging markets to enhance market presence.

Driving Factors

Increasing Demand in the Packaging Industry Drives Market Growth

The escalating use of laminating adhesives in the packaging industry is primarily fueled by the exponential growth of e-commerce platforms and evolving consumer preferences. With a significant shift towards online shopping, the demand for robust and visually appealing packaging has surged. Laminating adhesives are pivotal in producing multi-layered flexible packaging, which not only ensures product safety during transit but also extends shelf life and enhances aesthetic value.

The rise in packaging needs from major e-commerce platforms like Amazon and Alibaba has notably increased the consumption of these adhesives. This market segment is expected to expand as e-commerce continues to thrive globally, underpinning the continuous growth in demand for laminating adhesives.

Growth in Construction and Automotive Sectors Drives Market Growth

Laminating adhesives are experiencing robust demand from the construction and automotive industries. These adhesives are integral in manufacturing various components such as doors, windows, and furniture, adding enhanced durability and strength, which is essential in the construction sector. This demand is driven by increasing urbanization and a rising need for housing worldwide.

Similarly, in the automotive industry, the use of these adhesives in interior components aids in achieving lighter vehicle weights, which is crucial for fuel efficiency. Reports from companies like 3M and Henkel highlight a growth in adhesive sales, attributing this to the expansion of these sectors. This trend is projected to persist as urban development and automotive innovation continue to escalate.

Technological Advancements in Adhesive Formulations Drive Market Growth

Innovation in laminating adhesive formulations is a critical driver of market growth, with companies heavily investing in research and development. The introduction of new adhesive and sealants technologies such as water-based, solvent-free, and UV-curable adhesives presents multiple advantages, including reduced environmental impact, faster curing times, and broader compatibility with diverse substrates.

These improvements not only enhance the performance of adhesives but also meet the stringent environmental regulations increasingly implemented worldwide. For instance, Dow Chemical’s ADCOTE™ line of solvent-free adhesives has seen substantial market adoption due to its environmentally friendly attributes. This factor is pivotal as it supports industry compliance with regulatory standards and boosts the efficiency and appeal of laminating adhesives in various applications.

Restraining Factors

Volatile Raw Material Prices Restrain Market Growth

The fluctuating prices of raw materials such as ethylene and propylene, which are essential for producing laminating adhesives, significantly hinder market growth. These materials are derived from petrochemicals, making their costs susceptible to global economic shifts, geopolitical tensions, and crude oil price fluctuations.

For instance, during the COVID-19 pandemic in 2020, a drastic decline in oil prices was observed, followed by a sharp increase in 2021 due to tightened supply. This unpredictability affects adhesive manufacturers like Arkema and BASF, as they struggle to maintain stable profit margins amidst these swings. The inability to predict and manage costs effectively can lead to reduced competitiveness and financial strain, particularly for those heavily reliant on such volatile inputs.

Stringent Environmental Regulations Restrain Market Growth

Increasingly strict environmental regulations pose significant challenges to the growth of the laminating adhesives market. Governments across the globe are tightening rules on the use of volatile organic compounds (VOCs) and hazardous air pollutants (HAPs), which are commonly found in traditional solvent-based adhesives.

Adhering to these regulations necessitates substantial investment in research and development to create eco-friendly alternatives, as well as modifications to existing production facilities. This regulatory pressure is especially burdensome for smaller companies with limited resources. For example, the EU’s REACH regulations have compelled many manufacturers to overhaul their product formulations to meet new standards, adding financial and operational pressures that limit market expansion and innovation.

Resin Type Analysis

Polyurethane dominates with 48.6% due to its strong bonding and versatility

The Laminating Adhesives Market is segmented by resin type into Polyurethane, Acrylic, and others. Polyurethane leads the market, holding 48.6% of the market share. This dominance is due to its strong bonding capabilities, versatility, and durability.

Polyurethane laminating adhesives are highly preferred for their excellent adhesion to various substrates, including plastics, metals, and paper. They provide strong, flexible bonds that can withstand harsh environmental conditions. This makes them ideal for use in the packaging industry, particularly for food and beverage packaging, where safety and durability are paramount.

The significant market share of Polyurethane is driven by its widespread application in flexible packaging, which demands adhesives that can maintain integrity under various conditions such as heat, moisture, and mechanical stress. Additionally, polyurethane adhesives are crucial in the automotive and transportation industries for laminating interior components and ensuring long-lasting bonds.

Acrylic adhesives, while effective, hold a smaller market share compared to polyurethane. Acrylics are known for their clarity, UV resistance, and quick setting times, making them suitable for applications where these properties are essential, such as in transparent films and labels. However, their use is more limited in heavy-duty applications due to lower strength and flexibility compared to polyurethane.

Other resin types, including epoxy and silicone adhesives, cater to niche applications requiring specific properties like high-temperature resistance or chemical stability. Although these adhesives are crucial for certain industrial applications, their overall market share remains smaller due to higher costs and limited versatility.

Technology Analysis

Solvent-Based dominates with 51.6% due to strong bonding and quick drying

The Laminating Adhesives Market is segmented by technology into Solvent-Based, Water-Based, Solvent-less, and others. Solvent-Based adhesives lead with a 51.6% market share, driven by their strong bonding capabilities and quick drying times.

Solvent-Based laminating adhesives are preferred for their ability to provide robust bonds that withstand harsh conditions. They are widely used in the packaging industry, especially for flexible packaging applications. The quick drying times and strong adhesion make them ideal for high-speed manufacturing processes, which is crucial for maintaining efficiency and productivity in packaging operations.

The dominance of Solvent-Based adhesives is also attributed to their excellent performance on a variety of substrates, including films, foils, and papers. This versatility makes them suitable for a broad range of applications, from food and beverage packaging to pharmaceutical products.

Water-Based adhesives, while environmentally friendly and safer to use, hold a smaller market share compared to Solvent-Based adhesives. They are increasingly popular due to their low volatile organic compound (VOC) emissions and ease of handling. However, their longer drying times and potential performance issues in high-humidity conditions limit their use in certain applications.

Solvent-less adhesives are gaining traction due to their eco-friendly nature and reduced environmental impact. They eliminate the need for solvents, reducing VOC emissions and improving safety for workers. These adhesives are used in applications where environmental regulations are stringent, and sustainability is a priority. Despite their benefits, higher costs and specific application requirements limit their broader adoption.

Other adhesive technologies, including hot melt and UV-curable adhesives, serve niche markets with unique requirements. While they offer specific advantages like rapid curing and high strength, their overall market share remains smaller due to higher costs and specialized application processes.

End-Use Industry Analysis

Packaging dominates with 62.5% due to high demand in food and beverage sectors

The Laminating Adhesives Market is segmented by end-use industry into Packaging, Industrial, and Automotive & Transportation. Packaging leads with a 62.5% market share, driven by high demand in the food and beverage sectors.

In the Packaging industry, laminating adhesives are essential for creating durable, flexible packaging solutions that protect products and extend shelf life. The food and beverage sector, in particular, relies heavily on laminating adhesives to ensure packaging integrity, prevent contamination, and maintain freshness. The increasing demand for convenience foods and packaged beverages further boosts the market for laminating adhesives in this segment.

Pharmaceutical packaging is another significant area within the packaging industry. Laminating adhesives are used to ensure the safety and security of pharmaceutical products, providing tamper-evident seals and protecting against moisture and contamination. The growing pharmaceutical industry, driven by increasing healthcare needs, further enhances the demand for laminating adhesives.

The Industrial segment includes applications such as insulation, window films, and electronics. Laminating adhesives in this segment are used to enhance product durability, provide thermal insulation, and improve energy efficiency. While the market share in this segment is smaller compared to packaging, the demand is steady due to ongoing industrial development and the need for high-performance materials.

In the Automotive & Transportation industry, laminating adhesives are used for interior and exterior applications. They provide strong bonds for laminating various components, such as dashboards, door panels, and trim. The demand for lightweight and durable materials in vehicle manufacturing drives the use of laminating adhesives in this sector. Although the market share is smaller, the potential for growth is significant as the automotive industry continues to innovate and adopt new materials.

Key Market Segments

By Resin Type

- Polyurethane

- Acrylic

- Others

By Technology

- Solvent-Based

- Water-Based

- Solvent-less

- Others

By End-use Industry

- Packaging

- Food & Beverages

- Pharmaceuticals

- Consumer Products

- Industrial

- Insulation

- Window Films

- Electronics

- Others

- Automotive & Transportation

Growth Opportunities

Bio-Based Laminating Adhesives Offer Growth Opportunity

The shift towards sustainability globally is significantly increasing the demand for bio-based laminating adhesives. These adhesives, sourced from renewable materials like soy, corn, or sugarcane, present an eco-friendly alternative to conventional petroleum-based products. This not only helps companies align with environmental goals but also caters to the growing segment of eco-conscious consumers.

DuPont’s Biomaterials division, for example, has successfully utilized bio-based adhesives in sectors such as food packaging and personal care, showcasing their practical application and market acceptance. The trend towards sustainability is expected to propel the demand for such adhesives, presenting a substantial growth opportunity within the market.

Smart Packaging Solutions Offer Growth Opportunity

The integration of smart technologies like RFID, NFC, and QR codes into packaging has created a burgeoning demand for specialized laminating adhesives. These adhesives are crucial for securely attaching smart elements to packages without compromising their integrity. This technology trend is primarily driven by the increasing needs for supply chain transparency, anti-counterfeiting measures, and improved consumer interaction.

Avery Dennison’s intelligent labeling solutions demonstrate the successful application of these adhesives in enhancing brand protection and customer engagement, as seen with luxury brands such as Moncler. The ongoing advancement and adoption of smart packaging technologies present a significant growth opportunity for the laminating adhesives market.

Trending Factors

Customization and Technical Support Are Trending Factors

The demand for customized adhesive solutions tailored to specific industrial applications is a major trend shaping the laminating adhesives market. Industries such as electronics and aerospace often require adhesives that are not only effective but also specifically formulated for unique environmental and technical demands.

This trend has led manufacturers like LORD Corporation (now part of Parker Hannifin) to offer comprehensive services including custom formulations, on-site technical support, and specialized application equipment. This approach not only enhances product performance but also strengthens customer relationships by providing tailored solutions and expert assistance. As industries continue to evolve with complex requirements, the demand for such personalized services and products is expected to rise, highlighting a significant growth avenue within the market.

Mergers and Acquisitions Are Trending Factors

Mergers and acquisitions (M&A) have become strategic moves for companies aiming to enhance their market position and expand their product portfolios within the laminating adhesives market. This consolidation enables companies to access new technologies, markets, and distribution channels, which is crucial for staying competitive.

An example of this strategy is H.B. Fuller’s acquisition of Royal Adhesives & Sealants in 2017, which not only expanded its reach in the high-growth markets of engineering adhesives, including those used in electronics and transportation but also reinforced its technological capabilities and industry footprint. The trend of M&A is anticipated to continue as companies strive to meet the expanding scope of application needs and global market demands, making it a significant factor driving market dynamics and opportunities.

Regional Analysis

Asia-Pacific Dominates with 41.2% Market Share in the Laminating Adhesives Market

Asia-Pacific’s significant market share of 41.2% in the laminating adhesives market is primarily driven by its expansive manufacturing sectors, particularly in packaging, automotive, and electronics. The presence of large-scale manufacturing hubs in China, India, and Japan, coupled with the increasing demand for high-quality laminating adhesives in these applications, significantly contributes to the region’s dominance.

The region benefits from a combination of advanced manufacturing technologies, skilled labor, and lower production costs, which collectively enhance its competitive edge. Additionally, the growing consumer markets within the region increase the demand for packaged goods, further driving the need for effective laminating solutions. Government initiatives aimed at promoting industrial growth and sustainable manufacturing practices also play a crucial role in market expansion.

The forecast for Asia-Pacific in the laminating adhesives market remains positive. The ongoing expansion of the packaging and automotive sectors, coupled with advancements in adhesive technologies, suggests that the region will not only maintain but potentially increase its market share. Continued economic growth and urbanization are likely to fuel further demand, ensuring that Asia-Pacific remains at the forefront of the global market.

Regional Market Shares and Dynamics:

- North America: North America holds approximately 27.8% of the market. The region’s strong emphasis on sustainable and innovative adhesive solutions, particularly for the packaging and automotive industries, supports steady market growth.

- Europe: Europe accounts for about 24.1% of the market share, driven by stringent environmental regulations and high standards for product safety and quality. The demand in Europe is bolstered by the region’s advanced manufacturing base and focus on eco-friendly products.

- Middle East & Africa: This region captures a smaller market share of 2.1%, with potential growth driven by increasing industrialization and investment in manufacturing sectors.

- Latin America: Latin America holds a 4.8% market share. The region is experiencing gradual growth in industrial and packaging sectors, which are beginning to adopt more sophisticated manufacturing techniques, including the use of laminating adhesives.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The Laminating Adhesives Market features prominent players like Henkel AG & Co. KGaA, 3M Company, and Dow Chemical Company, which dominate due to their extensive product lines and global reach. These companies leverage advanced technology and R&D to maintain their market positions.

H.B. Fuller Company, Bostik, and Ashland Global Holdings Inc. also hold significant shares. They focus on product innovation and strategic acquisitions to expand their market presence. Sika AG and Avery Dennison Corporation utilize strong distribution networks and diversified portfolios to enhance their competitive edge.

Arkema S.A., Parker Hannifin Corporation, and Eastman Chemical Company impact the market through their specialized adhesive solutions, catering to diverse industries. Toyo-Morton, Ltd. and Wacker Chemie AG emphasize sustainable and high-performance products, meeting growing eco-friendly demands.

DIC Corporation and Vimasco Corporation, though smaller, influence niche segments with tailored solutions and customer-centric approaches. Collectively, these key players drive market growth through innovation, strategic alliances, and a focus on sustainability, shaping the competitive landscape of the Laminating Adhesives Market.

Market Key Players

- Henkel AG & Co. KGaA

- 3M Company

- Dow Chemical Company

- H.B. Fuller Company

- Bostik

- Ashland Global Holdings Inc.

- Sika AG

- Avery Dennison Corporation

- Arkema S.A.

- Parker Hannifin Corporation

- Eastman Chemical Company

- Toyo-Morton, Ltd.

- Wacker Chemie AG

- DIC Corporation

- Vimasco Corporation

Recent Developments

- May 2024: Arkema to acquire Dow’s flexible packaging laminating adhesives business for $150 million, expanding its portfolio and presence in the growing flexible packaging market.

- June 2022: Toyomorton launches epoxy-silane-free laminating adhesives, offering a more sustainable alternative for the packaging industry.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 3.5 Billion |

| Forecast Revenue (2033) | USD 6.6 Billion |

| CAGR (2024-2033) | 6.8% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Resin Type (Polyurethane, Acrylic, Others), By Technology (Solvent-Based, Water-Based, Solvent-less, Others), By End-Use Industry (Packaging: Food & Beverages, Pharmaceuticals, Consumer Products; Industrial: Insulation, Window Films, Electronics, Others; Automotive & Transportation) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Henkel AG & Co. KGaA, 3M Company, Dow Chemical Company, H.B. Fuller Company, Bostik, Ashland Global Holdings Inc., Sika AG, Avery Dennison Corporation, Arkema S.A., Parker Hannifin Corporation, Eastman Chemical Company, Toyo-Morton, Ltd., Wacker Chemie AG, DIC Corporation, Vimasco Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The Global Laminating Adhesives Market was valued at USD 3.5 billion in 2023.

The market includes solvent-based, water-based, and hot-melt adhesives.

Asia-Pacific holds the largest laminating adhesives market share at 41.2%, driven by extensive manufacturing activities.

Key players include Henkel AG & Co. KGaA, 3M Company, Dow Chemical Company, H.B. Fuller Company, Bostik, and Ashland Global Holdings Inc.