Global Mobile Gamma Cameras Market By Product Type (Single Head, Triple Head, Double Head and Hand Held), By Indications (Cardiac Imaging, Renal Imaging, Breast Imaging, Brain Imaging and Others), By End Users (Hospitals, Cancer Research Institutes, Ambulatory Surgical Centers and Specialized Clinics), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179729

- Number of Pages: 304

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

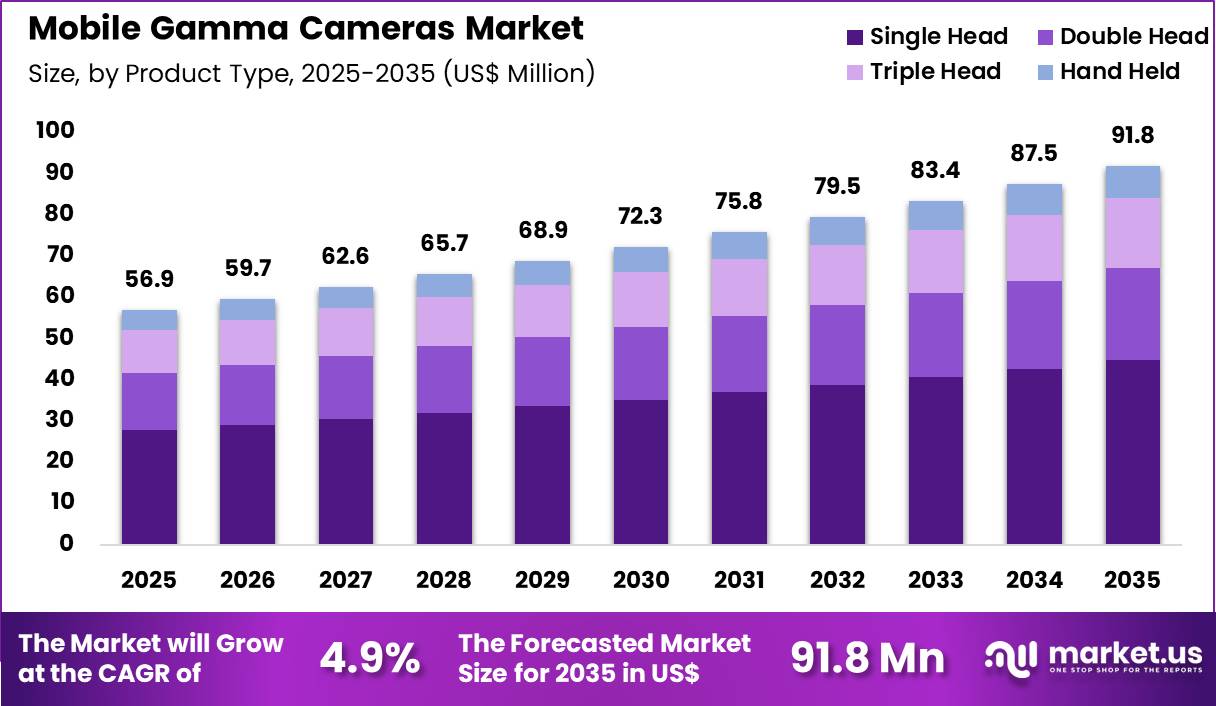

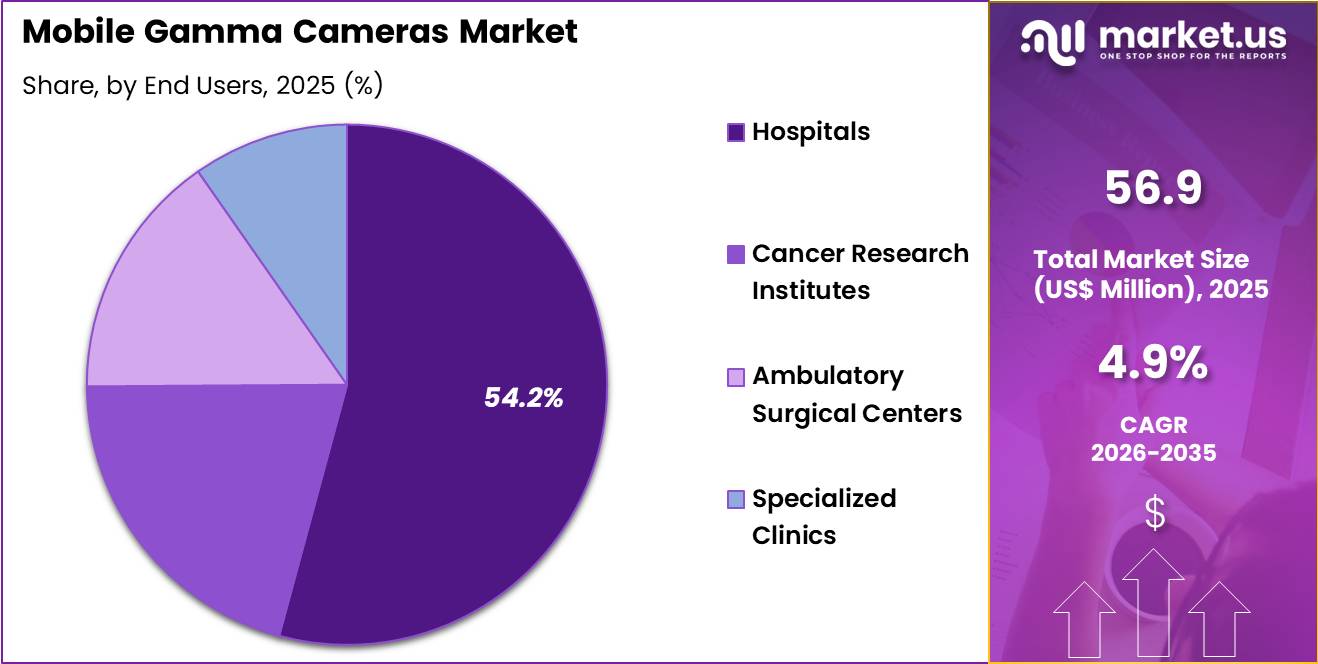

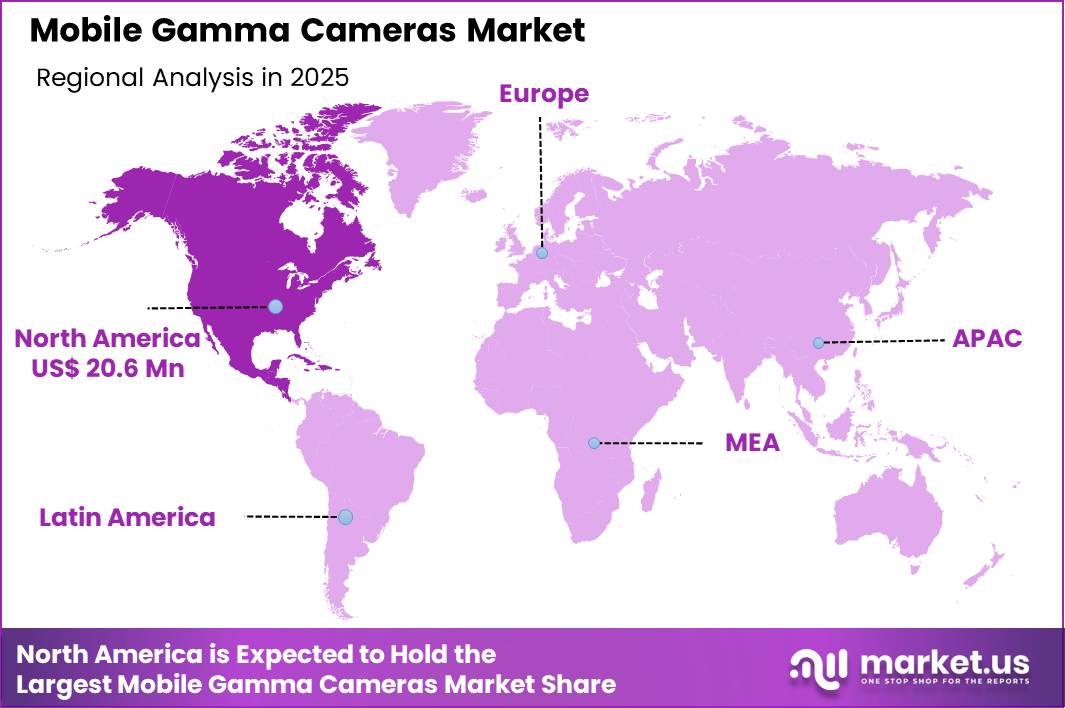

The Global Mobile Gamma Cameras Market size is expected to be worth around US$ 91.8 Million by 2035 from US$ 56.9 Million in 2025, growing at a CAGR of 4.9% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 36.2% share with a revenue of US$ 20.6 Million.

Increasing demand for portable diagnostic imaging in critical care settings propels the mobile gamma cameras market as healthcare providers seek flexible solutions that deliver high-resolution scintigraphic images without patient transport.

Clinicians increasingly utilize these devices in intensive care units to perform bedside myocardial perfusion scans, assessing cardiac ischemia in unstable patients where traditional fixed cameras prove impractical. These cameras support intraoperative applications during sentinel lymph node biopsies in breast cancer surgeries, enabling real-time localization of radioactive tracers to guide precise excision and staging.

Emergency departments apply mobile gamma cameras for rapid thyroid uptake studies in hyperthyroidism cases or bone scans for suspected fractures in trauma patients, facilitating quicker diagnosis and treatment initiation.

Oncology teams employ them for dynamic renal function assessments in chemotherapy monitoring, tracking glomerular filtration rates without disrupting patient mobility. Veterinary practices also adopt these systems for equine skeletal imaging, detecting stress fractures in performance animals during on-site evaluations.

Manufacturers pursue opportunities to integrate artificial intelligence algorithms that automate image reconstruction and artifact correction, expanding applications in hybrid operating rooms where gamma cameras combine with surgical navigation for enhanced tumor margin delineation.

Developers advance lightweight, battery-powered models with extended scan times, broadening utility in ambulatory clinics for routine parathyroid imaging and lymphoscintigraphy. These innovations facilitate wireless data transfer to cloud platforms, supporting remote consultations in multidisciplinary tumor boards.

Opportunities emerge in sustainable designs using recyclable components and low-energy detectors, appealing to eco-conscious facilities. Companies invest in multi-modal fusion capabilities that overlay gamma images with ultrasound or CT data, improving accuracy in interventional procedures.

Recent trends emphasize user-friendly interfaces with voice-activated controls and augmented reality overlays, positioning the market for growth in patient-centered, efficient diagnostic workflows across acute and chronic care scenarios.

Key Takeaways

- In 2025, the market generated a revenue of US$ 56.9 Million, with a CAGR of 4.9%, and is expected to reach US$ 91.8 Million by the year 2035.

- The product type segment is divided into single head, triple head, double head and hand held, with single head taking the lead with a market share of 48.7%.

- Considering indications, the market is divided into cardiac imaging, renal imaging, breast imaging, brain imaging and others. Among these, cardiac imaging held a significant share of 42.9%.

- Furthermore, concerning the end users segment, the market is segregated into hospitals, cancer research institutes, ambulatory surgical centers and specialized clinics. The hospitals sector stands out as the dominant player, holding the largest revenue share of 54.2% in the market.

- North America led the market by securing a market share of 36.2%.

Product Type Analysis

Single head mobile gamma cameras accounted for 48.7% of growth within product type and dominate due to their cost-effectiveness, portability, and versatility in routine nuclear medicine imaging. Hospitals and diagnostic centers prefer single head systems for cardiac and renal imaging as they provide reliable performance with lower acquisition and maintenance costs compared to multi-head systems.

Segment growth is projected to strengthen as smaller hospitals, outpatient facilities, and remote diagnostic centers expand nuclear imaging services. Technological advancements in detector sensitivity, image resolution, and digital integration improve diagnostic accuracy and workflow efficiency.

Growing awareness of early disease detection and rising prevalence of cardiovascular and renal disorders drive adoption. Manufacturers focus on compact, lightweight designs with faster acquisition times, supporting point-of-care diagnostics. The segment is anticipated to benefit from government initiatives promoting diagnostic accessibility in emerging regions and outpatient care facilities.

Indications Analysis

Cardiac imaging accounted for 42.9% of growth within indications and dominates the market due to the increasing prevalence of cardiovascular diseases worldwide. Hospitals implement cardiac imaging programs for early detection, risk assessment, and therapeutic monitoring.

Segment growth is expected to continue as advanced imaging protocols improve accuracy in myocardial perfusion studies and functional assessments. Mobile gamma cameras allow bedside imaging, reducing patient transfer and enhancing workflow efficiency.

Rising incidence of coronary artery disease, heart failure, and other cardiovascular conditions drives demand for non-invasive, real-time diagnostics. Expansion of preventive cardiology programs, coupled with reimbursement support, strengthens adoption. Manufacturers focus on optimized software for cardiac quantification and hybrid imaging integration, further enhancing segment growth.

End-User Analysis

Hospitals accounted for 54.2% of growth within end users and dominate due to their high patient throughput, specialized nuclear medicine departments, and comprehensive imaging capabilities. Hospitals provide centralized access to trained personnel, radiopharmaceuticals, and supportive diagnostic infrastructure.

Segment growth is projected to continue as hospitals expand cardiac, renal, and oncologic imaging services. Collaborations with manufacturers for training, maintenance, and equipment upgrades support adoption.

The increasing emphasis on early diagnosis, outpatient care integration, and bedside imaging further enhances demand. Hospitals in developed regions lead in adoption, while emerging markets present growth opportunities through government healthcare investments and private sector expansion.

Key Market Segments

By Product Type

- Single Head

- Triple Head

- Double Head

- Hand Held

By Indications

- Cardiac Imaging

- Renal Imaging

- Breast Imaging

- Brain Imaging

- Others

By End Users

- Hospitals

- Cancer Research Institutes

- Ambulatory Surgical Centers

- Specialized Clinics

Drivers

Rising demand for portable nuclear imaging in emergency and critical care is driving the market.

The growing need for immediate nuclear imaging at the bedside in emergency departments, intensive care units, and trauma centers has significantly increased the demand for mobile gamma cameras. These systems enable rapid assessment of organ function without transporting critically ill patients. Healthcare facilities are prioritizing portable solutions to support timely diagnosis in acute settings.

The correlation between time-sensitive conditions and the requirement for on-site imaging further amplifies adoption. Government health guidelines emphasize efficient diagnostic workflows in high-acuity environments. Mobile gamma cameras provide flexibility for imaging in confined spaces or during transport.

National emergency care protocols highlight the importance of rapid nuclear medicine capabilities. Key manufacturers are developing lightweight, battery-operated systems to meet this clinical imperative. This driver encourages innovation in detector design and user interfaces. The need for portable nuclear imaging in emergency and critical care settings is a primary market driver.

Restraints

High acquisition and maintenance costs are restraining the market.

The substantial purchase price of mobile gamma cameras, including detectors and software, limits their adoption in facilities with constrained capital budgets. Complex engineering for portability, radiation shielding, and image quality contributes to elevated manufacturing expenses.

Smaller hospitals and regional centers often defer acquisition due to competing equipment priorities. Regulatory requirements for radiation safety certification add to the total ownership cost. In public health systems, funding allocations favor stationary imaging systems over mobile units. Providers must balance diagnostic advantages against long-term maintenance expenses.

This restraint is particularly pronounced in low-resource environments. Industry efforts to offer refurbished or shared-use models provide partial mitigation. Despite mobility benefits, cost barriers slow replacement cycles and technological refreshment. High acquisition and maintenance costs remain a key market restraint.

Opportunities

Expansion of nuclear medicine services in outpatient and ambulatory settings is creating growth opportunities.

The increasing establishment of outpatient nuclear medicine centers presents avenues for mobile gamma cameras to support flexible imaging in non-hospital environments. Governmental policies promoting ambulatory care reimbursement encourage the deployment of portable systems in standalone facilities.

Rising demand for convenient diagnostic services amplifies potential for mobile units in community-based care. Partnerships with outpatient networks facilitate customized configurations for high-throughput clinics. The large volume of routine nuclear procedures in ambulatory settings magnifies prospects for device utilization.

Educational programs for nuclear medicine technologists promote standardized use in outpatient workflows. This opportunity enables manufacturers to diversify beyond inpatient applications. Leading companies are developing compact systems optimized for ambulatory use.

Overall, outpatient expansion aligns with efforts to improve access and reduce hospital burden. The expansion of nuclear medicine services in outpatient and ambulatory settings is a key growth opportunity.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic shifts shape the mobile gamma cameras market as hospital budgets tighten and healthcare providers reassess capital expenditures. Rising interest rates and inflation increase the cost of acquiring advanced imaging systems, slowing expansion in smaller clinics. Geopolitical instability affects the supply of isotopes, detectors, and high-precision components, creating uncertainty in production and delivery.

US tariffs on imported devices and electronic parts raise overall equipment costs, which can strain procurement decisions. These pressures challenge smaller facilities and slow adoption in cost-sensitive areas. On the positive side, trade barriers encourage local assembly, service networks, and domestic partnerships for isotope production.

The increasing reliance on gamma imaging for oncology and cardiac diagnostics drives steady demand. With strategic investments and service-focused solutions, the market remains positioned for long-term growth.

Latest Trends

Integration of solid-state detectors in mobile gamma cameras is a recent trend in the market.

In 2024, the adoption of solid-state detectors in mobile gamma cameras has improved portability and image quality while reducing system weight and power consumption. These detectors replace traditional photomultiplier tubes, enabling more compact designs suitable for bedside use. Manufacturers have prioritized energy resolution and count rate performance in solid-state configurations.

Clinical evaluations in 2024 confirmed superior sensitivity for low-dose imaging protocols. The integration of solid-state detectors represents a major trend in mobile gamma camera technology. This advancement addresses longstanding limitations in traditional crystal-based systems. The trend emphasizes battery efficiency for extended operation in clinical environments.

Regulatory clearances in 2024 for solid-state mobile systems have accelerated deployment. Industry collaborations optimize detector arrays for better spatial resolution. These innovations aim to expand applications while maintaining diagnostic reliability in point-of-care nuclear imaging.

Regional Analysis

North America is leading the Mobile Gamma Cameras Market

North America captured 36.2% of the mobile gamma cameras market in 2024 as healthcare systems expanded use of portable nuclear imaging solutions across inpatient, outpatient, and point‑of‑care settings. Hospitals and diagnostic centers reported more than 450 new gamma camera unit installations in the U.S. in 2023, many of which were mobile or hybrid models that improve flexibility for cardiology, oncology, and thyroid imaging outside fixed imaging suites, reinforcing clinical reach and workflow efficiency.

Patient demand for rapid, high‑quality functional imaging grew alongside rising prevalence of chronic conditions, compelling facilities to adopt mobile systems that reduce wait times and support bedside evaluation. Advances in digital detector technology and integration with clinical software strengthened image clarity and diagnostic confidence, particularly in high‑volume emergency and surgical environments.

Reimbursement policies in the U.S. and Canada increasingly accommodated use of portable imaging technologies, reducing financial barriers for hospitals to invest. Training initiatives helped clinical professionals leverage mobile gamma imaging across specialties, broadening practical applications.

Collaborations between equipment manufacturers and major health networks improved distribution and service support, accelerating adoption. Telehealth programs incorporated mobile imaging to better serve remote and underserved populations. These drivers collectively sustained robust growth of mobile nuclear imaging adoption throughout the region.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Healthcare delivery across Asia Pacific is expected to strengthen over the forecast period as rising chronic disease burdens and substantial investments in diagnostic imaging infrastructure elevate demand for advanced functional imaging technologies.

In China and neighboring markets, nuclear imaging adoption has increased significantly, supported by broader implementation of technologies such as SPECT and hybrid imaging systems that often rely on flexible, compact gamma imaging solutions and recorded a 22% increase in gamma camera installations in the region from 2023 to 2024, underscoring expanding clinical capacity.

Rapid expansion of hospitals and multi‑specialty diagnostic centers improved access to imaging services, especially in urban and peri‑urban areas, while government initiatives financed equipment acquisition in emerging markets. Rising population aging trends and higher incidence of cardiovascular disease and cancer heightened the urgency for accessible imaging across the care continuum.

Local manufacturers and service providers tailored solutions to regional clinical needs and cost sensitivities, enhancing uptake in cost‑conscious settings. Cross‑border partnerships and technical training programs helped build clinical expertise in nuclear imaging practices.

Outpatient care providers and mobile service units leveraged portable imaging to shorten referral times and improve patient throughput. Integrated healthcare networks in countries such as India, Japan, and South Korea optimized imaging workflows, supporting broader use of mobile and hybrid gamma systems. Collectively, these factors are positioned to drive sustained growth across Asia Pacific in the years ahead.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Leading companies in the portable nuclear imaging sector focus on expanding their global footprint through strategic partnerships, targeted product launches, and investment in advanced imaging technology. They actively enhance service networks and provide training programs to boost adoption in hospitals and specialized clinics.

Siemens Healthineers, a prominent player, develops innovative diagnostic solutions and maintains a strong presence across North America, Europe, and Asia. The company emphasizes research-driven product improvements and digital integration to meet evolving clinical needs.

Additionally, these firms pursue acquisitions of niche imaging technology providers to diversify offerings and strengthen market share. Collaborative initiatives with healthcare institutions further allow them to demonstrate clinical efficacy and build long-term client relationships.

Top Key Players

- GE HealthCare

- Siemens Healthineers

- Philips Healthcare

- Digirad Corporation

- DDD-Diagnostic A/S

- Spectrum Dynamics Medical

- Mediso Medical Imaging Systems

- Neusoft Medical Systems

- Crystal Photonics

- Gamma Medica

Recent Developments

- In September 2025, Digirad Corporation launched the Cardius-3, a mobile triple-head gamma camera designed specifically for cardiac imaging. With high-count imaging capabilities, the system serves hospitals, imaging centers, and physician offices, reinforcing Digirad’s position as a provider of specialized cardiovascular imaging solutions.

- In 2025, GE HealthCare partnered with NVIDIA to integrate advanced edge AI into its imaging systems. This collaboration aims to shorten scan times and enhance image reconstruction, improving diagnostic performance for portable and point-of-care scanners, especially in bedside and high-acuity clinical settings.

Report Scope

Report Features Description Market Value (2025) US$ 56.9 Million Forecast Revenue (2035) US$ 91.8 Million CAGR (2026-2035) 4.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Single Head, Triple Head, Double Head and Hand Held), By Indications (Cardiac Imaging, Renal Imaging, Breast Imaging, Brain Imaging and Others), By End Users (Hospitals, Cancer Research Institutes, Ambulatory Surgical Centers and Specialized Clinics) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape GE HealthCare, Siemens Healthineers, Philips Healthcare, Digirad Corporation, DDD-Diagnostic A/S, Spectrum Dynamics Medical, Mediso Medical Imaging Systems, Neusoft Medical Systems, Crystal Photonics, Gamma Medica Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Mobile Gamma Cameras MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Mobile Gamma Cameras MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- GE HealthCare

- Siemens Healthineers

- Philips Healthcare

- Digirad Corporation

- DDD-Diagnostic A/S

- Spectrum Dynamics Medical

- Mediso Medical Imaging Systems

- Neusoft Medical Systems

- Crystal Photonics

- Gamma Medica

Our Clients

- 179729

- Feb 2026