Quick Navigation

Report Overview

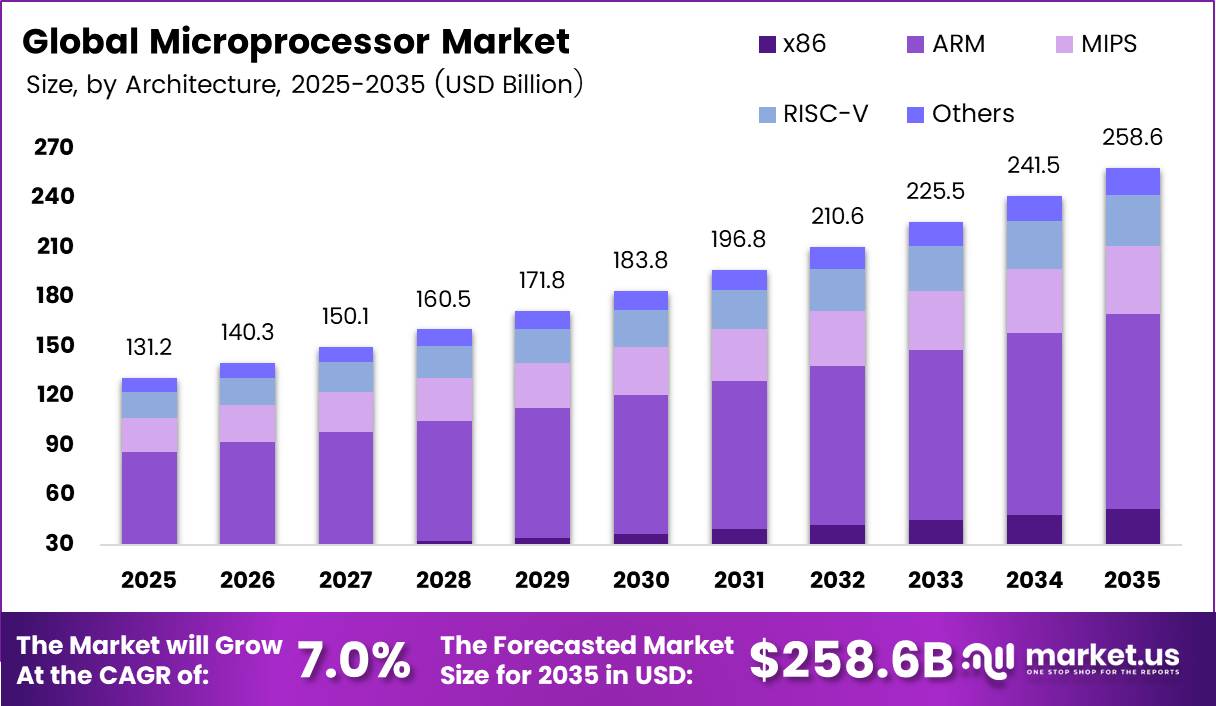

Global Microprocessor Market size is expected to be worth around USD 258.6 Billion by 2035 from USD 131.2 Billion in 2025, growing at a CAGR of 7.00% during the forecast period 2026 to 2035.

The microprocessor market encompasses the design, fabrication, and sale of programmable silicon logic devices that execute instructions across computing platforms. This includes CPUs, SoCs, and embedded processors serving data centers, consumer electronics, automotive systems, industrial automation, and healthcare equipment. The market spans multiple architecture families and core configurations across diverse end-use verticals.

Key Takeaways

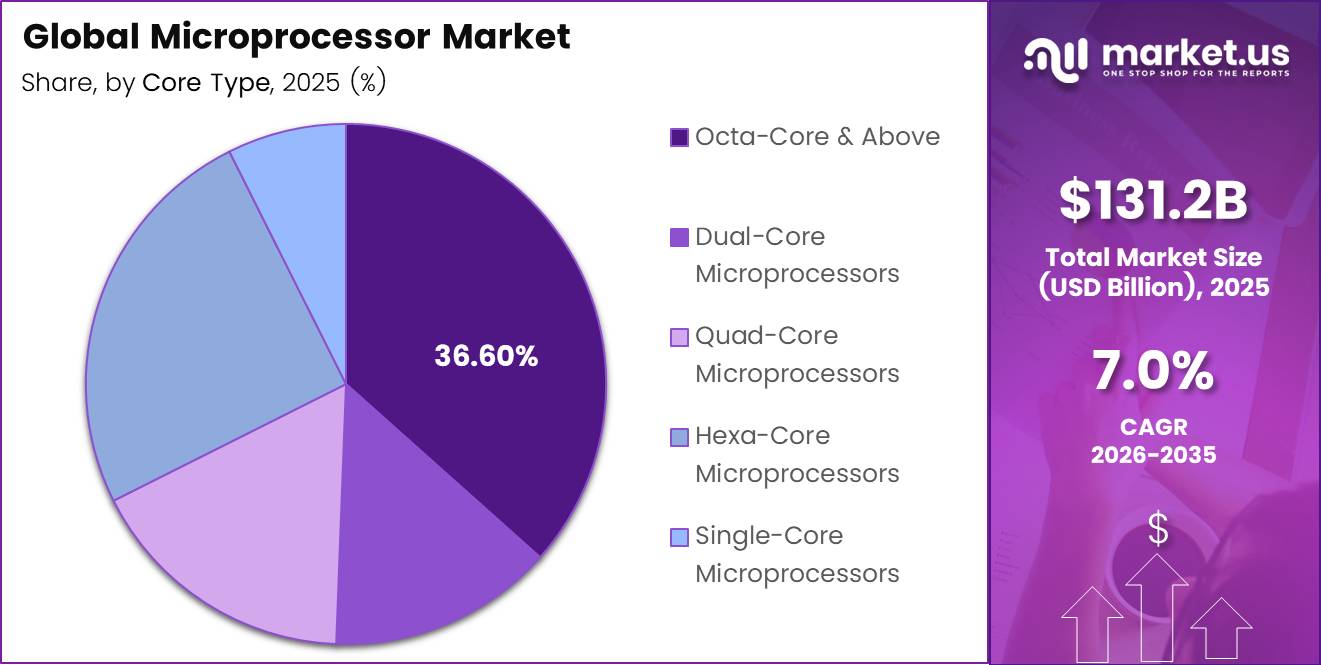

- The global Microprocessor Market is valued at USD 131.2 Billion in 2025 and is forecast to reach USD 258.6 Billion by 2035.

- The market grows at a CAGR of 7.00% during the forecast period 2026 to 2035.

- By Architecture, ARM dominates with a 45.60% share in 2025.

- By Core Type, Octa-Core and Above leads with a 36.60% share in 2025.

- By Bit Size, 64-bit processors hold the dominant share at 60.70% in 2025.

- By End Use Industry, Consumer Electronics holds the largest share at 34.60% in 2025.

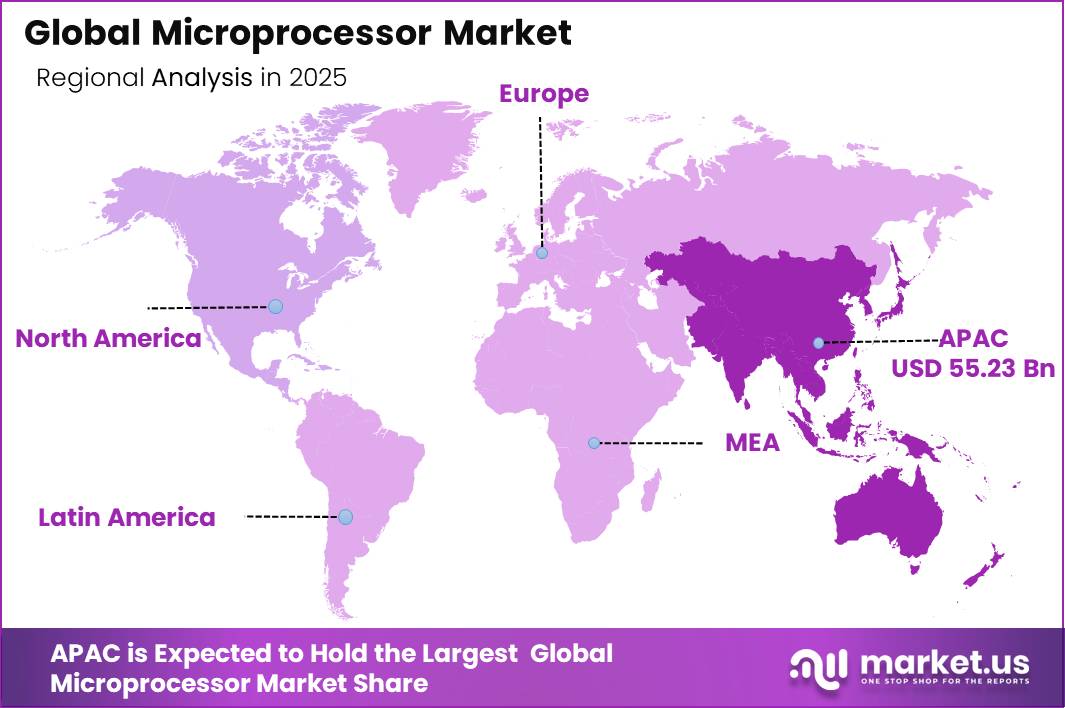

- Asia Pacific dominates the global market with a 42.10% share, valued at USD 55.24 Billion in 2025.

Sovereign chip programs across the US, European Union, and India are actively reshaping the geographic footprint of microprocessor fabrication. Government-backed initiatives including the CHIPS Act, EU Chips Act, and India Semiconductor Mission are directing capital toward domestic fab capacity. This policy push creates structural demand for regionally sourced processors outside the traditional Taiwan-centric supply model.

According to RISC-V International, RISC-V market penetration is projected to grow from 2.5% in 2021 to 33.7% by 2031. This trajectory reflects a decisive shift toward royalty-free architecture licensing. Vendors entering IoT and embedded segments now face a cost-competitive alternative that can undercut ARM-licensed designs on total program cost.

Data from NVIDIA’s Q1 FY2027 earnings shows its data center revenue reached a record USD 75.2 Billion on an annualized basis, rising 92% year-over-year. This validates the data center as the highest-velocity demand channel in the broader microprocessor ecosystem. In January 2026, Microsoft’s CES 2026 showcase featured OEM launches of Copilot+ PCs using Intel Core Ultra Series 3 processors, confirming commercial ramp-up of AI-capable client microprocessor platforms across consumer and enterprise segments.

Architecture Analysis

ARM dominates with 45.60% due to mobile and embedded design efficiency advantages.

In 2025, ARM held a dominant market position in the By Architecture segment of the Microprocessor Market, with a 45.60% share. ARM’s dominance reflects its energy-efficient RISC design, which aligns with the power constraints of smartphones, tablets, and embedded SoCs. This share leadership also reflects the architecture’s deep integration into hyperscaler custom silicon programs, including Apple M-series and AWS Graviton processors.

x86 retains a 20.00% architecture share, anchored by its entrenched position in enterprise servers and personal computers. Intel and AMD both compete on x86 silicon, maintaining backward compatibility as a switching barrier for enterprise workloads. However, ARM server adoption in hyperscale environments places ongoing competitive pressure on x86 market share.

MIPS holds a 16.00% share, primarily within embedded networking equipment, set-top boxes, and legacy industrial controllers. This segment faces headwinds as newer RISC-V designs offer a royalty-free alternative at comparable embedded performance. Vendors relying on MIPS-based designs in commodity applications face margin compression as alternatives commoditize below.

RISC-V accounts for 12.00% of the architecture segment, with Others at 6.40% holding the remaining share collectively. In January 2026, AMD announced new Ryzen AI 400 and Ryzen AI PRO 400 Series processors delivering up to 60 TOPS of NPU performance, signaling how non-RISC-V architectures are also pushing AI integration to defend share against open-standard challengers.

Core Type Analysis

Octa-Core and Above dominates with 36.60% due to AI workload parallelism requirements.

In 2025, Octa-Core and Above held a dominant market position in the By Core Type segment of the Microprocessor Market, with a 36.60% share. Multi-threaded AI inference, virtualization, and high-performance gaming demand parallel compute architectures that only higher core counts can satisfy. This positions Octa-Core and Above as the default specification for premium laptops, server CPUs, and AI-accelerated SoCs going forward.

Hexa-Core processors hold a 25.00% share, serving mid-range laptop, desktop, and workstation buyers who require meaningful multi-thread performance without premium pricing. This tier absorbs the largest volume of consumer-segment processor sales outside the flagship bracket. Hexa-Core designs remain the primary battleground for AMD and Intel in the sub-premium PC segment.

Quad-Core processors account for 17.00% share, predominantly found in budget laptops, entry-level desktops, and mid-tier mobile devices. AMD’s data center segment posted USD 5.8 Billion in Q1 2026, up 57% year-over-year on EPYC server processor demand, confirming that revenue concentration is accelerating toward higher core-count server platforms rather than consumer-grade quad-core silicon.

Dual-Core processors hold 14.00% and Single-Core processors hold 7.40% of the Core Type segment, together representing the remaining legacy and ultra-low-power embedded share. These tiers serve cost-sensitive microcontroller and IoT applications where compute overhead is minimal. Their combined share will contract as AI-inference requirements push minimum viable processor specs upward.

Bit Size Analysis

64-bit dominates with 60.70% due to memory addressability and OS compatibility demands.

In 2025, 64-bit held a dominant market position in the By Bit Size segment of the Microprocessor Market, with a 60.70% share. 64-bit architecture supports memory addressability beyond 4 GB, which is a baseline requirement for modern operating systems, AI workloads, and server virtualization. This makes 64-bit the standard specification for any processor targeting data center, PC, or premium mobile applications.

End Use Industry Analysis

Consumer Electronics dominates with 34.60% due to smartphone and PC volume scale.

In 2025, Consumer Electronics held a dominant market position in the By End Use Industry segment of the Microprocessor Market, with a 34.60% share. Smartphone processor volumes, coupled with PC and tablet refreshes tied to AI PC platform launches, sustain this segment’s revenue leadership. This creates a direct revenue dependency on consumer upgrade cycles, which are increasingly driven by on-device AI inference capability.

Key Market Segments

By Architecture

- x86

- ARM

- MIPS

- RISC-V

- Others

By Core Type

- Single-Core Microprocessors

- Dual-Core Microprocessors

- Quad-Core Microprocessors

- Hexa-Core Microprocessors

- Octa-Core and Above

By Bit Size

- 8-bit

- 16-bit

- 32-bit

- 64-bit

By End Use Industry

- IT and Telecommunications

- Consumer Electronics

- Automotive

- Industrial

- Healthcare

- Aerospace and Defense

- Others

Market Dynamics

Market Opportunity Analysis - Underserved architectures, emerging regions, and embedded verticals offer early-mover entry points

RISC-V holds a 12.00% architecture share today but carries a projected penetration trajectory reaching 33.7% by 2031. This gap between current share and projected adoption defines a specific design-win window for fabless vendors and embedded systems integrators. Entrants that lock in RISC-V platform relationships with automotive Tier 1 suppliers before 2027 will gain qualification lead times that late movers cannot easily replicate.

The Bit Size segment shows that non-64-bit architectures, covering 8-bit, 16-bit, and 32-bit combined, still represent the remaining 39.30% of unit volume. This installed base serves industrial sensors, medical devices, and legacy embedded controllers that face no near-term migration pressure. Vendors targeting long-lifecycle industrial and healthcare embedded replacement cycles can build predictable revenue streams without competing directly in high-volume consumer markets.

Latin America and Middle East and Africa lack indigenous fabrication infrastructure, meaning processor demand in both regions is entirely import-dependent. This creates a distribution and localization opportunity for fabless vendors willing to establish regional design support and certification services. By contrast, Asia Pacific’s entrenched foundry position means new entrants face structural supply barriers that are absent in these underserved regions.

The Automotive end-use vertical holds no disclosed standalone share figure in the current segment data, yet the AV chips segment is valued at USD 25.69 Billion in 2025 and expanding at an 8.46% CAGR through 2035. This growth rate exceeds the overall market CAGR of 7.00%. Vendors that secure domain-specific processor design wins in ADAS and software-defined vehicle architectures will capture a disproportionate share of automotive semiconductor revenue as vehicle compute content intensifies.

Technology and Innovation Landscape - Advanced node transitions, chiplet architectures, and on-device AI define the next competitive cycle

TSMC’s N2 process entered high-volume production in late 2025, and the A16 post-2nm node is on track for volume production in late 2026. This two-node progression within a single calendar year compresses design migration cycles for chip architects. Vendors who delay tape-out decisions to A16 risk missing the first consumer product cycle, ceding market share to Apple and NVIDIA, which are among the earliest A16 adopters.

Intel 18A-P delivers 9% higher performance at iso-power or 18% lower power at iso-performance compared to Intel 18A, with enhanced thermal efficiency. This incremental node improvement matters because server and AI PC buyers increasingly specify power-per-flop as a procurement criterion. Foundry customers that migrate designs to 18A-P gain a direct cost reduction on data center energy bills, which translates into total cost of ownership advantages in hyperscale infrastructure bids.

In October 2025, Intel unveiled its Panther Lake client architecture as the first AI PC platform built on Intel 18A, with launch scheduled for the first half of 2026. This marks the first time Intel’s own process node directly competes with TSMC for a flagship client processor design win. If Panther Lake achieves competitive yields at volume, it validates Intel Foundry as a credible alternative supply node for fabless and IDM customers beyond Intel’s internal roadmap.

In May 2025, Intel showcased workstation-focused configurations of Core Ultra Series 2 at Computex 2025, emphasizing enhanced multi-threaded performance and AI acceleration for creator and edge computing platforms. On-chip NPU integration delivering 15 to 30+ TOPS of AI inference performance enables real-time intelligence in industrial IoT, robotics, and consumer devices without cloud dependency. This eliminates per-inference cloud compute costs for edge-deployed applications, creating a direct operating expense reduction that accelerates enterprise adoption of AI-enabled processor platforms.

Drivers

Microprocessor growth in 2026 is constrained not only by end demand but by access to 3nm, 5nm, and sub-7nm manufacturing capacity, where wafer allocation directly determines the ability to ship premium CPUs at scale. TSMC reported that 3nm contributed 22% of wafer revenue, 5nm contributed 36%, and nodes at 7nm and below accounted for 73% of total wafer revenue in Q1 2025. This concentration enables significant performance-per-watt gains through higher transistor density and tighter integration of AI accelerators, sustaining ASP levels even as broader component cost pressures persist.

The result is a supply-driven competitive structure where firms with secured foundry capacity gain faster product cycles and stronger margin resilience. Diversification of fabrication into the US and Europe improves long-term supply security but does not immediately replicate existing scale advantages. Near-term leadership remains tied to long-term wafer commitments and co-optimized design with advanced packaging and power efficiency constraints.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI server CPU uplift | +2.4% | North America core, Taiwan-Korea supply base, EU hyperscale clusters | Short term (≤ 2 years) |

| Edge AI and AI PC refresh | +1.6% | North America, Western Europe, Japan, South Korea, urban China spill-over | Short term (≤ 2 years) |

| Advanced-node capacity expansion | +1.3% | Taiwan core, US reshoring zones, EU strategic fabs | Medium term (2–4 years) |

| Automotive compute intensification | +1.1% | China, EU, US, Japan, South Korea | Medium term (2–4 years) |

| Industrial and IoT embedded modernization | +0.9% | APAC manufacturing corridors, Germany, US industrial belt | Medium term (2–4 years) |

| Semiconductor sovereignty policy pull | +0.8% | US, EU, selective North American spill-over | Long term (≥ 4 years) |

Restraints

Tariff uncertainty is becoming a separate restraint from export controls because it affects procurement timing, contract structure, and total landed cost even when products remain legally sellable. The U.S. imposed a 25% tariff on certain advanced computing chips and derivative products effective January 15, 2026 under Section 232 measures. A duty of this size overwhelms normal semiconductor annual price-down assumptions, forcing hyperscalers, OEMs, and enterprise buyers to reconsider sourcing routes, redesign BOMs, or accelerate domestic qualification programs.

Industry surveys at end of 2025 showed tariffs and trade policy had become the top concern for semiconductor leaders, with 54% focused on geographic diversification and 45% prioritizing more flexible supply chains. This signals management attention and capital are being diverted toward resilience rather than pure growth. For the microprocessor market, this creates slower conversion of pipeline demand into booked revenue and more conservative distributor inventories, supporting a 0.9-point near-term CAGR haircut.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced-node cost inflation | -1.4% | North America core, Taiwan, Korea, EU fab buyers | Medium term |

| Export-control market loss | -1.2% | China, US vendors, Taiwan/Korea supply chain | Short term |

| Tariff-led procurement friction | -0.9% | North America core, China-linked routes, APAC corridors | Short term |

| HBM and packaging bottlenecks | -1.1% | US AI stack, Taiwan, Korea, global server chain | Medium term |

| Fab concentration and seismic risk | -0.7% | Taiwan-centric supply, Japan, Korea, global OEMs | Long term |

| Europe cost and subsidy drag | -0.6% | EU, US/EU cross-investment programs | Medium term |

Challenges

The most persistent 2026 microprocessor challenge is no longer front-end wafer access alone but backend synchronization across advanced logic, CoWoS-class packaging, substrates, and memory. This creates a nonlinear fulfillment bottleneck for high-performance CPUs, AI accelerators, and chiplet-based server processors. Industry reporting indicates the CoWoS supply-demand imbalance stood at around 20% in 2026 and may only narrow to about 10% by year-end.

TSMC’s monthly CoWoS capacity is rising toward 120,000 to 140,000 wafers, while total ecosystem capacity approaches 200,000 wafers per month. This means capacity expansion is material but still lagging demand velocity. Lead times for some packaging flows previously stretched into roughly 52 to 78 weeks, causing microprocessor vendors to face launch staggering, delayed server qualification cycles, and elevated inventory-buffer costs rather than outright shipment cessation.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Advanced Packaging Bottlenecks | -1.6% | Taiwan core, US AI clusters, Korea memory chain | Medium term (2-4 years) |

| Design Talent Pipeline Gaps | -1.1% | North America core, Taiwan, India design hubs, EU labs | Long term (≥ 4 years) |

| Geopolitical Trade Fragmentation | -1.3% | US-China corridor, EU regulatory hubs, East Asia supply chain | Long term (≥ 4 years) |

| Power And Utility Constraints | -0.8% | Taiwan fabs, Arizona, Japan, Singapore | Medium term (2-4 years) |

| Yield Complexity At Leading Nodes | -1.2% | Taiwan, Korea, US advanced foundries | Medium term (2-4 years) |

| Memory-Logic Synchronization Risk | -0.9% | Korea, Taiwan, US hyperscale corridor, China AI stack | Short term (≤ 2 years) |

Opportunities

CPU-as-a-service stacks qualify as a high-priority opportunity because baseline growth assumes transactional silicon revenue, while the underexploited upside lies in recurring monetization through microcode features, workload optimization subscriptions, security patch tiers, and fleet telemetry tied to enterprise and industrial deployments. A microprocessor supplier that attaches annual software and assurance contracts equal to 3% to 5% of silicon revenue across installed enterprise, edge, and embedded fleets can add roughly 1.2 percentage points to long-range CAGR.

This service layer also improves gross margins by 500 to 900 basis points on service revenue. Vendors that establish this model first create deep integration into orchestration, observability, and compliance workflows. This structural lock-in reduces customer churn and makes pure-silicon price competition less decisive as a switching lever.

RISC-V International confirms the architecture is approaching 2.5 Billion cores shipped annually in 2026, with the ecosystem reaching production-readiness for automotive-grade applications. This represents a concrete commercialization threshold, not an early-stage experiment. Vendors entering the automotive and IoT segments via RISC-V now access design wins without royalty overhead, creating a durable unit-economics advantage over ARM-licensed competitors.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Edge AI inference CPUs | +2.2% | North America, EU, APAC | Short term |

| Chiplet platform licensing | +1.9% | North America core, Taiwan, EU | Medium term |

| RISC-V sovereign compute | +1.6% | EU, India, Southeast Asia | Medium term |

| SDV zonal processors | +1.8% | EU, China, North America | Medium term |

| CPU-as-a-service stacks | +1.2% | North America, Japan, EU | Short term |

| Mature-node industrial roll-up | +1.4% | India, ASEAN, Eastern Europe | Long term |

Regional Analysis

Asia Pacific Dominates the Microprocessor Market with a Market Share of 42.10%, Valued at USD 55.24 Billion

Asia Pacific commands 42.10% of global microprocessor revenue, anchored by Taiwan’s foundry infrastructure, South Korea’s memory and logic output, China’s device assembly scale, and Japan’s materials supply chain. TSMC and Samsung together control the advanced node capacity that enables the highest-margin processor designs globally. This geographic concentration gives the region structural pricing influence over the entire microprocessor value chain.

North America holds the second-largest regional position, driven by hyperscaler data center investment and fabless chip design leadership from US-headquartered firms. NVIDIA’s automotive segment reached USD 592 Million in Q3 FY2026, up 32% year-over-year, reflecting accelerating automotive processor content growth that US-designed chips are capturing. Reshoring investments under the CHIPS Act are beginning to add domestic manufacturing capacity, though volume impact remains medium-term.

Europe’s microprocessor demand is driven by automotive semiconductor content, industrial automation, and defense electronics rather than consumer device volumes. EU Chips Act investments are directing capital toward European fab construction, with strategic intent to reduce external supply dependency. However, cost and subsidy execution gaps present a medium-term drag on Europe’s ability to capture advanced-node fabrication share quickly.

Latin America and Middle East and Africa represent smaller but structurally growing demand regions. Both regions benefit from electronics manufacturing diversification and government-backed digitization programs. However, neither region hosts significant indigenous fabrication capacity, meaning growth translates into import demand rather than local supply chain development.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Intel Corporation is executing a dual strategy of product and foundry recovery simultaneously, a high-risk position that creates both upside and execution vulnerability. Intel’s Panther Lake platform, built on Intel 18A, targets the AI PC cycle from the first half of 2026. In May 2026, AMD launched Ryzen AI Halo processors capable of running AI models up to 200 billion parameters locally, increasing competitive pressure on Intel’s AI PC positioning.

NVIDIA Corporation has moved beyond GPU dominance into CPU territory with the Vera CPU, which opens an estimated USD 200 Billion total addressable market and provides approximately USD 20 Billion in standalone CPU revenue visibility in calendar 2026. This signals that NVIDIA is no longer a GPU-only supplier but a full compute platform vendor. Any enterprise that has standardized on NVIDIA’s AI stack now faces a consolidated silicon vendor with pricing influence across the entire server hardware stack.

Key Players

- Intel Corporation

- Qualcomm Technologies, Inc.

- Texas Instruments Incorporated

- STMicroelectronics

- Microchip Technology Inc.

- NXP Semiconductors

- Renesas Electronics Corporation

- NVIDIA Corporation

- Analog Devices, Inc.

- Nuvoton Technology Corporation

- The Western Design Center, Inc.

- Other Key Players

Recent Developments

- January 2025 – Intel announced at CES 2025 the extension of its AI PC and edge computing lineup with new Intel Core Ultra Series 2 processors, including Core Ultra 200HX mobile enthusiast chips featuring integrated NPU for AI workloads.

- April 2025 – Intel launched the Intel Core Ultra 200V series, its most efficient x86 mobile processor family to date, positioning them as AI PC processors with systems scheduled to reach retail globally from September 24, 2025.

- March 2026 – AMD expanded its Ryzen AI portfolio at MWC 2026 by launching Ryzen AI 400 Series and Ryzen AI PRO 400 Series desktop processors for AM5 platforms, with AI PC desktops and mobile workstations using these parts scheduled to reach market from Q2 2026.

- May 2026 – The U.S. Commerce Department closed a loophole that had allowed hundreds of thousands of NVIDIA AI chips to reach Chinese firms through their overseas subsidiaries, tightening export enforcement for advanced AI silicon.

- April 2026 – The bipartisan MATCH Act was introduced in U.S. Congress, proposing new restrictions on DUV immersion lithography exports from ASML and other toolmakers to China, which would further constrain Chinese advanced-node chip manufacturing capability.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 131.2 Billion |

| Forecast Revenue (2035) | USD 258.6 Billion |

| CAGR (2026-2035) | 7.00% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Architecture (x86, ARM, MIPS, RISC-V, Others), By Core Type (Single-Core, Dual-Core, Quad-Core, Hexa-Core, Octa-Core and Above), By Bit Size (8-bit, 16-bit, 32-bit, 64-bit), By End Use Industry (IT and Telecommunications, Consumer Electronics, Automotive, Industrial, Healthcare, Aerospace and Defense, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Intel Corporation, Qualcomm Technologies, Inc., Texas Instruments Incorporated, STMicroelectronics, Microchip Technology Inc., NXP Semiconductors, Renesas Electronics Corporation, NVIDIA Corporation, Analog Devices, Inc., Nuvoton Technology Corporation, The Western Design Center, Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |