Quick Navigation

Report Overview

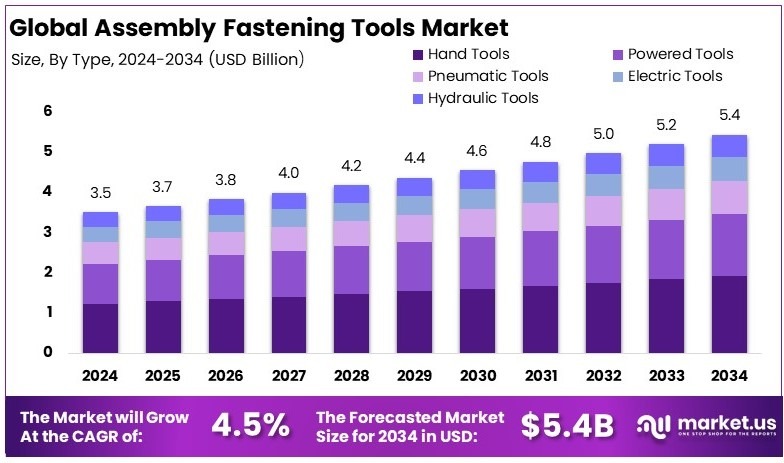

The Global Assembly Fastening Tools Market size is expected to be worth around USD 5.4 Billion by 2034, from USD 3.5 Billion in 2024, growing at a CAGR of 4.5% during the forecast period from 2025 to 2034.

Assembly Fastening Tools are mechanical devices designed to join or fasten parts together in assembly operations. They include tools like drills, screwdrivers, and impact wrenches that ensure secure and efficient connections in production lines, particularly in automotive and electronics manufacturing.

The Assembly Fastening Tools Market refers to the global demand and supply of tools used for fastening and joining parts in various industries. This market includes hand tools, power tools, and other devices utilized in assembly operations across sectors like automotive, electronics, and construction.

Assembly fastening tools are crucial in modern manufacturing, aligning with industry needs for precision and efficiency. These tools have become integral in sectors like automotive and electronics, where secure and rapid assembly is critical. The global market for these tools is expanding, fueled by advancements in technology and manufacturing demands.

According to industry reports, the broader industrial robotics market, which includes assembly fastening tools, is expected to grow significantly. It is projected to reach shipments of 517,000 units annually by 2024. This growth is driven by the increasing automation in manufacturing processes across various industries.

Furthermore, the demand for assembly fastening tools is closely linked to global automobile production trends. For instance, automobile production rose from about 80 million units in 2021 to nearly 85 million units in 2022, and again to nearly 94 million units in 2023. This increase underscores the growing need for efficient, automated assembly solutions in the automotive sector.

Moreover, the market for assembly fastening tools is becoming highly competitive as manufacturers innovate to meet precise industry specifications. This competition not only drives technological advancements but also broadens the range of applications for these tools. As a result, opportunities for market expansion and customer engagement continue to rise.

However, market saturation is an emerging concern, as many sectors have already integrated high levels of automation. Despite this, the impact of assembly fastening tools on both a broader and a local scale remains substantial. For example, regions with heavy manufacturing investments see significant economic benefits from adopting these technologies.

Key Takeaways

- The Assembly Fastening Tools Market was valued at USD 3.5 Billion in 2024 and is expected to reach USD 5.4 Billion by 2034, with a CAGR of 4.5%.

- In 2024, Hand Tools dominated the type segment with 40.0%, driven by widespread industrial and household applications.

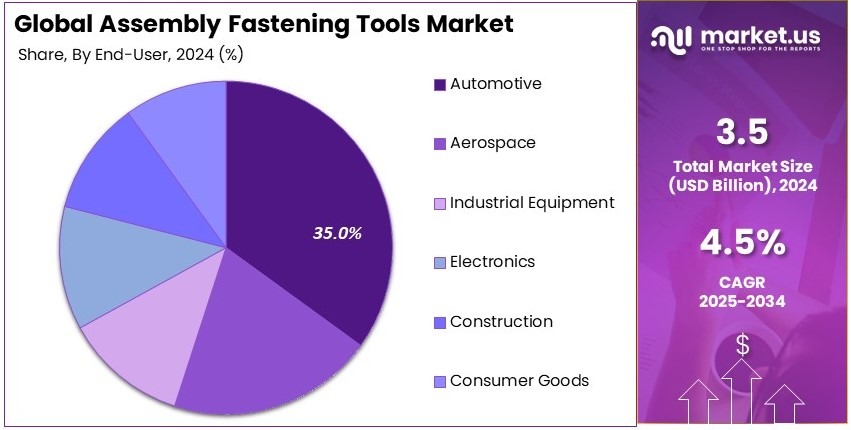

- In 2024, Automotive led the end-user industry with 35.0%, as vehicle manufacturing and maintenance require high precision fastening tools.

- In 2024, Screwing was the dominant fastening type with 53.1%, owing to its extensive use in assembly lines.

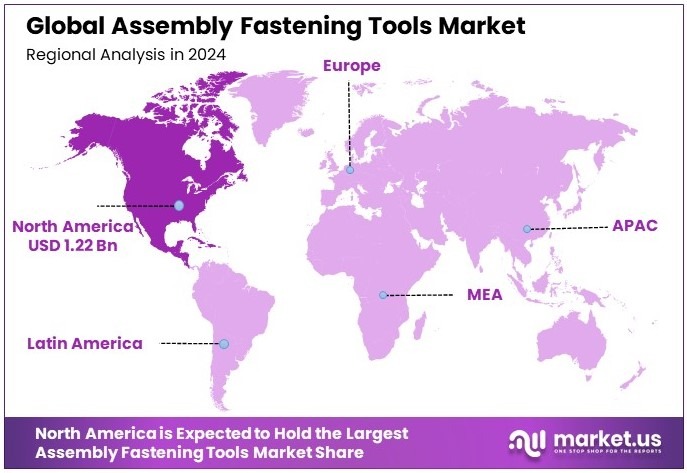

- In 2024, North America was the leading region with 34.8% valued at USD 1.22 Bn, supported by robust industrial manufacturing.

Type Analysis

Hand Tools dominate with 40.0% due to their versatility and widespread use across industries.

Hand tools are the most commonly used fastening tools in many industries, holding a dominant market share of 40.0%. Their widespread adoption can be attributed to their simplicity, cost-effectiveness, and ease of use. Unlike powered tools, hand tools do not require electricity or complex systems, which makes them a preferred choice for manual operations, especially in smaller tasks or precision assembly.

In sectors like automotive or industrial equipment, hand tools offer control and flexibility, ensuring a high level of accuracy in fastening applications. Their relatively low cost also makes them accessible for small businesses or workers who need tools for lighter tasks.

On the other hand, powered tools, though also crucial, are less commonly used for small or light fastening tasks. While they can enhance speed and efficiency, they come with higher upfront costs and may require more maintenance.

Powered tools, including pneumatic, electric, and hydraulic models, are more suitable for larger-scale operations where high volume or power is needed. These tools excel in settings such as construction or heavy industrial applications, where speed and durability are vital. However, their higher energy consumption and the need for power sources make them less attractive for basic or smaller-scale tasks.

End-User Industry Analysis

Automotive dominates with 35.0% due to the high volume of assembly required.

The automotive industry leads the market for assembly fastening tools, accounting for 35.0% of total demand. The automotive sector relies heavily on efficient fastening systems to ensure high-quality assembly while maintaining speed. This market’s growth is driven by the need for precision and efficiency in vehicle manufacturing.

Fastening tools such as powered tools and hand tools are used to assemble various vehicle parts, including engines, frames, and interiors. As automotive production becomes increasingly automated, fastening tools that can support high-speed assembly lines are in higher demand. Additionally, growing trends toward electric vehicles (EVs) and sustainability further fuel the need for advanced fastening tools capable of handling specialized materials and components.

Aerospace follows closely with a 25.0% share, as this industry requires very high precision and safety standards. Fastening tools in aerospace are used for assembling aircraft and spacecraft, where quality control is paramount.

The industrial equipment sector contributes 15.0%, as these tools are used in the assembly of heavy machinery, which requires durable and reliable fastening systems. Other industries such as electronics and consumer goods also contribute to the market, though their demand is lower due to less frequent use of high-power fastening tools. Finally, the construction industry, at 10.0%, uses fastening tools for tasks such as building frameworks, where heavy-duty tools are necessary for strength and durability.

Fastening Type Analysis

Screwing dominates with 53.1% due to its extensive use in assembly processes.

Screwing is the most widely used fastening type, holding a dominant market share of 53.1%. This fastening method is commonly used in a wide variety of industries due to its simplicity, efficiency, and strength. Screws provide a secure fastening solution for components that need to be assembled and disassembled repeatedly, which is important in sectors like automotive, aerospace, and industrial equipment.

Screwing tools are also highly versatile, used in applications ranging from small electronics assembly to large machinery construction. As industries continue to evolve towards automation, screwing tools are becoming more advanced, offering higher speeds and better torque control to meet modern production requirements.

On the other hand, bolting is a critical fastening method in industries that require stronger, more permanent joints. While not as widely used as screwing, bolting is essential in heavy-duty applications such as construction and industrial equipment manufacturing. Riveting, though also important, accounts for a smaller share of the market.

It is primarily used in applications where high-strength, permanent fastening is needed, such as in the aerospace and shipbuilding industries. Clamping, which is used to temporarily hold parts in place during the assembly process, has a more specialized role, with less frequent use compared to the other fastening types. While important, it does not see the same widespread application as screwing.

Key Market Segments

By Type

- Hand Tools

- Powered Tools

- Pneumatic Tools

- Electric Tools

- Hydraulic Tools

By End-User Industry

- Automotive

- Aerospace

- Industrial Equipment

- Electronics

- Construction

- Consumer Goods

By Fastening Type

- Screwing

- Bolting

- Riveting

- Clamping

Driving Factors

Precision and Efficiency Demand Drives Market Growth

The increasing demand for precision and efficiency in manufacturing processes is a key driver of the assembly fastening tools market. As industries continue to evolve, the need for tools that ensure accurate and quick fastening solutions becomes crucial. Precision tools help reduce errors, improve product quality, and enhance the overall production speed, which is vital in sectors like automotive and electronics.

Advancements in battery-powered tools have also significantly contributed to the market’s growth. These tools enhance mobility and usability, allowing workers to operate with greater flexibility. With no need for cords, battery-powered tools provide freedom of movement, increasing efficiency in complex assembly tasks.

Additionally, the rise of the automotive industry, which requires high-quality assembly solutions, has further boosted the demand for fastening tools. The industry’s continuous growth and need for advanced assembly methods create a consistent need for reliable, precise fastening solutions.

The adoption of automation in industrial assembly lines is another major driver. As automation systems become more common, the integration of fastening tools into these systems is essential for improving speed and accuracy. This shift towards automated processes is contributing to the increased demand for advanced fastening solutions, which offer consistent results with minimal human intervention.

Restraining Factors

High Costs and Integration Challenges Restrain Market Growth

While the assembly fastening tools market has notable growth drivers, several factors are restraining its expansion. High initial investment costs for advanced fastening systems remain a significant barrier for many businesses. The cost of acquiring and integrating advanced tools can be prohibitively expensive, particularly for small and medium-sized manufacturers.

Furthermore, the limited availability of skilled labor to operate specialized fastening tools poses another challenge. Many advanced fastening systems require workers with specific technical expertise, which can be difficult to find. This shortage of skilled labor hampers companies’ ability to fully adopt and benefit from modern fastening solutions.

Concerns regarding the maintenance and downtime of power tools also affect market growth. As with all machinery, fastening tools require regular maintenance to operate effectively. Unforeseen downtimes for repairs can disrupt production schedules and lead to higher operational costs.

Finally, the challenges in integrating modern fastening tools with legacy manufacturing systems also restrict the market. Many companies still operate older systems that may not be compatible with the latest fastening technologies, leading to significant integration hurdles and additional costs.

Growth Opportunities

Expanding Industries and Smart Solutions Offer Market Opportunities

There are several growth opportunities for players in the assembly fastening tools market. One of the key areas is the expanding applications in the aerospace and electronics industries. Both sectors require high levels of precision, and as these industries grow, so does the demand for advanced fastening tools that can meet their stringent requirements.

Moreover, the development of smart, connected fastening tools with IoT integration presents a significant opportunity. These tools can provide real-time data on their performance, enabling predictive maintenance and reducing downtime. Such innovations make the tools more efficient and cost-effective, increasing their appeal to manufacturers.

Growing demand for ergonomic tools to reduce worker fatigue is another opportunity. Manufacturers are increasingly aware of the physical toll that repetitive tasks can take on workers. As a result, there is a rising demand for fastening tools that are designed to reduce strain and improve comfort, which in turn boosts productivity.

Additionally, there is an increasing trend towards the use of cordless, compact fastening tools for on-site operations. These tools offer convenience and flexibility, allowing workers to easily carry out tasks in various locations, making them highly suitable for industries like construction and automotive.

Emerging Trends

Eco-Friendly and AI Innovations Lead Market Trends

Several trends are currently shaping the assembly fastening tools market. A growing focus on eco-friendly materials and sustainable tool designs is one such trend. As environmental concerns increase, manufacturers are seeking tools made from sustainable materials that reduce their environmental footprint, in line with broader sustainability goals.

The introduction of AI-driven tools for enhanced fastening precision is another notable trend. AI technologies can improve the accuracy and efficiency of fastening processes, reducing the likelihood of errors and enhancing overall productivity. This shift towards smarter tools allows manufacturers to achieve higher quality with greater speed and consistency.

Additionally, the growth of cordless power tools with longer battery life is revolutionizing the market. The demand for tools that can operate for extended periods without the need for frequent recharging is growing. Longer battery life increases the overall efficiency of fastening tasks and makes cordless tools more appealing for industries requiring high operational hours.

The rising popularity of modular and customizable tool kits for specific applications is another key trend. These toolkits allow workers to choose and configure tools based on their specific needs, improving versatility and functionality on the job. This trend reflects the growing desire for adaptable solutions that can cater to different production requirements.

Regional Analysis

North America Dominates with 34.8% Market Share

North America leads the Assembly Fastening Tools Market with a 34.8% share, amounting to USD 1.22 billion. This strong position is attributed to the region’s advanced manufacturing sector, significant industrial growth, and high demand for automation in industries like automotive and electronics. The presence of major players like Stanley Black & Decker and Bosch further strengthens the region’s dominance in this market.

The region’s market share is driven by its highly developed industrial infrastructure and growing focus on automation and labor efficiency. North American manufacturers are increasingly adopting advanced fastening tools to enhance productivity and reduce downtime in assembly lines.

Additionally, the growing need for precision and reliability in industries such as automotive, aerospace, and electronics has contributed to a high demand for advanced fastening tools. The adoption of Industry 4.0 technologies also plays a role in boosting the use of assembly fastening tools to improve operational efficiency.

Regional Mentions:

- Europe: Europe holds a strong share in the assembly fastening tools market, supported by its focus on precision engineering and strict quality standards. The region is driven by industries like automotive and aerospace, which require high-performance fastening solutions.

- Asia Pacific: The Asia Pacific region is growing rapidly due to its expanding industrial base, particularly in China, Japan, and India. The region’s demand for cost-effective and efficient fastening tools is propelled by mass production and a push toward automation in manufacturing.

- Middle East & Africa: The Middle East and Africa are steadily increasing their adoption of assembly fastening tools, driven by the construction, oil, and gas industries. The region’s push toward industrial growth and infrastructure development is fueling market expansion.

- Latin America: Latin America is gradually embracing automation in manufacturing, with countries like Brazil and Mexico witnessing growth in assembly fastening tool demand. The region’s market is shaped by efforts to modernize industries such as automotive and consumer electronics.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

The Assembly Fastening Tools Market is highly competitive and dominated by leading companies with strong brand recognition and comprehensive product offerings. Among the top players, Stanley Black & Decker, Inc., Bosch Power Tools, Makita Corporation, and Hilti Corporation stand out as key drivers of innovation and market expansion.

Stanley Black & Decker, Inc. is a global leader in power tools and fastening solutions. With its wide portfolio that includes hand tools, power tools, and fasteners, Stanley Black & Decker caters to industries such as automotive, construction, and aerospace. The company’s focus on quality, durability, and cutting-edge technology has positioned it as a dominant force in the fastening tools market.

Bosch Power Tools is another major player, known for its precision engineering and high-quality fastening tools. Bosch offers a wide range of products, including drills, screwdrivers, and impact wrenches, used in various applications such as automotive assembly and manufacturing. The company’s focus on innovation, user-friendly designs, and strong customer support has strengthened its position in the market.

Makita Corporation, a well-established brand in the power tools industry, delivers reliable fastening tools widely used in construction, woodworking, and heavy-duty industries. The company is recognized for its electric tools that combine performance and ease of use, making them a preferred choice for both professionals and DIY users.

Hilti Corporation is renowned for its high-performance fastening tools tailored to the needs of the construction industry. With a focus on quality and safety, Hilti’s tools are built for heavy-duty use, offering superior performance and longevity. The company’s commitment to technological advancements and customer satisfaction has made it a leading player in the fastening tools market.

These four companies continue to lead the Assembly Fastening Tools Market through continuous product innovation, global reach, and strong customer relationships, ensuring sustained growth and market dominance in the coming years.

Major Companies in the Market

- Stanley Black & Decker, Inc.

- Bosch Power Tools

- Makita Corporation

- Hilti Corporation

- Apex Tool Group

- Ingersoll Rand

- Snap-On Incorporated

- Parker Hannifin Corporation

- Chicago Pneumatic

- Desoutter Industrial Tools

- JET Tools

- Koki Holdings Co., Ltd.

- Atlas Copco AB

Recent Developments

- JRG Automotive Industries: On February 2025, JRG Automotive Industries acquired the two-wheeler functional plastics division of Stanley Engineered Fastening India (SEFI), expanding its manufacturing presence in key automotive hubs across India. The acquisition includes production facilities in Manesar and Bangalore, strengthening JRG’s capabilities in plastic injection-molded components. Meanwhile, SEFI continues to focus on engineered fastening solutions across various industries.

- Panasonic: On October 2024, Panasonic showcased its latest innovations in intelligent assembly systems at the Assembly Show in Rosemont, IL. The company introduced the High-Res Transducer, offering triple the resolution for improved torque measurement. Additionally, Panasonic featured its corded Electric Screwdriver System, nominated for Product of the Year, and new additions to the AccuPulse range, reinforcing its commitment to precision, efficiency, and quality in assembly technology.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 3.5 Billion |

| Forecast Revenue (2034) | USD 5.4 Billion |

| CAGR (2025-2034) | 4.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Hand Tools, Powered Tools, Pneumatic Tools, Electric Tools, Hydraulic Tools), By End-User Industry (Automotive, Aerospace, Industrial Equipment, Electronics, Construction, Consumer Goods), By Fastening Type (Screwing, Bolting, Riveting, Clamping) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Stanley Black & Decker, Inc., Bosch Power Tools, Makita Corporation, Hilti Corporation, Apex Tool Group, Ingersoll Rand, Snap-On Incorporated, Parker Hannifin Corporation, Chicago Pneumatic, Desoutter Industrial Tools, JET Tools, Koki Holdings Co., Ltd., Atlas Copco AB |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |