Quick Navigation

Report Overview

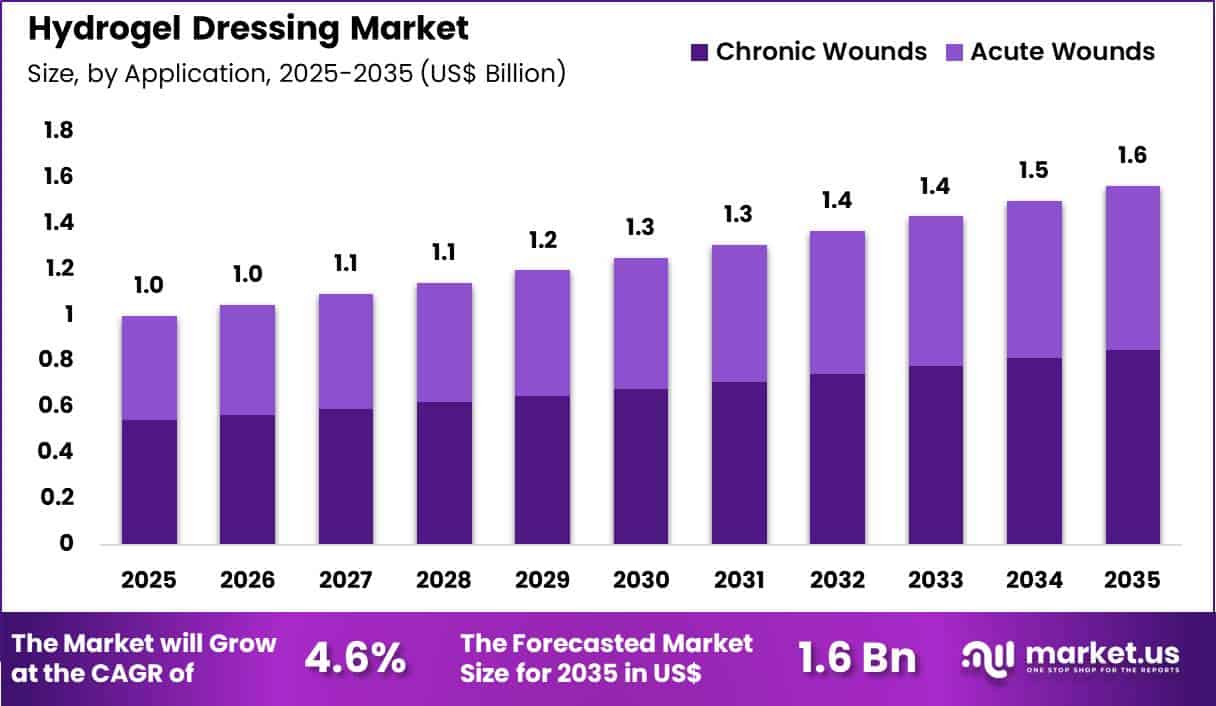

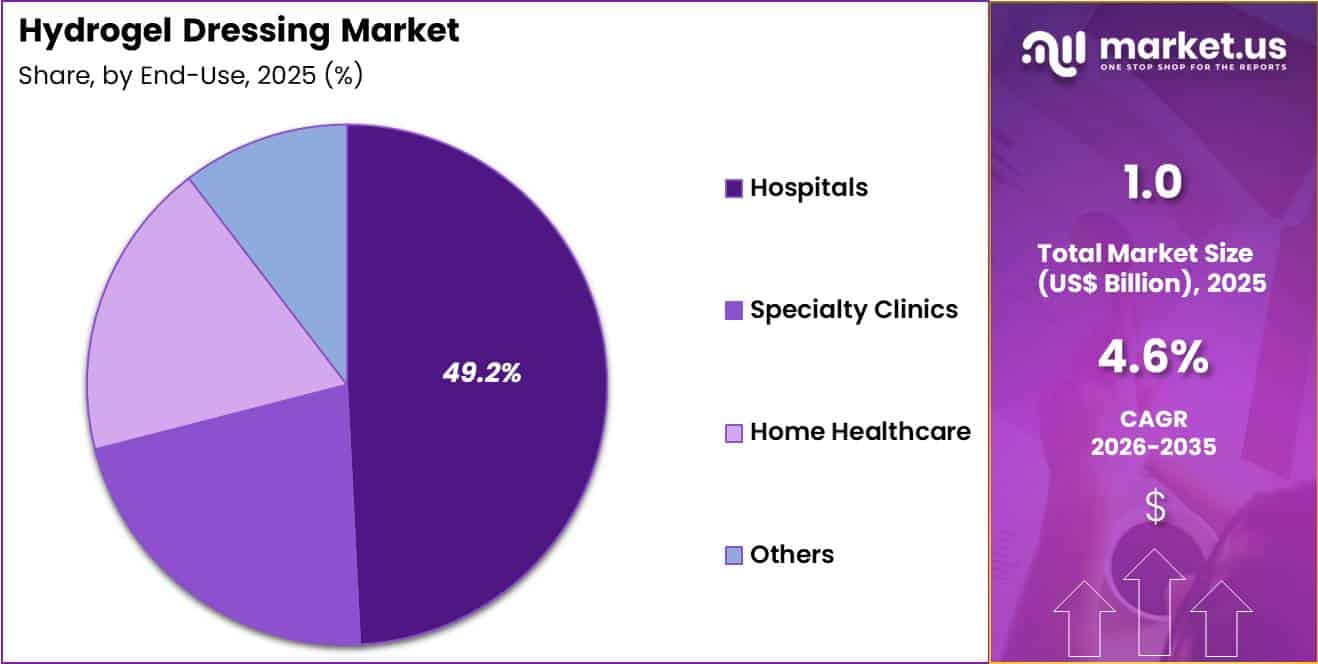

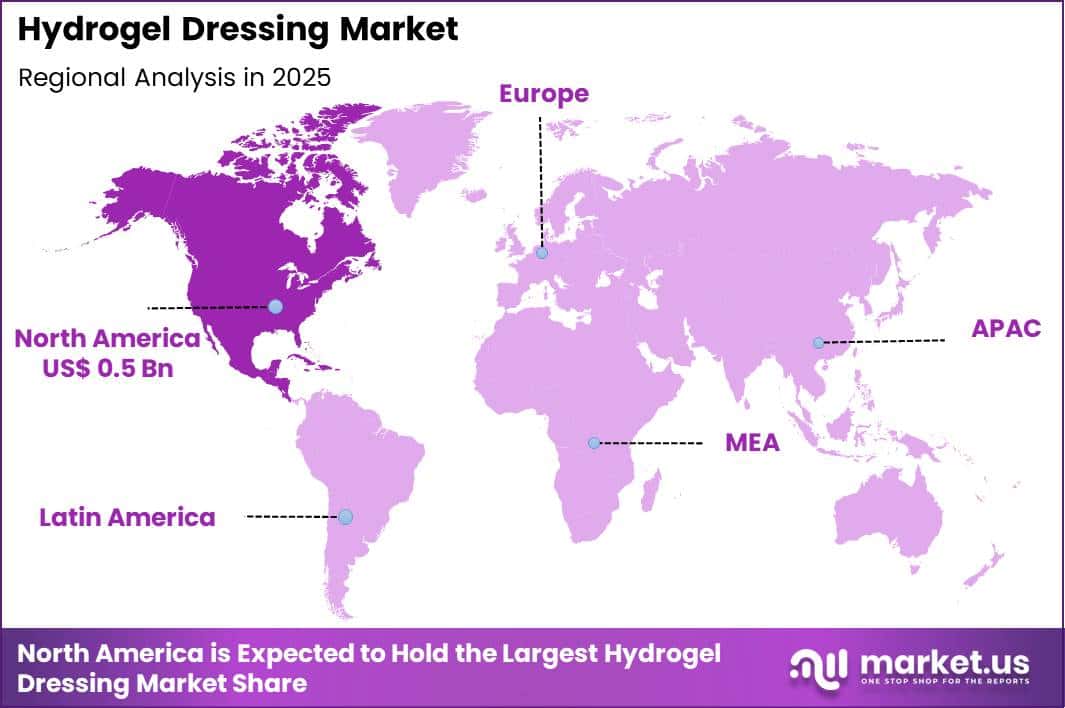

The Global Hydrogel Dressing Market size is expected to be worth around US$ 1.6 Billion by 2035 from US$ 1.0 Billion in 2025, growing at a CAGR of 4.6% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 46.3% share with a revenue of US$ 0.5 Billion.

Increasing prevalence of chronic wounds and the need for advanced moisture management solutions drive the Hydrogel Dressing market as clinicians seek dressings that maintain an optimal healing environment while minimizing patient discomfort and dressing change frequency.

Wound care specialists increasingly apply hydrogel dressings to partial-thickness burns and superficial abrasions, where the high water content cools the wound bed, reduces pain, and promotes autolytic debridement of necrotic tissue without adhering to the wound surface.

These dressings support diabetic foot ulcer treatment by providing sustained hydration to dry, necrotic wounds, facilitating granulation tissue formation and epithelialization in patients with impaired healing.

In pressure injury management, hydrogel sheets hydrate eschar and slough in stage III and IV ulcers, softening devitalized tissue for easier removal during debridement while preventing further tissue breakdown.

Hydrogel-impregnated gauze and foam composites enable effective management of moderately exuding wounds, absorbing excess fluid while maintaining a moist interface that accelerates healing in venous leg ulcers and surgical incisions. Palliative care teams utilize hydrogel dressings for malignant fungating wounds, reducing odor, controlling exudate, and alleviating pain associated with exposed tumor tissue.

Manufacturers pursue opportunities to develop antimicrobial hydrogel dressings infused with silver or honey, expanding applications in infected or high-risk wounds where bacterial colonization delays healing.

These advancements support combination products that integrate hydrogels with foam or alginate layers for superior exudate handling in heavily draining chronic ulcers. Opportunities emerge in bioactive hydrogels incorporating growth factors or extracellular matrix components to stimulate tissue regeneration in stalled wounds.

Companies invest in transparent, conformable formulations that allow visual wound monitoring without removal, improving assessment efficiency in outpatient and home care settings. Recent trends emphasize extended-wear designs and patient-friendly application features that reduce caregiver burden.

In March 2026, Smith & Nephew introduced the ALLEVYN COMPLETE CARE system, a foam-based wound management solution that incorporates advanced hydrocellular layers. The design is intended to support balanced moisture control and help reduce the risk of pressure injuries, with initial availability across the US and European markets.

The market continues to evolve toward multifunctional, evidence-based dressings that optimize healing outcomes while addressing infection control and patient comfort in diverse wound care scenarios.

Key Takeaways

- In 2025, the market generated a revenue of US$ 1.0 Billion, with a CAGR of 4.6%, and is expected to reach US$ 1.6 Billion by the year 2035.

- The product segment is divided into amorphous hydrogel (gels/tubes), impregnated hydrogel (gauze/sponge-based) and sheet hydrogel (solid 3d networks), with amorphous hydrogel taking the lead with a market share of 58.4%.

- Considering application, the market is divided into acute wounds and chronic wounds. Among these, chronic wounds held a significant share of 54.3%.

- Furthermore, concerning the end-use segment, the market is segregated into hospitals, specialty clinics, home healthcare and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 49.2% in the market.

- North America led the market by securing a market share of 46.3%.

Product Analysis

Amorphous hydrogel accounted for 58.4% of growth within product and dominates the hydrogel dressing market due to its high flexibility, ease of application, and strong moisture-retention capability for wound healing. Clinicians widely prefer gel-based hydrogels because they conform easily to irregular wound surfaces and support autolytic debridement, which improves healing outcomes.

Chronic wound care guidelines emphasize the importance of maintaining a moist wound environment, and amorphous hydrogels effectively support this requirement. The segment is expected to expand as the number of patients with diabetic ulcers, pressure ulcers, and venous leg ulcers continues to rise globally.

Healthcare data indicates that millions of people suffer from chronic wounds each year, which increases demand for advanced wound care solutions. Amorphous hydrogels are likely to gain further traction because they reduce pain during dressing changes and improve patient comfort.

Their ability to deliver hydration directly to dry or necrotic wounds makes them suitable for a wide range of clinical conditions. The segment also benefits from easy storage, cost-effectiveness, and compatibility with other wound care products.

Increasing adoption in both hospital and home care settings is projected to support consistent demand. As clinicians continue to prioritize effective moisture management and patient comfort, amorphous hydrogel is anticipated to remain the leading product segment in this market.

Application Analysis

Chronic wounds accounted for 54.3% of growth within application and dominate the hydrogel dressing market due to the long healing duration and high recurrence rates associated with these conditions. Chronic wounds such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers require ongoing treatment and advanced dressing solutions, which drives sustained product demand.

Global health organizations report that diabetes affects hundreds of millions of individuals worldwide, and a notable proportion of these patients develop foot ulcers during their lifetime. This growing patient base is expected to increase demand for effective wound management products.

Hydrogel dressings are likely to remain essential in chronic wound care because they provide hydration, support tissue regeneration, and reduce wound pain. The segment benefits from the need for repeated dressing changes over extended periods, which increases consumption volume.

Rising aging population and increasing incidence of lifestyle-related diseases are projected to further support growth. Healthcare providers are focusing more on advanced wound care protocols to reduce complications and hospitalization rates.

As chronic wounds continue to represent a significant healthcare burden, this segment is anticipated to maintain its dominant position in the hydrogel dressing market.

End-Use Analysis

Hospitals accounted for 49.2% of growth within end use and dominate the hydrogel dressing market due to their role as primary treatment centers for acute and chronic wound management. Hospitals handle a large volume of patients with surgical wounds, trauma injuries, and complex chronic conditions, which increases the demand for advanced wound care products.

Clinical settings provide access to trained healthcare professionals who assess wound severity and select appropriate dressing types, which strengthens hospital-based usage. Hospitals are expected to remain dominant as they manage high-risk patients requiring continuous monitoring and specialized care.

The segment benefits from increasing surgical procedures and rising cases of chronic diseases that lead to wound complications. Hospitals also adopt standardized wound care protocols that include hydrogel dressings for moisture balance and tissue repair.

Growing investment in healthcare infrastructure is projected to improve access to advanced wound care treatments. Patients often receive initial wound management in hospitals before transitioning to other care settings, which reinforces product demand in this segment.

As healthcare systems continue to focus on improving patient outcomes and reducing healing time, hospitals are anticipated to retain their leading position in the hydrogel dressing market.

Key Market Segments

By Product

- Amorphous Hydrogel (Gels/Tubes)

- Impregnated Hydrogel (Gauze/Sponge-based)

- Sheet Hydrogel (Solid 3D Networks)

By Application

- Acute Wounds

- Chronic Wounds

By End-use

- Hospitals

- Specialty Clinics

- Home Healthcare

- Others

Drivers

Increasing prevalence of chronic wounds is driving the Hydrogel Dressing market.

The rising incidence of conditions such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers has substantially increased the demand for effective moisture-retaining wound care solutions. Hydrogel dressings facilitate a moist healing environment that promotes autolytic debridement and reduces pain during dressing changes.

Global estimates indicate that diabetic foot ulcers affect approximately 1.6 million individuals annually in the United States and 18.6 million worldwide, as reported in medical literature from November 2023. This demographic burden necessitates advanced dressings capable of managing exudate while minimizing infection risks.

Aging populations and higher rates of obesity and vascular disorders further contribute to sustained wound prevalence. Healthcare systems increasingly prioritize products that accelerate healing and lower complication rates.

Adoption in both hospital and home care settings reflects the clinical advantages of hydrogels in chronic wound protocols. Professional guidelines emphasize moisture balance as essential for optimal tissue repair. Consequently, this epidemiological pattern remains a core driver supporting market progression from 2022 through 2025.

Restraints

High costs of treatment and limited reimbursement are restraining the Hydrogel Dressing market.

Elevated expenses linked to hydrogel dressing production and application restrict accessibility, particularly in cost-sensitive healthcare environments. Specialized polymers and manufacturing processes contribute to higher pricing compared to traditional dressings. Inadequate reimbursement policies from payers discourage widespread adoption in public and private systems.

For instance, substantial out-of-pocket expenditures arise for chronic wound management, limiting patient and provider choices. Annual wound care expenditures in certain national health services reach billions, with surgical wounds and leg ulcers identified as particularly resource-intensive.

Regulatory compliance requirements add to development and approval costs, delaying market entry for innovative formulations. Smaller facilities face financial barriers in procuring advanced products despite clinical benefits.

These economic constraints slow replacement cycles and reduce overall utilization rates. Persistent gaps in coverage frameworks hinder equitable access across regions. As a result, such financial and policy-related factors exert ongoing restraint on broader market expansion during the specified period.

Opportunities

Development of bioactive and antimicrobial hydrogel formulations is creating growth opportunities in the Hydrogel Dressing market.

Incorporation of antimicrobial agents, such as silver or natural compounds, into hydrogel matrices addresses infection risks in chronic and acute wounds. These enhanced dressings provide sustained release mechanisms that combat bacterial colonization while maintaining a moist environment.

Opportunities extend to integration with growth factors or anti-inflammatory components for multifaceted therapeutic effects. Emerging applications target diabetic ulcers and burns, where infection control accelerates recovery. Partnerships between manufacturers and research entities facilitate clinical validation and scalability.

Potential for home-based use aligns with shifts toward outpatient care models. Advancements enable customization for specific wound types, broadening applicability.

Financial incentives from health systems support adoption of products demonstrating reduced healing times. This innovation pathway supports differentiation in competitive segments. Overall, bioactive enhancements generate significant prospects for diversified growth and improved clinical outcomes.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions and geopolitical dynamics are influencing cost structures, supply availability, and adoption patterns in the hydrogel dressing market. Rising healthcare expenditure and increasing chronic wound cases support steady demand, while inflation raises the cost of raw materials such as polymers and packaging, which affects pricing across care settings.

Budget constraints in public healthcare systems can slow bulk procurement, especially in developing regions. Geopolitical tensions disrupt supply chains for medical-grade inputs and create delays in product distribution across borders.

Current US tariffs on imported medical supplies and polymer-based components increase manufacturing costs and place pressure on margins for producers and distributors. These cost increases may translate into higher prices for hospitals and home care providers, impacting accessibility for some patients.

At the same time, tariffs are encouraging local production and regional sourcing strategies, which improve supply stability over time. Overall, despite short-term pricing and supply challenges, strong clinical need and ongoing product innovation are expected to support consistent market growth.

Latest Trends

Advancements in smart and stimuli-responsive hydrogel dressings represent a recent trend in the Hydrogel Dressing market.

In 2025, research has emphasized development of intelligent hydrogel platforms capable of responding to wound microenvironment changes such as pH, temperature, or reactive oxygen species. These dressings incorporate dynamic release systems for therapeutics, enabling targeted delivery of antimicrobials or antioxidants.

Publications highlight tri-layer designs that combine antibacterial action, sustained drug release, and structural support for chronic diabetic wounds. Stimuli-responsive properties facilitate real-time adaptation to healing stages without frequent interventions.

Integration of sensors or conductive elements supports monitoring of wound parameters. This evolution prioritizes multifunctional solutions over passive barriers. Clinical explorations demonstrate accelerated healing in infected models through synergistic antibiofilm and antioxidative effects.

The trend aligns with demands for reduced antibiotic reliance and personalized care. Continued focus in 2025 positions these innovations as transformative in advanced wound management. This shift toward responsive technologies redefines standards for efficacy and patient-centered application.

Regional Analysis

North America is leading the Hydrogel Dressing Market

North America accounted for 46.3% of the hydrogel dressing market in 2025 as hospitals and wound care centers expanded use of advanced moist wound healing technologies for chronic and acute wound management.

Healthcare providers across the United States and Canada increasingly rely on hydrogel-based dressings to treat burns, diabetic ulcers, and pressure injuries due to their ability to maintain a moist environment and promote tissue regeneration.

According to the Centers for Disease Control and Prevention, about 37.3 million people in the United States were living with diabetes in 2022, creating a large patient base at risk of chronic wounds that require advanced wound care solutions.

Wound care clinics are therefore adopting specialized dressings that support faster healing and reduce infection risk. Hospitals are integrating hydrogel products into standardized wound management protocols, particularly for patients with complex or slow-healing wounds.

Growth in home healthcare services has also increased demand for easy-to-apply wound care products suitable for outpatient settings. Medical device companies are introducing improved hydrogel formulations with enhanced absorption, antimicrobial properties, and longer wear time.

Clinical training programs are strengthening expertise in advanced wound care techniques among healthcare professionals. These developments collectively supported steady expansion of advanced wound care solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience strong growth during the forecast period as healthcare infrastructure improves and awareness of advanced wound care increases across the region. Countries such as China, India, Japan, and South Korea are witnessing rising incidence of diabetes, burns, and traumatic injuries that require effective wound management solutions.

The International Diabetes Federation reported that about 206 million adults were living with diabetes in the Western Pacific region in 2023, highlighting a significant population at risk of chronic wounds. Healthcare providers across the region are expanding wound care services and adopting modern dressings that improve healing outcomes.

Governments are strengthening public healthcare systems and promoting early treatment of chronic wounds to reduce complications. Hospitals and clinics are increasing procurement of advanced dressings that offer better moisture balance and patient comfort.

Regional manufacturers are developing cost-effective hydrogel products tailored to local healthcare needs. Training programs for healthcare professionals are improving knowledge of modern wound management techniques. These developments are expected to accelerate adoption of advanced wound care solutions across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Hydrogel Dressing market expand growth by advancing moisture-retentive wound care technologies, strengthening collaborations with hospitals and home healthcare providers, and developing bioactive gel formulations that support faster healing in acute and chronic wounds.

Companies invest in antimicrobial hydrogels, improved absorption capacity, and patient-friendly application formats that enhance comfort and reduce dressing change frequency. They also focus on expanding product portfolios and distribution networks to address rising demand across surgical wounds, burns, and diabetic ulcers.

Smith & Nephew represents a prominent participant in the Hydrogel Dressing market and operates as a UK-based medical technology company that develops advanced wound care solutions, orthopedic devices, and sports medicine products for global healthcare systems.

The company emphasizes innovation in wound management and clinical education to improve treatment outcomes. Industry competitors continue to introduce next-generation hydrogel products, strengthen clinical partnerships, and invest in advanced materials to support effective wound healing and sustained market growth.

Top Key Players

- Cardinal Health

- Smith & Nephew

- 3M (Solventum)

- ConvaTec Group PLC

- Medline Industries, Inc.

- Integra LifeSciences Corp.

- McKesson Medical-Surgical

- DermaRite Industries, LLC

- AMERX Health Care Corp.

Recent Developments

- In July 2025, ConvaTec obtained regulatory clearance in both the US and Europe for its Aquacel ConvaFiber dressing. The product builds on Hydrofiber technology to provide a gel-like wound environment that supports autolytic debridement while maintaining structural stability during removal, with broader commercialization planned for 2026.

- Following its public listing in early 2026, Medline reported sales of $28.4 billion for 2025 and outlined a strategic shift toward non-acute care settings. The company has initiated a series of educational programs focused on skin health, targeting clinicians in home care and long-term care facilities to improve wound management practices.

- In February 2026, SolasCure reported clinical results for its Aurase wound gel, which incorporates the enzyme tarumase to support debridement. The findings indicated significantly improved effectiveness compared to standard approaches, positioning the product as a promising advancement in hydrogel-based wound care as it progresses toward later-stage clinical evaluation.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 1.0 Billion |

| Forecast Revenue (2035) | US$ 1.6 Billion |

| CAGR (2026-2035) | 4.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Amorphous Hydrogel (Gels/Tubes), Impregnated Hydrogel (Gauze/Sponge-based) and Sheet Hydrogel (Solid 3D Networks)), By Application (Acute Wounds (Surgical & Traumatic, Burns) and Chronic Wounds (Diabetic Foot Ulcers, Pressure Ulcers, Venous Leg Ulcers and Others)), By End-use (Hospitals, Specialty Clinics, Home Healthcare and Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Cardinal Health, Smith & Nephew, 3M, ConvaTec Group PLC, Medline Industries, Inc., Integra LifeSciences Corp., McKesson Medical-Surgical, DermaRite Industries, LLC, AMERX Health Care Corp. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |