Global HDPE Pipes Market Size, Share, And Industry Analysis Report By Diameter (Less than 500 MM, 500 to 1000 MM, 1000 to 2000 MM, 2000 to 3000 MM, Greater than 3000 MM), By Grade (PE 80, PE 100), By Application (Irrigation Systems, Drainage and Sewage, Chemical Processing, Electrofusion Fittings), By End User (Municipal Corporation, Farmers, Oil and Gas Explorer, Builders), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183865

- Number of Pages: 384

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

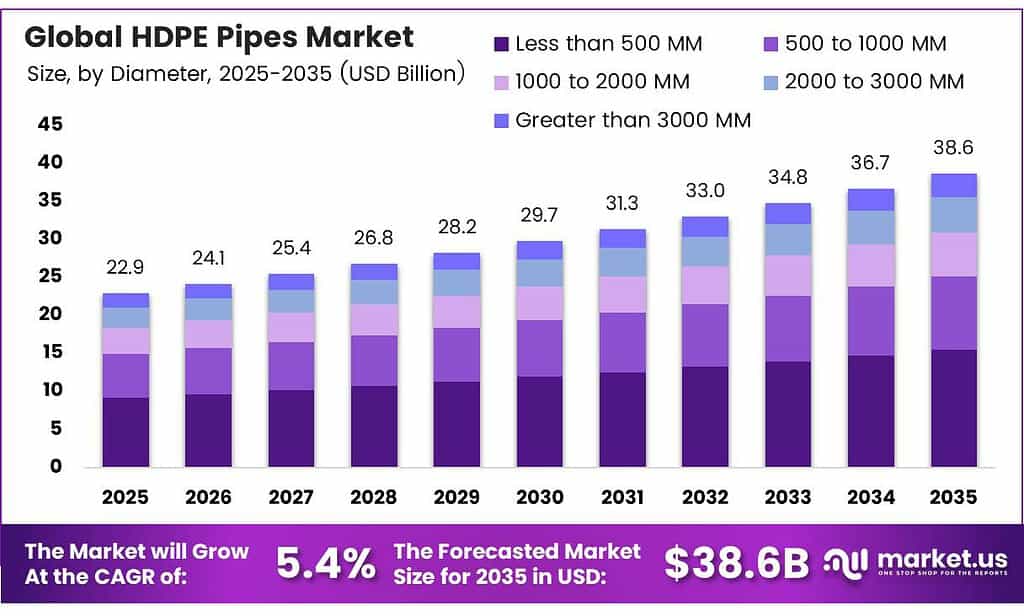

The Global HDPE Pipes Market size is expected to be worth around USD 38.6 billion by 2035 from USD 22.9 billion in 2025, growing at a CAGR of 5.4% during the forecast period 2026 to 2035.

The HDPE pipes market covers the production, distribution, and application of high-density polyethylene pipe systems used across water supply, irrigation, sewage, gas distribution, and industrial sectors. HDPE pipes offer superior corrosion resistance, flexibility, and long service life compared to traditional metal or concrete piping alternatives.

Municipal corporations, farmers, oil and gas operators, and construction companies drive strong demand for these water storage and transport solutions. Moreover, the lightweight nature of HDPE pipes reduces transportation and installation costs, making them a preferred choice for large-scale infrastructure projects worldwide.

Supreme Industries’ pipe systems sales volume reached 501,001 tons in India during FY2023-24, up from 375,046 tons in FY2022-23. This 125,955-ton year-over-year increase reflects strong domestic water infrastructure and irrigation demand, confirming HDPE pipe adoption as a primary growth engine across South Asian markets.

India’s plastic pipes exports under HS 3917 reached USD 361 million in 2024, ranking India as the 22nd largest exporter globally. This performance highlights India’s growing manufacturing capability and competitive export positioning in the global HDPE pipe supply chain.

Rapid urbanization in the Asia Pacific, Latin America, and Africa creates significant growth opportunities for piping system manufacturers. Additionally, rising awareness of water conservation and the need for efficient irrigation infrastructure push agricultural users toward modern HDPE-based harvesting solutions and drip systems.

Key Takeaways

- The Global HDPE Pipes Market is valued at USD 22.9 billion in 2025 and is projected to reach USD 38.6 billion by 2035 at a CAGR of 5.4% during the forecast period 2026 to 2035.

- Less than 500 MM holds the leading share at 35.6% in 2025.

- PE 100 dominates with 66.3% share in the HDPE pipes market in 2025.

- Irrigation Systems lead with 31.7% of the total market share in 2025.

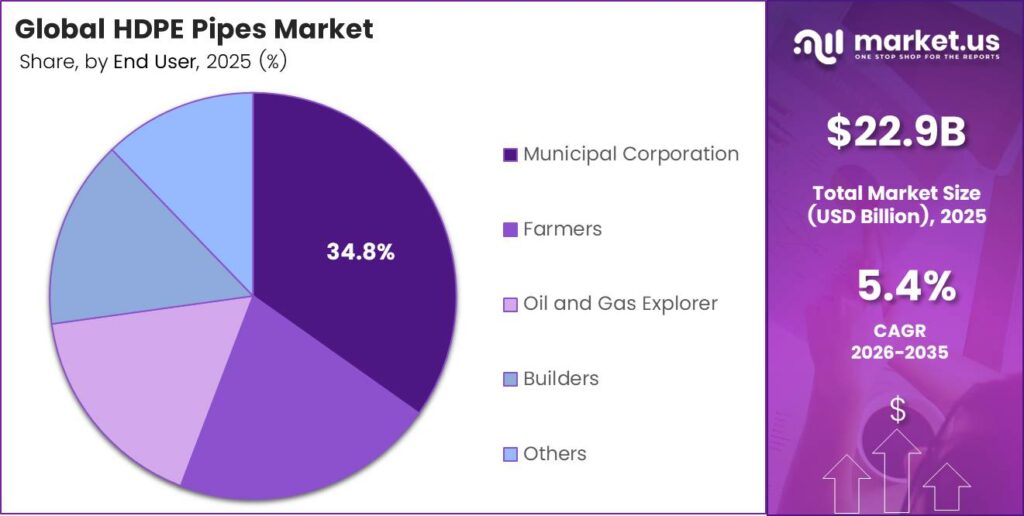

- Municipal Corporation holds the top position with 34.8% market share in 2025.

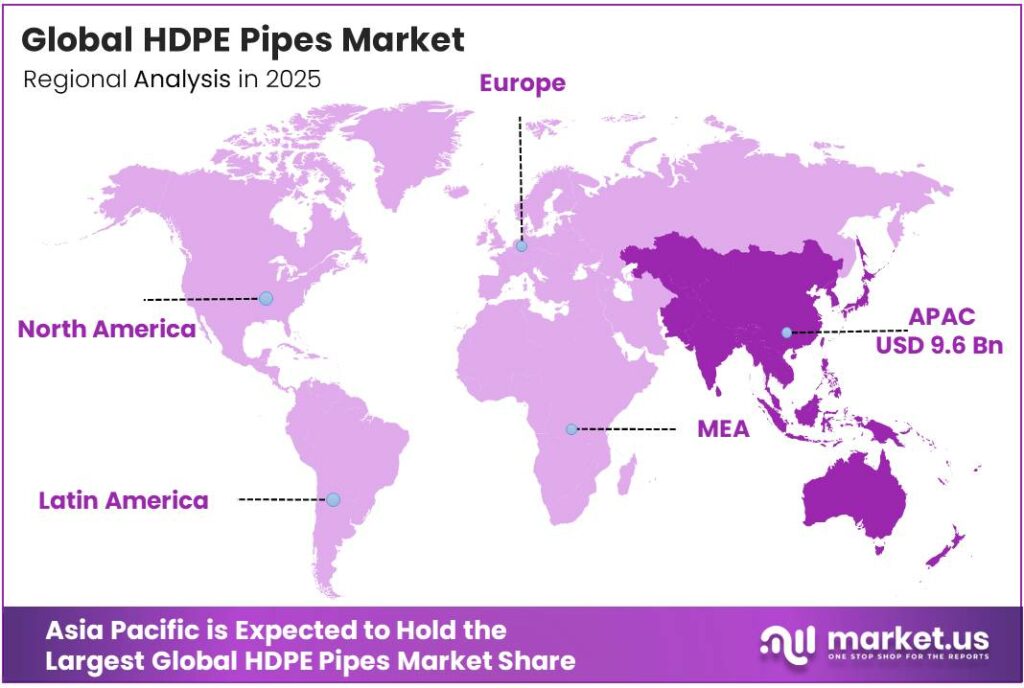

- Asia Pacific is the dominant region, holding 42.1% of the global market share, valued at USD 9.6 billion in 2025.

By Diameter Analysis

Less than 500 MM dominates with 35.6% due to widespread use in residential and agricultural piping networks.

In 2025, Less than 500 MM held a dominant market position in the By Diameter segment of the HDPE Pipes Market, with a 35.6% share. This size range serves residential water supply, small-scale irrigation, and sewage connections. Its affordability and ease of installation make it the preferred choice among farmers and municipal contractors across urban and peri-urban regions.

The 500 to 1000 MM diameter segment supports medium-scale water transmission and drainage networks. Therefore, municipalities and industrial developers commonly select this range for main supply trunk lines. Growing investments in urban water grid expansion and sewage upgrades drive consistent demand for this mid-range diameter category across emerging economies.

The 1000 to 2000 MM segment addresses large-scale water conveyance and industrial transfer needs. Consequently, this diameter range finds application in regional water supply projects and major sewage treatment connections. Infrastructure development programs in the Asia Pacific and the Middle East generate sustained procurement demand for this higher-capacity pipe category.

By Grade Analysis

PE 100 dominates with 66.3% due to superior pressure rating and durability for high-demand applications.

In 2025, PE 100 held a dominant market position in the By Grade segment of the HDPE Pipes Market, with a 66.3% share. PE 100 grade pipes offer higher pressure ratings and improved stress resistance compared to earlier standards. Consequently, infrastructure developers and municipal corporations prefer this grade for critical water transmission and gas distribution networks requiring long-term reliability.

The PE 80 grade retains a meaningful share in less demanding piping applications. Moreover, PE 80 pipes continue to serve agricultural irrigation, low-pressure drainage systems, and rural water supply schemes where the cost advantage outweighs the need for premium performance. Developing regions with cost-sensitive infrastructure budgets maintain consistent procurement of this grade.

By Application Analysis

Irrigation Systems dominate with 31.7% due to widespread agricultural adoption of efficient water delivery solutions.

In 2025, Irrigation Systems held a dominant market position in the By Application segment of the HDPE Pipes Market, with a 31.7% share. Agricultural modernization programs and water scarcity concerns push farmers toward HDPE-based drip and sprinkler systems. Additionally, government subsidies for irrigation infrastructure in countries like India and China accelerate market penetration in the agricultural sector.

The Drainage and Sewage application represents a key demand driver as cities expand wastewater management capacity. Therefore, urban planners and municipal engineers specify HDPE pipes for stormwater drainage, sewer rehabilitation, and effluent disposal systems. Their chemical resistance and long service life make them superior to concrete alternatives in sewage environments.

The Chemical Processing segment uses HDPE pipes for transporting aggressive fluids and industrial effluents. Moreover, HDPE’s excellent chemical resistance reduces maintenance costs and eliminates contamination risks in process plants. The oil and gas sector also relies on these pipes for safe chemical handling within refineries and production facilities.

By End User Analysis

Municipal Corporation dominates with 34.8% due to large-scale water supply and sewage infrastructure mandates.

In 2025, Municipal Corporation held a dominant market position in the By End User segment of the HDPE Pipes Market, with a 34.8% share. Governments worldwide fund municipal water supply, sewage treatment, and drainage upgrades that require large volumes of HDPE piping. Moreover, smart city initiatives and aging pipeline replacement programs sustain strong procurement activity among municipal buyers.

The Farmers segment forms a substantial customer base driven by irrigation system expansion. Therefore, agricultural users invest in HDPE pipe networks to support drip and sprinkler irrigation across field crops, horticulture, and livestock operations. Government subsidy schemes and micro-irrigation programs in Asia and Africa further stimulate farmer-level purchasing of HDPE irrigation products.

The Oil and Gas Explorer segment demands HDPE pipes for corrosion-resistant fluid transfer and chemical-safe line operations. Additionally, offshore and onshore drilling operations increasingly adopt HDPE pipes for produced water handling, chemical injection, and secondary containment systems where metal pipes pose corrosion and contamination risks.

Key Market Segments

By Diameter

- Less than 500 MM

- 500 to 1000 MM

- 1000 to 2000 MM

- 2000 to 3000 MM

- Greater than 3000 MM

By Grade

- PE 80

- PE 100

By Application

- Irrigation Systems

- Drainage and Sewage

- Chemical Processing

- Electrofusion Fittings

- Others

By End User

- Municipal Corporation

- Farmers

- Oil and Gas Explorer

- Builders

- Others

Emerging Trends

Trenchless Technologies and Advanced Jointing Drive Urban HDPE Pipe Adoption

Urban renewal projects increasingly favor trenchless installation methods for HDPE pipe deployment. These techniques minimize surface disruption, reduce project timelines, and lower costs in densely populated areas. Moreover, a surge in advanced extrusion and electrofusion jointing technologies enhances pipe joint strength and leak resistance, making HDPE systems more reliable for critical municipal and industrial infrastructure applications.

Eco-Friendly HDPE Solutions and Offshore Applications Gain Market Momentum

India’s HS 3917 pipe exports represented 0.064% of total merchandise exports in 2023, signaling growth headroom in international markets. Additionally, lightweight flexible HDPE pipes increasingly serve deep-sea and offshore slurry transport, while a shift toward eco-friendly designs with reduced carbon footprints aligns HDPE pipe systems with global green infrastructure goals.

Drivers

Global Infrastructure Investments and Urbanization Fuel HDPE Pipe Demand

Surging global investments in water supply, sewerage, drainage, and gas distribution networks create consistent procurement demand for HDPE pipe systems. Furthermore, rapid urbanization and smart city initiatives accelerate municipal infrastructure expansion. Global plastic pipes exports reached USD 4.62 billion from Germany alone in 2024, confirming strong international trade activity in this segment.

Corrosion Resistance Demand and Government Pipeline Replacement Policies

Escalating demand for corrosion-resistant piping in oil and gas exploration and drilling operations drives HDPE pipe adoption across energy sector end users. Therefore, operators replace legacy metal pipelines with durable HDPE solutions to reduce maintenance costs and downtime. Government policies and dedicated funding programs that mandate aging pipeline replacement further reinforce strong procurement growth across multiple regions.

Restraints

Raw Material Price Volatility Disrupts Cost Stability Across the Supply Chain

Persistent volatility in petrochemical raw material prices directly impacts HDPE pipe production costs and manufacturer margins. Since HDPE resin derives from ethylene, a petrochemical byproduct, global crude oil price fluctuations create unpredictable cost structures. Consequently, manufacturers struggle to maintain stable pricing for contractors and distributors, often leading to project delays and budget overruns in large infrastructure programs.

High Installation Costs and Project Delays Limit Market Accessibility

High initial installation expenses combined with project delays in large-scale construction present significant barriers to HDPE pipe market expansion. Moreover, skilled labor shortages for specialized jointing and pressure testing add to project costs. Therefore, smaller municipalities and budget-constrained infrastructure developers in developing regions often defer large HDPE pipe network upgrades despite recognizing the long-term performance benefits.

Growth Factors

Recycled HDPE and IoT-Enabled Smart Piping Systems Open New Growth Pathways

Rising adoption of recycled HDPE materials aligned with circular economy principles and green building certifications creates new market opportunities. Furthermore, the development of IoT-enabled smart HDPE piping systems for real-time leak detection and network monitoring adds significant value for municipal and industrial operators. Supreme Industries operates production capacity exceeding 750,000 metric tons annually in India as of 2025, demonstrating scale-driven efficiency gains.

Rural Market Expansion and High-Performance HDPE Innovations Accelerate Growth

Expansion into untapped rural and underserved regions for water, sanitation, and irrigation projects represents a major growth opportunity for HDPE pipe manufacturers. Additionally, innovation in multi-layer and high-performance HDPE designs enables use in extreme industrial and mining applications. Consequently, manufacturers invest in product development programs targeting both emerging market segments and technically demanding end-use scenarios worldwide.

Regional Analysis

Asia Pacific Dominates the HDPE Pipes Market with a Market Share of 42.1%, Valued at USD 9.6 Billion

Asia Pacific commands a 42.1% share of the global HDPE pipes market, valued at USD 9.6 billion in 2025. The region’s dominance reflects massive infrastructure investments across China, India, and Southeast Asia. Moreover, government-led water supply programs, rapid urbanization, and expanding agricultural irrigation networks drive sustained procurement of HDPE pipe systems at scale across the region.

North America maintains a strong market position driven by aging pipeline replacement programs and water infrastructure modernization initiatives. The United States leads regional demand as municipalities invest in lead pipe elimination and corrosion-resistant water supply upgrades. Additionally, the oil and gas sector in the Gulf Coast region sustains consistent demand for high-pressure HDPE piping solutions.

Europe presents a mature but steadily growing market for HDPE pipe systems, supported by EU environmental regulations and green infrastructure mandates. Germany and France lead regional consumption through large municipal water and sewage renewal contracts. Furthermore, sustainability requirements promoting recycled content and low-carbon construction materials align well with advanced HDPE pipe manufacturing capabilities across the region.

The Middle East and Africa region experiences growing demand driven by desalination plant expansions, water transmission projects, and oil and gas infrastructure investments. Gulf Cooperation Council countries fund large-scale water network upgrades to address water scarcity. Consequently, HDPE pipes gain preference over traditional materials due to their chemical resistance and suitability for harsh desert and coastal environments.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Advanced Drainage Systems operates as one of the world’s largest manufacturers of thermoplastic corrugated pipe and related water management products. The company focuses on high-density polyethylene pipe production for stormwater management, drainage, and sanitary sewer applications. Moreover, its extensive distribution network across North America positions it as a primary supplier to municipal and construction markets seeking reliable HDPE drainage solutions.

AGRU specializes in manufacturing high-performance plastic piping systems and geomembranes for industrial, environmental, and infrastructure applications. The company produces HDPE pipes with superior chemical resistance for use in chemical processing, mining, and water treatment sectors. Therefore, AGRU’s engineering expertise and focus on technically demanding end-use environments support its strong competitive positioning in European and global specialty markets.

Astral Pipes represents one of India’s leading manufacturers of HDPE and CPVC pipe systems for plumbing, agriculture, and industrial applications. The company serves a broad domestic customer base, including farmers, builders, and municipal contractors. Additionally, Astral Pipes continuously expands its product portfolio and manufacturing capacity to capture growth opportunities in India’s fast-growing water infrastructure and sanitation markets.

Jain Irrigation Systems Ltd. is a globally recognized manufacturer of irrigation systems and HDPE pipes serving agricultural markets across Asia, Africa, and the Americas. The company integrates HDPE pipe production with drip and sprinkler irrigation technologies to deliver complete water efficiency solutions. Consequently, Jain Irrigation’s focus on sustainable agriculture and water conservation aligns well with growing government programs promoting modern irrigation infrastructure.

Top Key Players in the Market

- Advanced Drainage Systems

- AGRU

- Al-Rowad Complex

- Astral Pipes

- Chevron Phillips Chemical Company LLC

- CHINA LESSO

- Cosmoplast Industrial Company LLC

- Dyka Group

- Florence Polytech

- Ionomr Innovations Inc.

- ISCO Industries

- Jain Irrigation Systems Ltd.

- JM EAGLE, INC.

- Saudi Arabian Amiantit Co.

- Supreme Industries Ltd.

Recent Developments

- In 2025, Astral is a leading Indian manufacturer of HDPE pipes for urban infrastructure, cable protection, drainage, and agriculture (e.g., D-Rex double-wall corrugated HDPE/PP pipes, TeleRex DWC PE pipes, Pre-StiRex sheathing ducts for post-tensioning in bridges/nuclear structures). Astral’s board approved the acquisition of Al-Aziz Plastics for manufacturing capabilities.

- In 2025, Chevron Phillips Chemical (CPChem) is a leading producer of polyethylene resins, including pipe-grade HDPE, through its Performance Pipe division (one of North America’s largest HDPE pipe producers). CPChem and QatarEnergy began construction of the Ras Laffan integrated polymers complex in Qatar, including HDPE units. This upstream expansion supports the long-term supply of high-quality pipe-grade polyethylene resins.

Report Scope

Report Features Description Market Value (2025) USD 22.9 Billion Forecast Revenue (2035) USD 38.6 Billion CAGR (2026-2035) 5.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Diameter (Less than 500 MM, 500 to 1000 MM, 1000 to 2000 MM, 2000 to 3000 MM, Greater than 3000 MM), By Grade (PE 80, PE 100), By Application (Irrigation Systems, Drainage and Sewage, Chemical Processing, Electrofusion Fittings, Others), By End User (Municipal Corporation, Farmers, Oil and Gas Explorer, Builders, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Advanced Drainage Systems, AGRU, Al-Rowad Complex, Astral Pipes, Chevron Phillips Chemical Company LLC, CHINA LESSO, Cosmoplast Industrial Company LLC, Dyka Group, Florence Polytech, Ionomr Innovations Inc., ISCO Industries, Jain Irrigation Systems Ltd., JM EAGLE, INC., Saudi Arabian Amiantit Co., Supreme Industries Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Advanced Drainage Systems

- AGRU

- Al-Rowad Complex

- Astral Pipes

- Chevron Phillips Chemical Company LLC

- CHINA LESSO

- Cosmoplast Industrial Company LLC

- Dyka Group

- Florence Polytech

- Ionomr Innovations Inc.

- ISCO Industries

- Jain Irrigation Systems Ltd.

- JM EAGLE, INC.

- Saudi Arabian Amiantit Co.

- Supreme Industries Ltd.

Our Clients

- 183865

- April 2026