Quick Navigation

Report Overview

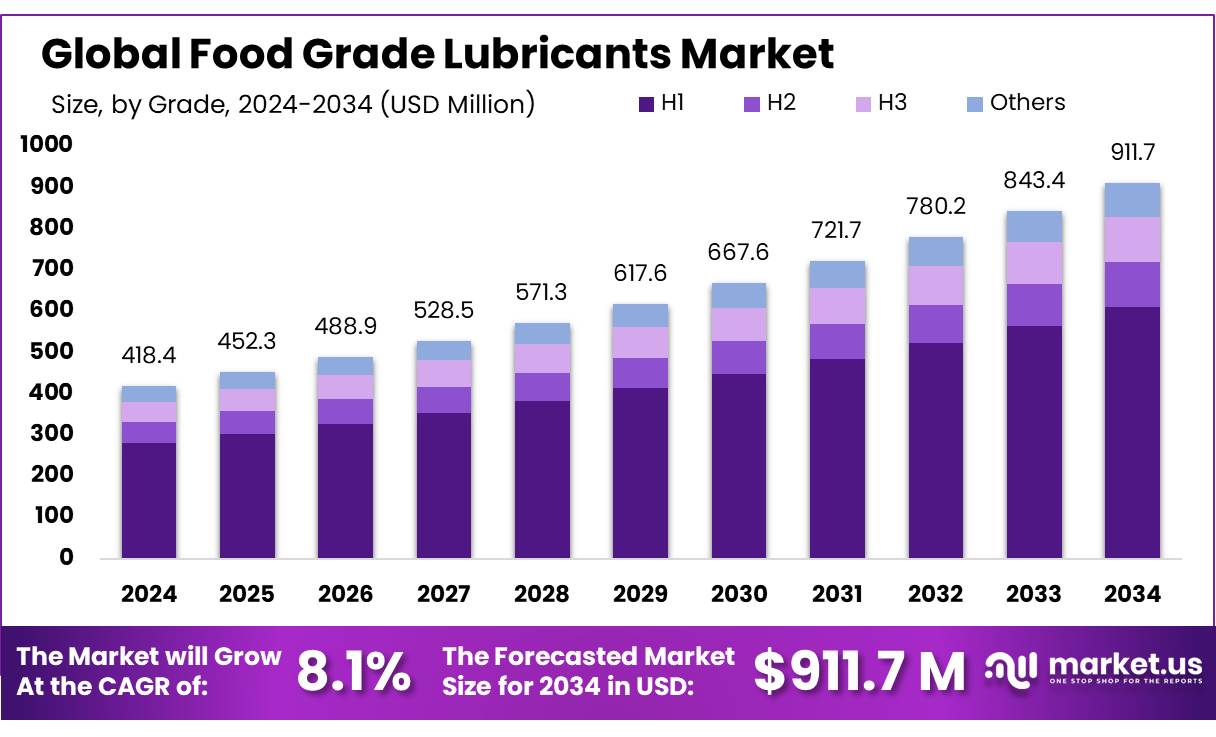

The Global Food Grade Lubricants Market size is expected to be worth around USD 911.7 Mn by 2034, from USD 418.4 Mn in 2024, growing at a CAGR of 8.1% during the forecast period from 2025 to 2034.

Food grade lubricants are specialized oils and greases formulated to meet stringent safety and hygiene standards for use in food processing environments. These lubricants are designed for incidental food contact, aligning with regulatory frameworks such as the U.S. Food and Drug Administration (FDA) 21 CFR 178.3570 and NSF H1 classification. They are widely used in applications including mixers, conveyors, packaging lines, and bottling equipment to ensure operational efficiency without compromising food safety.

Globally, food and beverage manufacturing is expanding, with the United Nations Food and Agriculture Organization (FAO) reporting that the global agri-food sector accounted for $9 trillion in economic output in 2023, roughly 10% of global GDP. This expansion directly fuels the demand for food-safe lubricants across the production chain.

According to the U.S. Department of Agriculture (USDA), the U.S. food and beverage industry alone reached $1.12 trillion in shipments in 2022, emphasizing the scale at which food-grade machinery operates and the growing requirement for compliant lubrication systems. Similarly, the European Commission’s Directorate-General for Agriculture and Rural Development reported €1.3 trillion in food sector turnover across EU-27 in 2022, highlighting the extensive scale of food machinery needing NSF-compliant lubrication.

Key drivers shaping the food-grade lubricants market include increasing food safety compliance regulations, automation in food processing, and the rise of clean-label production environments. The U.S. FDA’s Food Safety Modernization Act (FSMA), signed into law in 2011 and implemented through various guidelines since, mandates stringent preventive controls for food contact materials, thereby reinforcing the need for H1 or 3H lubricants. Furthermore, in India, the Food Safety and Standards Authority of India (FSSAI) issued a directive in 2021 recommending the exclusive use of food-grade lubricants in food processing units, reinforcing the regulatory emphasis.

Looking forward, emerging economies represent significant growth opportunities. According to China’s National Bureau of Statistics, the country’s food processing sector recorded a cumulative operating income of ¥14.3 trillion ($2.1 trillion) in 2022. With increasing export-oriented food manufacturing and rising internal consumption, lubricant adoption in hygienic machinery will intensify. Additionally, the Brazilian Ministry of Agriculture reported a 15% annual increase in food exports in 2023, indicating scale-up in food production infrastructure, and, by extension, lubrication needs.

Key Takeaways

- Food Grade Lubricants Market size is expected to be worth around USD 911.7 Mn by 2034, from USD 418.4 Mn in 2024, growing at a CAGR of 8.1%.

- H1 grade food lubricants firmly established themselves at the forefront of the market, securing a commanding 67.20% share.

- Mineral-based food lubricants commanded a significant presence in the market, holding a 43.40% share.

- Food grade oils held a dominant market position, capturing more than a 44.50% share.

- Low viscosity food grade lubricants captured a substantial market share of 37.50%.

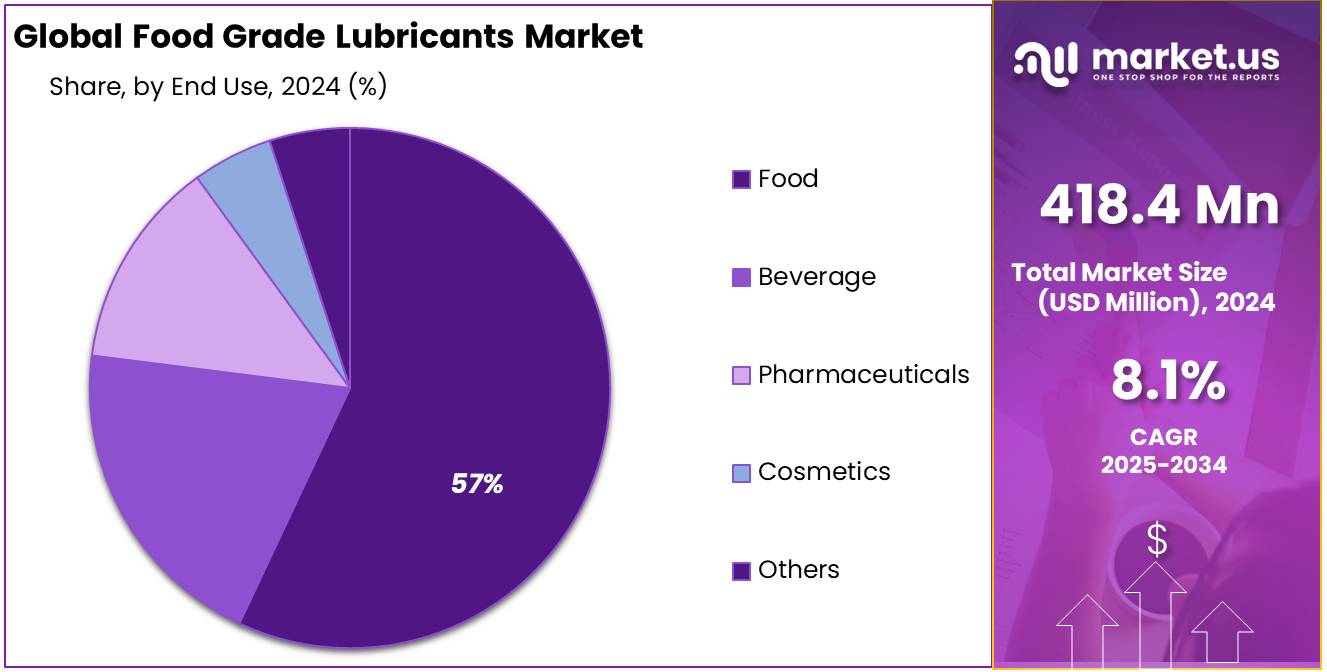

- Food sector held a dominant position in the food grade lubricants market, capturing a significant 57.50% share.

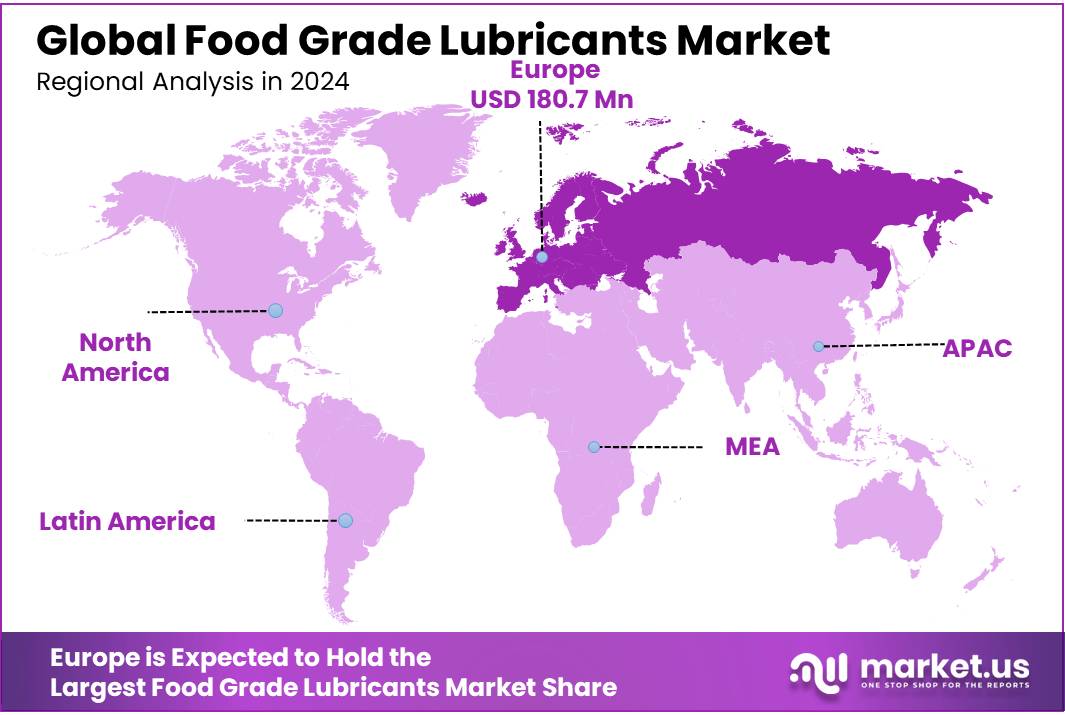

- Europe demonstrated a robust presence in the food grade lubricants market, capturing a significant 43.20% share, valued at approximately USD 180.7 million.

Analysts’ Viewpoint

From an investment perspective, the Food Grade Lubricants market is poised for growth with several compelling opportunities and some inherent risks. The market’s expansion is fueled by the increasing demand for processed foods and stringent food safety regulations which necessitate the use of high-quality lubricants in food processing equipment. As of recent estimates, the market has seen a significant push towards bio-based lubricants, driven by the growing emphasis on sustainability and environmental responsibility.

Investors should note the technological advancements that have enhanced the efficiency of lubrication systems, reducing equipment failure rates by up to 50% and thereby lowering maintenance costs significantly. Automated lubrication systems are becoming increasingly prevalent, improving the quality of products while reducing contamination risks.

Consumer insights also suggest a rising awareness of the ingredients in food products and their processing, influencing demand for lubricants that are safe and efficient. As consumers become more health-conscious, the push for transparency and safer, high-quality food products will likely continue to drive the demand for advanced food-grade lubricants.

By Grade

H1 Grade Food Lubricants Lead with 67.20% Market Share

In 2024, H1 grade food lubricants firmly established themselves at the forefront of the market, securing a commanding 67.20% share. This category of lubricants is particularly favored in the food processing industry due to its compliance with stringent safety standards, ensuring that they can safely come into contact with food products without risking contamination. This grade’s dominance is attributed to its critical role in maintaining the smooth operation of food processing equipment, coupled with a growing awareness amongst manufacturers about adhering to food safety regulations to avoid legal and health issues. The trust and reliability in H1 lubricants have made them an essential choice for businesses aiming to uphold high standards of food safety and equipment efficiency.

By Type

Mineral-Based Food Lubricants Lead with 43.40% Market Share

In 2024, mineral-based food lubricants commanded a significant presence in the market, holding a 43.40% share. These lubricants are favored in various food processing applications due to their cost-effectiveness and wide availability. Mineral lubricants are derived from refined petroleum, which makes them suitable for a range of equipment where food contact is incidental and not direct. Their ability to provide reliable lubrication under a variety of operating conditions ensures that they remain a preferred choice for manufacturers looking to balance performance with safety in their operations. The dominance of mineral-based lubricants in the market highlights their entrenched role in supporting the efficiency and safety of food production processes.

By Product Type

Food Grade Oils Command 44.50% Market Share Due to Versatility

In 2024, food grade oils held a dominant market position, capturing more than a 44.50% share. These oils are highly sought after in the food industry for their versatility and effectiveness in a wide range of applications. Food grade oils are used to lubricate food processing equipment, from baking conveyors to meat processing machines, where minimal food contact is inevitable. Their ability to maintain stability under high temperatures and provide long-lasting lubrication makes them indispensable in ensuring operational continuity and food safety. This substantial market share reflects their critical role in maintaining the efficiency and compliance of food processing operations.

By Viscosity Range

Low Viscosity Food Grade Lubricants Lead with 37.50% Market Share

In 2024, low viscosity food grade lubricants captured a substantial market share of 37.50%. These lubricants are favored primarily for their fluidity and ease of application, making them ideal for high-speed, less load-intensive food processing equipment. Their ability to operate effectively at lower temperatures and to coat machinery components thoroughly without excessive buildup contributes significantly to their popularity. This type of lubricant ensures that food processing operations run smoothly, with minimal risk of interruptions or mechanical failures, thereby upholding both efficiency and compliance with safety standards. The notable market share held by low viscosity lubricants underscores their essential role in the food industry’s operational toolkit.

By End-use

Food Sector Dominates Food Grade Lubricants with 57.50% Market Share

In 2024, the food sector held a dominant position in the food grade lubricants market, capturing a significant 57.50% share. This dominance is largely due to the critical need for specialized lubricants that meet strict food safety standards to prevent contamination during food processing. These lubricants are essential for the smooth operation of equipment in the baking, meat processing, dairy, and beverage industries, among others.

Their role in ensuring operational efficiency and compliance with health regulations makes them indispensable in the food production landscape. The substantial market share indicates the sector’s heavy reliance on high-quality, safe lubricants to maintain uninterrupted and safe food production processes.

Key Market Segments

By Grade

- H1

- H2

- H3

- Others

By Type

- Mineral

- Synthetic

- Polyalphaolefins (PAOs)

- Polyalkylene glycols (PAGs)

- Esters

- Others

- Bio-based

By Product Type

- Oil

- Grease

- Aerosol

By Viscosity Range

- Low

- Medium

- High

By End-use

- Food

- Bakery & Confectionery

- Dairy

- Meat, Poultry, & Seafood

- Animal Feed and Pet Food

- Sugar

- Others

- Beverage

- Carbonated Soft Drinks

- Fruit Beverages

- Sports Drinks

- Alcoholic Beverages

- Others

- Pharmaceuticals

- Cosmetics

- Others

Drivers

Stringent Food Safety Regulations Drive Demand for Food Grade Lubricants

One major driving factor for the growth of the food grade lubricants market is the stringent regulatory standards imposed by governments and international food safety organizations. These regulations are designed to ensure that all materials coming into contact with food, including lubricants, do not pose any risk of contamination.

For instance, according to the U.S. Food and Drug Administration (FDA), lubricants used in food processing equipment must comply with specific criteria to be considered safe for incidental food contact. These criteria are detailed under regulations like 21 CFR Part 178.3570, which outlines the requirements for lubricants with incidental food contact. These regulations mandate that the lubricants must be composed of substances that are recognized as safe when used under the intended conditions of use.

Furthermore, the Global Food Safety Initiative (GFSI), a coalition of some of the world’s leading food safety experts, emphasizes the importance of lubrication management in its Benchmarking Requirements. These requirements help food processing companies develop practices that ensure the safety and efficacy of lubricants used in production environments.

In Europe, the European Food Safety Authority (EFSA) provides guidelines similar to the FDA’s, focusing on the safety of chemicals used in food processing environments, including lubricants. Such regulations compel lubricant manufacturers to innovate and develop products that meet these rigorous standards, thereby driving the demand for food-grade lubricants.

Additionally, industry leaders like Nestlé and PepsiCo have implemented corporate policies that adhere to these strict food safety standards, further promoting the use of certified food grade lubricants in their production processes. These companies often publish their food safety protocols, which include standards for lubricants, on their official websites, reflecting their commitment to ensuring the safety and quality of their products.

Restraints

High Costs and Compliance Challenges Hinder Food Grade Lubricant Adoption

One significant restraining factor in the food grade lubricants market is the high cost associated with producing and maintaining compliance with stringent safety standards. These lubricants are specifically formulated to meet rigorous health and safety regulations, which can significantly drive up production costs compared to standard industrial lubricants.

For example, food grade lubricants must be made from ingredients that are either approved for use in food or are recognized as safe under various conditions of use. The United States Department of Agriculture (USDA) and the Food and Drug Administration (FDA) have clear guidelines and certifications for food grade lubricants, such as NSF H1 certification, which indicates that the lubricant is safe for incidental food contact. Achieving and maintaining these certifications requires ongoing testing and compliance efforts, which can be costly for manufacturers.

Furthermore, the market for food grade lubricants is significantly influenced by the global emphasis on food safety. Initiatives like the Food Safety Modernization Act (FSMA) in the U.S. aim to ensure the safety of food products by focusing on preventing contamination during manufacturing processes. This act puts additional pressure on lubricant manufacturers to produce products that not only meet but exceed regulatory requirements, adding to the cost burden.

These higher production and compliance costs can deter small to medium-sized enterprises (SMEs) in the food processing industry from adopting high-standard food grade lubricants. Instead, these businesses might opt for less expensive alternatives, which do not offer the same level of safety or quality assurance, potentially risking compliance with global food safety standards.

Opportunity

Expanding Food Industry in Emerging Markets Presents Growth Opportunities for Food Grade Lubricants

A major growth opportunity for the food grade lubricants market lies in the expanding food processing industry in emerging economies. As countries like India, Brazil, and China continue to experience rapid economic growth, their food industries are evolving correspondingly, leading to increased demand for food safety and production efficiency.

Governments in these regions are also stepping up their food safety regulations to align with international standards, influenced by organizations such as the World Health Organization (WHO) and the Food and Agriculture Organization (FAO). These initiatives aim to enhance food safety measures, which include stringent requirements for the lubricants used in food processing equipment.

For instance, the FAO and WHO jointly promote food safety guidelines that encourage the use of safe and effective food grade lubricants as part of good manufacturing practices. These guidelines help local food processors understand the importance of using certified lubricants to prevent food contamination, thus driving the demand for high-quality food grade lubricants.

Moreover, the growing middle class in these emerging markets is driving demand for processed foods, which requires more extensive and sophisticated food processing operations. This shift is creating significant opportunities for lubricant manufacturers who can provide products that meet the new regulatory and safety standards.

Trends

Sustainability Trends Shape the Future of Food Grade Lubricants

A significant trend in the food grade lubricants market is the shift towards sustainability and environmentally friendly products. As global awareness of environmental issues increases, food processors are seeking lubricants that not only meet safety and efficiency standards but also minimize environmental impact.

This trend is supported by various international guidelines and initiatives that encourage sustainable practices in industries, including food processing. For example, the United Nations Environment Programme (UNEP) actively promotes the adoption of sustainable manufacturing processes, which includes the use of environmentally friendly lubricants. These lubricants are designed to be biodegradable, non-toxic, and derived from renewable resources, thereby reducing the ecological footprint of food manufacturing facilities.

Additionally, major food corporations are committing to sustainability goals that influence their entire supply chain, including the types of lubricants used in their production processes. These companies are increasingly opting for food grade lubricants that offer reduced environmental impact, aligning with their corporate social responsibility (CSR) strategies and public expectations for environmental stewardship.

The trend towards sustainable lubricants is also driven by advancements in lubricant technology. Manufacturers are developing innovative formulations that provide the necessary performance characteristics required for food processing applications while being environmentally benign. These new formulations include lubricants made from vegetable oils and other renewable resources, which offer excellent lubricity, biodegradability, and lower toxicity compared to traditional petroleum-based products.

Regional Analysis

In 2024, Europe demonstrated a robust presence in the food grade lubricants market, capturing a significant 43.20% share, valued at approximately USD 180.7 million. This dominance is largely attributed to the region’s stringent regulatory landscape, which mandates the use of high-standard lubricants across the food processing industry to ensure safety and quality. European regulations, driven by agencies such as the European Food Safety Authority (EFSA), enforce strict compliance with food safety standards, which in turn fuels the demand for certified food grade lubricants.

Moreover, Europe’s focus on sustainability and environmental conservation significantly influences the types of lubricants that find favor in its markets. There is a growing preference for bio-based, environmentally friendly lubricants, which align with the EU’s aggressive environmental policies and the European Green Deal objectives. These factors not only drive innovation in product development but also enhance the adoption rates of advanced food grade lubricants designed to minimize environmental impact without compromising on performance.

The mature food and beverage manufacturing sector in Europe also plays a critical role in this market dominance. Countries such as Germany, France, Italy, and the United Kingdom host some of the largest food processing companies in the world, necessitating vast quantities of food grade lubricants to maintain smooth operational efficiencies and adhere to both regional and global food safety standards.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

DuPont is a leader in the development of specialty lubricants, including those certified for food-grade applications. Their products are designed to meet the rigorous standards required in food processing environments, offering superior performance in terms of safety, efficiency, and environmental impact. DuPont’s solutions help extend machinery life and reduce operational costs, reinforcing their strong position in the global food grade lubricants market.

Based in France, CONDAT is renowned for its wide range of lubricants tailored for the food industry. Their food-grade lubricants are non-toxic and designed to ensure maximum machinery uptime with minimal environmental impact. CONDAT’s commitment to innovation and adherence to international food safety standards makes it a trusted name in the food processing sector.

TotalEnergies offers a comprehensive line of food grade lubricants known for their safety, efficiency, and sustainability. These products meet stringent international standards and are suitable for a wide range of food processing applications. TotalEnergies focuses on providing solutions that enhance energy efficiency and reduce carbon footprints, aligning with global sustainability goals.

ExxonMobil is a major player in the food grade lubricants market, offering high-performance products under the Mobil brand. These lubricants are engineered to tackle the challenges of food and beverage processing, including high temperatures and contamination risks. ExxonMobil’s strong R&D capabilities ensure continuous improvement of their lubricant formulations to meet evolving industry demands.

Top Key Players

- DuPont de Nemours, Inc.

- CONDAT group

- TotalEnergies

- Exxon Mobil Corporation

- CITGO Petroleum Corporation

- FUCHS Group

- Petro-Canada Lubricants Inc.

- Kluber Lubrication

- SKF

- Lanxess AG

- Clearco Products Co., Inc.

- The Lubrizol Corporation

- Elba Lubrication Inc.

- Other Key Players

Recent Developments

In 2024, Exxon Mobil Corporation continued to play a pivotal role in the food grade lubricants market, leveraging its extensive experience and technical expertise to meet the rigorous safety and performance demands of the food processing industry.

In 2024, TotalEnergies continued to strengthen its position in the food grade lubricants market, focusing on its flagship Nevastane range, which is specifically tailored for the food and beverage industry.

In 2024, DuPont de Nemours, Inc. continued to be a significant player in the food grade lubricants market, leveraging its advanced technology and expertise in specialty lubricants. DuPont’s MOLYKOTE® brand offers a range of lubricants tailored for the food and beverage industry, designed to meet the stringent requirements for safety and efficiency.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 418.4 Bn |

| Forecast Revenue (2034) | USD 911.7 Bn |

| CAGR (2025-2034) | 8.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Grade (H1, H2, H3, Others), By Type (Mineral, Synthetic, Bio-based), By Product Type (Oil, Grease, Aerosol), By Viscosity Range (Low, Medium, High), By End-use (Food, Beverage, Pharmaceuticals, Cosmetics, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | DuPont de Nemours, Inc., CONDAT group, TotalEnergies, Exxon Mobil Corporation, CITGO Petroleum Corporation, FUCHS Group, Petro-Canada Lubricants Inc., Kluber Lubrication, SKF, Lanxess AG, Clearco Products Co., Inc., The Lubrizol Corporation, Elba Lubrication Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |