Global Flavored Whiskey Market Size, Share, And Business Benefits By Type (Bourbon, Scotch, Malted, Blended, Others), By Flavor Type (Honey, Citrus, Caramel, Cider, Apple, Others), By Distribution Channel (Hypermarket and Supermarket, Modern Store Formats, Liquor Stores, Traditional Store Formats, Food and Drink Specialty Stores, Independent Liquor Stores, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: August 2025

- Report ID: 156613

- Number of Pages: 261

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

The Global Flavored Whiskey Market size is expected to be worth around USD 35.7 billion by 2034, from USD 19.0 billion in 2024, growing at a CAGR of 6.5% during the forecast period from 2025 to 2034.

The Flavored Whiskey Market is witnessing steady expansion, driven by shifting consumer preferences toward premium alcoholic beverages with unique taste profiles. From an industrial perspective, flavored whiskey has moved from being a niche product to a mainstream offering, with established brands and craft distillers experimenting with flavors such as honey, apple, cinnamon, and maple.

In Scotland, whisky production plays a major role in both national revenue and tourism. There are 148 operational Scotch whisky distilleries, which contributed £7.1 billion to the UK economy. Remarkably, Scotch whisky accounts for 77% of Scottish food and beverage exports. Many distilleries also attract tourists, with visitor centres drawing over 2.2 million visitors annually.

The largest, such as Glenlivet and Glenfiddich, each have a production capacity of 21,000,000 LPA. In contrast, smaller distilleries like Dornoch operate with a capacity of just 25,000 LPA. The production process begins with the wort, cooled to 20–25°C before being transferred into wooden or stainless-steel washbacks. Yeast is then added at a pitching rate of 2–4 × 10 cells/ml to start fermentation. Unlike brewing, the wort is not boiled, which allows further starch breakdown and the growth of microorganisms.

During fermentation, yeast converts malt-derived sugars, mainly maltose, into ethanol, carbon dioxide, and flavour compounds. The temperature naturally rises to about 33°C due to yeast activity. After around 30 hours, the fermentation is mostly complete, producing a wash with 8–10% ABV and a pH drop to 4.2. Many distilleries extend fermentation time to let lactic acid bacteria enhance flavour development.

Distillation is usually carried out in traditional copper pot stills through a double distillation process. The first run produces low wines with 20–25% ABV. The second run separates the distillate into foreshots, spirit cut, and feints. Only the spirit cut (about 70% ABV) is chosen for maturation, which must last at least 3 years in oak casks, as required by the Scotch Whisky Regulations.

Key Takeaways

- The Global Flavored Whiskey Market is expected to grow from USD 19.0 billion in 2024 to USD 35.7 billion by 2034, with a CAGR of 6.5%.

- Bourbon led the flavored whiskey market in 2024, holding a 38.5% share due to its rich taste and cocktail versatility.

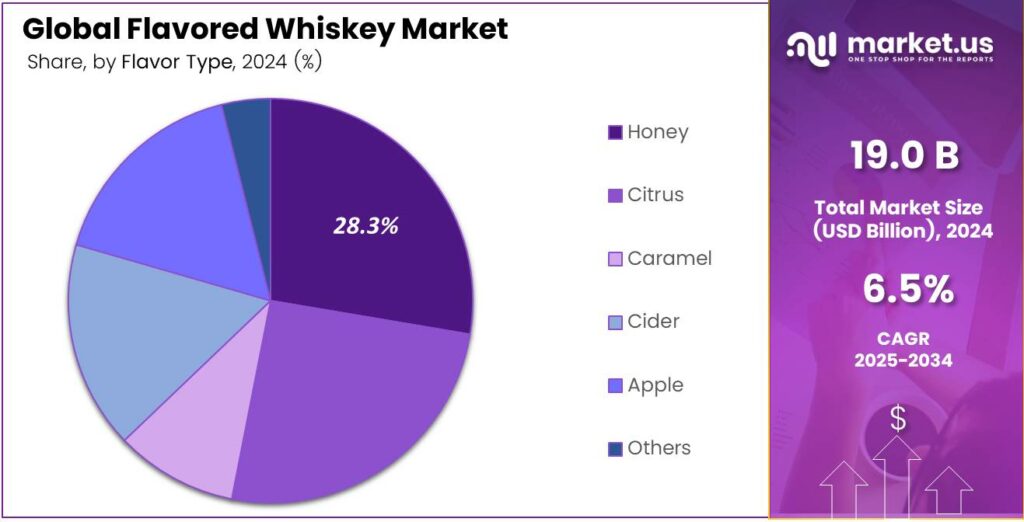

- Honey-flavored whiskey captured a 28.3% market share in 2024, popular for its smooth, approachable sweetness.

- Hypermarkets and supermarkets held a 27.4% share in 2024, driven by variety, discounts, and accessibility.

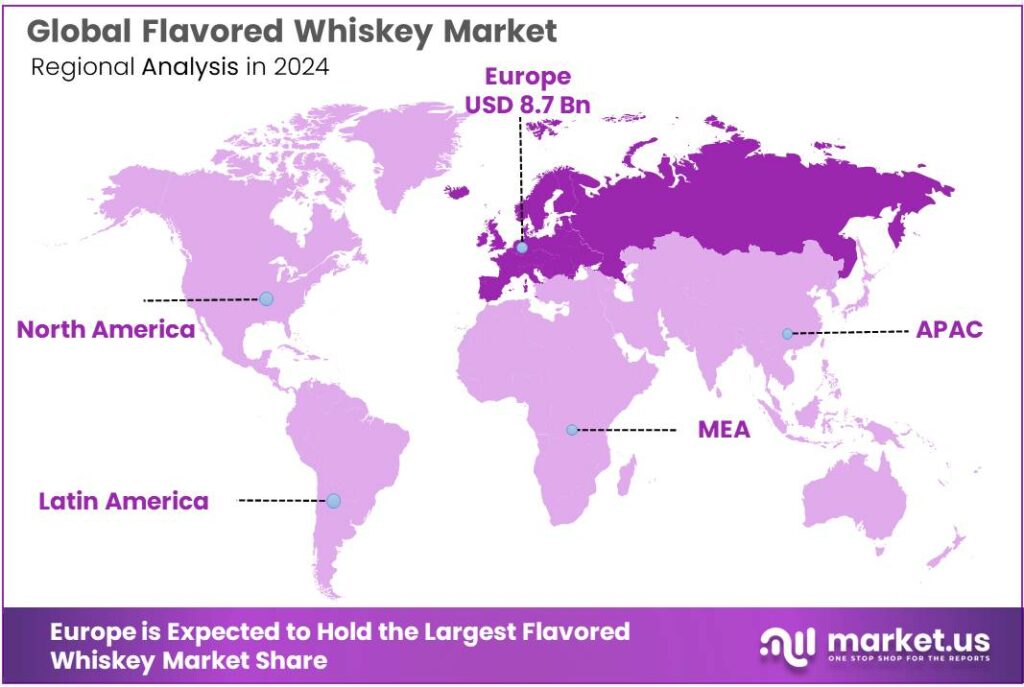

- Europe dominated the flavored whiskey market in 2024 with a 45.8% share, valued at USD 8.7 billion, led by Scotland and Ireland’s whiskey heritage.

Analyst Viewpoint

The flavored whiskey market is thriving, particularly among Gen Z and millennials, who are drawn to bold flavors like cinnamon, apple, and peanut butter. Investment opportunities are ripe in craft distilleries and established brands expanding their portfolios, as seen in the acquisition of Skrewball, a peanut butter-flavored whiskey, signaling a push toward premiumization.

Flavored whiskeys that offer unique experiences. Cocktail culture is a key driver, with flavored whiskeys being used in innovative mixes, appealing to younger audiences who value versatility and experimentation. The rise of craft distilleries in Europe and North America caters to this demand for authenticity and novel flavors, like herbaceous or spice-centric profiles, boosting consumer engagement through tastings and distillery tours.

The regulatory landscape is complex. New U.S. rules effective January 2025 provide clear standards for American single malt whiskey, aiding market legitimacy but increasing compliance costs. Proposed health warning labels could impact consumer perception if adopted. American whiskey adds pressure on exporters, pushing brands to explore Asia-Pacific and Latin American markets, which require investment in new logistics and marketing strategies.

By Type

Bourbon Leads with 38.5% Market Share

In 2024, Bourbon held a dominant market position, capturing more than a 38.5% share in the flavored whiskey market. This strong performance reflects the global appeal of bourbon’s unique taste profile, which combines rich caramel, vanilla, and smoky notes. Consumers increasingly prefer bourbon-based flavored whiskies for both traditional sipping and modern cocktail culture, making it a versatile choice across demographics.

By 2025, the demand is expected to strengthen further as premiumization trends and innovative flavor infusions expand bourbon’s presence in bars, restaurants, and retail shelves worldwide. This positions bourbon as a key driver of flavored whiskey growth.

By Flavor Type

Honey Flavor Dominates with 28.3% Market Share

In 2024, Honey held a dominant market position, capturing more than a 28.3% share in the flavored whiskey market. Its smooth sweetness and approachable taste have made honey-flavored whiskey especially popular among younger consumers and those new to whiskey drinking.

The balance between whiskey’s bold character and honey’s natural sweetness has also driven its success in both casual drinking and cocktail mixes. The category is expected to grow further as brands introduce new honey-infused blends and limited editions, reinforcing honey’s role as one of the most influential flavor types shaping flavored whiskey demand.

By Distribution Channel

Hypermarkets and Supermarkets Lead with 27.4% Share

In 2024, Hypermarket and Supermarket held a dominant market position, capturing more than a 27.4% share in the flavored whiskey market. Their wide product variety, attractive discounts, and convenient accessibility make them a preferred choice for consumers seeking both premium and affordable flavored whiskey options.

These retail formats provide strong visibility for leading brands through in-store promotions and dedicated beverage sections. The segment is expected to grow further as supermarkets expand premium liquor sections and urban consumers increasingly rely on organized retail outlets for trusted purchases, solidifying their role as a key sales channel for flavored whiskey.

Key Market Segments

By Type

- Bourbon

- Scotch

- Malted

- Blended

- Others

By Flavor Type

- Honey

- Citrus

- Caramel

- Cider

- Apple

- Others

By Distribution Channel

- Hypermarket and Supermarket

- Modern Store Formats

- Liquor Stores

- Traditional Store Formats

- Food and Drink Specialty Stores

- Independent Liquor Stores

- Others

Drivers

Government Policy and Trade Initiatives Boosting Domestic Whiskey

A key factor fueling the growth of flavored whiskey and whiskey in general across India is the push from government policies and trade initiatives that foster local production while easing export and operational hurdles. It’s this supportive environment that helps domestic distillers thrive and expand.

In Uttar Pradesh, a major hub for liquor manufacturing, government reforms have made a big difference. The number of functioning distilleries there rose from 61 to 85. In that same period, production almost doubled from 170 billion litres to 348 billion litres.

Exports saw a dramatic upturn too, surging 155% from 292 million litres to 743 million litres. These improvements were driven by policy shifts such as single-window approvals, digitized governance systems, and lower export duties on extra neutral alcohol (ENA), all of which made operations smoother and more investor-friendly.

Restraints

The Primary Concern: Health and Wellness Trends

The most significant restraint facing the flavored whiskey industry is the powerful, global shift in consumer behavior towards health and wellness. People are becoming increasingly conscious of what they put into their bodies, and this scrutiny extends directly to alcoholic beverages. The perception of flavored whiskeys, often sweetened and calorie-dense, clashes with this new health-conscious ethos.

While a traditional whiskey might be sipped slowly, flavored variants can be easier to drink quickly, which can lead to concerns about higher sugar and calorie intake per sitting. This isn’t just a niche trend; it’s a mainstream movement backed by major public health organizations.

The World Health Organization (WHO), for instance, has consistently highlighted the direct link between alcohol consumption and an increased risk of various health issues, including cancers and liver disease. Their reports suggest that no level of alcohol consumption is entirely safe for your health, a sobering message that is resonating with a generation more invested than ever in longevity and well-being.

Opportunity

The Driving Force: Capturing a New Generation of Drinkers

The single biggest engine for flavored whiskey’s growth is its remarkable ability to welcome new drinkers into the world of spirits, particularly millennials and legal-age Gen Z consumers. For many, the traditional, robust taste of straight whiskey can be too intense, a bit of an acquired taste that takes time to appreciate. Flavored whiskeys completely dismantle that barrier.

It’s less about confronting a strong spirit and more about enjoying a familiar, sweet flavor profile with a pleasant kick. This isn’t just a theory; it’s reflected in the very way people socialize. These sweeter, mixable options have become a staple at bars and home gatherings, allowing people to participate in a drinking culture without the initial bite that might have turned them away before.

This shift in consumer preference hasn’t gone unnoticed by the people who make our food and drink. The overall demand for more varied and approachable flavor experiences is a mega-trend that flavored whiskey taps into perfectly. While specific numbers on flavored whiskey are often tied to market firms, the broader data on flavor innovation is telling. The Food and Drug Administration (FDA), through its regulation of food additives and flavorings, oversees a massive market.

Trends

The New Frontier: The Demand for Natural and Authentic Ingredients

A powerful new factor shaping the future of flavored whiskey isn’t about a new wild flavor; it’s about what’s inside the bottle. After years of products dominated by artificial flavors and high fructose corn syrup, a significant shift is happening. Today’s drinkers are increasingly curious and concerned about where their food and drink come from.

They’re reading labels, not just for calorie counts, but for ingredients they can recognize and pronounce. This desire for authenticity is now a major emerging force in the flavored whiskey segment. This isn’t a fringe concern anymore; it’s moving into the mainstream, driven by a broader cultural push for transparency and natural goodness in everything we consume.

This trend is powerfully backed by consumer research from trusted, non-profit food organizations. The Consumer Brands Association, which represents the broader landscape of consumer-packaged goods, highlights that transparency is now a key purchasing driver. While they don’t poll specifically on whiskey, their data shows a massive consumer shift towards clean labels.

Regional Analysis

Europe: A Mature Market Holding 45.8% Share Valued at USD 8.7 Billion

In 2024, Europe emerged as the leading regional market for flavored whiskey, capturing 45.8% of the global share, equivalent to a market value of USD 8.7 billion. The region’s dominance is strongly linked to its deep-rooted whiskey heritage, particularly in countries such as Scotland and Ireland, where whiskey production is not only a cultural hallmark but also a significant contributor to economic growth.

The European spirits industry has also benefited from strong tourism and hospitality growth, with whiskey distilleries serving as major attractions. Countries like Scotland, which alone exports over a billion bottles of Scotch annually, have been quick to integrate flavored whiskey into their offerings to appeal to international and domestic markets.

Furthermore, urban nightlife trends in key cities such as London, Dublin, and Paris have supported flavored whiskey consumption, driven by a surge in cocktail culture and premium bar experiences. Another key factor strengthening Europe’s market leadership is the presence of established global players and distilleries, who are consistently innovating by introducing new flavors and limited-edition variants tailored to changing consumer palates.

The trend towards lower alcohol by volume (ABV) beverages and flavored spirits is also gaining momentum, further fueling growth across the region. Looking ahead, Europe is expected to maintain its dominant position, with ongoing product diversification and strong export demand ensuring sustained revenue expansion in the flavored whiskey sector.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Brown-Forman Corporation is a defining force in flavored whiskey, anchored by its iconic Jack Daniel’s Tennessee Honey. Its strength lies in powerful brand equity, extensive distribution, and strategic innovation, frequently launching new expressions like its ready-to-drink cocktails to capture evolving consumer trends. The company’s premium portfolio and consistent marketing investment solidify its dominant position.

Bacardi leverages its massive spirits portfolio and distribution muscle to make a significant impact in the category. Its key player is Dewar’s, with flavored expressions like Dewar’s Caribbean Smooth, which benefit from the brand’s established Scotch whisky heritage. This approach adds a layer of credibility and premiumness to its flavored offerings. Bacardi’s extensive global network and marketing prowess enable it to effectively introduce these products to a wide audience, competing directly with other major players.

Beam Inc. (Now Beam Suntory), the world’s best-selling bourbon, Beam Suntory holds a formidable position. Its flavored whiskey segment is driven by the successful Jim Beam Kentucky Fire and Kentucky Vanilla expressions. The strategy capitalizes on the core brand’s strong recognition and trust, making it an accessible choice for consumers exploring flavored variants. Beam Suntory’s extensive production capacity and global reach ensure its products are a ubiquitous and competitive presence in the market worldwide.

Top Key Players in the Market

- Brown-Forman Corporation

- Bacardi Limited

- Beam Inc.

- The Crown Royal Company

- Bird Dog Whiskey

- Distillery Co.

- Pernod Ricard SA

- Constellation Brands, Inc.

- Wild Turkey

- Knob Creek

Recent Developments

- In 2024, the company highlighted the product’s success and its role in driving growth in the flavored whiskey category, particularly in the U.S. The brand has been positioned as a key player in the flavored spirits market, appealing to younger consumers and those seeking innovative flavor profiles.

- In 2024, Bacardi noted the growing demand for flavored spirits, including whiskey, as a driver for its portfolio expansion. Bacardi’s focus on premium spirits and cocktails suggests potential future exploration in flavored whiskey to compete with brands like Jack Daniel’s Tennessee Fire.

Report Scope

Report Features Description Market Value (2024) USD 19.0 Billion Forecast Revenue (2034) USD 35.7 Billion CAGR (2025-2034) 6.5% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Bourbon, Scotch, Malted, Blended, Others), By Flavor Type (Honey, Citrus, Caramel, Cider, Apple, Others), By Distribution Channel (Hypermarket and Supermarket, Modern Store Formats, Liquor Stores, Traditional Store Formats, Food and Drink Specialty Stores, Independent Liquor Stores, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Brown-Forman Corporation, Bacardi Limited, Beam Inc., The Crown Royal Company, Bird Dog Whiskey, Distillery Co., Pernod Ricard SA, Constellation Brands, Inc., Wild Turkey, Knob Creek Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Brown-Forman Corporation

- Bacardi Limited

- Beam Inc.

- The Crown Royal Company

- Bird Dog Whiskey

- Distillery Co.

- Pernod Ricard SA

- Constellation Brands, Inc.

- Wild Turkey

- Knob Creek

Our Clients

- 156613

- August 2025