Quick Navigation

Report Overview

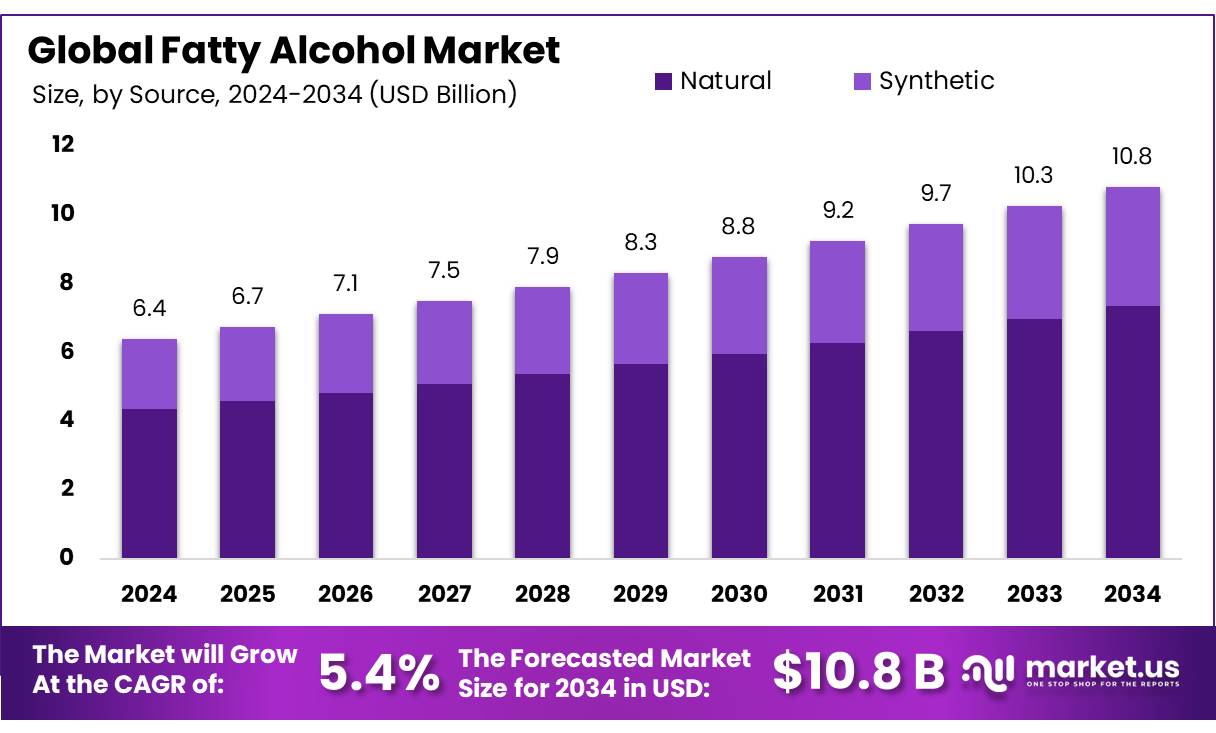

The Global Fatty Alcohol Market size is expected to be worth around USD 10.8 billion by 2034, from USD 6.4 billion in 2024, growing at a CAGR of 5.4% during the forecast period from 2025 to 2034.

Fatty alcohols are long-chain aliphatic alcohols typically derived from natural sources such as vegetable oils (e.g., palm, coconut, and soybean oils) or synthesized from petrochemical feedstocks. Characterized by carbon chain lengths ranging from C6 to C26, these compounds possess both hydrophobic and hydrophilic properties, making them amphipathic and particularly suitable for use in surfactants and emulsifiers. Fatty alcohols are widely utilized across multiple industries including personal care, cosmetics, pharmaceuticals, food processing, and detergents.

In cosmetic formulations, they function as thickeners, emollients, and emulsifiers, enhancing texture, stability, and skin feel. In household and industrial cleaning products, their surfactant properties offer efficient emulsification and dirt removal. The rising global demand for natural and sustainable ingredients in personal care products, coupled with the expansion of surfactant-based sectors, is fueling market growth.

Furthermore, the availability of cost-effective raw materials in emerging markets especially in Asia-Pacific strengthens production economics. The significance of fatty alcohols in modern industrial chemistry lies in their multifunctionality, renewability, and alignment with global sustainability trends. As consumer preferences shift toward bio-based and biodegradable ingredients, and as regulatory frameworks increasingly support green chemistry, fatty alcohols are emerging as important compounds in formulating eco-friendly products.

Key Takeaways

- The global fatty alcohol market was valued at US$ 6.4 billion in 2024.

- The global fatty alcohol market is projected to grow at a CAGR of 5.4% and is estimated to reach US$ 10.8 billion by 2034.

- Among sources, natural accounted for the largest market share of 68.2%.

- Among types, long chains accounted for the majority of the market share at 42.6%.

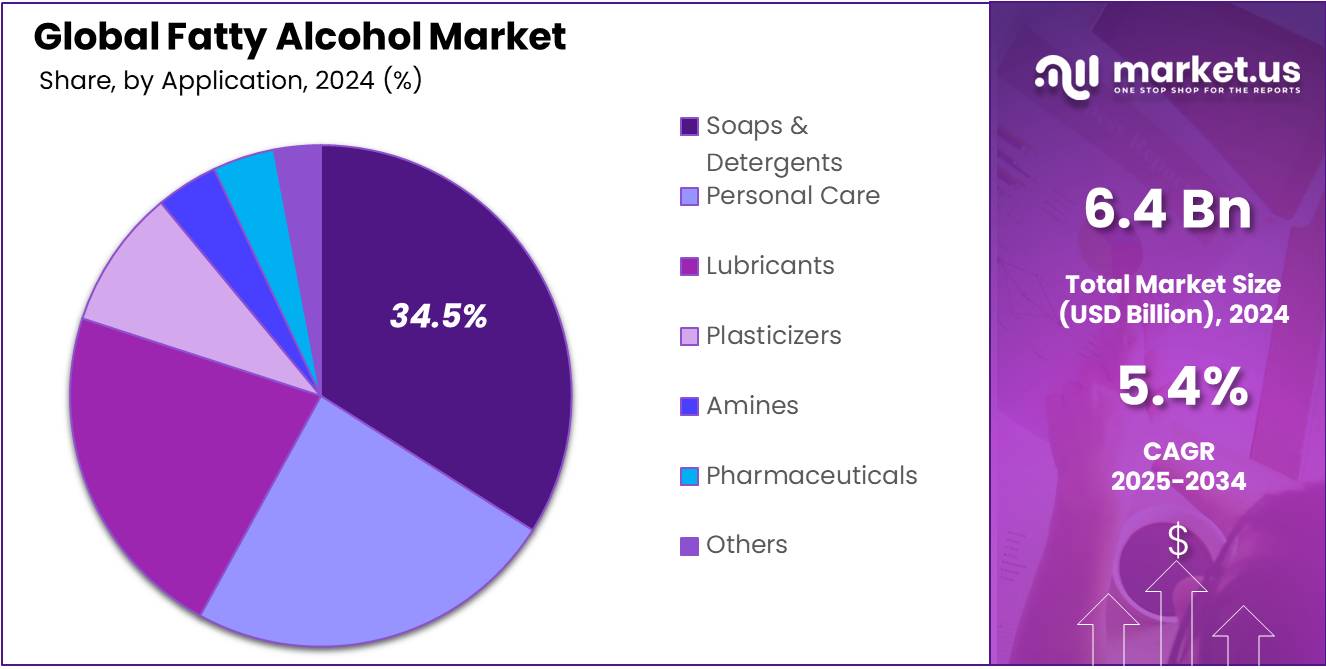

- By application, soaps and detergents accounted for the largest market share of 34.5%.

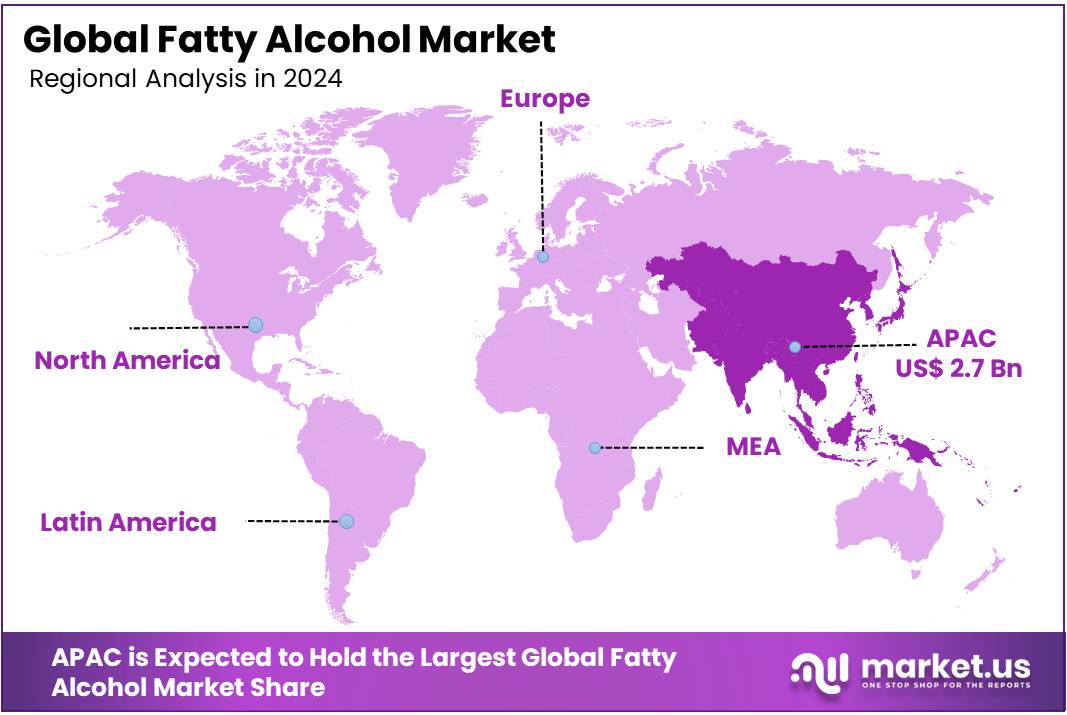

- Asia Pacific is estimated as the largest market for fatty alcohol with a share of 46.8% of the market share.

By Source

Naturally Sourced Fatty Alcohols Dominated The Market

The fatty alcohol market is segmented based source natural and synthetic. In 2024, the natural segment held a significant revenue share of 68.2%. Due to the growing consumer preference for bio-based and sustainable ingredients. Natural fatty alcohols, derived from sources like palm oil, coconut oil, and other vegetable oils, are increasingly favored in personal care, cosmetics, and home care products owing to their biodegradable nature and lower environmental impact. Additionally, regulatory support for green chemistry and rising awareness of ecological and health-related concerns further fueled the demand for naturally sourced fatty alcohols across key application sectors.

By Type

Long Chain Fatty Alcohol Type Leds Market Share Due To Its Extensive Use In Detergents And Personal Care Products For Superior Surfactant Properties.

Based on type, the market is further divided into short-chain, pure & mid-cut, long-chain, and higher-chain. The predominance of the long chain, commanding a substantial 46.6% market share in 2024. Due to its widespread use in the production of surfactants, detergents, and personal care formulations due to its excellent emulsifying and foaming properties. Long-chain fatty alcohols, typically derived from natural sources like palm and coconut oil, are preferred for their superior skin compatibility and moisturizing benefits. Their stability and effectiveness in various pH ranges make them ideal for formulations in cosmetics and industrial applications. Additionally, the growing demand for eco-friendly and sustainable ingredients further supports their market expansion.

By Application

Soaps and Detergent Segment Hold Largest Share In Fatty Alcohols Market.

Among applications, the fatty alcohol market is classified into soaps & detergents, personal care, lubricants, plasticizers, amines, pharmaceuticals, and others. In 2024, soaps & detergents held a dominant position with a 34.5% share. Due to the widespread use of fatty alcohols as key surfactants and emulsifying agents in cleaning products. Their excellent cleansing, foaming, and emulsification properties make them essential ingredients in both household and industrial detergents. Additionally, rising hygiene awareness, increased consumption of cleaning products, and the shift toward bio-based formulations have further fueled demand in this application segment.

Key Market Segments

By Source

- Natural

- Synthetic

By Type

- Long Chain

- Short Chain

- Pure and Mid cut

- Higher Chain

By Application

- Soaps and Detergents

- Personal Care

- Lubricants

- Plasticizers

- Amines

- Pharmaceuticals

- Others

Drivers

Rising Demand for Personal Care and Cosmetics

Rising demand for cosmetics and personal hygiene items driving the growth of the global fatty alcohol market growth. Driven by a confluence of factors including increasing consumer awareness of hygiene and well-being, coupled with evolving beauty standards influenced by social media increased demand for Fatty alcohols in a wide range of personal care products including skincare, haircare, and cosmetics due to their moisturizing, emulsifying, and thickening properties. They are valued for their emulsifying, wetting, dispersing, and foam control properties. Specifically, fatty alcohol ethoxylates and prophylaxes are commonly used as surfactants in cleaning agents and cosmetics.

- According to an article published by the National Library of Medicine, recent survey data reveals that Americans spend an average of 144 minutes per day on various social media platforms, highlighting social media usage has raised awareness of personal well-being, thereby boosting the demand for fatty alcohols used in health and personal care products.

Furthermore, shift toward natural and eco-friendly cosmetic formulations. Consumers increasingly seek products with plant-based, biodegradable components, prompting manufacturers to incorporate fatty alcohols derived from renewable sources. Fatty alcohols are key surfactants and emollients in conditioners, shower gels, and lipsticks, where their moisturizing and biodegradable nature aligns with consumer preference for natural, sustainable personal care products. There is a growing trend toward natural and organic cosmetics that use fatty alcohols derived from renewable sources. These products benefit from fatty alcohol’s non-irritating, moisturizing, and anti-acne properties, which are highly valued by consumers seeking safe, eco-friendly skincare.

Restraints

Competition from Alternative Material

The global fatty alcohol market is experiencing notable restraints due to the growing availability and adoption of alternative materials across various end-use industry ies. Synthetic and natural substitutes such as lanolin, cholesterol, and fatty acid esters are increasingly being utilized in personal care and beauty products, offering similar functional benefits as fatty alcohols while meeting consumer demand for natural and organic formulations. These alternatives are often more readily available and easier to integrate into product formulations, enhancing their appeal in daily-use applications.

Moreover, sectors such as personal care, detergents, and industrial manufacturing are increasingly prioritizing cost-efficiency, performance, and durability—areas where emerging substitutes are proving highly competitive. Technological advancements in synthetic chemistry and material science are further narrowing the performance gap, enhancing the sustainability and effectiveness of these alternatives. As a result, the widespread availability and growing preference for alternative raw materials are constraining the growth trajectory of the fatty alcohol market, especially in price-sensitive or mass-market product segments.

Opportunity

Adoption of Fatty Alcohol In Bio-Based Fuels Develo pment.

The global push toward sustainable energy is accelerating the adoption of biofuels, with fatty alcohols emerging as a valuable alternative to fossil fuels. As industries worldwide prioritize decarbonization and governments introduce net-zero emissions targets, fatty alcohols—derived from renewable sources such as palm oil, coconut oil, and other plant-based materials—offer a cleaner, biodegradable solution. These compounds can be processed into biodiesel and iso-paraffin-rich fuels suitable for use in transportation, including aviation.

Their compatibility with current fuel infrastructure and significantly lower carbon footprint make them a compelling choice for replacing petroleum-based energy sources. Biofuels made from fatty alcohols are gaining momentum, particularly in sectors such as aviation and heavy transport, where sustainable fuel options are urgently needed. Medium- and long-chain fatty alcohols (C8–C18) can undergo catalytic conversions to produce jet fuel components or be transformed into esters for biodiesel blends.

This growing trend is reinforced by strong regulatory support, technological advancements, and increased investments in biofuel infrastructure. As a result, the integration of fatty alcohols into renewable fuel production presents a significant growth opportunity for the global fatty alcohol market, particularly as industries and consumers alike demand more sustainable energy solutions.

Trends

Rising Demand For Natural And Sustainable Options

The global cosmetics, pharmaceutical, and personal care industries are undergoing a transformative shift, fueled by growing consumer awareness around health, wellness, and environmental sustainability. As more individuals prioritize clean-label products with natural, plant-based ingredients, the demand for fatty alcohols derived from renewable sources such as palm kernel oil and coconut oil is on the rise. These alcohols serve as essential emulsifiers, emollients, and thickeners in formulations, making them highly valuable for brands aiming to meet clean beauty and sustainability standards.

Consumers are actively seeking products free from synthetic chemicals, preservatives, and artificial additives, which aligns closely with the use of naturally sourced fatty alcohols. This trend is especially prominent in the personal care and cosmetic sectors, where transparency, ingredient traceability, and eco-friendliness have become key purchasing drivers. In addition, manufacturers are increasingly shifting towards fatty alcohols to formulate their product lines and develop new, sustainable offerings creating substantial opportunities for growth in the global fatty alcohol market.

Geopolitical Impact Analysis

The global fatty alcohol market is increasingly influenced by geopolitical factors, particularly concerning trade regulations, environmental policies, and raw material sourcing. Rising trade tensions and protectionist policies have led to the imposition of tariffs and countervailing duties, such as India’s recent CV duty on saturated fatty alcohols imported from Indonesia, Malaysia, and Thailand. These measures, aimed at protecting domestic industries, have disrupted supply chains and increased production costs for personal care and pharmaceutical sectors.

Moreover, geopolitical instability in key producing regions can affect the availability and pricing of natural feedstocks such as palm and coconut oil, which are crucial for fatty alcohol production. Additionally, growing international pressure to reduce deforestation and enforce sustainable sourcing practices is prompting regulatory shifts that impact the global flow of raw materials. Together, these geopolitical dynamics are forcing manufacturers to diversify sourcing, invest in local production capabilities, and enhance supply chain resilience.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Fatty Alcohol Market

In 2024, Asia Pacific dominated the global Fatty Alcohol market, accounting for 46.8% of the total market share, Driven by abundant natural resources such as palm and coconut oil. Countries like Indonesia, Malaysia, and the Philippines are major producers of these key feedstocks, ensuring a stable and cost-effective supply chain. Meanwhile, China and India are experiencing strong demand growth due to expanding personal care, home care, and industrial manufacturing sectors.

Rising urbanization, increasing disposable incomes, and a growing middle class are shifting consumer preferences toward natural and sustainable products. This is fueling greater adoption of bio-based fatty alcohols, especially in cosmetics, detergents, and pharmaceuticals. Moreover, regional governments are actively supporting green chemistry and renewable energy initiatives, creating a favorable environment for sustainable chemical manufacturing. These factors collectively position Asia-Pacific as a powerhouse for both production and consumption in the fatty alcohol industry.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Key Players In The Fatty Alcohol Market Dominate The Market Through Strategic Innovation.

Key players in the global fatty alcohol market play a crucial role in shaping industry dynamics through strategic investments, product innovation, and global expansion. Companies such as Kao Corporation, Godrej Industries, Sasol Limited, Wilmar International, Procter & Gamble Chemicals, and Emery Oleochemicals are among the leading players. These firms adopted advanced supply chain policies, sustainable sourcing practices, and production technologies to maintain market competition.

- For instance, Kao has committed to expanding its use of palm oil alternatives, while Godrej Industries is investing significantly in capacity expansion in India. Sasol remains a key synthetic fatty alcohol producer.

The presence of these players across multiple regions ensures a diversified supply base, while their focus on sustainability and innovation supports the evolving demand for natural, biodegradable, and eco-friendly fatty alcohols in personal care, detergents, and industrial applications.

Top Key Players

- Shell plc

- Kao Corporation

- Global Green Chemicals Public Company Limited.

- Sasol Limited

- Wilmar International Ltd

- Godrej Industries Limited

- Musim Mas Group

- KLK OLEO

- P&G Chemicals

- SABIC

- VVF Ltd

- PTT Global Chemical Public Company Limited

- CREMER OLEO GmbH and Co. KG

- Arkema

- Sinarmas Cepsa Pte. Ltd.

- Other Key Players

Recent Developments

- In March 2025 – Kao entered into a purchase agreement with Future Origins to secure a majority of the production capacity of NALO, a palm oil alternative fatty alcohol (C12/C14), from its first manufacturing plant. This move supports Kao’s global expansion of sustainable raw materials in its chemical and consumer product businesses and aligns with its decarbonization goals for 2040 and 2050.

- In March 2025 – Godrej Industries Ltd is investing ₹600 crore to expand its chemical manufacturing units in Gujarat and Maharashtra, with 83% allocated to a single Gujarat facility. The company aims to double its turnover to ₹5,000 crore within the next 3–4 years.

- In May 2025 – Musim Mas, through its subsidiary Masurf Inc., agreed to acquire Stepan’s manufacturing facility in Bauan, Philippines, to expand its surfactant portfolio. This strategic move strengthens its capabilities in personal care, home care, and industrial applications, aligning with its vision for sustainable and innovative growth in the oleochemicals sector.

- In Feb 2025 – KLK OLEO established a new representative office, KLK OLEO India (KLKOI), in Mumbai to strengthen its presence in the Indian market. This expansion aims to deepen customer relationships, enhance distribution networks, and tap into growing demand across sectors such as personal care, pharmaceuticals, and industrial chemicals while reinforcing its commitment to sustainable oleochemical solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.4 Billion |

| Forecast Revenue (2034) | USD 10.8 Billion |

| CAGR (2025-2034) | 5.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Natural, Synthetic), By Type (Long Chain, Short Chain, Pure and Mid cut, Higher Chain), By Application (Soaps and Detergents, Personal Care, Lubricants, Plasticizers, Amines, Pharmaceuticals, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Shell plc, Kao Corporation, Global Green Chemicals Public Company Ltd., Sasol Ltd., Wilmar International Ltd., Godrej Industries Ltd., Musim Mas Group, KLK OLEO, PandG Chemicals, SABIC, VVF Ltd., PTT Global Chemical Public Company Ltd., CREMER OLEO GmbH and Co. KG, Arkema, Sinarmas Cepsa Pte. Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |