Quick Navigation

Report Overview

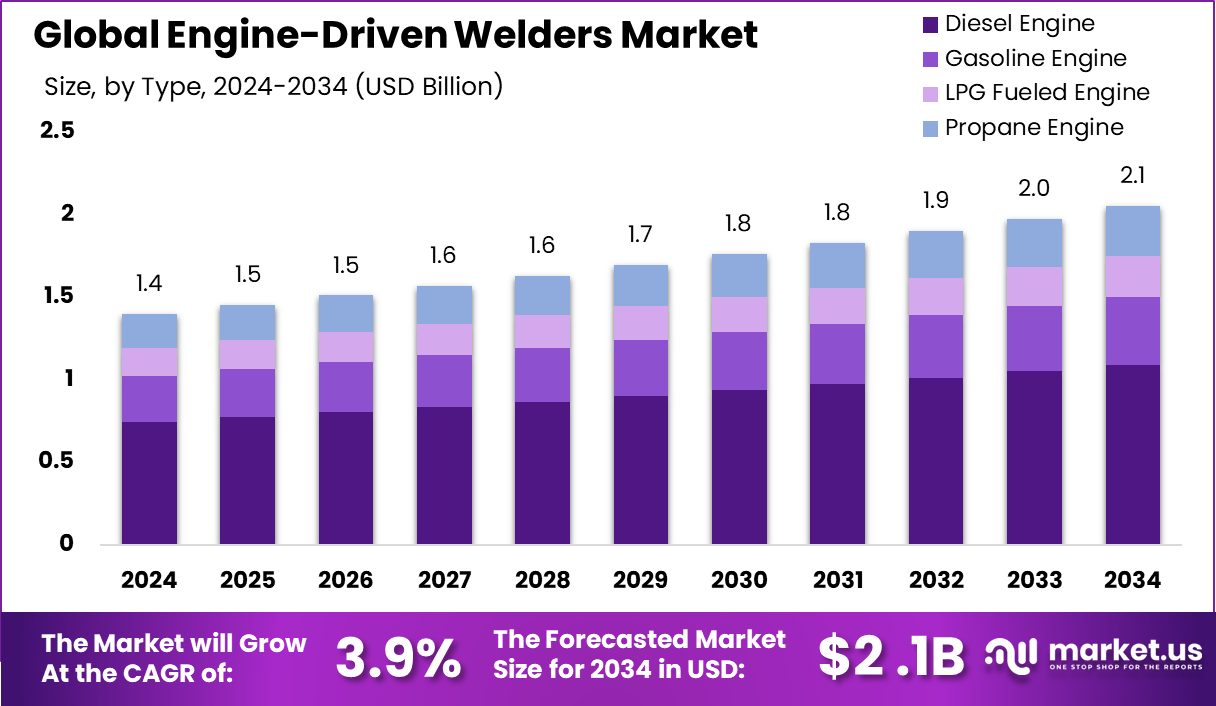

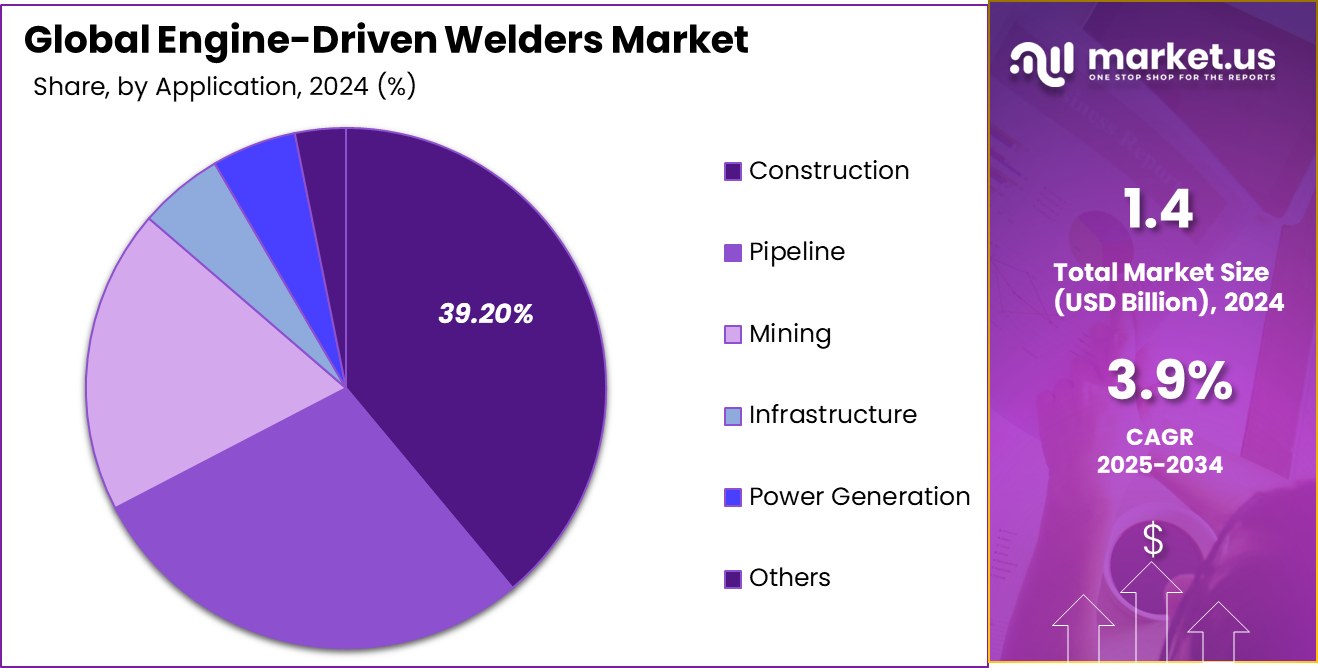

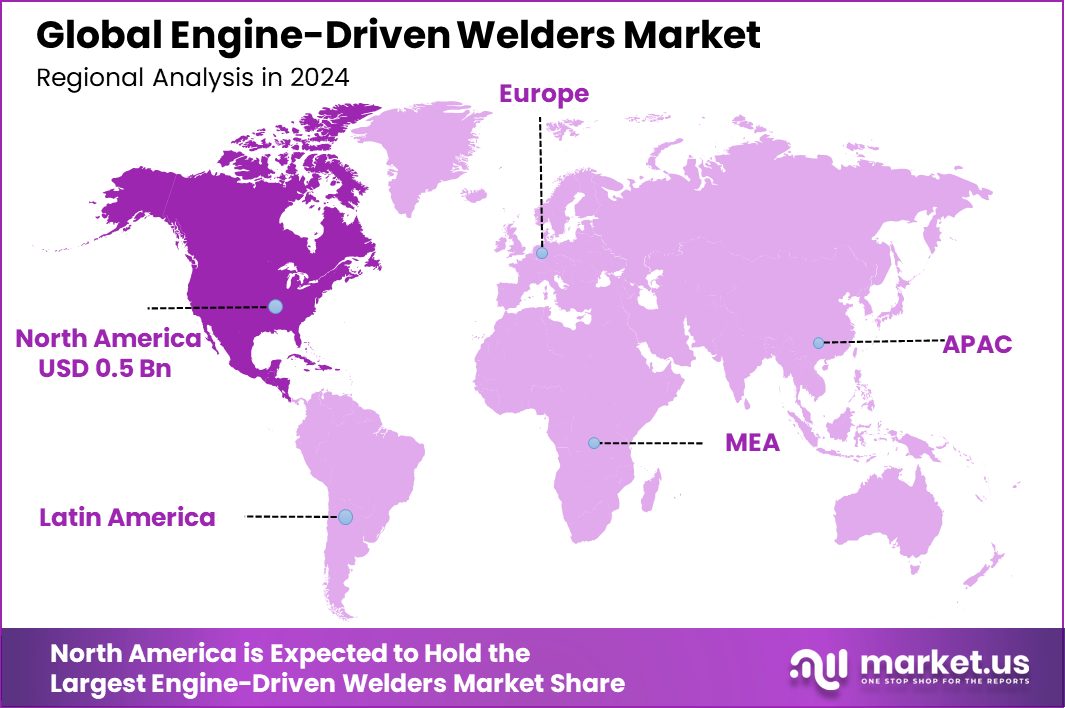

Global Engine-Driven Welders Market is expected to be worth around USD 2.1 billion by 2034, up from USD 1.4 billion in 2024, and grow at a CAGR of 3.9% from 2025 to 2034. With a market share of 38.20%, North America’s USD 0.5 billion segment leads growth.

Engine-driven welders are portable welding machines powered by internal combustion engines, typically gasoline or diesel, rather than relying on electricity. They are widely used in various industries for tasks that require mobility, such as construction, infrastructure projects, and remote work sites. These welders are known for their robust performance, versatility, and reliability, making them suitable for heavy-duty applications in environments without access to a stable electrical supply.

The engine-driven welders market is experiencing steady growth due to the increasing demand for portable and reliable welding solutions in the construction, oil & gas, and shipbuilding sectors. Their ability to operate in remote or outdoor locations, where access to electricity is limited, makes them indispensable for these industries. Additionally, the growth of the industrial sector and increasing infrastructure development contribute to the rising demand for engine-driven welders.

A key growth factor for engine-driven welders is the increasing need for mobility in welding operations. As industries expand into less accessible regions, the demand for portable and durable welding solutions will continue to rise. These machines are also favored for their ability to work in harsh conditions, making them ideal for a wide range of applications.

Opportunities in this market lie in technological advancements, particularly in improving fuel efficiency and reducing emissions. Innovations aimed at enhancing the efficiency, portability, and environmental footprint of engine-driven welders are expected to attract new customers and open doors to new markets. This could lead to more sustainable solutions while maintaining the high-performance standards required in industrial settings.

Key Takeaways

- Global Engine-Driven Welders Market is expected to be worth around USD 2.1 billion by 2034, up from USD 1.4 billion in 2024, and grow at a CAGR of 3.9% from 2025 to 2034.

- Engine-driven welders market sees a 37.20% share from welding currents up to 250 amps.

- Diesel engine-powered welders hold a dominant 53.20% share in market applications.

- Arc welding accounts for a significant 63.20% of the engine-driven welders market.

- The construction sector drives 39.20% of the engine-driven welders market growth.

- The North America strong performance, valued at USD 0.5 billion, underscores robust industrial activity.

By Welding Current Analysis

Upto 250 amp welding current holds a 37.20% market share.

In 2024, the Engine-Driven Welders Market was significantly influenced by the “Up to 250 amp” category within the By Welding Current segment, holding a dominant market position with a 37.20% share. This segment’s strong performance highlights its widespread acceptance and utility across various industries requiring substantial, yet manageable, welding power.

The preference for “Up to 250 amp” welders underscores the balance they offer between portability and adequate power for medium to heavy-duty tasks, making them ideal for both on-site repairs and remote operations where electricity is not readily available.

This market dominance also suggests robust sales driven by industries like construction, automotive repair, and infrastructure development, which often require reliable welding solutions that can be deployed in various environments.

The preference in this segment indicates a targeted demand for welders that offer a blend of efficiency, durability, and ease of use, catering specifically to professional welders and technicians who seek precision and reliability in their welding equipment.

By Type Analysis

Diesel engine-powered welders dominate the market at 53.20%.

In 2024, the Diesel Engine category asserted its dominance in the By Type segment of the Engine-Driven Welders Market, capturing a significant 53.20% market share. This commanding presence underscores the robust preference for diesel engines among users, primarily due to their reliability, efficiency, and longer operational lifespan compared to other engine types.

Diesel engine-driven welders are particularly favored in heavy industrial environments and outdoor applications, where their enhanced durability and superior power output are essential for heavy-duty welding tasks. The preference for diesel engines is also driven by their operational cost-effectiveness and ability to perform under challenging conditions, making them indispensable in sectors such as construction, pipeline work, and large-scale manufacturing.

Additionally, the higher energy density of diesel fuel translates into longer running times between refueling, a critical factor for projects in remote locations. This segment’s strong performance is indicative of a market that values robustness and efficiency, where diesel engine-driven welders continue to be the go-to choice for professionals seeking dependable, high-performance welding solutions in demanding industrial contexts.

By Welding Process Analysis

Arc welding accounts for 63.20% of the market share.

In 2024, Arc Welding dominated the by-welding process segment of the Engine-Driven Welders Market, securing a substantial 63.20% market share. This significant lead reflects the widespread adoption and dependability of arc welding techniques in various industrial applications.

The dominance of arc welding is attributed to its versatility and efficiency in joining metal parts through the use of an electric arc. This process is particularly suited for heavy-duty operations and is widely utilized in industries such as construction, automotive, and manufacturing due to its ability to create strong, high-quality welds in a variety of metals and thicknesses.

The preference for arc welding in engine-driven welders also stems from its adaptability to outdoor and on-site fabrication, where conditions can vary significantly. Furthermore, advancements in arc welding technology have enhanced its appeal by increasing efficiency and ease of use, making it accessible to a broader range of users, from skilled professionals to novices.

The robust market share of arc welding in this segment underlines its fundamental role in modern industrial activities, where precision, durability, and cost-effectiveness are paramount.

By Application Analysis

Construction application leads with a 39.20% share in the market.

In 2024, the Construction sector held a dominant market position in the By Application segment of the Engine-Driven Welders Market, with a 39.20% share. This significant market share reflects the essential role of welding in the construction industry, where it is pivotal for structural frameworks, pipework, and other critical joining tasks.

The high demand in the construction sector is driven by global infrastructure development and urbanization, which require robust and reliable welding solutions that can be deployed on-site and in varied environmental conditions.

Engine-driven welders are particularly valued in construction for their portability and independence from fixed power sources, allowing for flexibility in remote or newly developing areas without established electrical infrastructure.

The preference for these welders in construction also stems from their ability to provide consistent power for extended periods, crucial for completing large-scale projects efficiently. The dominance of construction in this market segment highlights the ongoing investments in infrastructure and the indispensable nature of welding technology in building and maintaining modern structural projects.

Key Market Segments

By Welding Current

- Upto 250 amp

- 250 amp to 400 amp

- Above 400 amp

By Type

- Diesel Engine

- Gasoline Engine

- LPG Fueled Engine

- Propane Engine

By Welding Process

- Arc Welding

- MIG Welding

- TIG Welding

By Application

- Construction

- Pipeline

- Mining

- Infrastructure

- Power Generation

- Others

Driving Factors

Increased Demand in Construction and Infrastructure

One of the primary driving factors for the Engine-Driven Welders Market is the booming construction and infrastructure sector. As urban areas expand and infrastructure projects multiply globally, the need for portable and efficient welding solutions is at an all-time high.

Engine-driven welders are especially crucial in locations where electrical supply is inconsistent or non-existent, such as in remote or developing regions. These machines empower construction crews to perform essential welding tasks without reliance on stationary power sources, enhancing productivity and enabling continuous work on critical projects.

The robust growth in construction activities, including roads, bridges, and buildings, directly correlates with increased demand for engine-driven welders, pushing market growth forward. This trend is expected to persist as infrastructure development continues to be a global priority.

Restraining Factors

High Initial Investment Limits Market Expansion

A significant restraining factor for the Engine-Driven Welders Market is the high initial cost of these machines. Engine-driven welders are generally more expensive than their traditional counterparts due to the sophisticated technology and the robust construction required to enable mobility and outdoor functionality. This high upfront cost can be a substantial barrier for small to medium enterprises (SMEs) and individual contractors who may find the investment prohibitive.

As a result, potential buyers often opt for rental solutions or purchase less expensive, less capable equipment, which limits market growth. The cost issue is particularly acute in developing regions, where budget constraints are more pronounced, potentially stifling the market expansion in these high-growth areas.

Growth Opportunity

Emerging Markets Offer New Growth Avenues

Emerging markets present a significant growth opportunity for the Engine-Driven Welders Market. As developing countries focus on expanding their infrastructure, there is an increasing need for robust, portable welding solutions that can operate independently of the grid. These regions often face challenges with electrical supply consistency, making engine-driven welders particularly valuable for construction and repair tasks in remote and rural areas.

The market potential is further enhanced by the ongoing industrialization and urbanization in these countries, which drives demand for new construction and maintenance of existing infrastructure. By capitalizing on these trends, manufacturers can tap into new customer bases and significantly expand their market reach, contributing to the overall growth of the sector.

Latest Trends

Integration of Advanced Technologies in Welding Equipment

A key trend in the Engine-Driven Welders Market is the integration of advanced technologies into welding equipment. Modern engine-driven welders are increasingly equipped with features such as improved engine efficiency, greater output consistency, and user-friendly digital interfaces. These enhancements not only boost the welder’s performance but also contribute to fuel efficiency and reduced emissions, aligning with global sustainability goals.

Additionally, the incorporation of technologies like remote monitoring and control systems allows for better precision and easier management of welding operations, especially in challenging field conditions. This trend towards technologically enhanced welders is driven by the growing demand for higher productivity and operational efficiency in industries such as construction and manufacturing.

Regional Analysis

North America holds 38.20% of the Engine-Driven Welders Market, valued at USD 0.5 billion.

The Engine-Driven Welders Market exhibits diverse performance across global regions, with North America emerging as the dominant region, holding 38.20% of the market share and valued at USD 0.5 billion. This leadership is largely driven by extensive infrastructure projects and a robust manufacturing sector. Europe follows with significant market activity, supported by its strong automotive and construction industries which demand reliable and portable welding solutions for on-site applications.

In the Asia Pacific, rapid industrialization and urbanization are propelling market growth, as countries like China and India invest heavily in infrastructure development. This region is anticipated to experience the highest growth rate in the coming years due to increasing industrial activities and infrastructural developments.

Meanwhile, the Middle East & Africa region, though smaller in comparison, is seeing growth due to increasing construction activities and the development of the oil and gas sector which relies heavily on welding for pipeline and facility maintenance.

Latin America, though holding a smaller share of the market, shows potential for growth driven by increasing industrial and construction activities, particularly in countries like Brazil and Mexico. Each region’s performance underscores the global reliance on durable and efficient welding solutions critical for industrial and construction resilience.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global Engine-Driven Welders Market was significantly shaped by the activities and strategies of key players such as Miller Electric, Lincoln Electric, and Kemppi, each bringing distinct advancements and regional strengths to the industry.

Miller Electric has maintained its position as a leader in the market through continuous innovation in product design and technology integration. The company’s focus on enhancing the energy efficiency and user-friendliness of its engine-driven welders appeals to a broad range of industries, from construction to manufacturing. Miller Electric’s strong distribution network across North America, combined with its reputation for durability and reliability, supports its substantial market share.

Lincoln Electric stands out for its commitment to expanding its reach in emerging markets, particularly in the Asia Pacific and Latin America. By tailoring its engine-driven welders to meet the specific needs of these regions, such as portability and robustness in diverse environmental conditions, Lincoln Electric has capitalized on rapid industrial growth and infrastructure development, enhancing its global footprint.

Kemppi, known for its innovative approach, focuses on the integration of digital solutions with traditional welding technology. The company’s advancements in remote operation and real-time welding analytics have positioned it as a forward-thinking player in the market. This approach not only improves operational efficiencies but also attracts a tech-savvy segment of the market, eager for next-generation welding solutions.

Top Key Players in the Market

- Miller Electric

- Lincoln Electric

- Kemppi

- ESAB

- Welding Industries of Australia

- Multiquip

- Denyo

- Jasic Technology

- Ingersoll Rand

- Wacker Neuson

- Perkins Engines

- Fronius

- Shindaiwa

- Yamaha Motor

Recent Developments

- In 2024, Denyo’s engine-driven welders segment grew 0.8% to ¥4,438 million, driven by steady overseas TIG welder shipments and strong domestic demand, despite parts shortages. The company held a dominant 55% market share in Japan for this segment.

- In 2024, Yamaha Motor is expected to expand its industrial engine applications, possibly enhancing its presence in engine-driven welders. With proven strength in power equipment and steady Marine segment growth, Yamaha may tap new utility machinery markets for diversified revenue streams.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.4 Billion |

| Forecast Revenue (2034) | USD 2.1 Billion |

| CAGR (2025-2034) | 3.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Welding Current (Upto 250 amp, 250 amp to 400 amp, Above 400 amp), By Type (Diesel Engine, Gasoline Engine, LPG Fueled Engine, Propane Engine), By Welding Process (Arc Welding, MIG Welding, TIG Welding), By Application (Construction, Pipeline, Mining, Infrastructure, Power Generation, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Miller Electric, Lincoln Electric, Kemppi, ESAB, Welding Industries of Australia, Multiquip, Denyo, Jasic Technology, Ingersoll Rand, Wacker Neuson, Perkins Engines, Fronius, Shindaiwa, Yamaha Motor |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |