Quick Navigation

- Key Takeaways

- By Discharge Pressure Analysis

- By Stage Configuration Analysis

- By Category Analysis

- By Drive Type Analysis

- By Compressible Gases Analysis

- By End-Use Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

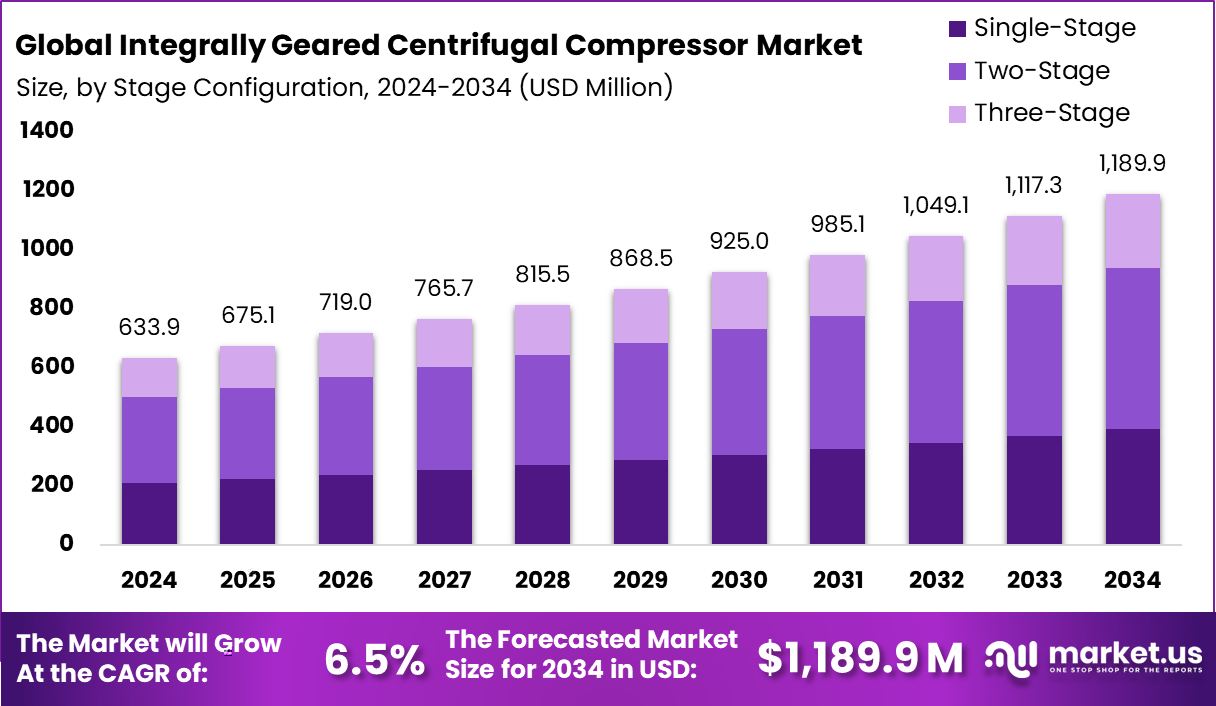

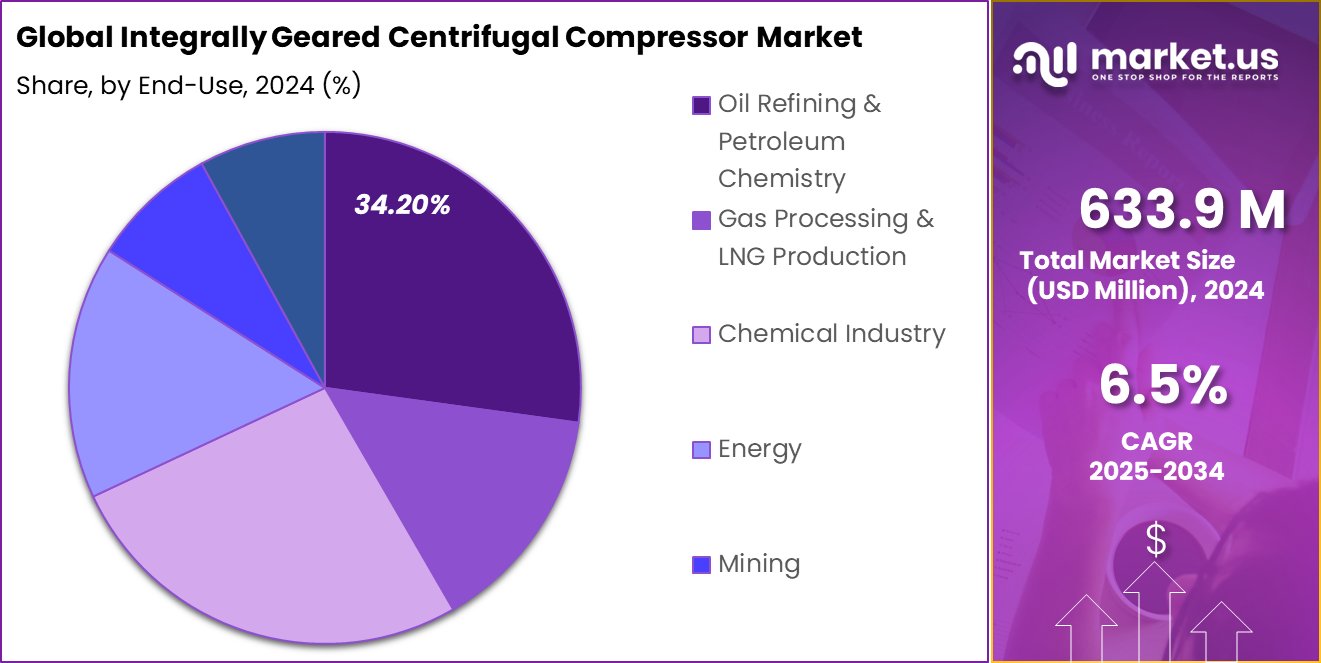

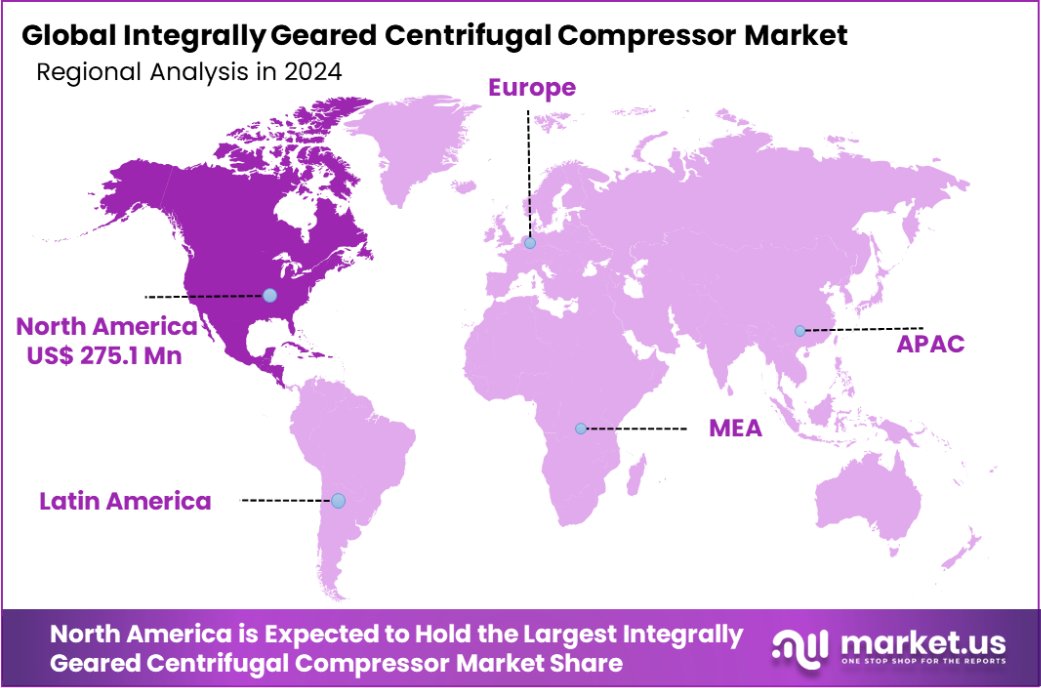

Global Integrally Geared Centrifugal Compressor Market is expected to be worth around USD 1,189.9 million by 2034, up from USD 633.9 million in 2024, and grow at a CAGR of 6.5% from 2025 to 2034. With a market share of 43.40%, North America’s Integrally Geared Centrifugal Compressor sector is worth USD 275.1 million.

An integrally geared centrifugal compressor is a sophisticated machine used primarily in gas, oil, and process industries for its efficiency in compressing gases. It features multiple compression stages arranged around a central gearbox, enabling each impeller to rotate at optimal speeds.

This design facilitates handling large capacities up to 600,000 cubic meters per hour and achieving high discharge pressures, up to 300 barg. Such compressors are valued for their exceptional performance and flexibility, catering to various industrial needs.

The integrally geared centrifugal compressor market is driven by a surge in demand across industries such as chemical processing, oil and gas, and power generation. This market benefits significantly from the push towards more energy-efficient systems and the expansion of industrial activities in emerging economies.

The market is also seeing innovation, such as Kobe Steel’s prototype compressor, which processes approximately 300,000 Nm³/h, showcasing the potential for high-capacity and efficient gas handling.

One key growth factor in the market is the increasing focus on energy efficiency. Companies are constantly seeking advanced technologies that reduce energy consumption and increase operational efficiency, making these compressors highly attractive. Additionally, the ability of these compressors to handle high pressure and large volumes efficiently supports their adoption in critical sectors that demand reliability and high performance.

The demand for integrally geared centrifugal compressors is bolstered by the global expansion of industries that require extensive gas movement and processing capabilities. As sectors like natural gas, petrochemicals, and renewables grow, the need for robust compression solutions escalates, directly benefiting the compressor market. The API-standard compressors in this category are particularly in demand due to their high availability rates—between 98.5 and 99.5% enhancing plant operability and reducing downtime.

Opportunities within the integrally geared centrifugal compressor market lie in technological advancements and geographic expansion. Innovations that offer improved compression efficiency, reduced maintenance costs, and extended lifecycles are likely to capture interest. Moreover, expanding industrial infrastructures in Asia-Pacific and the Middle East offer new opportunities for market growth, driven by increased investments in these regions’ oil and gas and chemical sectors.

Key Takeaways

- Global Integrally Geared Centrifugal Compressor Market is expected to be worth around USD 1,189.9 million by 2034, up from USD 633.9 million in 2024, and grow at a CAGR of 6.5% from 2025 to 2034.

- In the Integrally Geared Centrifugal Compressor Market, compressors with a discharge pressure of 100 to 200 Bar represent 43.40%.

- Two-stage integrally geared centrifugal compressors account for 46.80% of the market’s stage configuration segment.

- Oil-free compressors are preferred in 58.30% of applications, highlighting their significance in the market.

- Electric motor-driven compressors dominate the drive type category, making up 78.30% of the market.

- Hydrocarbon process gases are compressed using these systems in 31.20% of cases within the market.

- Oil refining and petroleum chemistry end-uses constitute 34.20% of the market, underscoring their industrial importance.

- The market for Integrally Geared Centrifugal Compressors in North America commands USD 275.1 million, representing a 43.40% regional share.

By Discharge Pressure Analysis

Discharge pressure 100 to 200 Bar dominates with 43.40% market share.

In 2024, the “100 to 200 Bar” range held a dominant market position in the “By Discharge Pressure” segment of the Integrally Geared Centrifugal Compressor Market, capturing a significant 43.40% share. This segment’s prominence is largely attributed to its critical role in numerous high-pressure applications across various industries, including oil and gas, petrochemicals, and energy. These sectors require reliable and efficient compressors capable of handling substantial pressures, making the 100 to 200 Bar compressors ideal for their needs.

The dominance of this segment is also reflective of ongoing industrial advancements and the increasing adoption of high-performance machinery to achieve greater operational efficiencies. As companies continue to prioritize sustainability and cost-effectiveness, the demand for integrally geared centrifugal compressors within this pressure range has surged. This trend is expected to continue, driven by the global push toward more energy-efficient technologies and the expansion of industrial activities that rely heavily on effective compression systems.

Moreover, the market’s inclination toward this discharge pressure range underscores the technological evolution within the compressor industry, where precision in pressure management translates to substantial gains in process control and output quality. This segment’s robust position in the market highlights its pivotal role in shaping the operational dynamics and future growth trajectories within the broader compressor landscape.

By Stage Configuration Analysis

Two-stage configuration holds a significant 46.80% of the market.

In 2024, the Two-Stage configuration held a dominant market position in the “By Stage Configuration” segment of the Integrally Geared Centrifugal Compressor Market, commanding a substantial 46.80% share. This configuration’s popularity is underpinned by its enhanced efficiency and capability to meet the varied pressure requirements of multiple industries, such as chemical processing, oil and gas production, and power generation. The two-stage configuration, which involves two levels of compression, enables better energy management and improved cost-effectiveness compared to single-stage compressors.

The dominance of the two-stage segment reflects the ongoing technological advancements that prioritize operational flexibility and energy savings in industrial processes. As industries continually seek optimized solutions for more complex and demanding environments, two-stage compressors provide a balance of performance and energy consumption, making them a preferred choice for applications requiring moderate to high pressure levels.

Furthermore, the market’s inclination toward two-stage compressors is indicative of a broader trend toward sustainable industrial practices. By reducing energy usage and enhancing performance, two-stage compressors contribute significantly to lowering operational costs and environmental impact, factors that are critically important as industries move towards greener solutions and more stringent regulatory compliance. This segment’s strong market share highlights its integral role in meeting the evolving needs of modern industries.

By Category Analysis

Oil-free compressors are preferred, comprising 58.30% of the category.

In 2024, the Oil-free category held a dominant market position in the “By Category” segment of the Integrally Geared Centrifugal Compressor Market, securing a significant 58.30% share. This commanding presence is primarily driven by the increasing demand for cleaner and more environmentally friendly industrial processes. Oil-free compressors offer the advantage of reducing contamination risks in sensitive environments, making them essential in industries such as pharmaceuticals, food and beverage, and electronics manufacturing, where purity of air supply is paramount.

The preference for oil-free compressors is also a reflection of stringent environmental regulations that necessitate the use of equipment that minimizes emissions and waste. As industries continue to face pressure to adhere to strict environmental standards, the adoption of oil-free integrally geared centrifugal compressors is expected to rise, reinforcing their market dominance.

Moreover, the technological advancements in oil-free compressor designs, which enhance reliability and reduce maintenance costs, further bolster their appeal. These compressors are not only capable of providing high-quality compressed air but are also designed to be energy efficient, aligning with the global push toward energy conservation and operational efficiency. The substantial market share held by the oil-free category underscores its critical role in supporting sustainable industrial practices.

By Drive Type Analysis

Electric motor drives lead, capturing 78.30% of the market.

In 2024, the Electric Motor drive type held a dominant market position in the “By Drive Type” segment of the Integrally Geared Centrifugal Compressor Market, with an impressive 78.30% share. This prevalence is largely due to the electric motor’s inherent advantages, including its reliability, efficiency, and lower maintenance costs compared to other drive types. Electric motors are highly favored in various industrial applications where consistent and efficient power delivery is critical.

The electric motor’s dominance in this market segment is also propelled by the global shift toward electrification and sustainable energy practices. Industries are increasingly opting for electrically powered equipment to reduce greenhouse gas emissions and comply with international environmental standards. This trend is particularly pronounced in sectors such as manufacturing, oil and gas, and utilities, where energy efficiency is closely monitored and continuously optimized.

Furthermore, the integration of advanced technologies like variable frequency drives (VFDs) enhances the functionality of electric motors in integrally geared centrifugal compressors, allowing for precise control over compressor speed and energy consumption. This capability not only improves operational efficiency but also significantly reduces energy costs, making electric motor-driven compressors a strategic investment for modern industries. The substantial market share of this segment highlights its pivotal role in the ongoing evolution and efficiency enhancement across key industrial domains.

By Compressible Gases Analysis

Hydrocarbon process gas usage constitutes 31.20% of compressible gases.

In 2024, Hydrocarbon Process Gas held a dominant market position in the “By Compressible Gases” segment of the Integrally Geared Centrifugal Compressor Market, capturing a 31.20% share. This segment’s leadership is primarily attributed to the extensive use of these compressors in the oil and gas industry, where they are essential for gas processing tasks, including natural gas liquefaction, gas lift, and flare gas recovery.

The reliance on hydrocarbon process gases in refining and petrochemical processes further cements their importance, driving demand for compressors that can handle these types of gases effectively.

The prominence of hydrocarbon process gas compressors is also a result of their ability to improve operational efficiencies and reduce emissions in processing environments. As environmental regulations become stricter and the global emphasis on reducing carbon footprints intensifies, the industry’s dependence on efficient and reliable gas compression solutions like integrally geared centrifugal compressors for hydrocarbon gases continues to grow.

Moreover, technological innovations in compressor design, which aim to maximize throughput while minimizing energy consumption and operational costs, have bolstered the adoption of these compressors in handling hydrocarbon process gases. This trend underscores the crucial role of this compressor type in supporting the energy sector’s operational needs and environmental goals, reflecting its significant market share within the segment.

By End-Use Analysis

Oil refining and petroleum chemistry use 34.20%, leading end-use sectors.

In 2024, Oil Refining and Petroleum Chemistry held a dominant market position in the “By End-Use” segment of the Integrally Geared Centrifugal Compressor Market, commanding a 34.20% share. This substantial market share highlights the critical role these compressors play in the refining and petrochemical industries. Integrally geared centrifugal compressors are pivotal in numerous key processes such as fluid catalytic cracking, hydrocracking, and alkylation, where precise pressure control and reliability are paramount.

The preference for these compressors in oil refining and petroleum chemistry is driven by their efficiency and ability to handle large volumes of gases at variable pressure ranges, which is essential for maximizing the output and efficiency of chemical reactions and refining operations. Additionally, the ability of these compressors to operate continuously under harsh conditions reduces downtime and maintains steady production rates, a vital requirement in these industries.

Moreover, as global demand for petroleum products remains high and refineries seek to optimize their operations to meet environmental standards and improve profitability, the reliance on advanced compression technology like integrally geared centrifugal compressors will likely continue to grow. Their significant market share within this segment is indicative of their indispensability and effectiveness in meeting the stringent requirements of modern oil-refining and petrochemical processes.

Key Market Segments

By Discharge pressure

- Up to 100 Bar

- 100 to 200 Bar

- Above 200 Bar

By Stage Configuration

- Single-Stage

- Two-Stage

- Three-Stage

By Category

- Oil-free

- Oil-injected

By Drive Type

- Electric Motor

- Steam Turbine

By Compressible Gases

- Nitrogen

- Acid Hydrocarbon Gas

- Chlorine

- Air

- Fuel Gas

- Hydrocarbon Process Gas

- Refrigerants

- Others

By End-Use

- Oil Refining and Petroleum Chemistry

- Gas Processing and LNG Production

- Chemical Industry

- Energy

- Mining

- Others

Driving Factors

Rising Demand for Energy Efficiency in Industries

One of the primary driving factors for the Integrally Geared Centrifugal Compressor Market is the escalating demand for energy efficiency across various industries. As companies continue to seek ways to reduce operational costs and adhere to stricter environmental regulations, the need for energy-efficient solutions has become more pronounced.

Integrally geared centrifugal compressors are highly efficient, capable of maximizing airflow while minimizing energy use, which makes them particularly appealing. Their ability to operate at different speeds and handle varying loads also allows for more precise energy management.

This efficiency not only helps companies lower their energy bills but also reduces their carbon footprint, aligning with global sustainability goals. As industries from manufacturing to oil and gas continue to expand and modernize, the demand for these energy-efficient compressors is expected to drive significant market growth.

Restraining Factors

High Initial Investment Limits Market Accessibility

A major restraining factor for the Integrally Geared Centrifugal Compressor Market is the high initial investment required for these systems. While integrally geared centrifugal compressors offer substantial long-term benefits, such as high efficiency and reduced operational costs, the upfront cost of acquiring and installing these systems can be prohibitively high.

This significant initial expense often acts as a barrier for small to medium-sized enterprises (SMEs) and industries operating with tight capital budgets. Additionally, the complexity involved in the design and engineering of these compressors requires skilled technicians for installation and maintenance, further adding to the initial costs.

This financial burden can deter potential users from adopting this technology, thereby restraining market growth, especially in regions with less economic flexibility.

Growth Opportunity

Technological Advancements Open New Market Opportunities

A significant growth opportunity within the Integrally Geared Centrifugal Compressor Market lies in ongoing technological advancements. As industries increasingly demand higher efficiency and lower emissions, the development of more advanced, smarter compressor technologies offers considerable market potential.

Innovations such as improved aerodynamic designs, better sealing materials, and integration with digital technologies like the Internet of Things (IoT) enable these compressors to achieve higher performance levels while reducing energy consumption.

Additionally, advancements in predictive maintenance capabilities, facilitated by AI and machine learning, can extend the lifespan and enhance the reliability of these systems. These technological improvements not only meet the evolving needs of traditional sectors like oil and gas but also create new applications in emerging markets such as renewable energy and advanced manufacturing processes.

Latest Trends

Integration of IoT Enhances Compressor Efficiency

One of the latest trends in the Integrally Geared Centrifugal Compressor Market is the integration of the Internet of Things (IoT) technology. This trend is revolutionizing how compressors are monitored and maintained, leading to significant enhancements in efficiency and reliability.

By incorporating IoT sensors and connectivity, these compressors can continuously collect and analyze data on their operational parameters and health status. This real-time data allows for predictive maintenance, where potential issues can be identified and addressed before they lead to failures, minimizing downtime and maintenance costs.

Additionally, IoT integration helps optimize compressor performance by adjusting operations based on actual demand and conditions, which further improves energy efficiency and reduces wear and tear. This technological trend is quickly becoming a standard in the industry, providing a competitive edge to those who adopt it early.

Regional Analysis

In North America, the Integrally Geared Centrifugal Compressor Market holds a 43.40% share, valued at USD 275.1 million.

The Integrally Geared Centrifugal Compressor Market exhibits diverse dynamics across various global regions, reflecting their industrial activities and technological adoption rates. In North America, the market is particularly robust, holding a dominating share of 43.40%, which equates to a market value of USD 275.1 million. This significant market presence is supported by the region’s advanced manufacturing sector, substantial investments in oil and gas, and stringent environmental regulations driving the demand for efficient, energy-saving technologies.

Europe and Asia Pacific also show substantial market activities. Europe benefits from its strong regulatory framework promoting energy efficiency, which propels the adoption of advanced compressors in industries such as chemical and petrochemical processing. Meanwhile, Asia Pacific is witnessing rapid industrial growth, particularly in China and India, where there is increasing investment in infrastructure and manufacturing. The demand in these regions is driven by the expanding industrial base and the shift toward more energy-efficient technologies.

Middle East & Africa and Latin America, though smaller in comparison, are emerging markets with potential growth due to developing oil and gas sectors and industrialization. These regions are gradually adopting more advanced technologies, including integrally geared centrifugal compressors, to meet their growing industrial needs and efficiency standards.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global Integrally Geared Centrifugal Compressor market is significantly shaped by the contributions and innovations of key players such as Atlas Copco Group, Baker Hughes, General Electric Co., Hitachi Ltd., and Hyundai Heavy Industries. Each company brings its own strategic advantages and technological prowess to the forefront, reinforcing its position in this competitive landscape.

Atlas Copco Group stands out with its robust portfolio of energy-efficient compressors, emphasizing sustainability and innovation. The company’s focus on developing products that offer lower life cycle costs and enhanced environmental benefits has made it a preferred choice for industries seeking to reduce their carbon footprint.

Baker Hughes excels in integrating digital technologies with its compressor solutions. By leveraging advanced analytics and IoT, Baker Hughes enhances the operational efficiency of its compressors, which is crucial for industries like oil and gas that demand high reliability and performance.

General Electric Co. brings its extensive experience in industrial manufacturing to the table, focusing on durability and high performance. GE’s compressors are known for their ability to operate under stringent conditions, making them ideal for critical applications in various sectors, including petrochemical and energy.

Hitachi Ltd. is recognized for its innovative engineering and ability to customize solutions based on specific industry needs. Hitachi’s commitment to R&D has resulted in highly efficient compressors that cater to a wide range of pressures and capacities, addressing the diverse requirements of global markets.

Hyundai Heavy Industries continues to expand its footprint in the compressor market by offering products that are not only technologically advanced but also cost-effective. This strategy is particularly appealing in emerging markets where cost considerations are paramount alongside performance.

Top Key Players in the Market

- Atlas Copco Group

- Baker Hughes

- General Electric Co.

- Hitachi Ltd.

- Hyundai Heavy Industries

- Ingersoll Rand Inc.

- Kobe Steel Ltd.

- MAN Energy Solutions SE

- Mitsubishi Heavy Industries Ltd.

- Siemens Energy AG

- Sundyne LLC

- Kazancompressormash

Recent Developments

- In October 2024, Baker Hughes secured the largest integrated compressor line order in its history, which includes 10 ICL units for gas storage and injection boosting in the UAE. This is part of Dubai’s decarbonization strategy.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 633.9 Million |

| Forecast Revenue (2034) | USD 1,189.9 Million |

| CAGR (2025-2034) | 6.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Discharge pressure (Up to 100 Bar, 100 to 200 Bar, Above 200 Bar), By Stage Configuration (Single-Stage, Two-Stage, Three-Stage), By Category (Oil-free, Oil-injected), By Drive Type (Electric Motor, Steam Turbine), By Compressible Gases (Nitrogen, Acid Hydrocarbon Gas, Chlorine, Air, Fuel Gas, Hydrocarbon Process Gas, Refrigerants, Others), By End-Use (Oil Refining and Petroleum Chemistry, Gas Processing and LNG Production, Chemical Industry, Energy, Mining, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Atlas Copco Group, Baker Hughes, General Electric Co., Hitachi Ltd., Hyundai Heavy Industries, Ingersoll Rand Inc., Kobe Steel Ltd., MAN Energy Solutions SE, Mitsubishi Heavy Industries Ltd., Siemens Energy AG, Sundyne LLC, Kazancompressormash |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |