Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of Mineral Processing Equipment

- By Equipment Type Analysis

- By Application Analysis

- By Mobility Analysis

- By End-Use Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

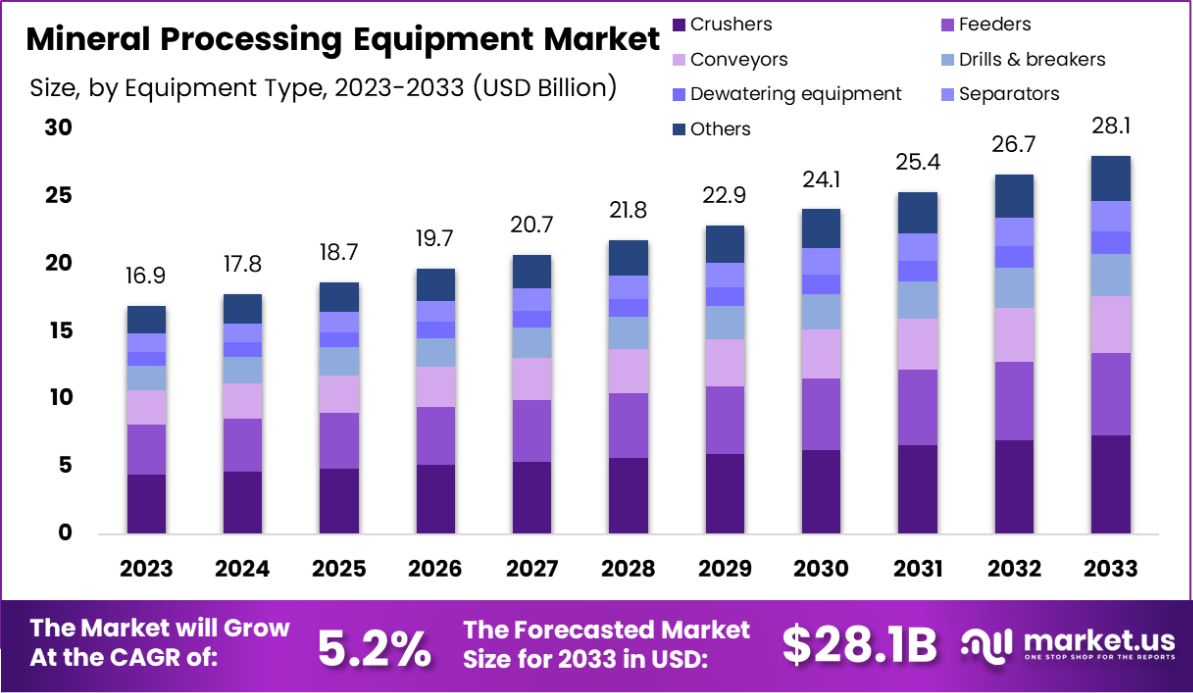

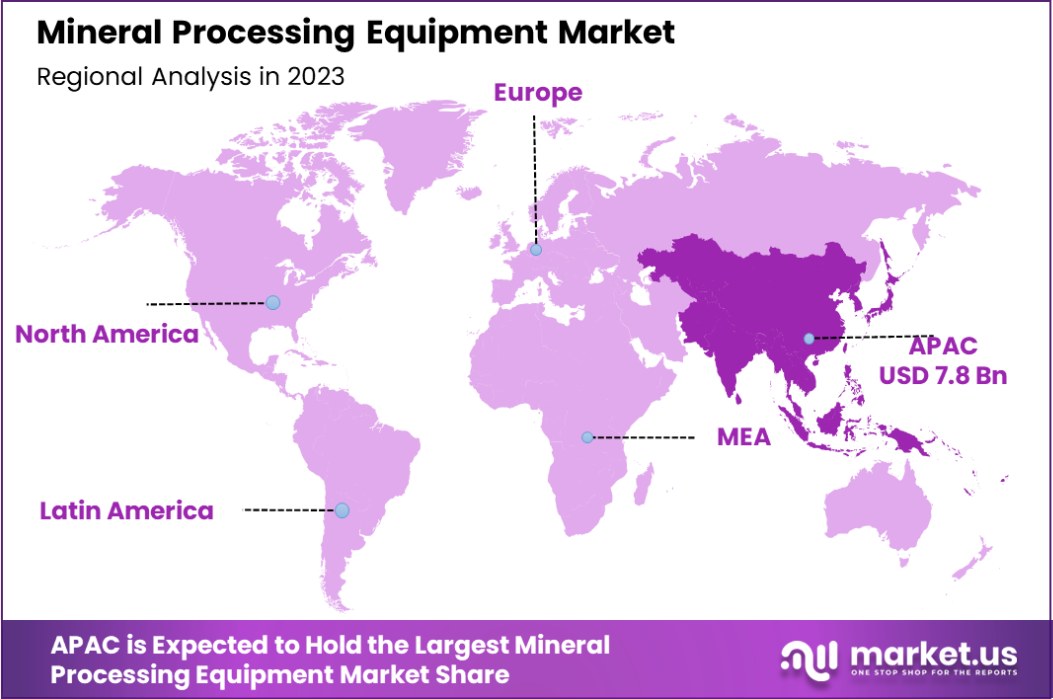

The Global Mineral Processing Equipment Market is expected to be worth around USD 28.1 Billion by 2033, up from USD 16.9 Billion in 2023, and grow at a CAGR of 5.2% from 2024 to 2033. Asia-Pacific leads with 46.2%, reaching USD 7.8 Bn in sales.

Mineral processing equipment includes various machines and devices used to process raw minerals extracted from mines into usable products. This equipment encompasses grinders, crushers, classifiers, separators, and concentrators, among others, essential for sorting, crushing, and refining minerals. They are integral to extracting metals, improving ore quality, and achieving environmental compliance by reducing waste.

The mineral processing equipment market refers to the global demand and supply for these devices, influenced by mining activities and technological advancements. This market is propelled by the increasing need for metals in various industries like construction, automotive, and electronics, driving equipment innovation to handle diverse and complex ores efficiently.

Key growth factors for this market include rising urbanization and industrialization, which amplify mineral demand, particularly in developing countries. Additionally, the adoption of automation and digital technologies in mineral processing enhances equipment efficiency and ore recovery rates, contributing significantly to market expansion.

The demand in the mineral processing equipment market is driven by the relentless extraction of lower-grade ores, necessitating more sophisticated and energy-efficient machinery. Environmental regulations also push for cleaner mining practices, fostering demand for modern processing solutions.

Opportunities within this market are vast, especially in the integration of IoT and AI to optimize operations, reduce energy consumption, and improve safety. The shift towards sustainable mining practices opens further avenues for developing eco-friendly and more effective mineral processing technologies.

The global Mineral Processing Equipment Market is poised for transformative growth, propelled by technological advancements and strategic governmental initiatives. The sector is witnessing a significant infusion of capital and technological expertise, as highlighted by the U.S. Department of Energy’s Advanced Materials and Manufacturing Technologies Office (AMMTO).

AMMTO’s recent allocation of $33 million towards advancing smart manufacturing technologies underscores a strategic push towards more efficient and sustainable mineral processing methods. This initiative is expected to catalyze innovations that enhance productivity and reduce environmental footprints, aligning with global sustainability goals.

Moreover, environmental regulations continue to shape operational frameworks within the industry. According to the Environmental Protection Agency (EPA), emissions from metallic mineral processing operations demonstrate considerable variability. For instance, dry grinding processes can emit up to 14.4 kg of filterable particulate matter (PM) per megagram of material processed.

Such data underscore the pressing need for industry stakeholders to adopt advanced equipment and technologies that mitigate environmental impact. This regulatory landscape not only challenges existing operational protocols but also opens avenues for market players to innovate and differentiate themselves through environmentally compliant solutions.

In essence, the Mineral Processing Equipment Market is at a critical juncture, where the integration of smart technologies and adherence to stringent environmental standards are not just strategic advantages but essential imperatives.

Stakeholders are encouraged to leverage these trends to foster resilience, compliance, and innovation in their operational strategies, positioning themselves favorably within the evolving market landscape.

Key Takeaways

- The Global Mineral Processing Equipment Market is expected to be worth around USD 28.1 Billion by 2033, up from USD 16.9 Billion in 2023, and grow at a CAGR of 5.2% from 2024 to 2033.

- Crushers dominate the equipment type segment with a 25.5% share in the market.

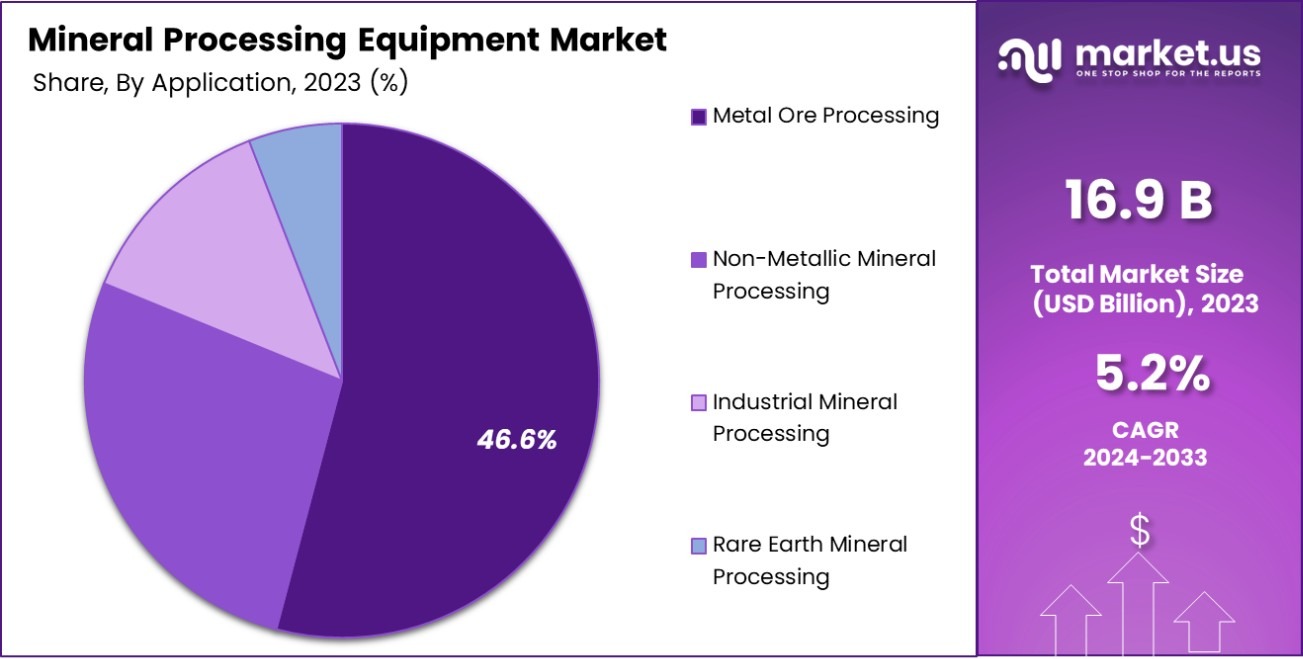

- Metal ore processing leads applications in the mineral processing equipment market at 46.6%.

- Stationary equipment holds the majority with 58.6% in the mobility category of the market.

- Mining as an end-use sector commands a significant 56.4% portion of the market.

- The Asia-Pacific mineral processing equipment market stands at USD 7.8 billion, 46.2%.

Business Benefits of Mineral Processing Equipment

Mineral processing equipment plays a critical role in enhancing the productivity and energy efficiency of the mining industry. For instance, advanced sensor technology helps optimize ore characterization and processing, improving the overall output and reducing energy consumption.

Additionally, government and industry collaborations focus on developing technologies that enhance the safety and environmental performance of mining operations. Such initiatives often involve cost-shared support for research and development projects aimed at boosting competitiveness and energy efficiency in the sector.

On average, the U.S. mining industry consumes significant energy, particularly in comminution, which is the most energy-intensive part, accounting for more than 50% of the energy used in mining processes.

By Equipment Type Analysis

The mineral processing equipment market sees crushers dominating with a 25.5% share by equipment type.

In 2023, Crushers held a dominant market position in the “By Equipment Type” segment of the Mineral Processing Equipment Market, commanding a 25.5% share. Their prominence is attributed to the essential role they play in initial ore processing, effectively reducing large rocks into smaller particles suitable for subsequent processing stages.

Following closely, Feeders accounted for 19.8% of the market. These devices are integral in ensuring a steady, controllable flow of material into crushing machines, optimizing the efficiency of the entire processing line.

Conveyors, which facilitate the movement of processed materials between different stages of mineral processing, captured 17.6% of the market. This equipment is vital for maintaining continuous operations and minimizing manual handling, which enhances safety and throughput.

Drills and Breakers held a 14.7% share, which is critical for the extraction phase, where breaking through rock and earth is essential.

The Dewatering equipment and Separators segments recorded shares of 12.2% and 10.2%, respectively. Dewatering equipment is crucial for reducing moisture in minerals, and improving the efficiency of transport and processing.

Meanwhile, Separators play a pivotal role in isolating valuable ores from other extracted materials, thereby enhancing product purity and operational efficiency. These segments collectively underscore the diverse technologies essential for optimizing mineral processing operations.

By Application Analysis

Metal ore processing leads applications in the mineral processing equipment sector, capturing 46.6% of the market.

In 2023, Metal Ore Processing held a dominant market position in the “By Application” segment of the Mineral Processing Equipment Market, with a commanding 46.6% share. This substantial portion highlights the extensive use of processing equipment in extracting and refining metal ores, which are crucial for producing metals used across various industries, including construction, automotive, and electronics.

Following Metal Ore Processing, Non-Metallic Mineral Processing accounted for 24.1% of the market. This segment focuses on materials such as sand, gravel, and phosphates, which are essential for the construction industry and chemical manufacturing. The demand in this sector is driven by the global expansion in infrastructure and urban development.

Industrial Mineral Processing, which involves minerals used in their natural form such as silica, gypsum, and clays, captured 17.8% of the market share. These minerals are pivotal in the production of cement, ceramics, glass, and other industrial materials, reflecting their broad applications and steady demand.

Lastly, Rare Earth Mineral Processing, which deals with the extraction of minerals critical for high-tech applications such as electronics and renewable energy technologies, held a smaller share of 11.5%. Despite its lower market share, this segment is experiencing rapid growth due to the increasing reliance on advanced technological products.

By Mobility Analysis

Stationary units hold the largest share in the mobility category, making up 58.6% of the market.

In 2023, Stationary equipment held a dominant market position in the “By Mobility” segment of the Mineral Processing Equipment Market, securing a 58.6% share. This significant dominance is attributed to the extensive deployment of fixed installations in large-scale industrial and mining operations where high-volume processing capabilities are crucial. The robustness and ability of stationery equipment to handle vast quantities of materials efficiently make it indispensable for sustained, heavy-duty use.

Portable equipment, designed for flexibility and ease of relocation, captured 25.7% of the market. These units are particularly favored in applications where temporary processing sites are necessary or in remote locations where permanent installations are not viable. The adaptability of portable equipment to various site conditions without compromising operational efficiencies is a key factor driving its market demand.

Lastly, Mobile equipment accounted for 15.7% of the market share. These units are integral to operations requiring frequent movements within a mining site or across multiple sites. Their mobility offers logistical advantages, reducing the need for additional transport equipment and facilitating faster setup times, thereby enhancing overall productivity and operational flexibility.

By End-Use Analysis

In terms of end-use, the mining sector overwhelmingly leads, constituting 56.4% of the market demand.

In 2023, Mining held a dominant market position in the “By End-Use” segment of the Mineral Processing Equipment Market, with a substantial 56.4% share. This leadership underscores the critical role of mineral processing equipment in extracting and processing raw materials from the earth, a fundamental activity in the mining industry.

The sector’s reliance on efficient, high-capacity machinery to handle and process large volumes of ore and minerals is key to its operational success and profitability.

Following Mining, the Metallurgy sector accounted for 26.3% of the market. In metallurgy, processing equipment is essential for the transformation of raw ores into usable metal and alloy products, which are fundamental to various manufacturing and industrial processes. The demand in this sector is primarily driven by the need for refined metals in the automotive, aerospace, and construction industries.

Construction, the third segment, held a 17.3% share of the market. Equipment used in this sector typically processes non-metallic minerals for producing materials such as sand, gravel, and crushed stone, essential for construction activities.

The growth in global infrastructure and building projects continues to drive demand for mineral processing equipment in the construction industry. These segments collectively highlight the extensive applications and dependencies of various industries on mineral processing technology.

Key Market Segments

By Equipment Type

- Crushers

- Feeders

- Conveyors

- Drills & breakers

- Dewatering equipment

- Separators

- Others

By Application

- Metal Ore Processing

- Non-Metallic Mineral Processing

- Industrial Mineral Processing

- Rare Earth Mineral Processing

By Mobility

- Stationary

- Portable

- Mobile

By End-use

- Mining

- Metallurgy

- Construction

- Others

Driving Factors

Increasing Demand for Metals in Various Industries

As industries like construction, automotive, and electronics continue to expand, there is a growing need for metals, which drives the demand for mineral processing equipment. These machines are crucial for extracting and processing ores into usable forms.

The ongoing urbanization and industrial development worldwide further propel the need for such equipment, ensuring a steady market demand.

Technological Advancements in Equipment Efficiency

Recent technological innovations have significantly improved the efficiency of mineral processing equipment. Developments such as automation and better data analytics help in optimizing the extraction and processing phases, reducing waste, and increasing yield.

These advancements make equipment more appealing to mining companies aiming to enhance productivity and reduce operational costs.

Stringent Environmental Regulations

Governments worldwide are imposing stricter environmental regulations to minimize the ecological impact of mining activities. This factor compels companies to invest in newer, more efficient mineral processing technologies that comply with environmental standards.

Equipment that can ensure more precise material handling and waste reduction not only helps in complying with these regulations but also in improving the overall sustainability of operations.

Restraining Factors

High Cost of Installation and Maintenance

The initial investment for high-quality mineral processing equipment is substantial, which can be a significant barrier for smaller mining operations. Additionally, the ongoing maintenance and operation costs add financial strain.

These high costs can deter new entrants and limit the expansion of existing facilities, particularly in regions with less financial flexibility or where the cost of capital is high.

Volatility in Raw Material Prices

Fluctuating prices of raw materials required for manufacturing mineral processing equipment, such as steel and other metals, directly affect production costs. This volatility makes it challenging for manufacturers to maintain stable pricing, potentially delaying investment decisions by mining companies.

Such unpredictability can restrain market growth as companies may postpone purchasing new equipment in anticipation of lower prices.

Regulatory and Compliance Challenges

Navigating the complex landscape of global regulations can be a major hurdle. Each region may have different compliance standards for safety, emissions, and environmental impact, making it difficult for equipment manufacturers to design products that meet all criteria universally.

This factor can limit market expansion, especially in areas with the most stringent regulations, and can increase the time and cost of bringing new equipment to market

Growth Opportunity

Expansion into Emerging Markets

Emerging markets offer significant growth opportunities for the mineral processing equipment sector. These regions often have untapped mineral reserves and are starting to invest more in their extraction and processing capacities. As local economies grow and infrastructure needs increase, the demand for mineral processing technologies is expected to rise.

Companies that can establish a presence in these markets early may gain a competitive advantage, benefiting from first-mover status and building long-term relationships with local industries.

Adoption of Green and Sustainable Technologies

There is a growing trend towards sustainability in mining operations, driven by both regulatory pressures and corporate responsibility initiatives. Equipment that reduces environmental impact, such as those featuring energy-efficient designs and reduced emissions, presents a substantial growth opportunity.

Manufacturers who innovate and market these greener technologies can capitalize on the increasing demand for sustainable mining solutions, positioning themselves as leaders in a shifting market.

Integration of Automation and IoT

Integrating automation and IoT (Internet of Things) technologies into mineral processing equipment can significantly enhance operational efficiency and data collection capabilities. This integration allows for real-time monitoring and adjustment of operations, leading to optimized performance and reduced downtime.

As industries continue to move towards digitalization, the demand for smart and connected machinery is expected to grow. Companies that invest in these technologies can access new market segments and improve their competitive edge.

Latest Trends

Increased Focus on Precision and Recovery Rates

The mineral processing equipment market is witnessing a trend toward technologies that enhance precision and recovery rates. As ore grades decline, the ability to efficiently process large volumes of material while maximizing the recovery of valuable minerals becomes crucial.

Equipment that offers finer, more accurate sorting and processing capabilities is in higher demand. This trend is driven by the need to optimize resource use and minimize waste, ensuring economic viability even with lower-grade ores.

Rise of Autonomous and Remote-Controlled Machinery

Autonomous and remote-controlled equipment is becoming more prevalent in the mineral processing industry. This technology reduces the need for human operators in potentially hazardous environments, increasing safety and efficiency.

The use of remote-controlled loaders, drills, and other machinery allows for continuous operations, even in extreme or dangerous conditions. This trend is facilitated by advancements in robotics, sensor technology, and wireless communications, providing new opportunities for innovation and operational improvements.

Integration of Artificial Intelligence in Processing

Artificial Intelligence (AI) is increasingly being integrated into mineral processing equipment to enhance decision-making and process optimization. AI can analyze vast amounts of data from equipment sensors and operations, providing insights that improve efficiency and reduce costs.

This technology enables predictive maintenance, where AI algorithms predict equipment failures before they occur, minimizing downtime. The adoption of AI is a growing trend that enhances operational efficiencies and drives the development of smarter, more responsive processing solutions.

Regional Analysis

In 2023, the Asia-Pacific Mineral Processing Equipment Market reached USD 7.8 billion, holding a 46.2% share.

The Mineral Processing Equipment Market is segmented by various global regions, each exhibiting distinct market dynamics. Asia-Pacific is the dominating region, accounting for 46.2% of the market with a revenue of USD 7.8 billion.

This robust market share is driven by rapid industrialization, significant investments in mining and infrastructure, and the presence of vast mineral reserves in countries like China, Australia, and India.

North America also represents a substantial portion of the market, propelled by technological advancements in mineral processing technologies and stringent environmental regulations that push for more efficient and cleaner processes. The presence of established mining operations in the United States and Canada further supports this trend.

Europe, while mature, continues to see moderate growth due to the adoption of cutting-edge technologies and increasing automation in mineral processing equipment. Environmental sustainability and regulatory compliance are significant drivers in this region, influencing equipment upgrades and replacements.

The Middle East & Africa, with its abundant natural resources, especially in the African continent, presents considerable growth opportunities. Investment in infrastructure development and mining exploration projects is set to drive demand for mineral processing equipment.

Latin America, with its rich deposits of copper, iron ore, and precious metals, sees growing demand as the region expands its mining capabilities. Increased foreign investments and local government initiatives to boost the mining sector are pivotal in driving the market growth in this region.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global Mineral Processing Equipment Market has seen significant contributions from a range of key companies, each bringing unique strengths and strategies to the industry. Astec Industries Inc. and Caterpillar Inc. are notable for their comprehensive product lines and robust global distribution networks, enhancing their capability to serve diverse mining operations worldwide. Their focus on reliability and efficiency continues to set them apart in competitive markets.

CITIC Ltd. stands out due to its strong foothold in the Asia-Pacific region, capitalizing on local growth dynamics and infrastructure development. Its extensive involvement in heavy industries provides a strategic advantage in integrating mineral processing solutions with broader industrial applications.

Companies like Derrick Corporation and General Kinematics Corp. are pushing the boundaries in specialized screening and separation technology, which is critical for achieving high-quality outputs in mineral processing. Their commitment to innovation is evident in their advanced vibratory equipment designed to improve material recovery rates and operational efficiency.

European manufacturers such as Sandvik AB and Terex Corp. emphasize technological advancements and sustainability. These companies are leading the way in automation and remote operation technologies, which enhance safety and productivity, particularly in challenging mining environments.

Metso Corporation and FLSmidth and Co. AS have been pivotal in driving the adoption of environmentally friendly technologies within the sector. Their focus on energy-efficient systems and reducing water usage in mineral processing aligns with global regulatory trends and market demands for sustainable practices.

Lastly, smaller specialists like Multotec Pty Ltd. and Prater Industries Inc. offer customized solutions that address niche market needs, allowing them to compete effectively by focusing on specific segments such as fine particle processing and bulk material handling.

Collectively, these key players are not just shaping the competitive landscape but are also crucial in driving innovation, efficiency, and sustainability in the Mineral Processing Equipment Market. Their efforts are crucial for meeting the evolving challenges of the mining sector globally.

Top Key Players in the Market

- Astec Industries Inc.

- Caterpillar Inc.

- CITIC Ltd.

- Derrick Corporation

- Eagle Crusher Co. Inc.

- Epiroc AB

- FEECO International, Inc.

- FLSmidth and Co. AS

- General Kinematics Corp.

- Kemper Equipment

- Kleemann GmbH

- Komatsu Ltd.

- L and H Industrial Inc.

- McLanahan Corporation

- Metso Corporation

- Multotec Pty Ltd.

- Prater Industries Inc.

- Rubble Master HMH GmbH

- Sandvik AB

- Terex Corp.

- WIRTGEN INTERNATIONAL GmbH

- Wm. W. Meyer and Sons Inc.

Recent Developments

- In 2023, Astec Industries Inc. made significant strides in enhancing its mineral processing equipment sector, investing $9.1 million to expand capacity and boost efficiency. This led to a 5% increase in annual net sales, reaching $1.3 billion.

- In 2023, Caterpillar Inc.’s Mineral Processing Equipment sector, part of its Resource Industries, saw significant growth. Efforts to enhance product lines and services, driven by increased sales volumes and favorable pricing, led to a 13% rise in annual revenues, reaching $67.1 billion.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 16.9 Billion |

| Forecast Revenue (2033) | USD 28.1 Billion |

| CAGR (2024-2033) | 5.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Equipment Type (Crushers, Feeders, Conveyors, Drills and breakers, Dewatering equipment, Separators, Others), By Application (Metal Ore Processing, Non-Metallic Mineral Processing, Industrial Mineral Processing, Rare Earth Mineral Processing), By Mobility (Stationary, Portable, Mobile), By End-use (Mining, Metallurgy, Construction, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Astec Industries Inc., Caterpillar Inc., CITIC Ltd., Derrick Corporation, Eagle Crusher Co. Inc., Epiroc AB, FEECO International, Inc., FLSmidth and Co. AS, General Kinematics Corp., Kemper Equipment, Kleemann GmbH, Komatsu Ltd., L and H Industrial Inc., McLanahan Corporation, Metso Corporation, Multotec Pty Ltd., Prater Industries Inc., Rubble Master HMH GmbH, Sandvik AB, Terex Corp., WIRTGEN INTERNATIONAL GmbH, Wm. W. Meyer and Sons Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |