Quick Navigation

Report Overview

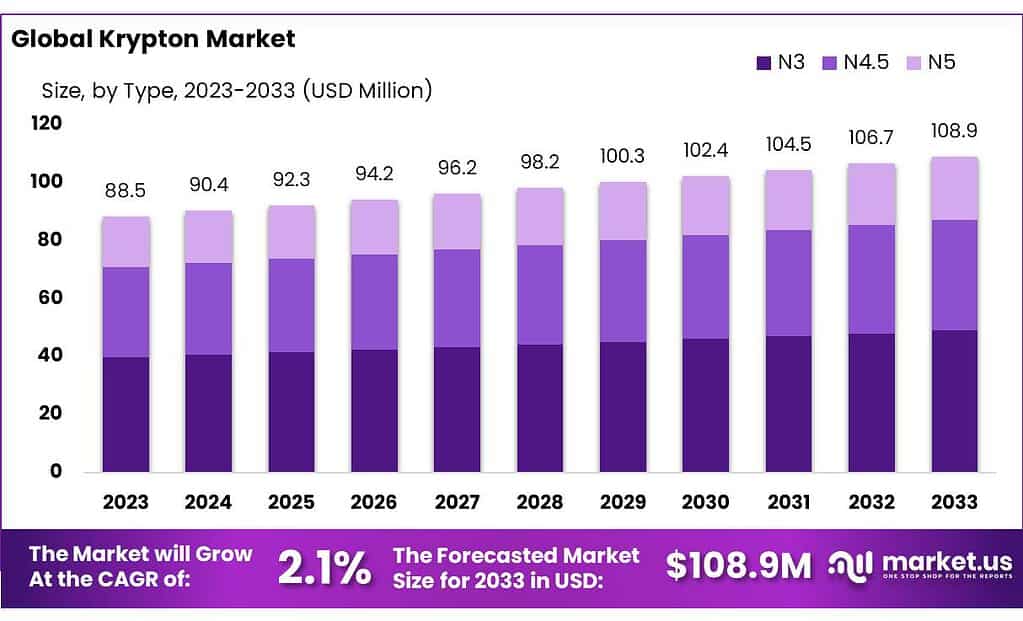

The global Krypton Market size is expected to be worth around USD 108.9 Million by 2033, from USD 88.5 Million in 2023, growing at a CAGR of 2.1% during the forecast period from 2023 to 2033.

The Krypton market is an essential sector focused on producing and distributing krypton, a noble gas renowned for its unique properties. It serves key roles in specialized industries, notably in enhancing the efficiency and lifespan of fluorescent lamps in the lighting industry and improving thermal insulation in window manufacturing. The market thrives on niche applications that capitalize on krypton’s distinct thermal and optical characteristics, making it invaluable despite its smaller market size compared to other industrial gases.

Globally, the demand for krypton is driven by technological advancements in energy efficiency and by regulatory initiatives aimed at sustainability and energy conservation. These factors are crucial in sectors such as aerospace, where krypton is used for space propulsion, and in scientific research, where its stability and inertness make it ideal for precise calibration tasks.

Krypton’s use in lighting, particularly in energy-efficient fluorescent lamps and certain halogen bulbs, although challenged by the rise of LEDs, remains robust due to its ability to enhance luminous efficiency. In the construction sector, krypton-filled double-pane windows are increasingly popular for their ability to significantly reduce energy costs in residential and commercial buildings, aligning with global trends toward energy conservation.

The market’s regulatory environment, particularly in regions like the European Union and the United States, further influences krypton’s use. EU regulations aiming to cut electricity consumption and U.S. Department of Energy standards both foster the use of energy-efficient materials, indirectly boosting the krypton market. These regulations ensure ongoing innovation within the industry, pushing manufacturers towards more sustainable practices.

In terms of trade, krypton is not typically dealt with in bulk but is affected by the production outputs of major air separation units in the U.S., China, and Russia. The distribution and availability of krypton are managed by industrial gas giants through extensive global networks, ensuring a steady supply of this gas alongside other noble gases like xenon and argon.

Key Takeaways

- The global krypton market is projected to grow from USD 88.5 million in 2023 to USD 108.9 million by 2033, growing at a CAGR of 2.1% during the forecast period

- In 2023, N3 krypton captured 45.6% of the market share due to its widespread use in lighting and window insulation, balancing performance and cost.

- Krypton delivered in cylinders held a dominant market position in 2023, accounting for 55.4% of the supply, favored for portability and small-scale applications.

- The lighting sector held 43.2% of the krypton market share in 2023, driven by krypton’s use in high-efficiency fluorescent and high-intensity discharge lamps.

- The construction industry accounted for 30.2% of the krypton market in 2023, driven by the increasing demand for energy-efficient double and triple-glazed windows.

- North America held 34.4% of the total krypton market in 2023, valued at USD 30.4 million, driven by advanced aerospace and lighting industries.

By Type

In 2023, N3 krypton held a dominant market position, capturing more than a 45.6% share of the overall krypton market. This type of krypton is widely appreciated for its balance of performance and cost-effectiveness, making it particularly popular in industrial applications such as lighting and insulation. Its ability to enhance energy efficiency in these applications drives its substantial market share.

Following N3, N4.5 krypton represents a premium segment of the market, utilized primarily in specialized applications that require higher purity levels. These include critical scientific research and aerospace applications, where the superior properties of N4.5 krypton can significantly impact performance outcomes. Its market share is smaller due to its specialized use and higher price point.

N5 krypton, the highest purity grade, is used in extremely specialized and sensitive environments, such as advanced optical applications and in standards calibration for scientific measurements. While its market share is the smallest, N5 krypton commands a premium price and is essential for applications where the utmost purity is required.

By Supply Mode

In 2023, cylinders held a dominant market position in the distribution of krypton, capturing more than a 55.4% share. Cylinders are the most common mode of supply for krypton due to their convenience and suitability for a wide range of applications, from industrial uses to scientific research. They are particularly favored for their portability and ease of handling, making them ideal for customers who require krypton in smaller, more controlled quantities.

Bulk and micro bulk supply modes are also significant, catering primarily to larger-scale industrial users who demand a continuous, reliable supply of krypton for processes like lighting manufacturing and window insulation. While bulk supply caters to the largest volume needs, micro bulk systems provide a cost-effective solution for users with intermediate volume requirements, offering the benefits of bulk delivery without the need for large storage facilities.

Drum tanks, another method of krypton supply, are used less frequently but are critical in certain applications where neither cylinders nor bulk solutions are feasible. They are typically used in unique situations where storage and gas requirements are specific to a particular operation or location.

By Application

In 2023, lighting held a dominant market position in the krypton industry, capturing more than a 43.2% share. Krypton is extensively used in the manufacturing of energy-efficient lighting solutions, particularly in high-intensity discharge lamps and fluorescent lights, where it helps extend the life and improve the luminosity of these products. Its unique properties make it ideal for reducing energy consumption while maintaining brightness, driving its widespread use in both residential and commercial settings.

Window insulation is another significant application for krypton, utilizing its excellent insulating properties to enhance the thermal efficiency of double and triple-glazed window units. This application is particularly valued in regions with extreme weather conditions, where energy efficiency in heating and cooling is crucial.

The use of krypton in lasers represents a smaller but vital segment of the market. Krypton lasers are used in a variety of medical and industrial applications, known for their ability to produce powerful and precise light beams.

By End-Use

In 2023, construction held a dominant market position in the krypton industry, capturing more than a 30.2% share. Krypton is highly valued in this sector for its application in high-efficiency window insulation systems, where it significantly enhances thermal performance, reducing heating and cooling costs in buildings. This application is especially crucial in regions with stringent energy efficiency regulations, contributing to sustainable building practices.

The automotive industry also utilizes krypton, primarily in lighting systems where its properties help improve the brightness and longevity of vehicle headlights. Although it represents a smaller share of the market, the demand in this sector is driven by advancements in automotive safety and design technologies.

In healthcare, krypton finds applications in imaging and laser treatments, providing essential functionality in diagnostic and therapeutic equipment. This niche application benefits from krypton’s ability to generate intense light sources that are used in various medical procedures.

The electronics and semiconductor industry employs krypton in the manufacturing process of semiconductors and electronic components, particularly where precise and controlled atmospheres are required for high-quality production standards.

Aerospace and defense is another critical sector for krypton, utilizing the gas in lighting solutions for aircraft and spacecraft, as well as in other specialized applications that require the unique properties of krypton for safety and performance.

Market Key Segments

By Type

- N3

- N4.5

- N5

By Supply Mode

- Cylinders

- Bulk & Micro bulk

- Drum tanks

- Others

By Application

- Lighting

- Window Insulation

- Laser

- Others

By End-Use

- Construction

- Automotive

- Healthcare

- Electronics & Semiconductor

- Aerospace & Defense

- Others

Drivers

Advancements in Energy-Efficient Building Technologies

One of the primary driving factors for the krypton market is the global shift towards energy-efficient building technologies. As governments around the world intensify their focus on reducing energy consumption and carbon emissions, the demand for advanced insulation materials, such as krypton in window glazing, is rapidly increasing.

The global push for more sustainable building practices has led to an increased use of krypton in high-performance window insulation. Krypton gas is used between panes in double and triple-glazed window units to significantly enhance their thermal efficiency. This application is crucial for achieving lower energy costs and reduced environmental impact in both residential and commercial buildings.

Various governments have implemented stringent building codes that require improved energy efficiency. For example, the European Union’s directives on the energy performance of buildings mandate that new constructions and major renovations meet high thermal efficiency standards, which often include the use of krypton-filled windows.

In the United States, the Department of Energy (DOE) promotes the adoption of energy-efficient technologies through incentives and rebates that encourage homeowners and builders to use krypton in window applications. These initiatives help drive the adoption of energy-saving technologies and boost the demand for krypton.

The advancement in window manufacturing technologies that allow for more effective incorporation of krypton gas has also spurred its use. Manufacturers are now able to offer more cost-effective solutions that make krypton an attractive option for a broader market, further fostering growth in its demand.

There is a growing public and corporate awareness regarding the importance of energy conservation, which has led to increased investment in energy-efficient construction materials. As Krypton plays a critical role in this sector, its market is experiencing significant growth.

According to industry sources, the market for energy-efficient windows is expected to grow substantially, with krypton as a key component due to its superior insulation properties compared to air or other gases.

The supply chain for Krypton has matured, with major gas suppliers expanding their production capabilities to meet the growing demand. This development ensures a stable supply of krypton, making it more accessible for window manufacturers and building contractors.

Restraints

High Production Costs and Limited Availability

One of the most significant restraining factors for the krypton market is the high production costs associated with extracting and purifying this noble gas, coupled with its limited availability. Krypton is extracted from the air, which contains only about 1 part per million of krypton, making its extraction and purification a highly energy-intensive and costly process.

The extraction of krypton requires sophisticated air separation units that are both capital and energy-intensive. The specialized equipment needed for krypton separation contributes significantly to the overall costs, limiting the production capacity to only a few key global players.

Due to these high costs, the price of krypton is substantially higher than more commonly used gases, which can deter potential new users, particularly in cost-sensitive applications.

Krypton’s scarcity in the atmosphere inherently limits its abundance and availability. This scarcity can lead to supply constraints, particularly during periods of high demand in the electronics or aerospace industries, where krypton is used for critical applications.

The limited number of production facilities worldwide further exacerbates these supply issues, as any operational disruptions can significantly impact global availability.

Environmental regulations concerning energy consumption also indirectly affect krypton production. As governments impose stricter energy usage standards and seek to reduce carbon emissions, the operation of air separation units becomes more regulated and potentially more costly.

These regulatory pressures can restrain the expansion of existing facilities or the establishment of new ones, particularly in regions with stringent environmental standards.

The krypton market is subject to volatility due to its dependency on the performance of end-use industries like electronics and construction. Any downturns in these sectors can lead to decreased demand for krypton, impacting producers who may face overcapacity and underutilization of their production facilities.

The development of alternative technologies and substitute materials that do not require krypton, especially in insulation and lighting applications, poses a significant threat to the krypton market. Innovations in materials science may lead to more cost-effective and readily available substitutes, further restraining market growth for krypton.

Opportunities

Expanding Use in High-Efficiency Insulation and Aerospace Applications

A major growth opportunity for the krypton market lies in its expanding use in high-efficiency insulation materials and the aerospace sector. As global emphasis on energy efficiency and sustainability intensifies, the demand for advanced insulation solutions and innovative aerospace technologies is rising, presenting significant opportunities for krypton utilization.

Krypton is highly valued in the construction industry for its superior insulating properties, especially in high-performance window units. These krypton-filled windows provide exceptional thermal efficiency, helping buildings meet stringent energy codes and sustainability standards.

The global push for greener buildings is supported by various government initiatives promoting energy efficiency. For instance, the European Union’s Energy Performance of Buildings Directive (EPBD) aims to improve the energy performance of buildings, a move that directly benefits the market for krypton as an insulation gas.

The increasing renovation and retrofitting of existing buildings to make them more energy-efficient also drive demand for krypton-enhanced insulation products.

In the aerospace industry, krypton is used in lighting systems and as a propellant in ion propulsion systems for spacecraft. Its effectiveness in these roles, particularly in enhancing the efficiency of ion thrusters, is critical as the global space economy grows.

Agencies like NASA and private space ventures are continually looking for ways to extend the duration and reduce the costs of space missions, where krypton’s role as a low-reactivity, high-performance propellant is invaluable.

The expansion of satellite launches and increased investment in space exploration missions offer new opportunities for the application of krypton in the aerospace sector.

Advances in air separation technology have made the extraction of krypton more efficient, reducing costs and increasing the available supply. These technological improvements are crucial in making krypton more accessible and economically viable for broader applications.

Furthermore, initiatives to recycle krypton from waste streams in industries where it is already used can provide a sustainable and cost-effective supply of the gas, supporting market growth.

The krypton market is poised for growth not only due to direct applications but also due to strategic expansions by key players in the gas production and distribution sectors. Investments in capacity expansion and geographical diversification by major industrial gas companies are expected to enhance the availability and reduce the cost of krypton.

Latest Trends

Enhanced Use of Krypton in Advanced Insulation Technologies

One of the most significant trends in the krypton market is its enhanced use in advanced insulation technologies within the construction and architectural sectors. As global focus sharpens on energy efficiency and sustainable building practices, krypton is increasingly valued for its superior insulating properties, particularly in high-performance window applications.

The drive towards more energy-efficient buildings is accelerating demand for krypton. This is particularly evident in the architectural sector where krypton gas is used between the panes of double and triple-glazed windows to significantly reduce thermal transfer, enhancing the building’s overall energy efficiency.

According to industry estimates, the usage of krypton in window applications can improve insulation performance by up to 50% compared to argon, making it a preferred choice for premium energy-efficient constructions.

Numerous government initiatives worldwide are reinforcing the trend towards sustainable building practices. For example, the European Union’s directives and the building codes in the United States, such as those recommended by the Department of Energy (DOE), are increasingly stringent about the energy performance of buildings. These regulations are direct catalysts for the adoption of advanced insulating materials including krypton-filled windows.

The push for net-zero buildings, which aim to significantly reduce carbon footprints, further bolsters the use of advanced materials like krypton for achieving desired energy standards and compliance with green building certifications.

Innovations in window manufacturing technology have made it more feasible to use krypton on a larger scale. Improved techniques in the sealing and longevity of krypton-filled windows enhance their appeal to both builders and consumers, which drives further adoption.

Companies are also developing multi-pane window designs that optimize the insulating properties of krypton, pushing the boundaries of what’s possible in thermal insulation for residential and commercial buildings.

The market for high-performance insulating glass is expected to grow steadily, driven by the rising awareness of the benefits of energy savings and the increasing economic incentives provided by governments for energy-efficient renovations and constructions.

As a result, the demand for krypton, though it comprises a smaller niche in the global gases market, is poised for significant growth, especially in developed markets where regulations and building practices aggressively support energy efficiency.

Regional Analysis

The global krypton market exhibits distinct regional trends, with North America leading the market. In 2023, North America accounted for 34.4% of the total market share, valued at approximately USD 30.4 million. This dominance is driven by the region’s advanced lighting and aerospace industries, particularly in the United States. The demand for krypton in high-efficiency lighting, especially in medical equipment and specialty lighting applications, is a significant growth factor. Additionally, the increasing use of krypton in energy-efficient windows contributes to its strong market position.

Europe follows closely, with substantial demand for krypton in the construction and automotive sectors. The region is focused on enhancing energy efficiency, with countries like Germany and France leading in the adoption of krypton-filled insulating windows. Europe’s push for sustainability and energy-saving technologies further bolsters krypton demand.

Asia Pacific (APAC) is experiencing rapid growth, driven by its expanding electronics and semiconductor industries. Countries like China, Japan, and South Korea are key contributors, leveraging krypton in electronics manufacturing, especially in plasma displays and specialized lighting applications. The growing construction sector in APAC also supports the market, with rising investments in energy-efficient building materials.

In the Middle East & Africa, krypton demand is primarily influenced by infrastructure development and increasing energy-efficiency initiatives. The use of krypton in insulating glass units for high-rise buildings is notable in this region.

Latin America remains a smaller market but is witnessing steady growth, particularly in the construction and automotive industries, with Brazil and Mexico being significant contributors to the demand for krypton-filled products.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The krypton market is highly competitive, with key players such as Air Liquide, Linde PLC, and Air Products & Chemicals Inc. holding significant market shares due to their extensive gas production capabilities and distribution networks. These companies focus on the supply of high-purity krypton for applications in sectors like lighting, energy-efficient windows, and electronics.

Linde PLC and Air Liquide have strengthened their market positions through continuous investment in research and development to meet the growing demand for krypton in energy-efficient technologies. Additionally, Messer Group GmbH and Taiyo Nippon Sanso Corporation also play crucial roles in serving the growing needs of the electronics and semiconductor industries, especially in Asia-Pacific.

Regional players such as Coregas Pty Ltd. and Axcel Gases cater to localized markets with specific krypton applications in industries such as automotive and construction. Electronic Fluorocarbons, LLC and Matheson Tri-Gas, Inc. focus on providing specialty gas solutions, particularly in North America, where the demand for krypton in high-end lighting and medical equipment is substantial. Companies like BASF SE and American Gas Products contribute by offering krypton-based solutions in niche markets such as chemical synthesis and industrial processes.

Emerging players like Proton Gases and Akela-p Medical Gases P. are focusing on expanding their product portfolios and regional presence, aiming to tap into the growing demand for krypton across various sectors. This competitive landscape reflects the rising global demand for krypton, driven by advancements in energy-efficient technologies and increasing applications in the electronics and construction industries.

Market Key Players

- Air Liquide

- Air Products & Chemicals Inc.

- Air Water Inc.

- Akela-p Medical Gases P.

- American Gas Products

- BASF SE

- Coregas Pty Ltd.

- Electronic Fluorocarbons, LLC

- Iceblick Ltd.

- Linde PLC

- Matheson Tri-Gas, Inc

- Messer Group GmbH

- Proton Gases

- The Linde Group.

- Taiyo Nippon Sanso Corporation

- Axcel Gases

Recent Developments

Air Liquide’s multi-year contracts worth over €50 million in regions like Europe, North America, and Asia underscore its commitment to supporting these high-tech industries.

Air Products & Chemicals Inc. is a significant player in the global krypton market, focusing on the supply of high-purity krypton for specialized applications such as lighting, window insulation, and aerospace technologies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 88.5 Mn |

| Forecast Revenue (2033) | US$ 108.9 Mn |

| CAGR (2024-2033) | 2.1% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type(N3, N4.5, N5), By Supply Mode(Cylinders, Bulk and Micro bulk, Drum tanks, Others), By Application(Lighting, Window Insulation, Laser, Others), By End-Use(Construction, Automotive, Healthcare, Electronics and Semiconductor, Aerospace and Defense, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Air Liquide, Air Products & Chemicals Inc., Air Water Inc., Akela-p Medical Gases P., American Gas Products, BASF SE, Coregas Pty Ltd., Electronic Fluorocarbons, LLC, Iceblick Ltd., Linde PLC, Matheson Tri-Gas, Inc, Messer Group GmbH, Proton Gases, The Linde Group., Taiyo Nippon Sanso Corporation, Axcel Gases |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |