Global Coal Tar Pitch Market Size, Share, And Industry Analysis Report By Type (Solid Coal Tar Pitch, Liquid Coal Tar Pitch), By Grade (Aluminium Grade, Binder and Impregnation Grade, Special and Mesophase Grade), By Application (Aluminium Smelting, Graphite Electrodes, Roofing, Carbon Fiber, Refractories, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 184091

- Number of Pages: 397

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

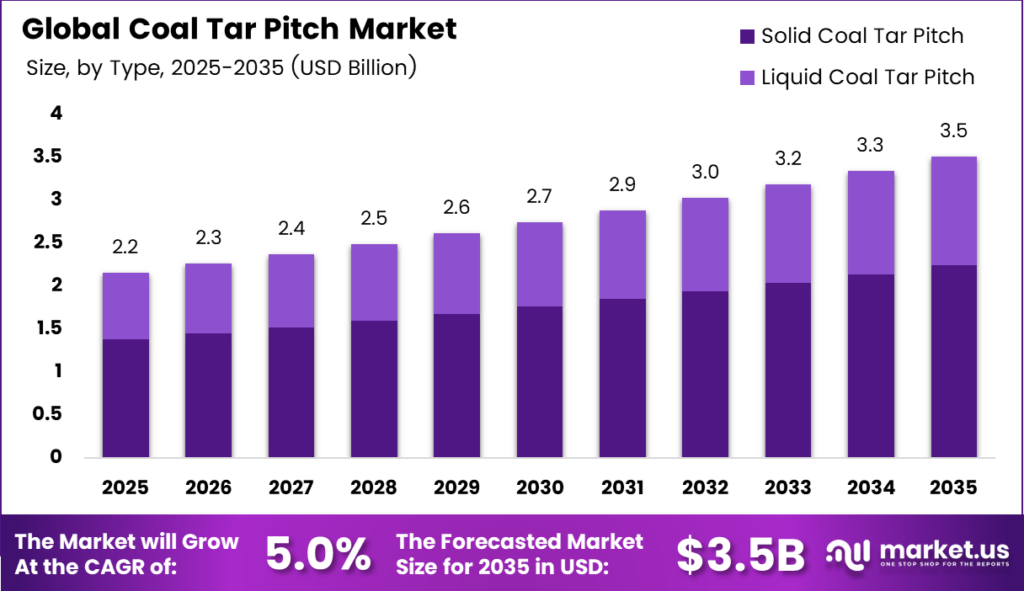

The Global Coal Tar Pitch Market size is expected to be worth around USD 3.5 billion by 2035 from USD 2.2 billion in 2025, growing at a CAGR of 5.0% during the forecast period 2026 to 2035.

Coal tar pitch is a dense, carbon-rich byproduct derived from the high-temperature carbonization of coal in coking ovens. Industries use it extensively as a binder and impregnation material in aluminum smelting, graphite electrode production, and specialty carbon applications. Its high carbon yield, thermal resistance, and low electrical resistivity make it indispensable in electrochemical and industrial processes.

The market draws primary demand from the aluminum industry, where coal tar pitch serves as the essential binder in prebaked carbon anodes. Rising global aluminum production capacities, particularly in Asia and the Middle East, continue to expand the consumption base. Moreover, graphite electrode manufacturing for electric arc furnaces adds a significant and growing demand layer.

The carbon fibre segment represents a high-growth application frontier for coal tar pitch. Coal tar pitch-based carbon fibre uses 2.4–2.5 times less total embodied energy than conventional PAN-based carbon fibre, thanks to a higher fibre conversion yield of 74% compared to 45% for PAN. This energy efficiency advantage positions coal tar pitch as a preferred feedstock for sustainable carbon fibre manufacturing.

Furthermore, research confirms that across nine TRACI 2.1 environmental impact categories, pitch-based carbon fibre manufacturing exhibits mostly below 50% of the environmental impacts of PAN-based carbon fibre. This finding, reported by Oak Ridge National Laboratory, signals growing material competitiveness for coal tar pitch in advanced manufacturing and green industrial transitions. Consequently, the market outlook remains firmly positive through 2035.

Key Takeaways

- The Global Coal Tar Pitch Market is valued at USD 2.2 billion in 2025 and is projected to reach USD 3.5 billion by 2035, growing at a CAGR of 5.0%.

- Solid Coal Tar Pitch dominates with a market share of 64.7% in 2025.

- Aluminum Grade holds the leading position with a 49.1% share.

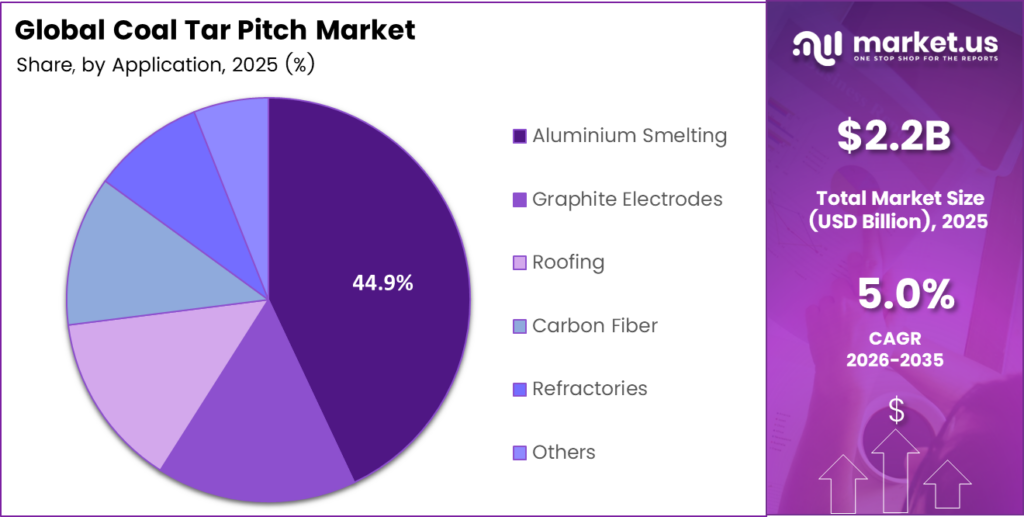

- Aluminum Smelting leads all end-use segments with a 44.9% share.

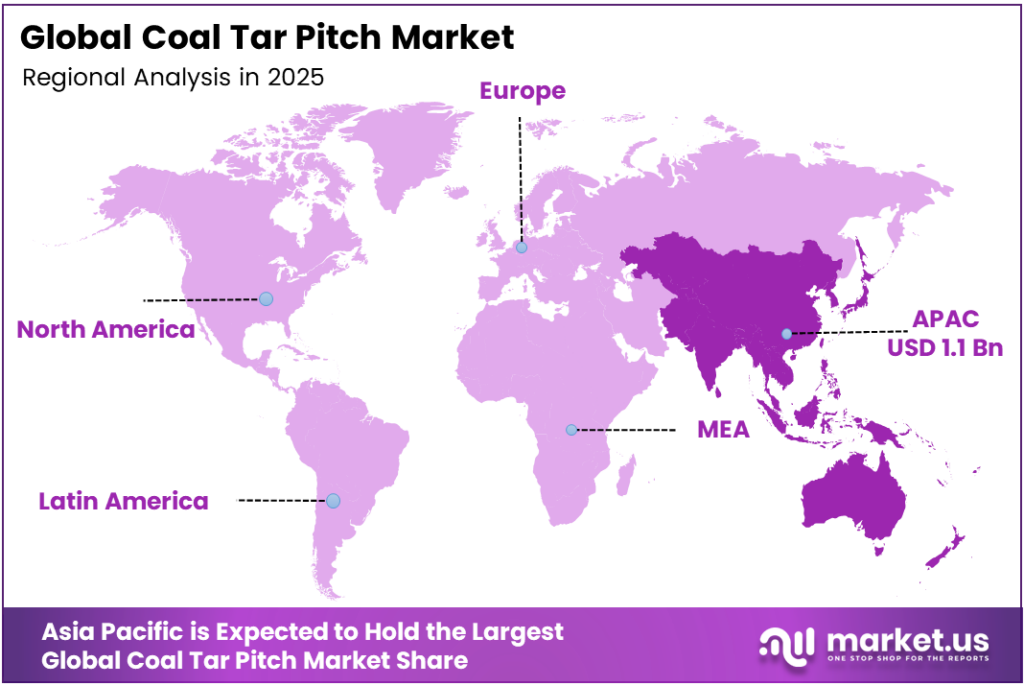

- Asia Pacific is the dominant region, accounting for 49.6% of the global market, valued at approximately USD 1.1 billion in 2025.

By Type Analysis

Solid Coal Tar Pitch dominates with 64.7% due to its widespread use as a carbon anode binder in aluminum smelting and graphite electrode manufacturing.

In 2025, Solid Coal Tar Pitch held a dominant market position in the By Type segment of the Coal Tar Pitch Market, with a 64.7% share. Solid pitch delivers superior carbon yield, high softening points, and excellent binding properties. Consequently, aluminum smelters and graphite electrode producers rely on it as their primary raw material for high-performance carbon anodes and electrodes.

Liquid Coal Tar Pitch occupies the remaining share and is gaining adoption for its logistical advantages. Aluminum anode plants increasingly prefer liquid formats because they simplify handling, reduce energy consumption during processing, and enable seamless integration into automated manufacturing lines. Moreover, emerging supply partnerships in the Middle East are accelerating liquid pitch infrastructure development.

By Grade Analysis

Aluminum Grade dominates with 49.1% due to massive demand from global aluminum production and prebaked carbon anode manufacturing.

In 2025, Aluminum Grade held a dominant market position in the By Grade segment of the Coal Tar Pitch Market, with a 49.1% share. Aluminum smelters require this grade for its precise softening point, low ash content, and optimal quinoline insoluble levels. Therefore, expanding aluminum production capacities across the Asia Pacific and the Middle East continues to sustain high and stable demand for this grade.

Binder and Impregnation Grade serve specialized applications in graphite electrodes, refractories, and carbon composites. This grade delivers strong adhesion and excellent thermal stability, making it suitable for electric arc furnace electrodes and high-temperature industrial processes. Additionally, growing investments in steel infrastructure drive incremental demand for this grade globally.

Special and Mesophase Grade represents the highest-value segment, targeting advanced applications such as carbon fibre and next-generation battery anodes. Researchers and manufacturers increasingly utilize this grade to develop high-performance materials with superior mechanical and electrochemical properties. However, its production complexity and lower volume availability limit current market penetration.

By Application Analysis

Aluminum Smelting dominates with 44.9% due to its critical role as the primary end-use application consuming coal tar pitch as a carbon anode binder.

In 2025, Aluminum Smelting held a dominant market position in the By Application segment of the Coal Tar Pitch Market, with a 44.9% share. Prebaked carbon anodes for the Hall-Héroult process smelting require coal tar pitch as the core binder. Moreover, rising global aluminum demand for automotive, aerospace, and packaging sectors continues to expand anode production volumes.

Graphite Electrodes represent the second-largest application, driven by the global expansion of electric arc furnace-based steelmaking. Manufacturers depend on coal tar pitch as an impregnation and binder material to produce high-density graphite electrodes. Additionally, surging Indian and Middle Eastern exports of liquid pitch directly support graphite electrode production across the Americas.

Roofing applications utilize coal tar pitch for waterproofing membranes and industrial coatings, particularly in heavy infrastructure projects. Although it remains a traditional application, regulatory scrutiny around polycyclic aromatic hydrocarbon content is gradually reshaping product formulations in this segment.

Key Market Segments

By Type

- Solid Coal Tar Pitch

- Liquid Coal Tar Pitch

By Grade

- Aluminium Grade

- Binder and Impregnation Grade

- Special and Mesophase Grade

By Application

- Aluminium Smelting

- Graphite Electrodes

- Roofing

- Carbon Fiber

- Refractories

- Others

Emerging Trends

Liquid Pitch Formats Reshape Aluminum Anode Plant Operations

Aluminum producers increasingly shift toward liquid coal tar pitch formats to improve handling efficiency and reduce processing steps. This operational preference drives dedicated melting facility investments and MoU-based supply partnerships between pitch producers and primary aluminum smelters. Consequently, liquid pitch logistics networks are expanding across the Middle East and Asia Pacific regions to support regional supply security.

Coal Tar Pitch Derivatives Target Next-Generation Battery Anode Materials

Research institutions actively focus on coal tar pitch-derived hard carbon anodes for sodium-ion and lithium-ion battery applications. Pitch-derived hard carbon anodes achieved a reversible capacity of 711.3 mAh g⁻¹ after 100 cycles, demonstrating strong electrochemical stability. This performance positions coal tar pitch as a strategic feedstock for next-generation energy storage materials.

Drivers

Rising Aluminum Production Expands Coal Tar Pitch Demand Globally

Global aluminum production growth directly drives coal tar pitch consumption as a critical carbon anode binder. Smelters in the Middle East are forming long-term liquid pitch supply partnerships and investing in localized melting facilities to secure consistent raw material access. Additionally, Indian producers are ramping up pitch exports to fulfill aluminum and graphite electrode manufacturing needs across the Americas and the Middle East.

Steel Sector Expansion Strengthens Downstream Pitch Supply Chains

Battery-grade synthetic graphite production using petroleum coke and coal tar pitch feedstocks consumes 10.4–16.5 kWh per kilogram, highlighting pitch’s centrality in energy-intensive manufacturing. Growing steel sector capacity expansions in India generate greater coal tar byproduct availability, directly supporting downstream pitch production volumes. Moreover, public listings of Indian steel producers further strengthen supply chain financing and infrastructure capacity.

Restraints

EU REACH Regulations Tighten Restrictions on PAH Content in Coal Tar Pitch

The European Union’s implementation of strengthened REACH Annex XVII restrictions on polycyclic aromatic hydrocarbons in coal tar pitch binders, effective April 2026, introduces significant compliance burdens for producers and end-users. Manufacturers must reformulate products or reduce PAH concentrations to maintain market access. Therefore, this regulatory tightening adds cost pressure and limits product flexibility for coal tar pitch suppliers serving European customers.

Occupational Health Classifications Increase Operational Compliance Costs

OSHA, NIOSH, and international health agencies enforce occupational exposure standards for coal tar pitch volatiles, classifying them as carcinogens requiring strict workplace controls. Industrial operators must invest in ventilation systems, personal protective equipment, and health monitoring programs. Consequently, these compliance requirements raise operating costs for smelters and electrode manufacturers, particularly in markets with limited infrastructure for worker safety management.

Growth Factors

Middle East Infrastructure Investments Create Regional Pitch Processing Hubs

Middle Eastern governments and private investors are establishing dedicated coal tar pitch processing infrastructure to reduce aluminum smelter dependence on long-haul imports. These regional processing hubs improve supply chain resilience and reduce procurement lead times. Moreover, the expansion of coal tar pitch utilization in graphite electrode production, tied to energy-intensive infrastructure projects, further accelerates regional demand and local capacity investment.

Decarbonization Research Unlocks New Markets for Sustainable Pitch Applications

Substituting renewable electricity and green hydrogen in pitch-based synthetic graphite production can reduce lifecycle carbon footprint by 41–70%. This decarbonization potential opens new market opportunities as battery manufacturers and industrial buyers prioritize low-carbon raw materials. Additionally, the development of compliant low-PAH coal tar pitch variants enables producers to serve both the aluminum and battery sectors under tightening environmental standards.

Regional Analysis

Asia Pacific Dominates the Coal Tar Pitch Market with a Market Share of 49.6%, Valued at USD 1.1 Billion

Asia Pacific leads the global coal tar pitch market with a 49.6% share, valued at approximately USD 1.1 billion in 2025. China, India, and Japan drive demand through massive aluminum smelting operations, steel production, and graphite electrode manufacturing. Moreover, expanding byproduct coal tar availability from growing Indian steel capacity strengthens the region’s downstream pitch production base and export capabilities.

North America sustains steady coal tar pitch demand through established aluminum smelting facilities, roofing applications, and specialty carbon manufacturing. The region’s graphite electrode sector benefits from liquid pitch imports, particularly from Indian producers. However, evolving environmental regulations and PAH compliance requirements are reshaping procurement strategies and encouraging investment in low-emission pitch processing technologies.

Europe faces significant regulatory pressure from strengthened REACH Annex XVII restrictions on PAH content in coal tar pitch products, effective April 2026. Producers and users across Germany, France, and the UK are accelerating reformulation efforts to maintain compliance. Additionally, European aluminum and specialty carbon manufacturers are exploring low-PAH pitch alternatives to secure long-term supply chain continuity within the regulatory framework.

The Middle East represents the fastest-growing regional market for coal tar pitch, driven by large-scale aluminum smelter expansions and energy infrastructure investments. Regional producers are establishing dedicated liquid pitch processing facilities to reduce import dependence. Furthermore, long-term supply partnerships between global pitch producers and Middle Eastern aluminum smelters are formalizing through structured MoU-based agreements for supply security.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Koppers Inc. is a globally recognized producer of carbon compounds and commercial chemicals derived from coal tar. The company operates an integrated network of carbon materials facilities supplying aluminum smelters, graphite electrode manufacturers, and specialty carbon producers worldwide. Koppers focuses on product quality consistency and supply chain reliability, positioning itself as a preferred long-term partner for industrial pitch consumers across multiple regions.

Himadri Chemicals and Specialty Ltd. is India’s leading coal tar pitch producer and a significant contributor to the country’s growing pitch export capabilities. The company supplies aluminum-grade and binder-grade pitch to domestic and international customers, benefiting from strong upstream coal tar availability from Indian steel producers. Moreover, Himadri’s strategic positioning enables it to serve growing demand across the Middle East, Southeast Asia, and the Americas.

JFE Chemical Corporation operates as a major Japanese producer of coal tar pitch and related carbon materials, serving the aluminum, graphite, and specialty chemical sectors. The company leverages advanced carbonization technology and quality control systems to produce consistent-grade pitch products. Additionally, JFE Chemical maintains strong relationships with downstream manufacturers in the Asia Pacific, supporting regional supply chain integration for aluminum anode and graphite electrode production.

Mitsubishi Chemical Corporation brings significant research capability and production scale to the coal tar pitch market, with expertise spanning mesophase pitch, binder pitch, and specialty carbon materials. The company actively explores advanced applications, including carbon fibre and battery anode materials, aligning its pitch portfolio with emerging demand for high-performance materials. Furthermore, Mitsubishi Chemical’s global network supports supply diversification for industrial customers across multiple end-use sectors.

Top Key Players in the Market

- Bathco Ltd

- Bilbaina de Alquitranes S.A.

- Coopers Creek Chemical Corporation

- Crowley Chemical Company Inc.

- Deza, a.s.

- Epsilon Carbon Private Limited

- Hengshui Zehao Chemicals Co., Ltd

- Himadri Chemicals Specialty Ltd.

- JFE Chemical Corporation

- Koppers Inc.

- Lone Star Specialties

- Mitsubishi Chemical Corporation

Recent Developments

- In 2025, Bilbaina de Alquitranes S.A. (Spain) continues to distill coal tar from coke oven batteries (producing pitches, special tars, creosote, and oils) at its Lutxana-Barakaldo facility near Bilbao. It is a long-established player and member of Coal Chemistry Europe.

- In 2025, Deza, a.s. (Czech Republic) processes coal tar and crude benzol, producing coal tar pitch, tar oils, esters/plasticizers, benzene, and aromatic solvents. It is part of the Agrofert group and a member of Coal Chemistry Europe.

Report Scope

Report Features Description Market Value (2025) USD 2.2 Billion Forecast Revenue (2035) USD 3.5 Billion CAGR (2026-2035) 5.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Solid Coal Tar Pitch, Liquid Coal Tar Pitch), By Grade (Aluminum Grade, Binder and Impregnation Grade, Special and Mesophase Grade), By Application (Aluminum Smelting, Graphite Electrodes, Roofing, Carbon Fibre, Refractories, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Bathco Ltd, Bilbaina de Alquitranes S.A., Coopers Creek Chemical Corporation, Crowley Chemical Company Inc., Deza a.s., Epsilon Carbon Private Limited, Hengshui Zehao Chemicals Co. Ltd, Himadri Chemicals Specialty Ltd., JFE Chemical Corporation, Koppers Inc., Lone Star Specialties, Mitsubishi Chemical Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Bathco Ltd

- Bilbaina de Alquitranes S.A.

- Coopers Creek Chemical Corporation

- Crowley Chemical Company Inc.

- Deza, a.s.

- Epsilon Carbon Private Limited

- Hengshui Zehao Chemicals Co., Ltd

- Himadri Chemicals Specialty Ltd.

- JFE Chemical Corporation

- Koppers Inc.

- Lone Star Specialties

- Mitsubishi Chemical Corporation

Our Clients

- 184091

- April 2026