Quick Navigation

Report Overview

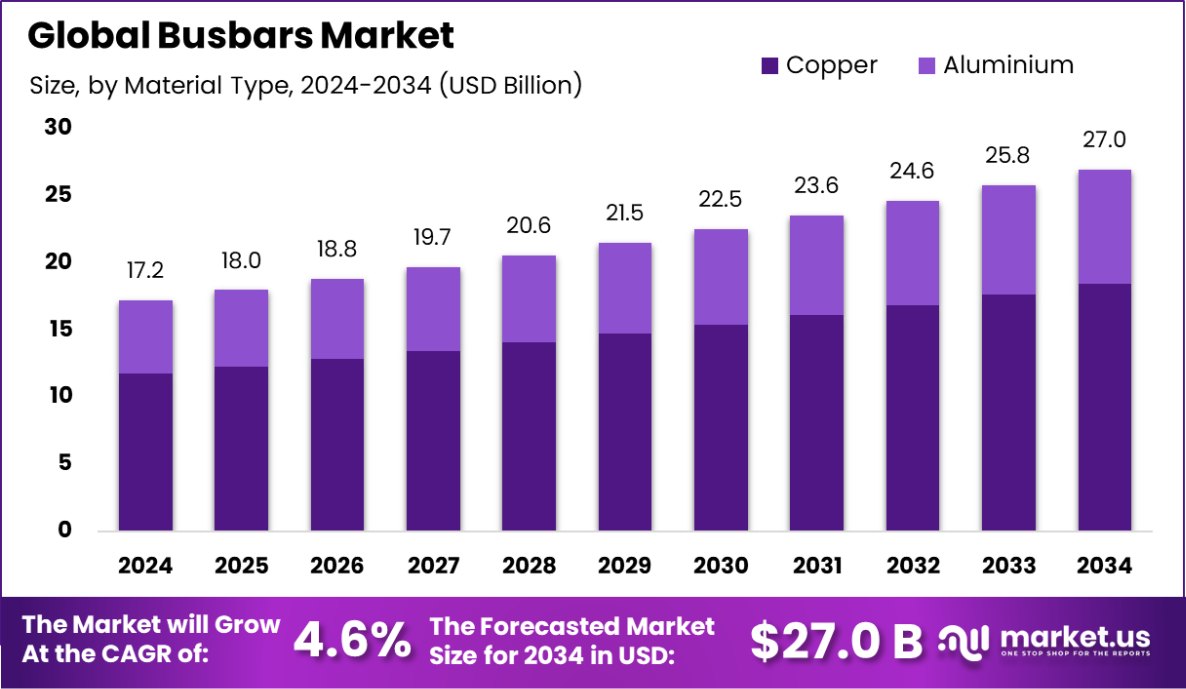

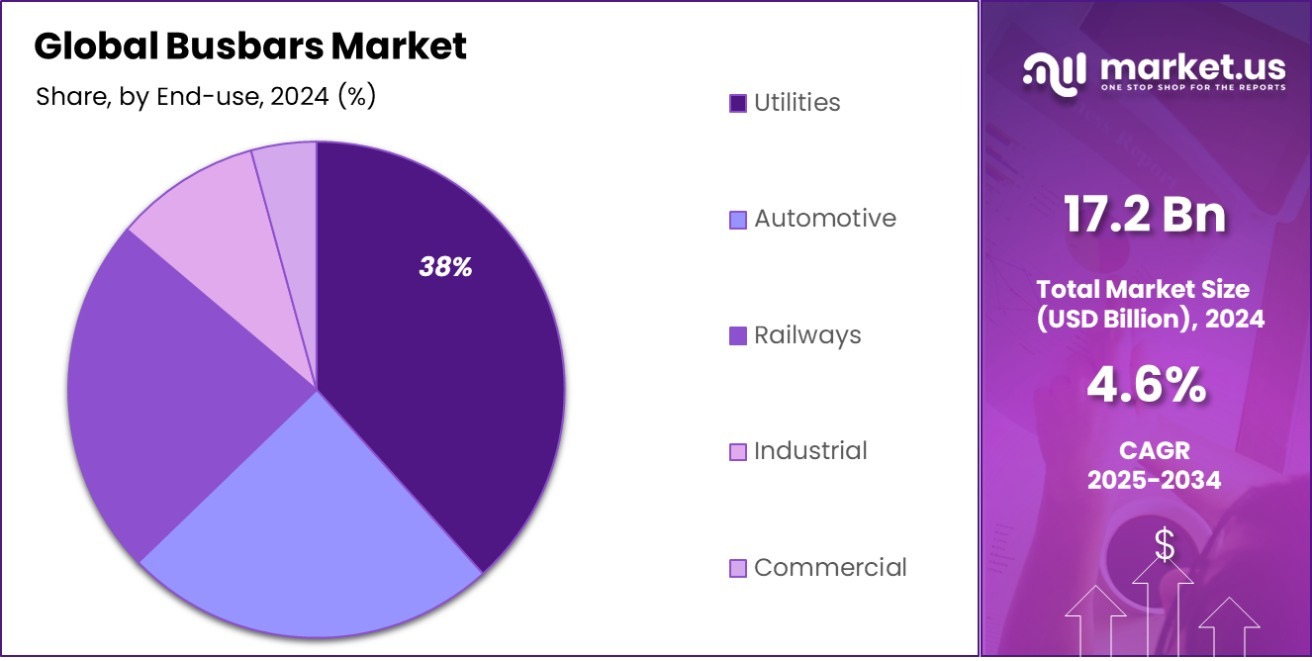

Global Busbar Market is expected to be worth around USD 27.0 billion by 2034, up from USD 17.2 billion in 2024, and grow at a CAGR of 4.6% from 2025 to 2034. The region’s Busbar Market dominance is evident with its Asia-Pacific 45.40% market share, totaling USD 7.8 billion.

A busbar is a metallic strip or bar, typically made from copper or aluminum, that conducts electricity within a switchboard, distribution board, substation, battery bank, or other electrical apparatus. Its primary purpose is to distribute power to electrical devices and equipment, consolidating incoming and outgoing electrical currents in a compact, controlled way. Busbars are essential for efficient power distribution and management, minimizing the space occupied and enhancing the safety and reliability of electrical systems.

The Busbar Market refers to the global industry centered around the manufacturing and distribution of busbars. This market is influenced by various sectors, including energy, manufacturing, and construction, due to the crucial role busbars play in electrical distribution. As industries and technologies advance, the demand for more efficient and robust power distribution solutions drives the growth of the busbar market.

One significant growth factor for the busbar market is the increasing demand for reliable and efficient energy solutions. As industries expand and infrastructure develops, especially in emerging economies, there is a growing need for robust electrical systems, boosting the demand for busbars.

Another growth driver is the global shift toward renewable energy. Busbars are vital in distributing power generated from renewable sources such as solar and wind, which require effective and efficient electrical distribution systems to handle high voltages and currents. This trend is accelerating the adoption of advanced busbar technologies.

Furthermore, the opportunity in the busbar market is linked to advancements in electric vehicle (EV) technology. EVs rely heavily on efficient power management systems, where busbars play a critical role in battery management and power distribution. As the EV market continues to expand, the demand for high-performance busbars is expected to increase significantly, presenting substantial opportunities for market growth.

Key Takeaways

- Global Busbar Market is expected to be worth around USD 27.0 billion by 2034, up from USD 17.2 billion in 2024, and grow at a CAGR of 4.6% from 2025 to 2034.

- Copper dominates By Material Type in the Busbar Market with a 67.40% share.

- Single Conductor leads By Type segment, holding 58.40% of the market.

- Medium power rating leads with a 47.60% share in the Busbar Market.

- Laminated insulation type holds a 50.50% share in the Busbar Market.

- Utilities are major end-users in the Busbar Market, holding a 38.40% share.

- With a market valuation of USD 7.8 billion, Asia-Pacific holds a 45.40% share in the Busbar Market.

By Material Type Analysis

The Busbar Market by material type shows copper leading with a substantial 67.40% share.

In 2024, Copper held a dominant market position in the By Material Type segment of the Busbar Market, with a 67.40% share. This significant market share is primarily attributed to copper’s superior electrical conductivity and efficiency in power distribution systems. The material’s high reliability and resistance to corrosion make it a preferred choice for various applications, ranging from industrial manufacturing to residential infrastructure.

The robust presence of copper busbars is also bolstered by their critical application in renewable energy systems, where efficient energy transfer is essential. As global industries continue to shift toward sustainable energy sources, the demand for copper busbars is expected to remain strong, supporting their dominant market position. Additionally, the development of smart cities and advancements in infrastructure are driving the adoption of copper busbars, given their effectiveness in managing high loads and distributing power evenly across extensive networks.

This segment’s outlook remains positive as innovations in material science and enhancements in copper alloy compositions are likely to improve the performance characteristics of copper busbars. With ongoing research and development aimed at increasing the efficiency of copper in electrical applications, the market share of copper busbars is poised for sustained growth in the coming years.

By Type Analysis

In terms of type, single conductors dominate the Busbar Market, holding a 58.40% market share.

In 2024, the Conductor held a dominant market position in the By Type segment of the Busbar Market, with a 58.40% share. This dominance is largely due to the essential role that conductors play in electrical distribution systems, where they facilitate the efficient transfer and management of electrical power. Their critical importance across a wide range of applications, from large-scale industrial facilities to commercial buildings, underpins their significant market share.

The high percentage reflects an increasing demand for reliable and efficient power distribution mechanisms driven by global urbanization and industrialization. As the backbone of electrical infrastructure, conductors made from materials like copper and aluminum are favored for their ability to handle substantial electrical loads with minimal energy loss, which is crucial for maintaining system efficiency and safety.

Looking forward, the market for conductors is expected to continue its growth trajectory, supported by ongoing developments in power technology and electrical infrastructure. The push towards more energy-efficient systems and the expansion of renewable energy installations worldwide are particularly likely to spur further adoption of high-performance conductors.

By Power Rating Analysis

Medium power rating busbars are prevalent, capturing 47.60% of the Busbar Market by power rating.

In 2024, Medium held a dominant market position in the By Power Rating segment of the Busbar Market, with a 47.60% share. This prominence in the market can be attributed to the versatile applications of medium power-rated busbars in both industrial and commercial sectors.

These busbars are designed to efficiently handle moderate levels of electrical currents, making them suitable for a wide range of applications that require a balance between power capacity and size, such as in medium-scale manufacturing facilities, large commercial buildings, and data centers.

The preference for medium power-rated busbars is driven by their ability to provide a cost-effective solution for energy distribution, offering a combination of performance and flexibility that is not always achievable with higher or lower power ratings. This segment’s substantial market share is also reflective of the ongoing expansion in industrial automation and smart building projects, where medium power-rated busbars are increasingly favored for their reliability and adaptability to modern electrical demands.

Given the continued growth in these sectors and the increasing focus on energy efficiency and system optimization, the demand for medium power-rated busbars is expected to remain strong. This will likely ensure their ongoing dominance in the busbar market, supported by technological advancements and evolving industry requirements.

By Insulation Type Analysis

The laminated insulation type is favored in the Busbar Market, accounting for 50.50% of the segment.

In 2024, Laminated held a dominant market position in the By Insulation Type segment of the Busbar Market, with a 50.50% share. This significant market presence is largely due to the unique advantages offered by laminated busbars, including enhanced safety, reliability, and efficiency in electrical distribution systems.

Laminated busbars are preferred for their compact design and ability to reduce system inductance and improve capacitance, which is crucial in applications requiring high-speed and high-power distribution with minimal electromagnetic interference.

The strong performance of laminated busbars is also tied to their extensive use in sectors such as data centers, telecommunications, and high-tech manufacturing facilities, where precise and efficient power distribution is critical. The design of laminated busbars allows for customized configurations that fit specific technical requirements, making them a versatile solution across various industries.

As industries continue to advance technologically, the demand for laminated busbars is expected to grow, driven by their critical role in modern electrical infrastructure projects. With ongoing innovations in insulation materials and techniques, laminated busbars are well-positioned to maintain their market dominance, catering to the evolving needs of a digitally-driven world.

By End-use Analysis

Utilities are a significant end-use sector in the Busbar Market, with a 38.40% share.

In 2024, Utilities held a dominant market position in the by-end-use segment of the Busbar Market, with a 38.40% share. This leading position reflects the critical role of busbars in the utility sector, where they are extensively used for effective power distribution and management within electrical grids and substations. Utilities rely on busbars to enhance the reliability and efficiency of power transmission, essential for meeting the growing energy demands of urban and rural areas alike.

The preference for busbars in utilities is driven by their ability to handle high currents and distribute power uniformly across extensive networks. This is particularly important in the context of expanding renewable energy integration, where busbars facilitate the efficient transmission of power from renewable sources to the grid. Additionally, the ongoing upgrades to aging electrical infrastructure globally are spurring the demand for advanced busbar solutions, supporting their dominant market position.

As the utility sector continues to evolve with technological advancements and shifts toward sustainable energy, the need for robust and efficient busbars remains pronounced. This trend is expected to sustain the growth of the busbar market in the utilities segment, underscoring its pivotal role in contemporary energy systems.

Key Market Segments

By Material Type

- Copper

- Aluminium

By Type

- Single Conductor

- Multi Conductor

By Power Rating

- Low

- Medium

- High

By Insulation Type

- Laminated

- Powder-coated

- Bare

By End-use

- Utilities

- Automotive

- Railways

- Industrial

- Commercial

Driving Factors

Increasing Demand for Energy Efficiency

One of the top driving factors of the Busbar Market is the increasing demand for energy efficiency in power distribution systems. As global energy consumption rises, there is a growing emphasis on optimizing the efficiency of electrical systems to reduce energy losses and enhance overall system performance. Busbars play a crucial role in this context due to their ability to distribute electricity effectively and minimize losses compared to traditional cabling systems.

This efficiency is particularly critical in high-demand environments like industrial facilities, large commercial complexes, and data centers, where even small improvements in energy distribution can lead to significant cost savings and sustainability benefits. The push towards greener and more energy-efficient buildings and infrastructure continues to drive the busbar market forward.

Restraining Factors

High Costs and Complex Installation Processes

A major restraining factor for the Busbar Market is the high cost and complexity involved in the installation processes. Installing busbars, especially in existing systems or complex new developments, requires significant technical expertise and can be more labor-intensive compared to conventional wiring methods. This complexity often results in higher upfront costs for projects, which can deter potential adopters, particularly in cost-sensitive markets.

Additionally, the customization needed for busbars to fit specific applications or infrastructure can add to the expenses, impacting the overall affordability and scalability of busbar solutions in various sectors. These factors can limit market growth, especially in regions where budget constraints are a significant concern for infrastructure development.

Growth Opportunity

Expansion into Renewable Energy Infrastructure Development

A significant growth opportunity for the Busbar Market lies in the expansion into renewable energy infrastructure development. As the world increasingly shifts towards sustainable energy sources like solar and wind power, the need for effective power distribution systems that can handle the variable outputs of these sources becomes paramount.

Busbars are ideal for integrating into renewable energy infrastructures due to their efficiency and capability to manage high-power overloads.

Their adaptability and durability make them suitable for both on-grid and off-grid renewable systems, enhancing their utility in diverse environmental conditions. The ongoing global push for cleaner energy solutions continues to drive investments in renewable infrastructure, presenting lucrative opportunities for growth in the busbar market.

Latest Trends

Integration of Smart Technology in Busbar Systems

A leading trend in the Busbar Market is the integration of smart technology into busbar systems. This trend involves incorporating advanced monitoring and control mechanisms that enhance the functionality and reliability of busbars. Smart busbars are equipped with sensors and connectivity features that allow for real-time data analytics, predictive maintenance, and enhanced operational efficiency.

These technologies enable precise control over power distribution, reduce downtime, and optimize energy usage, which are crucial for modern industrial and commercial settings. As industries continue to focus on digital transformation and IoT integration, smart busbars are becoming increasingly popular, providing significant improvements in safety and efficiency that drive their adoption in various applications across the electrical distribution sector.

Regional Analysis

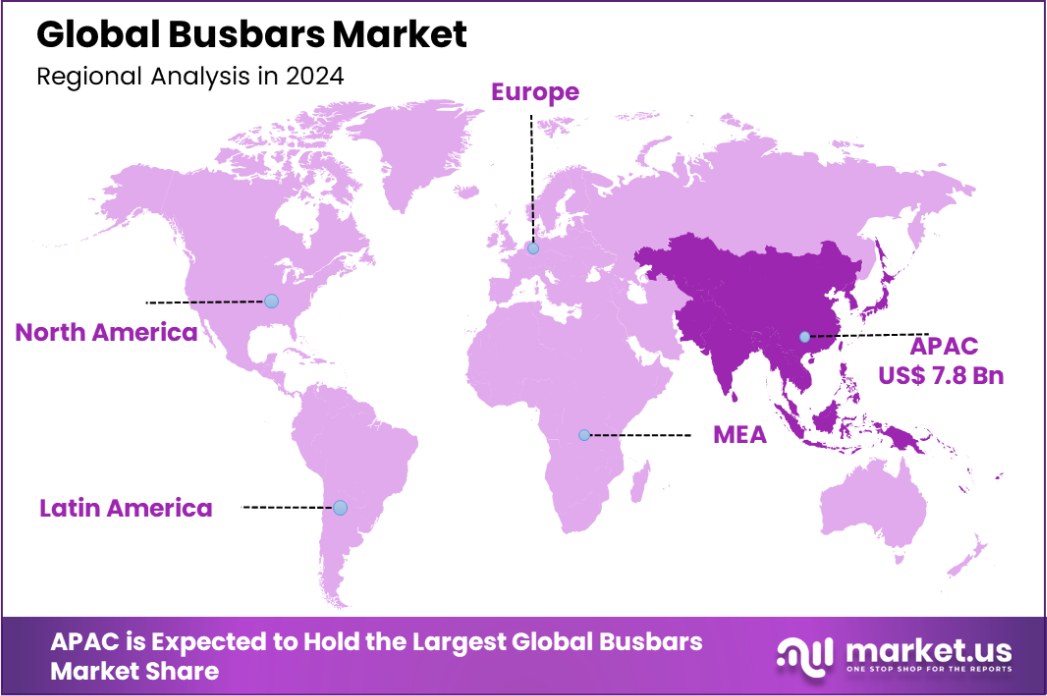

Asia-Pacific leads the Busbar Market with a commanding 45.40% share, valued at USD 7.8 billion.

The Busbar Market is witnessing varied growth across different regions, with Asia-Pacific emerging as the dominating region, accounting for 45.40% of the market share and valued at USD 7.8 billion. This substantial market presence is primarily driven by rapid industrialization and urbanization in major economies such as China and India.

These countries are experiencing significant investments in infrastructure development and renewable energy projects, which require robust and efficient power distribution systems like busbars.

In contrast, North America and Europe are also key players in the busbar market, albeit with a focus on upgrading existing infrastructure and integrating renewable energy sources into their grids. The push for energy efficiency and sustainability is driving the adoption of advanced busbar technologies in these regions.

Meanwhile, the Middle East & Africa, and Latin America are experiencing gradual growth in the busbar market. The focus in these regions is on developing the power and energy infrastructure to support economic growth and urban development.

Investments in new construction projects and energy systems in these regions are expected to increase the demand for busbars over the coming years, although they currently hold smaller shares compared to the Asia-Pacific.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In the global Busbar market of 2024, Schneider Electric SE, ABB Group, Methode Electronics Inc., Mersen, and Rogers Corporation are key players demonstrating significant influence and strategic growth.

Schneider Electric SE and ABB Group, being leaders in energy management and automation, have effectively leveraged their vast networks and technological expertise to innovate and supply busbars that meet evolving industry standards and efficiency requirements. Their focus on integrating smart technology into busbar systems positions them well within sectors pushing for digitalization and energy efficiency.

Methode Electronics Inc., known for its precision in manufacturing electrical components, stands out for its tailor-made solutions that cater to specific industry needs, enhancing the flexibility and applicability of busbars across various applications. This customization has proven vital in industries where standard solutions do not suffice, enabling Methode to carve a niche market presence.

Mersen, with its expertise in advanced materials science, has focused on enhancing the safety and durability of busbars. Their products are particularly noted for high reliability under harsh conditions, making them ideal for sectors like renewable energy, where stability and longevity are paramount.

Rogers Corporation, specializing in engineered materials, brings innovations that significantly reduce energy losses and improve overall system performance. Their research into new material composites for busbars provides superior electrical properties, which is crucial for high-demand applications and makes them a strong contender in the market.

Each of these companies, through their unique strengths and strategic market approaches, not only drives their individual growth but also collectively pushes the boundaries of what is possible in the Busbar market, catering to a rapidly evolving technological landscape.

Top Key Players in the Market

- Schneider Electric SE

- ABB Group

- Methode Electronics Inc

- Mersen

- Rogers Corporation

- Eaton

- Sun.King Technology Group Limited

- Chint Europe (UK) Ltd

- RYODEN KASEI CO.,LTD.

- Exxelia SAS

- TE Connectivity

- EAE Electric

- Molex, LLC

- Shanghai Eagtop Electronic Technology Co., Ltd.

- RPK Group

- Other Key Players

Recent Developments

- In 2024, Eaton invested $750M in a 65,000 sq.ft. facility for Bussmann EV fuses, creating 300 jobs. Supports growing demand for EV safety components.

- In December 2024, Mersen focused on automated busbar production lines for EV batteries, targeting European CAFE standards and collaborations with non-Chinese automakers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 17.2 Billion |

| Forecast Revenue (2034) | USD 27.0 Billion |

| CAGR (2025-2034) | 4.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Copper, Aluminium), By Type (Single Conductor, Multi Conductor), By Power Rating (Low, Medium, High), By Insulation Type (Laminated, Powder-coated, Bare), By End-use (Utilities, Automotive, Railways, Industrial, Commercial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Schneider Electric SE, ABB Group, Methode Electronics Inc, Mersen, Rogers Corporation, Eaton, Sun.King Technology Group Limited, Chint Europe (UK) Ltd, RYODEN KASEI CO.,LTD., Exxelia SAS, TE Connectivity, EAE Electric, Molex, LLC, Shanghai Eagtop Electronic Technology Co., Ltd., RPK Group, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |