Quick Navigation

Report Overview

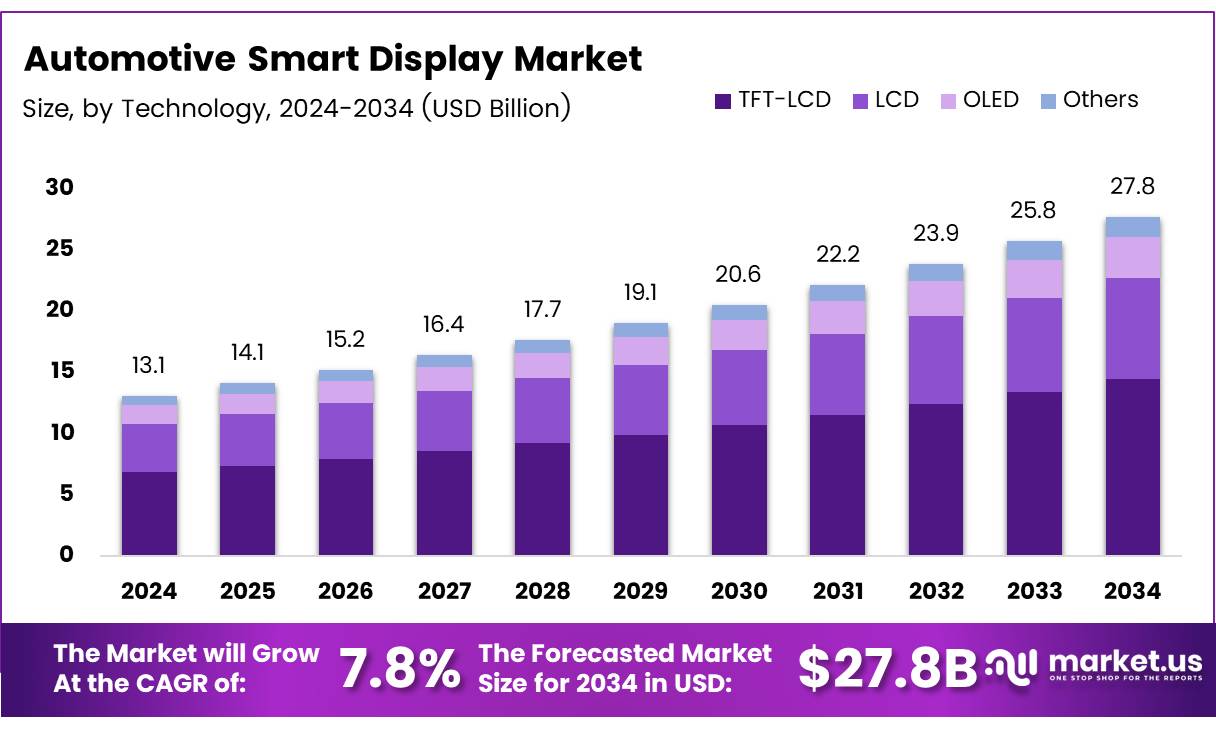

The Global Automotive Smart Display Market size is expected to be worth around USD 13.1 Billion by 2034, from USD 27.8 Billion in 2024, growing at a CAGR of 7.8% during the forecast period from 2025 to 2034.

The Automotive Smart Display Market encompasses an innovative segment of the automotive industry focused on integrating advanced display technologies into vehicle dashboards, instrument clusters, and infotainment systems. These smart displays are designed to enhance the driving experience by providing intuitive, interactive, and high-resolution interfaces that relay crucial information to the driver efficiently.

The market is propelled by advancements in display technology, such as LED, OLED, and TFT-LCD, which offer superior brightness, color accuracy, and energy efficiency compared to traditional displays.

The Automotive Smart Display sector is poised for significant expansion. This growth is driven by the increasing adoption of electric and autonomous vehicles, which incorporate more sophisticated display systems to manage and relay complex vehicle data. Furthermore, consumer demand for enhanced in-car experience and connectivity continues to push automotive manufacturers to innovate in this space.

According to Recent Statistics, the LTPS LCD technology captured 30% of total display shipments in Q2 2024, up from 28% in the previous quarter, and is expected to reach 33% by year-end, indicating a strong preference for high-quality display components in automotive applications.

In terms of opportunities and government influence, the Automotive Smart Display Market is witnessing substantial investment and regulatory attention. Governments worldwide are implementing standards and regulations that promote the use of advanced safety and environmental technologies in vehicles, indirectly boosting the smart display market. These regulations often encourage the adoption of technologies that enhance driver awareness and vehicle efficiency, aligning with the broader goals of reducing road accidents and emissions.

Moreover, the projected increase in the number of autonomous vehicles, as highlighted by Ciklum with an estimate of 3.5 million autonomous vehicles on American roads by 2025, underscores the potential for growth in the smart display market. This surge will necessitate further advancements in display technologies to accommodate the complex interfaces required for autonomous driving.

Simultaneously, as the market for AMOLED in automotive applications remains relatively small, despite its prevalence in smartphones, it presents an opportunity for market players to differentiate and capture niche segments by enhancing AMOLED technology for automotive use.

Key Takeaways

- The Automotive Smart Display Market is projected to decline from USD 27.8 billion in 2024 to USD 13.1 billion by 2034, with a CAGR of 7.8%.

- Displays smaller than 5 inches dominated the market in 2024 with a 45.1% share, favored in small to mid-sized vehicles.

- TFT-LCD technology was predominant in 2024, holding a 50.2% market share, known for its reliability and high-quality display.

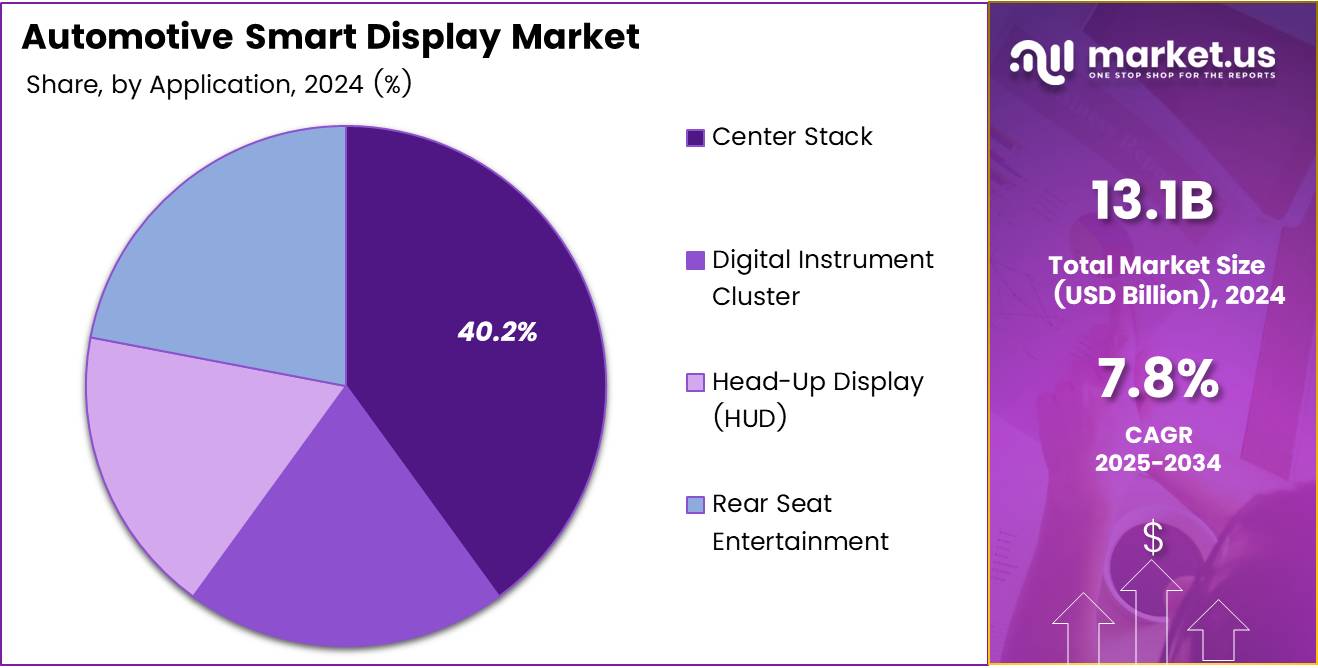

- The Center Stack application led with a 40.2% market share in 2024, central to improving multimedia access and vehicle control.

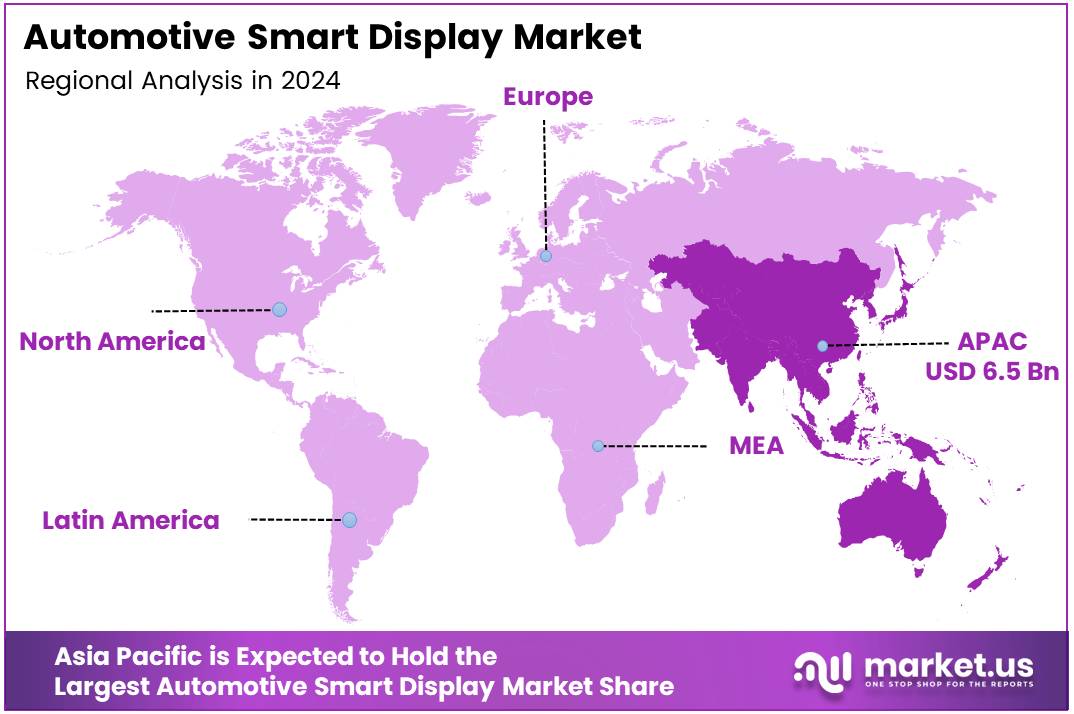

- Asia Pacific led the global market, accounting for 50.1% of the share and generating USD 6.55 billion in revenue, driven by strong automotive sectors in China, Japan, and South Korea.

Size Analysis

Compact Automotive Smart Displays Lead with Strong Market Hold

In 2024, the By Size Analysis segment of the Automotive Smart Display Market was distinctly led by displays measuring less than 5 inches, securing a dominant market share of 45.1%. This category benefitted primarily from its widespread integration in small to mid-sized vehicles, where space optimization is critical, and the demand for compact, efficient technology is high.

These smaller displays are preferred for their cost-effectiveness and lower power consumption, making them ideal for basic display functions like showing vehicle stats, multimedia information, and connectivity features.

The 5 to 10 size range of smart displays accounted for a substantial portion of the market as well. These medium-sized displays are typically utilized in higher-end models and provide enhanced usability with more advanced features such as touch-screen interfaces, navigation, and improved connectivity options. Their adaptability across various vehicle segments has helped sustain their market presence.

Meanwhile, smart displays larger than 10 are gradually gaining traction, particularly in luxury and high-performance vehicles. They offer superior graphics, larger viewing areas, and can integrate more complex functions, which enhance user interaction and safety. As consumer preferences shift towards larger, more interactive screens, this segment is expected to grow, albeit at a slower pace compared to its smaller counterparts due to higher costs and more complex installation requirements.

Technology Analysis

TFT-LCD Leads the Pack in Automotive Smart Display Technology with a 50.2% Market Share

In 2024, TFT-LCD held a dominant market position in the By Technology Analysis segment of the Automotive Smart Display Market, capturing a 50.2% share. This technology, renowned for its reliability and high-quality display capabilities, has become a staple in automotive applications, offering excellent visibility and durability under various environmental conditions.

Following TFT-LCD, LCD technology also maintained a significant presence, appreciated for its cost-effectiveness and wide-ranging application in budget-friendly vehicle models. OLED technology, known for its superior color contrast and sharpness, is gradually increasing its market penetration as it becomes more accessible and as consumer demand for higher-quality displays grows.

The Others category, which includes emerging technologies like AMOLED and flexible displays, is also gaining traction, promising innovative display solutions that could reshape future market dynamics. Collectively, these technologies are pivotal in enhancing user interface and experience, catering to evolving consumer preferences in the automotive sector.

Application Analysis

Center Stack Leads in Automotive Smart Displays with 40.2% Market Share

In 2024, the Center Stack continued to dominate the By Application Analysis segment of the Automotive Smart Display Market, boasting a 40.2% share. This segments prominence is primarily attributed to its integral role in enhancing user experience by centralizing access to multimedia and vehicle controls, thus improving driver engagement and safety.

Following the Center Stack, the Digital Instrument Cluster held a significant position, favored for its ability to provide drivers with crucial, easy-to-read vehicle diagnostics and navigational information directly within their line of sight. This technology has been crucial in streamlining information delivery, thereby reducing driver distraction and increasing road safety.

The Head-Up Display (HUD) also saw considerable adoption, driven by its advanced projection capabilities that display essential information on the windshield. HUD technology has been instrumental in keeping the drivers focus on the road, simultaneously providing real-time data like speed, navigation, and traffic alerts without the need to divert ones gaze.

Lastly, the Rear Seat Entertainment systems, although smaller in market share, remained a key component in luxury and family vehicles, offering value through enhanced passenger experience during long journeys. These systems have been pivotal in improving passenger comfort, which in turn contributes to the vehicle’s overall appeal and market competitiveness.

Key Market Segments

By Technology

- TFT-LCD

- LCD

- OLED

- Others

By Size

- Less than 5”

- 5”-10”

- Greater than 10”

By Application

- Center Stack

- Digital Instrument Cluster

- Head-Up Display (HUD)

- Rear Seat Entertainment

Drivers

Rising Adoption of ADAS Fuels Automotive Smart Display Market

The automotive smart display sector, the market is predominantly driven by several compelling factors. Firstly, the rising adoption of Advanced Driver Assistance Systems (ADAS) is pivotal, as these systems rely heavily on smart displays for effective real-time data visualization, enhancing safety and driving efficiency.

Concurrently, there’s a growing consumer demand for connected vehicles, which are equipped with seamless infotainment systems, advanced navigation, and robust internet connectivity—all facilitated through smart displays. Technological advancements in display panels, including OLED, AMOLED, and QLED, further boost this demand by offering superior visual clarity and responsiveness, making these displays more appealing to consumers and manufacturers alike.

Additionally, the surge in electric vehicle (EV) sales amplifies the need for integrated digital dashboards and sophisticated infotainment systems, marking a significant shift towards more digitally-centric vehicles. These elements together create a robust environment for the expansion of the automotive smart display market.

Restraints

High Production and Installation Costs Limit Smart Display Integration in Vehicles

The automotive smart display market faces considerable challenges that hinder its broader acceptance and integration into vehicles. Elevated production and installation costs associated with advanced display technologies make these systems less affordable, which can deter both manufacturers and consumers from adopting them.

Moreover, as vehicles become increasingly connected, there is a heightened risk of cybersecurity threats and concerns over data privacy. These issues not only complicate the implementation of smart displays but also slow down market growth by reducing consumer trust and willingness to invest in these technologies.

Growth Factors

Electric and Autonomous Vehicles Fuel Smart Display Market Growth

In the automotive industry, smart displays are poised for significant growth opportunities, particularly as electric and autonomous vehicles continue to evolve. These smart displays are essential in the new ecosystem of self-driving and electric cars, enhancing functionality and user experience through improved vehicle control interfaces and information systems.

Furthermore, the development of cutting-edge technologies like holographic and 3D displays is set to revolutionize the visual depth and interactivity of these systems, offering a more engaging user experience. The integration of biometric authentication methods, such as fingerprint and facial recognition, adds an extra layer of security, making vehicles safer and more personalized.

Additionally, the growth in shared mobility services, like ride-hailing and car-sharing, is increasing the demand for sophisticated in-vehicle entertainment and information systems. This demand creates a robust market for smart displays, underlining their importance in the next generation of automotive design and functionality.

Emerging Trends

Multi-Display Cockpits Shape the Future of Driving

The automotive smart display market is being transformed by several key trends that are shaping the future of driving experiences. One of the most prominent trends is the widespread adoption of multi-display cockpits, where vehicles feature several interconnected displays to provide a seamless and immersive driving experience. This setup enhances functionality and accessibility, allowing drivers and passengers to interact with various vehicle functions effortlessly.

Additionally, the integration of AI-powered voice assistants such as Alexa and Google Assistant into these displays is enhancing user interaction, making it more intuitive and hands-free. There is also a rise in personalized and adaptive displays that leverage AI to customize settings and visuals according to individual driver preferences, enhancing the personal connection between the vehicle and its user.

Moreover, as vehicles increasingly become software-defined, smart displays are becoming indispensable components of modern vehicle architectures. These displays serve as vital interfaces for the software that controls various vehicle functions, underscoring their growing importance in the automotive industry.

Regional Analysis

The Asia Pacific region holds a commanding lead in the Automotive Smart Display market, accounting for 50.1% of the global share and generating a revenue of USD 6.55 billion. This dominance is driven by robust automotive manufacturing sectors in countries such as China, Japan, and South Korea, coupled with high adoption rates of advanced vehicular technologies. Increasing consumer demand for enhanced safety features and connectivity solutions in vehicles also significantly contribute to the market’s expansion in this region.

Regional Mentions:

North America follows as a significant player in the Automotive Smart Display market, spurred by technological advancements and the integration of IoT and AI in automotive applications. The U.S. market is particularly buoyant due to its well-established automotive industry and early adoption of technologies such as heads-up displays and digital instrument clusters. Strategic collaborations between automotive manufacturers and tech companies in Silicon Valley are also pivotal in propelling market growth.

In Europe, the market is characterized by stringent automotive safety regulations, which drive the demand for smart display solutions that enhance user interface and safety. European automotive giants like Volkswagen, BMW, and Mercedes-Benz are at the forefront of integrating these advanced displays into their vehicles, further supported by a robust technological infrastructure and consumer preference for luxury vehicles.

The market in Latin America and the Middle East & Africa is emerging, with growth driven by gradual economic recovery, increasing vehicle sales, and growing awareness about vehicle safety technologies. In these regions, the expansion is slower compared to other regions but shows promise with increasing investments in automotive sectors and urbanization trends.

Overall, while the Asia Pacific region continues to dominate the Automotive Smart Display market, North America and Europe remain vital for the global market’s dynamics, contributing significantly to technological innovations and market expansion..

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the 2024 global Automotive Smart Display Market, Hyundai Mobis emerges as a pivotal player, distinguishing itself through innovation and market adaptation.

Hyundai Mobis has strategically positioned itself by integrating advanced technologies such as OLED and AMOLED displays into its product offerings, catering to the rising consumer demand for high-quality vehicle displays. The company’s commitment to R&D has enabled it to offer versatile smart display solutions, enhancing user experience and vehicle functionality.

Robert Bosch GmbH, another significant contender, excels in integrating smart display technologies with driver assistance systems, promoting safety and convenience. Bosch’s reputation for reliability and its broad automotive expertise enable it to maintain a strong market presence, while its investment in connected car technologies reinforces its competitive edge.

Continental AG stands out for its focus on sustainable and innovative display solutions. By leveraging its strong capabilities in software and system integration, Continental offers a wide range of smart displays that enhance interactive user interfaces and vehicle connectivity, which are crucial for autonomous driving solutions.

Panasonic Corporation and Pioneer Corporation also play key roles, with Panasonic focusing on the integration of infotainment and navigation features, and Pioneer leading in aftermarket smart display solutions. Both companies adapt swiftly to market trends, such as the shift towards larger, more interactive displays, ensuring their ongoing relevance in the market.

Visteon Corporation and Denso Corporation, with their robust focus on next-generation technologies, are set to capitalize on the trend towards digital cockpits. These companies are enhancing the driver’s user experience by integrating multi-functional displays that consolidate various control functions.

Overall, key players in the 2024 Automotive Smart Display Market are driven by technological advancements, consumer expectations for connectivity and interactivity, and the integration of digital interfaces into the automotive environment. This competitive landscape pushes continual innovation, particularly in enhancing the interface and user experience in automotive interiors.

Top Key Players in the Market

- Hyundai Mobis

- Robert Bosch GmbH

- Continental AG

- Panasonic Corporation

- Pioneer Corporation

- Alps Alpine Co., Ltd.

- Nippon Seiki Co., Ltd.

- Visteon Corporation

- SAMSUNG (HARMAN International)

- Denso Corporation

Recent Developments

- In February 2025, Europe announced a massive $208.4 billion investment in artificial intelligence, aimed at revolutionizing automotive production and enhancing innovation across the continent.

- In October 2023, AUO’s Board gave the green light for the acquisition of German company Behr-Hella Thermocontrol GmbH (BHTC), a move set to bolster AUO’s strategic expansion into the smart mobility ecosystem globally.

- In April 2024, Microchip Technology finalized the purchase of VSI Co. Ltd., a company renowned for its innovations in ADAS and digital cockpit connectivity, thereby solidifying its leadership in the automotive networking market.

- In November 2024, AUO declared the creation of AUO Mobility Solution Corporation, a new subsidiary focused on advancing its capabilities and offerings within the smart mobility sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 13.1 Billion |

| Forecast Revenue (2034) | USD 27.8 Billion |

| CAGR (2025-2034) | 7.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (TFT-LCD, LCD, OLED, Others), By Size (Less than 5”, 5”-10”, Greater than 10”), By Application (Center Stack, Digital Instrument Cluster, Head-Up Display (HUD), Rear Seat Entertainment) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Hyundai Mobis, Robert Bosch GmbH, Continental AG, Panasonic Corporation, Pioneer Corporation, Alps Alpine Co., Ltd., Nippon Seiki Co., Ltd., Visteon Corporation, SAMSUNG (HARMAN International), Denso Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |