Quick Navigation

Report Overview

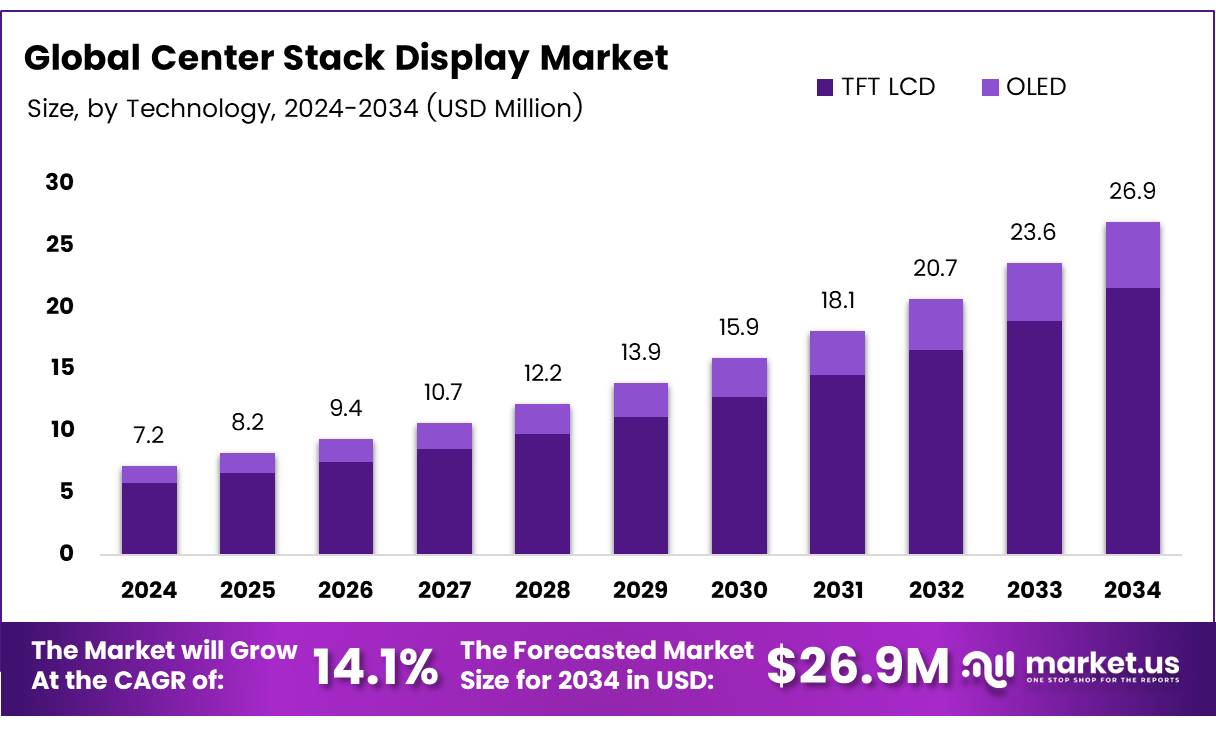

The Global Center Stack Display Market size is expected to be worth around USD 7.2 Million by 2034, from USD 26.9 Million in 2024, growing at a CAGR of 14.1% during the forecast period from 2025 to 2034.

The Center Stack Display Market refers to the segment of the automotive industry that focuses on the development, production, and integration of center stack displays within vehicle dashboards.

These displays are central control surfaces that provide drivers and passengers with interactive access to multimedia functions, navigation systems, climate controls, and vehicle settings. The rapid advancement in automotive technology, coupled with increasing consumer demand for enhanced in-vehicle experiences, has propelled the growth of this market.

The Center Stack Display Market is poised for significant expansion, driven by several key factors. The integration of advanced technologies such as touchscreens, haptic feedback, and voice control has transformed these displays into essential features of modern vehicles.

As the automotive industry continues to evolve towards more connected and autonomous vehicles, the role of center stack displays becomes increasingly critical. According to eta-publications, the number of autonomous vehicles is expected to surpass 54 million by 2024, indicating a direct correlation with the demand for sophisticated center stack systems capable of managing complex functionalities and providing greater user engagement.

Regarding market opportunities and growth, the Center Stack Display Market is experiencing a surge due to the global shift towards electric vehicles (EVs) and the standardization of high-tech in-car features.

As of March 2023, India alone had over 2.3 million electric vehicles, as noted by eta-publications, underscoring the broader adoption of EVs that typically feature advanced center stack displays. This trend is complemented by government investments and regulations promoting automotive safety and environmental standards, which often include mandates for technologies embodied in center stack displays.

Moreover, the market’s potential is further underscored by consumer expectations and regulatory requirements, pushing automotive manufacturers to equip over 75% of new passenger vehicles with center stack displays, as highlighted by the global risk community. This widespread adoption reflects the essential role of these systems in enhancing user interface and connectivity, critical for today’s tech-savvy consumers.

The convergence of these are factors technological advancements, regulatory frameworks, and shifting consumer preferences creates a robust environment for continued growth and innovation within the Center Stack Display Market. The ongoing integration of these systems in both conventional and emerging vehicle types marks a dynamic progression towards more interactive and user-centered automotive experiences.

Key Takeaways

- The global center stack display market is projected to shrink from USD 26.9 million in 2024 to USD 7.2 million by 2034, with a CAGR of 14.1%.

- TFT LCD technology dominated the market in 2024 with an 80.1% share due to its reliability and cost-effectiveness in automotive applications.

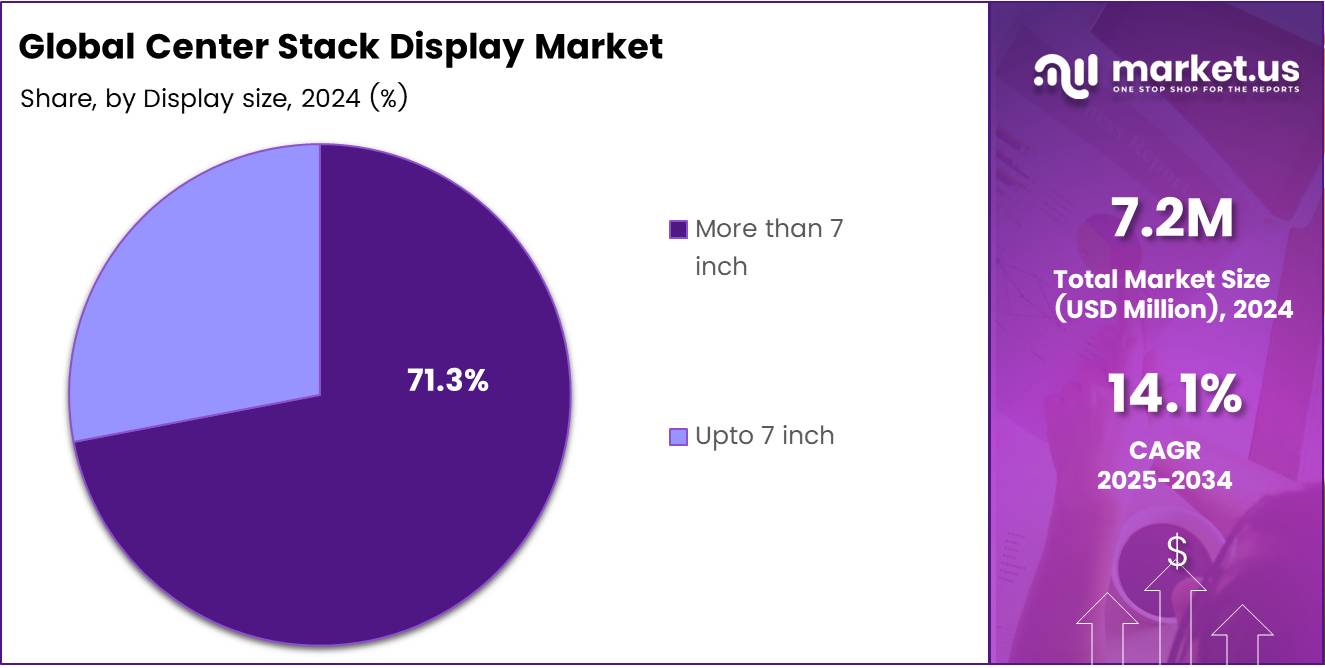

- Displays larger than 7 inches held a significant market share of 71.3% in 2024, preferred for their enhanced visibility and interactive capabilities.

- Passenger cars led the market in vehicle type, driven by the increasing integration of advanced infotainment systems.

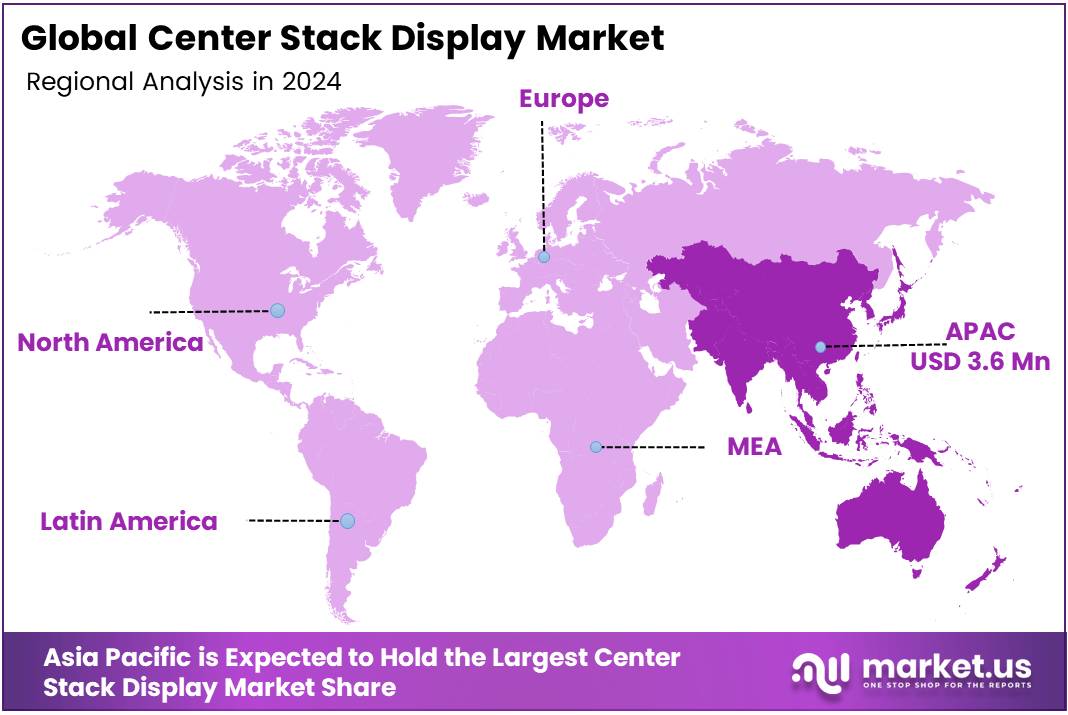

- The Asia Pacific region held a dominant 50.1% market share, fueled by a strong automotive industry and growing demand for luxury and high-tech vehicles.

Technology Analysis

TFT LCD Leads with 80.1% in Center Stack Display Technology, Outpacing OLED

In 2024, the Center Stack Display Market’s By Technology Analysis segment witnessed TFT LCD technology holding a commanding market share of 80.1%. This dominance is attributed to TFT LCD’s longstanding reputation for reliability and cost-effectiveness in automotive applications. As the automotive industry continues to prioritize cost efficiency alongside display performance, TFT LCD has become the preferred choice for center stack displays.

These displays are essential for controlling various in-car functions, including HVAC systems, multimedia, and connectivity settings, making their visibility and durability paramount.

In contrast, OLED technology, known for its superior contrast and color saturation, trails significantly in market share. Despite its aesthetic advantages, the higher cost and concerns over screen burn-in and lifespan in diverse automotive environments have hindered its widespread adoption in center stack applications.

However, as manufacturers work towards addressing these durability issues and reducing costs, OLED is expected to gradually increase its presence in the market. This anticipated growth will be driven by demand for more visually striking and energy-efficient display solutions in high-end vehicle segments.

Display Size Analysis

Large Center Stack Displays Lead with 71.3% Market Share Due to Consumer Preference for High-Visibility Interfaces

In 2024, the By Display Size Analysis segment of the Center Stack Display market was notably dominated by displays larger than 7 inches, capturing a 71.3% share. This significant majority underscores a clear preference among consumers for larger screens within vehicle dashboards, which offer enhanced visibility and a more interactive user experience. These larger displays support higher-resolution graphics and more sophisticated user interfaces, which are essential for modern infotainment systems and connectivity features.

Conversely, displays up to 7 inches accounted for the remaining market portion. While these smaller displays are typically found in compact vehicles and are valued for their cost-effectiveness and sufficient functionality, they do not meet the growing consumer demand for advanced vehicle technology and immersive display solutions.

The trend towards larger displays is driven by the consumer’s increasing desire for vehicles equipped with advanced navigation, connectivity, and entertainment systems, directly influencing the dynamics of the Center Stack Display market. As automotive manufacturers continue to innovate, the preference for more expansive and technologically equipped displays is expected to steer the market trajectory.

Vehicle Type Analysis

Passenger Cars Lead with Commanding Presence in Center Stack Display Market

In 2024, Passenger Cars held a dominant market position in the By Vehicle Type Analysis segment of the Center Stack Display Market. This category secured a substantial market share, attributed primarily to the increasing integration of advanced infotainment systems and connectivity solutions in passenger vehicles. As consumers demand more sophisticated user interfaces for navigation, communication, and entertainment, automakers have responded by significantly enhancing the center stack displays in their latest models.

Light Commercial Vehicles (LCVs) also experienced notable growth in this sector. The rise in LCV adoption for urban logistics and e-commerce delivery services has driven the demand for upgraded center stack displays that provide better route management and efficiency tools for drivers.

Heavy Commercial Vehicles (HCVs), while having a smaller share compared to Passenger Cars and LCVs, are seeing incremental growth in the adoption of center stack displays. The emphasis on safety and operational efficiency in HCVs is prompting fleet operators to invest in advanced display technologies that offer real-time vehicle monitoring and navigation assistance.

Overall, the escalating demand for high-tech vehicle features across all segments underscores the importance of center stack displays, with Passenger Cars leading the market due to their widespread consumer base and the rapid adoption of technological innovations.

Key Market Segments

By Technology

- TFT LCD

- OLED

By Display size

- More than 7 inch

- Upto 7 inch

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

By Application

- Navigation

- HVAC Control

- Infotainment

- Others

Drivers

Growing Demand for Connected Vehicles Bolsters Center Stack Display Market

As the automotive industry shifts towards connected vehicles, the demand for sophisticated center stack displays is soaring. These displays, which provide essential connectivity options, are becoming a standard expectation among consumers who seek enhanced in-car experiences. Advances in technology, particularly in OLED, LED, and TFT LCD displays, have significantly improved the functionality and visual appeal of these systems, further propelling market growth.

Additionally, the overall expansion of the automotive sector globally supports the increasing integration of these advanced displays into new vehicles. As consumer preferences evolve towards more interactive and informative driving experiences, manufacturers are compelled to adopt and innovate in center stack display technologies, making them a pivotal feature in modern cars.

Restraints

Driver Distraction Concerns May Hinder Center Stack Display Market Expansion

As an analyst examining the center stack display market, it’s crucial to recognize that despite the rapid adoption and technological advancements in this area, there are significant restraints that could temper market growth.

Consumer concerns about the potential for these displays to distract drivers are at the forefront. This apprehension is not unfounded, as the increasing complexity and functionality of center stack displays can divert attention from driving, raising safety issues.

Such concerns are likely to attract regulatory scrutiny, possibly leading to tighter regulations that could limit design aspects or the implementation of these systems.

Additionally, technical challenges such as screen glare and fingerprint marks, coupled with questions about the long-term reliability of these relatively new systems, further complicate the market’s expansion. These factors collectively create a cautious atmosphere among manufacturers and consumers alike, potentially stalling the widespread adoption of advanced display technologies in vehicles.

Growth Factors

Expanding Vehicle Sales in Developing Regions Drive Market Growth

The center stack display market is poised for significant growth, primarily driven by expanding vehicle sales in emerging markets. These regions present a fertile ground for market expansion as rising consumer incomes and urbanization boost demand for vehicles equipped with advanced technologies, including high-quality center stack displays.

Additionally, forging partnerships with automotive Original Equipment Manufacturers (OEMs) offers lucrative opportunities for developing customized, integrated display solutions that enhance user experience and meet specific automaker needs. Innovations in user interface design are also crucial, as more intuitive and user-friendly displays can substantially differentiate products in a competitive landscape.

Moreover, the adoption of curved and flexible displays can cater to luxury and technologically savvy consumers, further expanding the market’s reach. Each of these elements—market expansion in developing regions, strategic OEM partnerships, user interface innovations, and advanced display technologies—contributes to a robust growth trajectory for the center stack display industry.

Emerging Trends

Bigger Screens Lead the Charge in Center Stack Display Innovations

The center stack display market is witnessing a notable shift towards larger screens, catering to consumer demands for enhanced interactivity and richer information display. This trend is being driven by several key factors. Firstly, the penetration of touchscreen technology is replacing traditional button-based systems, offering a more intuitive user experience.

Additionally, voice control integration is becoming increasingly common, allowing drivers to operate systems hands-free, which significantly improves safety by minimizing distractions. Furthermore, augmented reality (AR) technology is being integrated into these displays, projecting critical information and navigation aids directly onto the screen, thereby enhancing visibility and safety. These innovations not only boost the functionality of vehicle dashboards but also align with the growing expectations for a connected, seamless driving experience.

Regional Analysis

Asia Pacific Leads Center Stack Display Market with 50.1% Share, Driven by Strong Automotive Production and Tech Adoption

The Asia Pacific region dominates the global center stack display market, commanding a substantial 50.1% share and generating revenues of USD 3.6 million. This significant market dominance can be attributed to several factors, including a robust automotive industry, rapid advancements in automotive technology, and increasing consumer demand for luxury and technologically enhanced vehicles.

Countries like China, Japan, and South Korea, known for their automotive manufacturing prowess, are driving innovation in center stack technologies, integrating high-resolution displays and connectivity features that appeal to tech-savvy consumers.

Regional Mentions:

In North America, the center stack display market is driven by a strong preference for high-end vehicles equipped with advanced infotainment systems. The United States leads the region, supported by technological innovation and a high adoption rate of new technologies such as touch screen and voice-activated controls, contributing to the market’s growth.

Europe follows closely, with a focus on luxury vehicles that include sophisticated center stack displays as standard features. The region’s stringent regulations regarding driver safety and fuel efficiency encourage manufacturers to integrate advanced display technologies that provide critical information with minimal distraction.

The Middle East & Africa region, although smaller in market size compared to other regions, is experiencing growth due to an increasing number of luxury vehicles sold in countries like the UAE and Saudi Arabia. These markets are seeing a rise in demand for vehicles equipped with advanced navigation and entertainment systems, boosting the adoption of center stack displays.

Latin America shows promising growth potential, driven by recovering economic conditions and a growing middle class that is increasingly interested in vehicles with advanced technological features. Countries such as Brazil and Mexico are witnessing an increase in automotive sales, paired with a rising demand for connectivity and infotainment systems in vehicles, which is expected to boost the region’s market in the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2024, the global Center Stack Display (CSD) market remains highly competitive with several key players driving innovation and growth. Among them, Continental AG, Alpine Electronics, Inc., and Visteon Corporation are particularly noteworthy due to their strategic advancements and market penetration.

Continental AG has consistently been at the forefront of the CSD market, leveraging its extensive expertise in automotive technology. The company’s focus on integrating advanced driver assistance systems (ADAS) with center stack displays offers a more interactive and safer driving experience, appealing to both automakers and consumers seeking enhanced connectivity and safety features.

Alpine Electronics, Inc., known for its high-quality audio and navigation systems, has made significant inroads in the CSD market by integrating multimedia and infotainment capabilities. Their products stand out for their user-friendly interfaces and superior display technology, catering effectively to the luxury and mid-tier vehicle segments.

Visteon Corporation has distinguished itself with its innovative approach to digital cockpit solutions. By focusing on customizable and scalable platforms, Visteon meets the diverse needs of global automakers. Their emphasis on cloud-connected services and the integration of artificial intelligence (AI) in displays is setting new standards in the industry, potentially reshaping future market dynamics.

These companies, along with other key players like Panasonic Holdings Corporation and Robert Bosch Manufacturing Solutions GmbH, contribute to a dynamic market environment. Their continual investment in R&D and strategic partnerships are crucial in driving the evolution of center stack technologies, ultimately influencing consumer preferences and technological adoption in the automotive sector.

Top Key Players in the Market

- Continental AG

- Alpine Electronics, Inc.

- MTA S.p.A

- PREH GMBH

- Panasonic Holdings Corporation

- Texas Instruments Incorporated

- HARMAN International

- MOBIS INDIA LIMITED

- Robert Bosch Manufacturing Solutions GmbH

- Visteon Corporation.

Recent Developments

- In November 2024, Alt Mobility secured a series A funding round of US$ 10 million to advance its innovations in alternative mobility solutions, focusing on eco-friendly transportation options.

- In July 2024, Matter raised $35 million in fresh funding to bolster its e-bike development and manufacturing capabilities, aiming to enhance sustainable urban mobility.

- In January 2024, Italy-based Mogu raised €11 million to expand its production of mycelium materials, targeting applications in interior design, fashion, and automotive industries, supporting sustainability and innovation

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 7.2 Million |

| Forecast Revenue (2034) | USD 26.9 Million |

| CAGR (2025-2034) | 14.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (TFT LCD, OLED), By Display size (More than 7 inch, Upto 7 inch), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), By Application (Navigation, HVAC Control, Infotainment, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Continental AG, Alpine Electronics, Inc., MTA S.p.A, PREH GMBH, Panasonic Holdings Corporation, Texas Instruments Incorporated, HARMAN International, MOBIS INDIA LIMITED, Robert Bosch Manufacturing Solutions GmbH, Visteon Corporation. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |