Quick Navigation

Market Overview

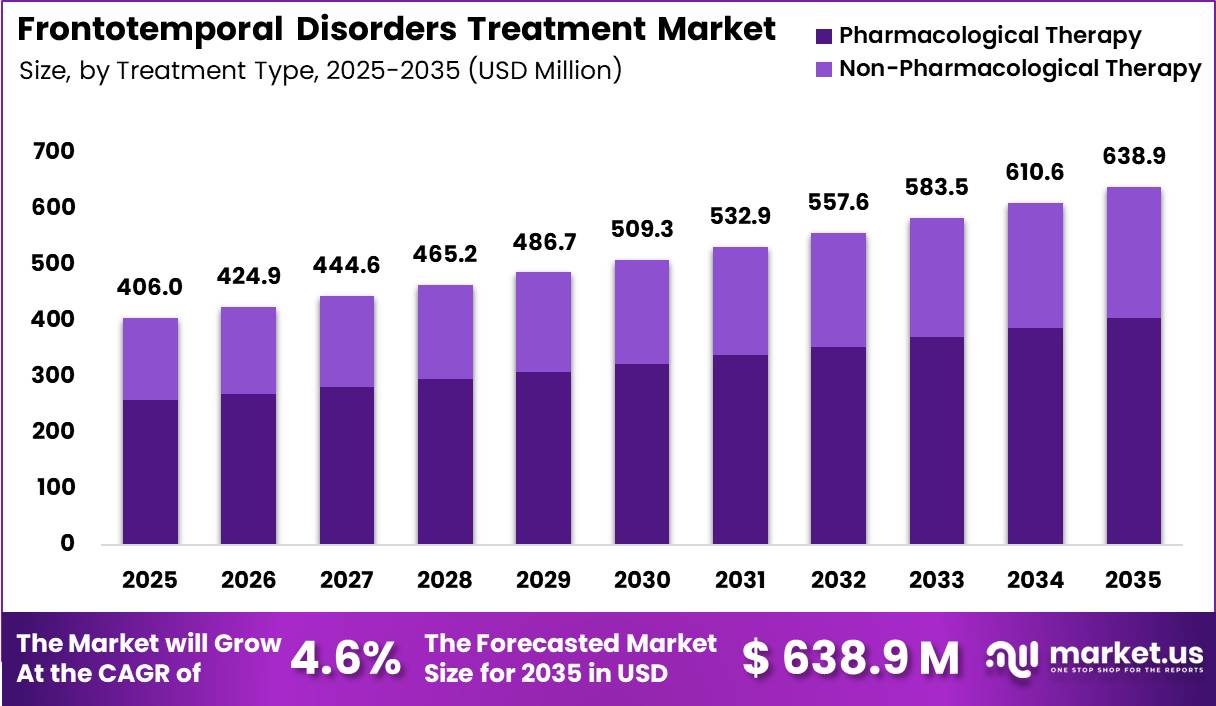

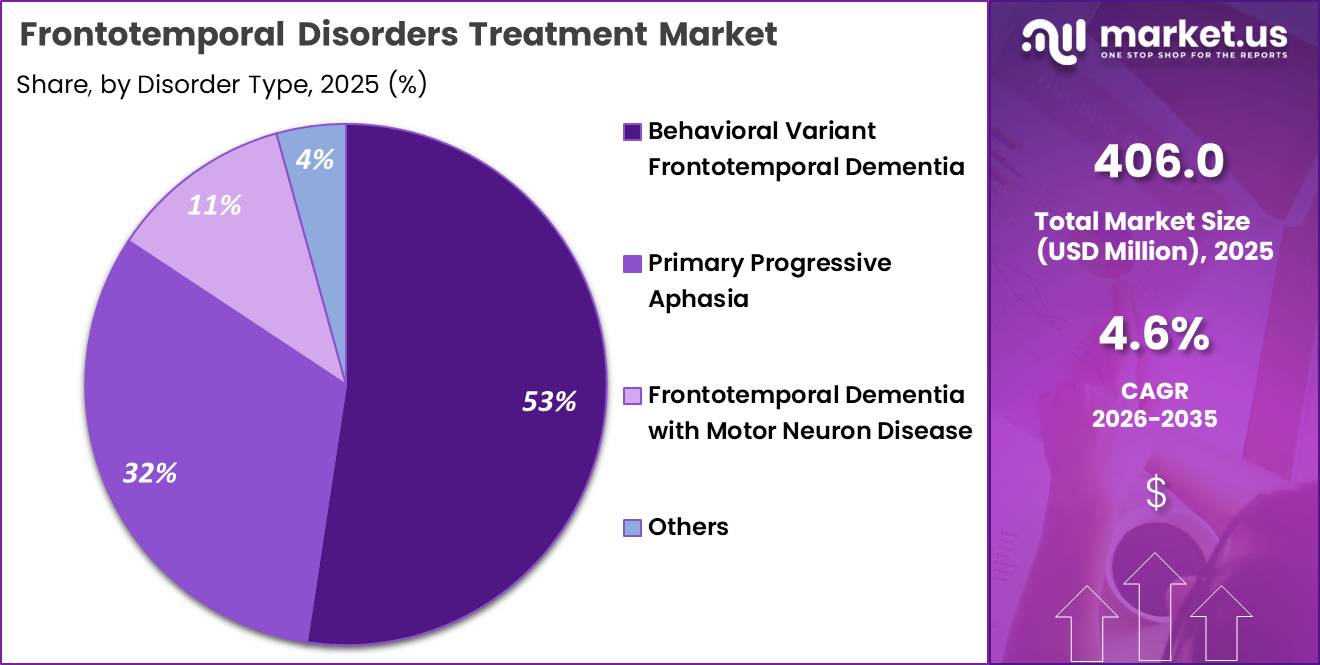

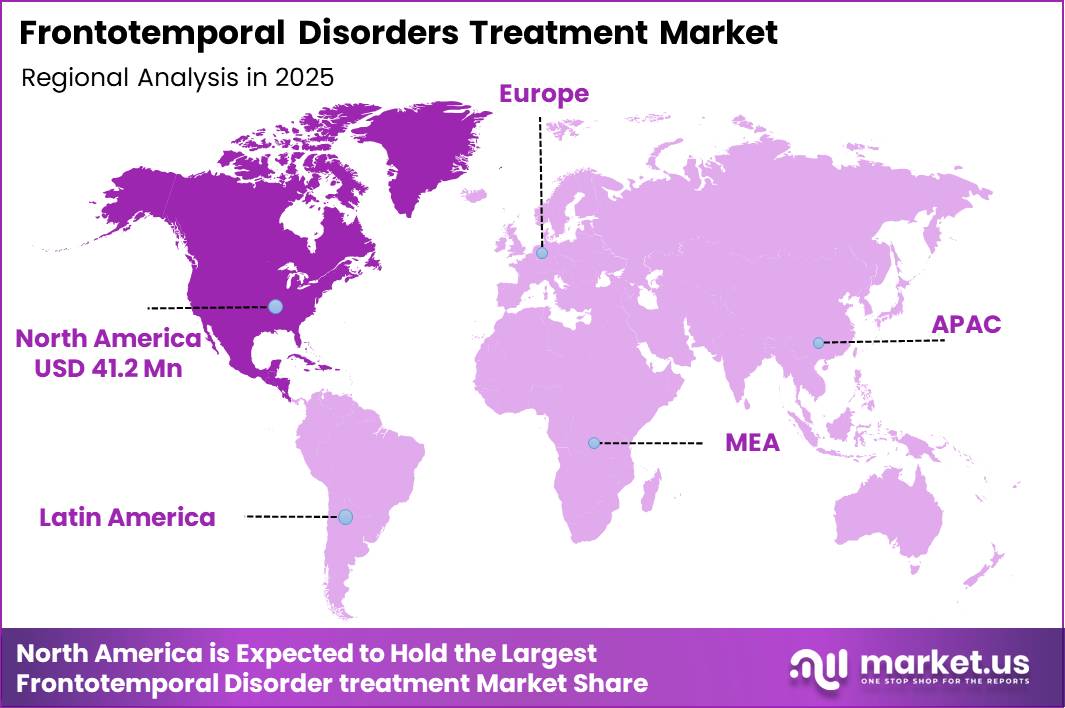

Global Frontotemporal Disorders Treatment Market size is expected to be worth around US$ 638.9 Million by 2035 from US$ 406.0 Million in 2025, growing at a CAGR of 4.6% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 41.2% share with a revenue of US$ 167.29 Million.

Frontotemporal disorders are a group of progressive neurodegenerative conditions that affect the frontal and temporal lobes of the brain, regions responsible for behavior, judgment, language, and movement.

These disorders, often referred to collectively as frontotemporal dementia (FTD), tend to occur earlier in life than Alzheimer’s disease, commonly striking adults between 45 and 64 years of age. Symptoms may include changes in personality, social conduct, language difficulties, and movement problems, and progressively worsen over time.

Currently, there is no cure and no treatment proven to slow or stop disease progression. Medications are used to manage specific symptoms: selective serotonin reuptake inhibitors (SSRIs) can help address behavioral symptoms such as social disinhibition, irritability, or depression; low-dose antipsychotics may be considered cautiously for severe agitation.

Speech, physical, and occupational therapies support communication and daily functioning, and personalized care plans are developed with multidisciplinary teams of neurologists, therapists, and caregivers.

Non-pharmacological approaches including tailored communication strategies, structured routines, safety adaptations, and caregiver education are central to improving quality of life for patients and families. Research funded by the NIH and other public health agencies continues to explore novel therapeutic targets, clinical trials, and biomarkers to inform future disease-modifying treatments.

Key Takeaways

- Market Size: Global Dental Medical Instruments Market size is expected to be worth around US$ 43.1 billion by 2035 from US$ 21.3 billion in 2025.

- Market Share: The market is growing at a CAGR of 7.30% during the forecast period from 2026 to 2035.

- Treatment Type Analysis: In 2025, pharmacological therapy dominated the market with a 63.5% share, reflecting its central role in managing behavioral symptoms, mood disturbances, and cognitive decline associated with frontotemporal disorders.

- Disorder Type Analysis: In 2025, behavioral variant frontotemporal dementia (bvFTD) dominated the market with a 52.4% share.

- Route of Administration Analysis: In 2025,oral administration dominated the market with an 81.2% share, making it the most preferred route across all treatment settings.

- Distribution Channel Analysis: In 2025,retail pharmacies dominated the market with a 46.5% share, highlighting their accessibility and convenience for patients and caregivers managing long-term treatment.

- Regional Analysis: In 2025, North America led the market, achieving over 36.00% share with a revenue of US$ 7.7 billion.

Treatment Type Analysis

The treatment type segmentation of the Frontotemporal Disorders Treatment Market is broadly divided into pharmacological therapy and non-pharmacological therapy. In 2025, pharmacological therapy dominated the market with a 63.5% share, reflecting its central role in managing behavioral symptoms, mood disturbances, and cognitive decline associated with frontotemporal disorders.

Medications such as antidepressants, antipsychotics, and mood stabilizers are commonly prescribed to reduce agitation, impulsivity, depression, and anxiety, which are major challenges for patients and caregivers. The dominance of this segment is supported by widespread clinical adoption, ease of administration, and ongoing research aimed at symptom-targeted drug development.

The non-pharmacological therapy segment accounted for 36.5% of the market and plays a critical supportive role in disease management. This segment includes speech therapy, behavioral interventions, occupational therapy, and caregiver training programs. These approaches are particularly important for preserving daily functioning, communication skills, and quality of life, especially as the disease progresses.

Growing awareness of holistic care, combined with multidisciplinary treatment models, is expected to gradually strengthen the contribution of non-pharmacological therapies within the overall market landscape

Disorder Type Analysis

Based on disorder type, the market is segmented into behavioral variant frontotemporal dementia (bvFTD), primary progressive aphasia (PPA), and frontotemporal dementia with motor neuron disease (FTD-MND). In 2025, behavioral variant frontotemporal dementia (bvFTD) dominated the market with a 52.4% share.

This dominance is driven by its higher prevalence and the significant behavioral and personality changes it causes, which often require long-term medical and supportive treatment. Patients with bvFTD frequently exhibit disinhibition, apathy, and compulsive behaviors, increasing demand for both drug-based and supportive therapies.

Primary progressive aphasia (PPA) accounted for 31.9% of the market, supported by the rising need for speech and language therapies alongside symptomatic medications. Early diagnosis and growing awareness of language-focused neurodegenerative disorders contribute to this segment’s steady growth.

Meanwhile, FTD-MND represented 11.4% of the market, reflecting its lower prevalence but high disease severity. This segment requires complex, multidisciplinary care, including neurological and motor symptom management, which sustains its presence despite a smaller patient population.

Route of Administration Analysis

By route of administration, the Frontotemporal Disorders Treatment Market is categorized into oral, injectable, and other routes. In 2025,oral administration dominated the market with an 81.2% share, making it the most preferred route across all treatment settings.

Oral drugs are widely used due to their convenience, patient compliance, and suitability for long-term therapy, which is essential in chronic neurodegenerative conditions like frontotemporal disorders. Most antidepressants, antipsychotics, and cognitive-support medications are available in oral formulations, reinforcing this segment’s leadership.

The strong dominance of oral therapies is also supported by ease of dose adjustment and lower treatment complexity for caregivers and healthcare providers. Injectable and other alternative routes hold a smaller share and are mainly used in specific clinical situations, such as severe behavioral symptoms or when oral intake becomes difficult.

However, these routes often require medical supervision, limiting their widespread adoption. Overall, the preference for non-invasive, easy-to-administer treatments ensures that oral administration remains the primary route in the market.

Distribution Channel Analysis

The distribution channel segmentation includes retail pharmacies, hospital pharmacies, and online pharmacies. In 2025,retail pharmacies dominated the market with a 46.5% share, highlighting their accessibility and convenience for patients and caregivers managing long-term treatment.

Retail pharmacies play a crucial role in dispensing chronic medications, offering refill services, and providing patient counseling, which is particularly important for neurodegenerative disorders requiring continuous care.

Hospital pharmacies represent a significant share due to their role in diagnosis-linked treatment initiation and management of severe or advanced cases. Patients often begin therapy in hospital settings, especially during neurological evaluations or acute behavioral episodes.

Meanwhile, online pharmacies are gradually gaining traction, supported by increasing digital adoption and home-delivery services, especially for repeat prescriptions. Despite this growth, trust, immediate availability, and face-to-face interaction keep retail pharmacies as the leading distribution channel. Their strong network and patient familiarity continue to support their dominant position in the Frontotemporal Disorders Treatment Market.

Market Segmentations

Treatment Type

- Pharmacological Therapy

- Antidepressants

- Selective Serotonin Reuptake

- Inhibitors (SSRIs) Tricyclic Antidepressants (TCAs)

- Others

- Antipsychotics

- Cognitive Enhancers

- Mood Stabilizers

- Anxiolytics

- Others

- Non-Pharmacological Therapy

- Speech & Language Therapy

- Occupational Therapy

- Physical Therapy

- Behavioral Therapy

- Cognitive Rehabilitation

- Others

Disorder Type

- Behavioral Variant Frontotemporal Dementia (bvFTD)

- Primary Progressive Aphasia (PPA)

- Nonfluent/Agrammatic Variant PPA

- Semantic Variant PPA

- Logopenic Variant PPA

- Frontotemporal Dementia with Motor Neuron Disease (FTD-MND)

- Others

Route of Administration

- Oral

- Injectable

- Others

Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Challenges

Biomarker Validation Gaps

A major constraint in frontotemporal dementia drug development is the incomplete validation of biomarker systems needed to reliably support diagnosis, patient stratification, pharmacodynamic tracking, and payer-acceptable outcomes across heterogeneous disease subtypes.

While markers such as blood neurofilament light provide useful disease-activity signals and progranulin is informative in specific genetic forms, there is still no universally robust biomarker framework that performs consistently across behavioral-variant FTD, primary progressive aphasia subtypes, and mutation-defined cohorts.

This forces trial designs to rely on layered and often redundant evidence strategies, combining plasma panels, cerebrospinal fluid analysis, volumetric MRI, FDG-PET imaging, and exploratory tracers to compensate for uncertainty in endpoint selection.

As a result, development programs face 6–12 month extensions in trial timelines,12–18% higher per-patient evidence generation costs, and increased operational complexity from multiple assay handoffs across multicenter studies.

The lack of standardized, widely trusted biomarker pathways also slows clinical adoption and reimbursement alignment, keeping late-stage development and commercialization dependent on incremental validation rather than streamlined translational pathways.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Biomarker Validation Gaps | -1.6% | North America core, EU academic hubs, Japan specialty centers | Medium term (2-4 years) |

| Phenotype Trial Heterogeneity | -1.9% | US trial clusters, EU referral networks, Australia-Canada rare disease sites | Long term (≥ 4 years) |

| Specialist Capacity Shortfall | -1.3% | North America core, EU secondary cities, emerging APAC neurology corridors | Long term (≥ 4 years) |

| Rare-Disease Recruitment Burden | -1.7% | US pivotal studies, Western Europe, multinational orphan-trial corridors | Medium term (2-4 years) |

| Genetic Testing Access Friction | -1.1% | North America core, EU reimbursement-sensitive markets, urban APAC centers | Medium term (2-4 years) |

| Post-Phase-3 Capital Repricing | -1.4% | US biotech financing base, UK-EU translational clusters | Short term (≤ 2 years) |

Opportunity

Genotype-led therapy platforms

Genotype-led therapy platforms in frontotemporal dementia represent an emerging opportunity rather than a current market driver because most care today is still focused on symptomatic management and fragmented experimental programs, while the real commercial white space lies in genetically stratified treatment pathways targeting subtypes such as GRN, MAPT, and C9orf72.

Although FTD is a rare disease overall, a meaningful share of cases is genetically defined, including roughly 25%–30% inherited forms and about 5%–10% linked specifically to GRN mutations, creating a smaller but highly addressable population for precision therapies. This enables a platform model where gene therapies and biologics can be developed with mutation-specific labeling, supported by companion diagnostics and biomarker-linked monitoring systems.

Even with mixed clinical signals such as late-stage biomarker-correction failures, the long-term direction supports second-generation assets, improved endpoint design, and tighter integration between therapeutic and diagnostic stacks.

The economic upside comes from high-value orphan pricing, strong gross margins, and expansion from single-mutation indications into adjacent neurodegenerative cohorts, with adoption potentially reaching 8%–12% of diagnosed patients in core Western markets by the early 2030s, as integrated therapy-and-testing platforms gradually replace fragmented care pathways.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Genotype-led therapy platforms | +2.4% | North America core, EU, Japan | Medium term |

| Biomarker-first early intervention | +2.1% | US, EU5, academic Asia hubs | Medium term |

| Digital speech and home neurocare | +1.6% | North America, EU, urban APAC | Short term |

| Orphan route expansion into APAC | +1.8% | China, Japan, South Korea, Australia | Medium term |

| Rare-neuro roll-up and companion Dx M&A | +1.9% | US and EU biotech clusters | Short term |

| Caregiver and employer-linked monetization | +1.3% | US, Canada, Western Europe | Short term |

Driver

Orphan-drug incentives and regulatory facilitation

FTD remains commercially attractive as a rare, high-unmet-need indication because orphan frameworks can partially offset weak absolute patient numbers through regulatory support, data exclusivity, and faster sponsor engagement.

In the EU, an AAV1 human GRN gene therapy received orphan designation for FTD in 2021 and remains a reference point for regulator openness to subtype-specific innovation, while in the U.S. PBFT02 received both Fast Track and Orphan Drug designation for FTD-GRN, validating that agencies view the indication as suitable for expedited rare-disease development pathways.

These designations do not guarantee approval, but they improve project economics by supporting financing, partnership formation, and earlier market-access planning; for a treatment class likely to target a few thousand highly characterized patients per launch region, even a 6–12 month reduction in development friction can materially increase net present value and sustain market CAGR above a pure symptomatic-care baseline

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biomarker-led earlier FTD identification | +1.9% | North America core, EU5 core, Japan selective | Short term (≤ 2 years) |

| Genetic and precision-therapy pipeline acceleration | +2.6% | U.S. core, EU orphan corridors, UK, select APAC tertiary centers | Medium term (2-4 years) |

| Trial-network and registry expansion improving patient capture | +1.4% | U.S. academic hubs, Western Europe, Australia spill-over | Short term (≤ 2 years) |

| Orphan-drug incentives and regulatory facilitation | +1.2% | U.S., EU, UK | Medium term (2-4 years) |

| Rising economic burden of early-onset dementia shifting care models | +1.7% | North America core, EU, urban APAC | Short term (≤ 2 years) |

| Remote neuromodulation and specialty supportive-care innovation | +1.0% | U.S., Canada, EU, developed APAC | Medium term (2-4 years) |

Restraint

Diagnostic Ambiguity

Diagnostic uncertainty remains one of the most significant barriers to frontotemporal disorders treatment adoption because the disease is frequently underrecognized and misdiagnosed, particularly outside specialist neurology settings. Current estimates suggest a prevalence of approximately 20 per 100,000 people aged 45–64, yet the true burden is widely considered underestimated due to overlapping symptoms with psychiatric and other neurodegenerative conditions.

Definitive diagnosis often requires extensive evaluation, including MRI, neuropsychological testing, and in some cases FDG-PET, cerebrospinal fluid analysis, or genetic testing, with genetic confirmation available only in familial cases and pathological confirmation typically occurring post-mortem. As a result, patients commonly experience 9–15 months of delay between initial behavioral or language symptoms and specialist-confirmed treatment eligibility.

The challenge is further compounded by the absence of widely adopted biomarkers capable of reliably differentiating underlying disease biology, such as tau-related versus TDP-43-related pathology. This diagnostic complexity increases pre-treatment costs, slows patient identification and referral pathways, raises medical affairs and education requirements, and ultimately limits the speed at which emerging therapies can translate into meaningful treated-patient growth.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diagnostic ambiguity | -2.1% | North America core, EU, Japan, urban APAC | Medium term (2-4 years) |

| Small recruitable pool | -1.8% | North America, EU5, Japan, Australia | Medium term (2-4 years) |

| Clinical failure risk | -2.4% | Global innovation hubs | Short term (≤ 2 years) |

| High therapy cost base | -1.7% | US, EU, Japan | Long term (≥ 4 years) |

| Reimbursement friction | -1.5% | US core, EU payer markets | Medium term (2-4 years) |

| Caregiver and safety burden | -1.2% | Global, strongest in aging health systems | Short term (≤ 2 years) |

Regional Analysis

In 2025, North America dominated the Frontotemporal Disorders (FTD) Treatment Market, accounting for over 41.2% share and generating revenue of US$ 167.29 million. The region’s leadership is supported by advanced healthcare infrastructure, high awareness of neurodegenerative disorders, and strong adoption of pharmacological and supportive therapies.

Early diagnosis rates are higher due to better access to neurologists, cognitive assessment tools, and imaging technologies, while sustained investment in neuroscience research and clinical trials continues to expand treatment availability.

Europe represents the second-largest regional market, driven by an aging population and well-established public healthcare systems. Countries across Western Europe show growing emphasis on early intervention, multidisciplinary care models, and reimbursement support for dementia-related treatments, which collectively contribute to steady market expansion.

The Asia Pacific market is expected to witness the fastest growth over the forecast period. Rising healthcare expenditure, improving diagnostic capabilities, and increasing awareness of frontotemporal disorders in populous countries such as China, Japan, and India are key growth drivers, although underdiagnosis remains a challenge.

Meanwhile, Latin America and the Middle East & Africa hold comparatively smaller shares. Growth in these regions is supported by gradual improvements in healthcare access, increasing neurological disease burden, and expanding physician education initiatives, though limited specialist availability continues to restrain market penetration.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

The global Frontotemporal Disorders (FTD) treatment market remains moderately fragmented and is transitioning from a predominantly symptomatic-care landscape toward an early-to-mid stage of disease-modifying therapy development.

Competitive advantage is defined less by commercial scale and more by neuroscience specialization, depth of clinical research, biomarker alignment, and the ability to translate complex neurobiology into targeted therapeutic strategies. Competitive dynamics are shaped by high unmet need, limited approved options, and long development timelines, driving both innovation intensity and partnership-led progress.

The market can be broadly structured into three tiers. Large multinational pharmaceutical companies focus on late-stage clinical development, global trial execution, and lifecycle management of neuropsychiatric and neurodegenerative portfolios.

Mid-sized specialty pharma and generics players emphasize symptomatic management and treatment accessibility. Innovation-led biotechnology firms concentrate on precision approaches such as antisense oligonucleotides, epigenetic modulation, neuroinflammation targeting, and genetically defined FTD subtypes.

At the competitive core, established companies including Teva Pharmaceutical Industries Ltd., Pfizer Inc., AstraZeneca PLC, Viatris Inc., Sanofi S.A., Eli Lilly And Company, F. Hoffmann-La Roche Ltd., Novartis AG, and Takeda Pharmaceutical Co. Ltd. leverage extensive R&D infrastructure, CNS expertise, and global regulatory capabilities.

Specialty and generics manufacturers such as Apotex Inc. and Aurobindo Pharma Ltd. support market penetration through cost-effective symptomatic therapies. Innovation-driven biopharma players including Lundbeck A/S, Biogen Inc., Ionis Pharmaceuticals, Inc., Alector, Inc., Denali Therapeutics Inc., Oryzon Genomics S.A., Athira Pharma, Inc., and Prilenia Therapeutics B.V. differentiate through focused pipelines, strategic collaborations, and ecosystem-based competition centered on precision medicine and workflow-integrated clinical development.

Top Key Players

- Teva Pharmaceutical Industries Ltd.

- Pfizer Inc

- AstraZeneca PLC

- Viatris Inc.

- Sanofi S.A.

- Apotex Inc.

- Aurobindo Pharma Ltd.

- Lundbeck A/S

- Biogen Inc.

- Ionis Pharmaceuticals, Inc.

- Alector, Inc.

- Denali Therapeutics Inc.

- Eli Lilly And Company

- F. Hoffmann-La Roche Ltd.

- Novartis AG

- Takeda Pharmaceutical Co. Ltd.

- Oryzon Genomics S.A.

- Athira Pharma, Inc.

- Prilenia Therapeutics B.V.

Recent Developments

- In 2025–2026, Prilenia advanced pridopidine programs in neurodegenerative disorders including ALS and Huntington’s disease, targeting sigma-1 receptor pathways relevant to FTD neurobiology.

Its mechanism overlaps with motor and cognitive dysfunction pathways seen in FTD. - In 2025, AstraZeneca expanded neurology collaborations through antisense and rare disease partnerships, including continued advancement of CNS-targeting genetic therapy programs via Ionis collaboration ecosystem.

While not FTD-specific, AstraZeneca’s 2025 pipeline activity includes CNS-targeted RNA therapeutics supporting broader neurodegenerative disease mechanisms relevant to FTD.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 406.0 Billion |

| Forecast Revenue (2035) | US$ 638.9 Billion |

| CAGR (2026-2035) | 4.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Treatment Type(Pharmacological Therapy ,Antidepressants ,Selective Serotonin Reuptake Inhibitors (SSRIs),Tricyclic Antidepressants (TCAs) ,Others ,Antipsychotics ,Cognitive Enhancers ,Mood Stabilizers,Anxiolytics ,Others ,Non-Pharmacological Therapy ,Speech & Language Therapy ,Occupational Therapy ,Physical Therapy ,Behavioral Therapy ,Cognitive Rehabilitation ,Others) By Disorder Type (Behavioral Variant Frontotemporal Dementia (bvFTD) ,Primary Progressive Aphasia (PPA) ,Nonfluent/Agrammatic Variant PPA ,Semantic Variant PPA ,Logopenic Variant PPA ,Frontotemporal Dementia with Motor Neuron Disease (FTD-MND) ,Others) By Route of Administration (Oral ,Injectable ,Others ) By Distribution Channel (Hospital Pharmacies ,Retail Pharmacies ,Online Pharmacies) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Teva Pharmaceutical Industries Ltd. ,Pfizer Inc. ,AstraZeneca PLC ,Viatris Inc. ,Sanofi S.A. ,Apotex Inc. Aurobindo Pharma Ltd. ,Lundbeck A/S ,Biogen Inc. ,Ionis Pharmaceuticals, Inc. ,Alector, Inc. ,Denali Therapeutics Inc. ,Eli Lilly And Company ,F. Hoffmann-La Roche Ltd. ,Novartis AG ,Takeda Pharmaceutical Co. Ltd. ,Oryzon Genomics S.A. ,Athira Pharma, Inc. ,Prilenia Therapeutics B.V. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |