Quick Navigation

Report Overview

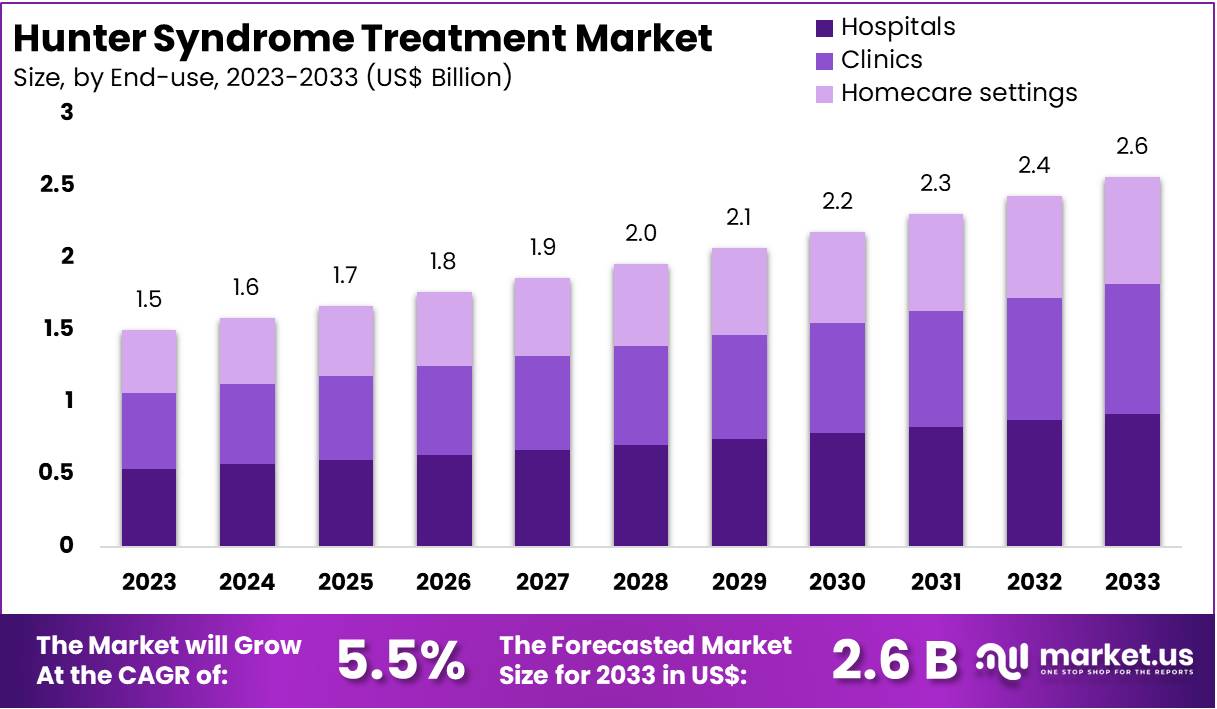

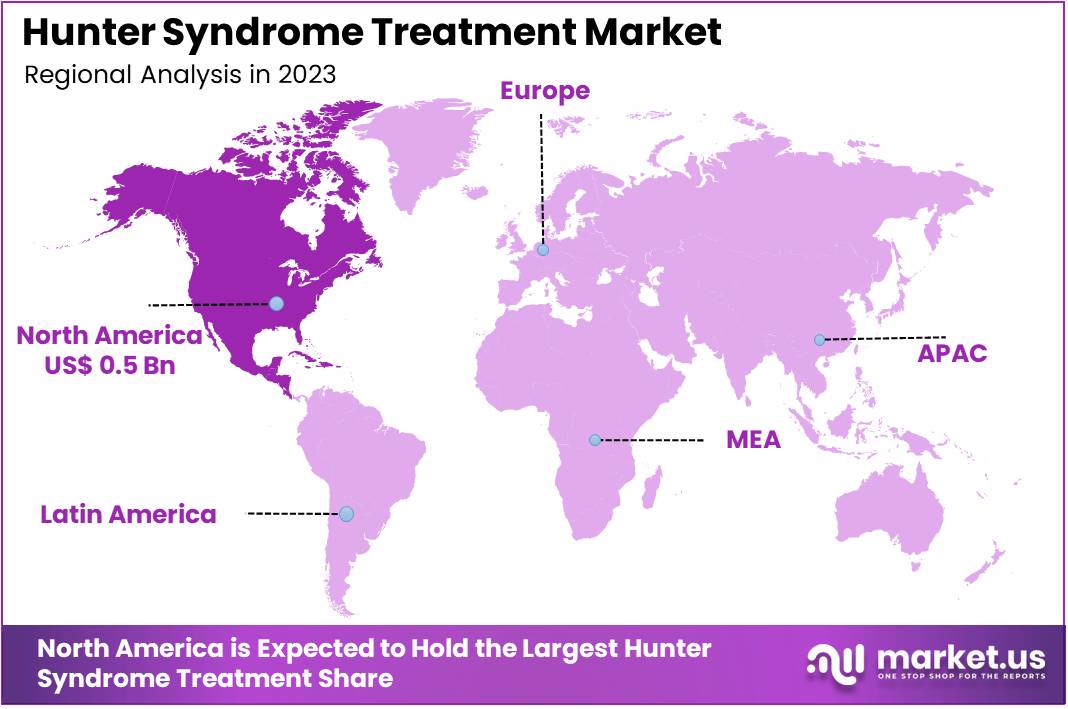

The Global Hunter Syndrome Treatment Market size is expected to be worth around US$ 2.6 Billion by 2033, from US$ 1.5 Billion in 2023, growing at a CAGR of 5.5% during the forecast period from 2024 to 2033. North America maintained a leading position in the market, accounting for over 38% of the share, with a market value of approximately US$ 0.5 billion.

Hunter syndrome, also known as Mucopolysaccharidosis Type II (MPS II), is a rare genetic disorder caused by a deficiency in the enzyme iduronate-2-sulfatase. This enzyme is vital for breaking down complex molecules in the body. Without it, these molecules build up, leading to symptoms like skeletal abnormalities, joint stiffness, respiratory issues, and cognitive decline. The condition primarily affects males, with over 600 mutations of the IDS gene identified. These mutations lead to varying disease severities, categorized into severe and attenuated phenotypes.

Enzyme Replacement Therapy (ERT) is the primary treatment for Hunter syndrome. ERT involves administering synthetic iduronate-2-sulfatase to help reduce cellular waste accumulation and manage symptoms. For instance, Shire’s Elaprase, the only FDA-approved enzyme replacement therapy for Hunter syndrome, achieved sales of $55.1 million in the third quarter of 2023. Additionally, Hematopoietic Stem Cell Transplantation (HSCT) is sometimes used to introduce cells that can produce the missing enzyme, though it comes with significant risks.

Gene therapy is an emerging treatment option, showing promise as a potential long-term solution for Hunter syndrome. According to recent studies, researchers are working to introduce a correct copy of the IDS gene, which could lead to natural enzyme production. This development holds promise, especially with advancements in genetic research. As a result, the market for Hunter syndrome treatments is expected to grow in the coming years, driven by progress in both enzyme replacement and gene therapies.

The Hunter syndrome treatment market is niche, primarily due to the rarity of the disease. According to market analysts, this rarity increases treatment costs due to the specialized nature of drug production. Furthermore, significant investments in research and development (R&D) are crucial to improving treatment efficacy and reducing side effects. Regulatory incentives, such as orphan drug designations, also play a key role in making new treatments more accessible by ensuring market exclusivity.

Global demand for Hunter syndrome treatments is growing, especially in emerging markets. For example, Green Cross Corp and JCR Pharmaceuticals partnered in March 2024 to market JR-141 (pabinafusp alfa), a therapy targeting neuronopathic features of Hunter syndrome. This therapy, administered intravenously, highlights the growing interest in developing effective treatments for this rare condition. As more collaborations and research funding emerge, access to Hunter syndrome therapies is likely to expand, further driving market growth.

Key Takeaways

- The global Hunter Syndrome Treatment Market is projected to reach approximately US$ 2.6 billion by 2033, up from US$ 1.5 billion in 2023.

- The market is expected to grow at a compound annual growth rate (CAGR) of 5.5% from 2024 to 2033.

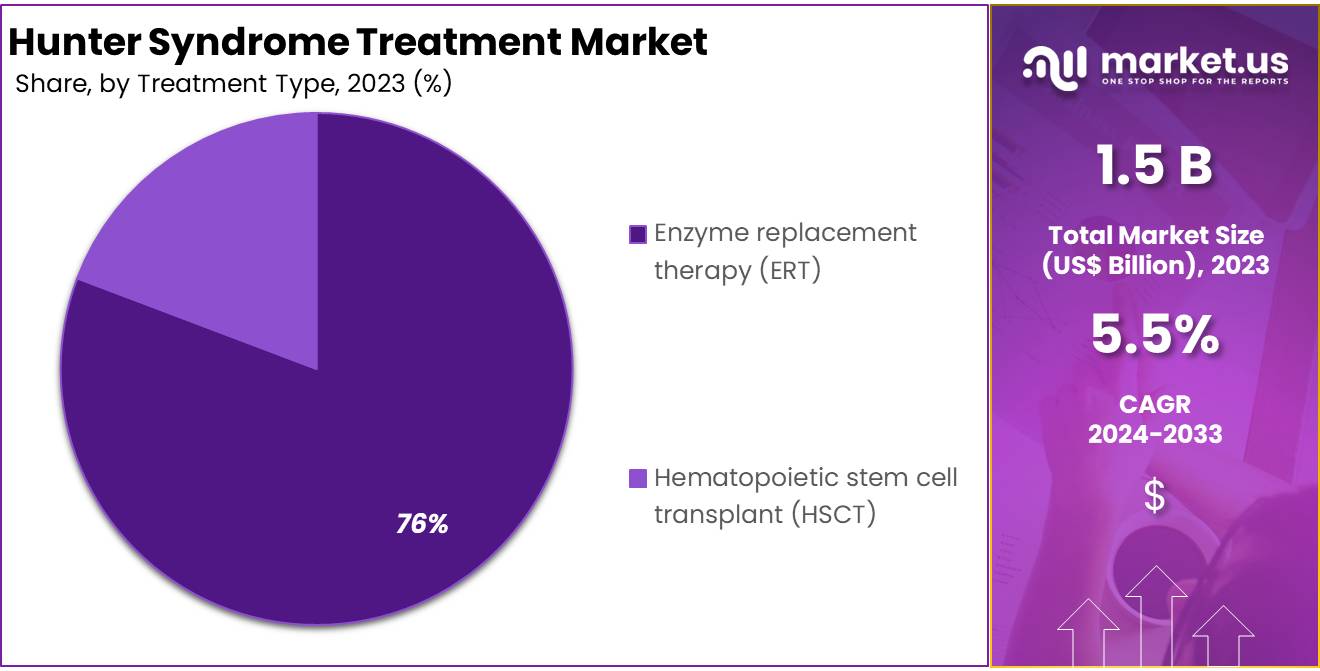

- In 2023, Enzyme Replacement Therapy (ERT) dominated the Treatment Type segment, accounting for over 76% of the market share.

- The Hospitals segment led the End-Use segment in 2023, holding more than 76% of the market share in Hunter Syndrome Treatment.

- North America was the leading region in 2023, commanding over 38% of the global Hunter Syndrome Treatment Market.

Treatment Type Analysis

In 2023, the Enzyme Replacement Therapy (ERT) segment held a dominant market position in the Treatment Type segment of the Hunter Syndrome Treatment Market, capturing more than a 76% share. This approach is vital for managing symptoms of Hunter Syndrome, an inherited genetic disorder. It involves administering synthetic enzymes to replace deficient or malfunctioning ones in patients.

The dominance of the ERT segment underscores its effectiveness and acceptance in standard treatment protocols. By directly addressing enzyme deficiencies, ERT helps alleviate many symptoms of the disease. Its widespread use reflects the trust healthcare providers place in this treatment, marking it as a primary therapeutic option.

While smaller in market share, the Hematopoietic Stem Cell Transplant (HSCT) segment is crucial. It offers a potential cure by rebuilding enzyme-producing cells, particularly in severe cases of Hunter Syndrome or those not responsive to ERT. This treatment is vital for patients needing alternative options.

Despite its smaller size, the importance of the HSCT segment is significant. With advancements in transplant methods and patient care, HSCT’s role in treating Hunter Syndrome is expected to grow. It provides a critical lifeline for patients with severe conditions, highlighting its potential in the broader treatment landscape.

End-use Analysis

In 2023, the hospitals segment held a dominant market position in the end-use segment of the Hunter Syndrome Treatment market, capturing more than a 76% share. Hospitals are pivotal in managing this complex genetic disorder. They offer comprehensive care, essential for diagnosis, treatment, and ongoing management of patients with Hunter Syndrome.

Hospitals are equipped with specialized healthcare professionals and advanced technology. These facilities are crucial for administering and monitoring enzyme replacement therapies and other treatments. Their extensive capabilities make them indispensable in the treatment framework for Hunter Syndrome.

Clinics also contribute to the treatment landscape, albeit on a smaller scale. They are often the first point of contact for diagnosis. Some clinics also administer treatments. However, their share in the market is smaller, reflecting the intensive healthcare services required by Hunter Syndrome patients that clinics typically cannot provide.

Homecare settings are gaining traction as an alternative for ongoing management and care. Advances in home healthcare services and equipment have made at-home treatment more viable. Despite this growth, homecare remains the smallest segment. Most critical treatments still necessitate the facilities and expertise found in hospitals.

Key Market Segments

By Treatment Type

- Enzyme replacement therapy (ERT)

- Hematopoietic stem cell transplant (HSCT)

By End-use

- Hospitals

- Clinics

- Homecare settings

Drivers

Rising Prevalence of Hunter Syndrome

The increasing prevalence of Hunter Syndrome is a key factor driving the treatment market. The disease is diagnosed in approximately 1 out of every 100,000 to 170,000 children globally. Prevalence varies across regions, such as 1 case per 140,000-330,000 live births in Germany and the Netherlands and 1 case per 132,000 children in the UK. According to recent studies, the rise in diagnosis rates is attributed to the inclusion of newborn screening programs for lysosomal storage disorders, allowing earlier detection and treatment.

The growing awareness of Hunter Syndrome and advancements in healthcare infrastructure have fueled demand for specialized treatments. According to studies, FDA-approved enzyme replacement therapies are widely used, and many clinical trials are underway to develop new treatments. For example, ongoing research focuses on improving both life expectancy and the quality of life for patients. These developments cater to the increasing treatment demand and are pivotal in shaping the future of the Hunter Syndrome Treatment Market.

The active pipeline of treatments for Hunter Syndrome highlights significant market potential. According to sources, research into enzyme replacement therapies and other innovative approaches aims to meet the rising need for effective solutions. For instance, early intervention enabled by genetic testing and newborn screenings has played a critical role in the rising diagnosis rates. This trend, combined with the global impact of the disease, underscores the importance of continued investment and innovation in Hunter Syndrome treatments to address this growing market demand.

Restraints

High Cost of Treatment

The high cost of treatment serves as a major restraint in the Hunter Syndrome treatment market. Therapies like enzyme replacement therapy (ERT) and gene therapy are essential for managing this rare disorder. However, their production involves complex processes and significant research investments. These factors make the therapies expensive. Furthermore, the rarity of Hunter Syndrome limits economies of scale. This drives up the overall cost per patient. Such high expenses create financial barriers for patients and their families seeking effective treatments.

Financial challenges extend beyond treatment costs. Diagnostic evaluations, ongoing care, and long-term follow-ups further add to the economic burden. These additional expenses often become overwhelming for families. Moreover, limited insurance coverage and reimbursement options compound the problem. Many patients face difficulties in securing financial support for their treatment. This issue is particularly severe in regions with underdeveloped healthcare systems. These constraints make advanced therapies inaccessible for a significant portion of the affected population.

High treatment costs also affect healthcare systems worldwide. Developing countries face significant challenges due to budget constraints. Even in developed regions, high costs can strain healthcare funding. Limited access to affordable treatments negatively impacts adoption rates of advanced therapies. As a result, market growth remains constrained. Addressing these economic barriers is essential to expanding access. Reducing treatment costs and improving reimbursement frameworks could significantly enhance the market’s potential. Without such measures, the adoption of innovative therapies will remain limited.

Opportunities

Advancements in Gene Therapy

Advancements in gene therapy represent a transformative opportunity for the Hunter Syndrome treatment market. As research progresses and clinical trials expand, gene therapy has shown immense potential to address the underlying genetic cause of the disorder, rather than merely managing symptoms. This innovative approach offers the possibility of curative outcomes, dramatically improving patient quality of life and reducing the long-term burden of treatment.

For market players, these advancements open avenues for the development of groundbreaking therapies tailored to this rare disease. Gene therapy not only provides hope for effective, long-lasting treatments but also positions companies at the forefront of a cutting-edge medical revolution, enhancing their competitive edge and reputation in the field of rare disease management. Additionally, the growing interest and investment in precision medicine further solidify the market’s potential for sustained growth and innovation. The global gene therapy market size is expected to be worth around USD 49.3 Bn by 2032 from USD 5.6 Bn in 2022, growing at a CAGR of 25% during the forecast period from 2022 to 2032.

Trends

Focus on Personalized Medicine

The focus on personalized medicine is rapidly growing in the Hunter Syndrome treatment market. This approach tailors treatments to individual patients based on their genetic makeup and unique biomarkers. By personalizing therapies, treatments can more effectively address the root causes of the disease. This helps avoid the generalized, one-size-fits-all methods and leads to more targeted care. Precision medicine has the potential to improve patient outcomes significantly, making it a crucial trend in the treatment of Hunter Syndrome.

Genetic profiling and biomarker analysis are central to personalized medicine for Hunter Syndrome. These technologies help identify specific genetic variations and molecular markers in patients. By doing so, doctors can develop treatment plans tailored to the patient’s specific needs. This not only improves the effectiveness of treatments but also allows for earlier detection and more accurate diagnoses. Early intervention is key in managing Hunter Syndrome and ensuring better long-term health outcomes for patients.

The use of biomarkers also plays a significant role in monitoring disease progression. Through regular tracking of these markers, healthcare providers can assess how well treatments are working. This leads to more precise adjustments in treatment plans. As personalized medicine continues to grow, it will enhance how Hunter Syndrome is managed, providing better care for patients. This approach promises to improve both the efficiency of treatments and the overall quality of care in the market. According to Market.us The Global Predictive & Personalized Medicine Market size is expected to be worth around USD 692.0 Billion by 2032 from USD 347.2 Billion in 2023, growing at a CAGR of 8.2% during the forecast period from 2024 to 2032.

Regional Analysis

In 2023, North America held a dominant market position in the Hunter Syndrome Treatment Market, capturing more than a 38% share. The region’s market value reached US$ 0.5 billion for the year. This leadership is primarily due to high rates of diagnosis and treatment. Enhanced healthcare infrastructure and heightened awareness about genetic disorders promote early detection and intervention, driving demand for effective treatments.

The region benefits from the presence of leading pharmaceutical companies. These entities invest heavily in research and development, innovating new treatments that cater specifically to the complexities of Hunter Syndrome. Their efforts ensure a steady supply of advanced therapeutic options available within the market, thereby supporting robust growth.

Additionally, supportive government initiatives play a critical role. Financial backing and favorable policies from governmental bodies improve access to vital treatments. Subsidies for rare diseases and targeted health programs significantly enhance patient care and treatment accessibility, bolstering the market’s expansion.

Collaborations between research institutions and healthcare providers further strengthen the treatment landscape. These partnerships facilitate the advancement and widespread adoption of new therapies. Through combined efforts, North America continues to lead in setting high standards for treatment efficacy and patient care in the Hunter Syndrome Treatment Market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Denali Therapeutics and ArmaGen are significant players in the Hunter Syndrome treatment market. Denali Therapeutics focuses on innovative therapies targeting the genetic root of the disorder. Their pipeline includes gene and enzyme replacement therapies aimed at improving treatment delivery and outcomes. ArmaGen specializes in addressing neurological symptoms through enzyme therapies that cross the blood-brain barrier. This focus on neurological complications sets them apart. Their expertise in developing advanced delivery systems positions both companies as leaders in advancing Hunter Syndrome treatment options.

Inventiva and Green Cross Corp. also contribute significantly to the Hunter Syndrome treatment market. Inventiva focuses on small molecule drugs that modify disease processes, offering potential alternatives to traditional therapies. Their research broadens treatment options and aims for accessibility. Green Cross Corp. specializes in enzyme replacement therapies with a strong presence in rare disease treatment. Based in South Korea, their global reach ensures reliable patient access. Both companies drive innovation and diversity in treatment approaches.

Other key players in the Hunter Syndrome treatment market are investing in research and development to expand treatment possibilities. Their work includes improving current therapies and exploring new approaches. These advancements are shaping a competitive market landscape and creating better solutions for patients. Collectively, these companies aim to enhance patient care and address unmet needs in the market. Their efforts contribute to the steady growth and innovation within the Hunter Syndrome treatment space. This collaborative progress is improving the quality of life for affected individuals.

Market Key Players

- Shire

- Denali Therapeutics

- ArmaGen

- Inventiva

- Green Cross Corp.

- CANbridge Life Sciences Ltd.

- JCR Pharmaceuticals Co. Ltd.

- REGENXBIO Inc.

- Sangamo Therapeutics

- Terumo Corporation

- Thermo Fisher Scientific

Industrial Advantages and Opportunities For Market Players

Hunter syndrome treatment offers significant revenue potential due to the specialized and costly nature of therapies required for this rare disorder. Establishing long-term customer relationships is feasible, given the chronic treatment regimen, which boosts revenue sustainability for companies. Additionally, developing effective treatments enhances a company’s reputation within the medical and biotech communities, positioning them as leaders in pharmaceutical innovation.

The industry benefits from regulatory incentives like tax credits and fee waivers that reduce the financial strain of R&D in rare diseases. The complexity of Hunter syndrome fosters advanced biotechnological advancements and collaborative research efforts. These collaborations often involve leading biotech firms, academic institutions, and healthcare providers, driving forward innovation and understanding of rare genetic conditions.

The Hunter syndrome treatment market holds opportunities for expansion through the development of new treatment modalities, such as advanced biologics and small molecule therapies. These innovations can offer improved efficacy and patient convenience. There is also potential for geographic expansion into emerging markets, where awareness and diagnostic capabilities are increasing, opening new avenues for revenue.

Strategic partnerships with global health entities and governments can facilitate the faster development and distribution of new therapies. By investing in patient support services, companies not only enhance treatment compliance and outcomes but also strengthen patient trust and satisfaction, creating distinct competitive advantages in the healthcare sector.

Recent Developments

- In July 2023: Shire entered into a collaboration with ArmaGen to develop AGT-182, an investigational enzyme replacement therapy for Hunter syndrome. This agreement grants Shire worldwide commercialization rights. ArmaGen will receive up to approximately $225 million, which includes an initial upfront payment of $15 million, additional equity, R&D funding, and potential future royalties. This collaboration is a strategic move to enhance treatment options that address both central nervous system and somatic symptoms of Hunter syndrome.

- In July 2023: ArmaGen progressed in its clinical trials by presenting data from the first cohort of adult patients enrolled in the Phase 1/2a Breaking Barriers clinical trial of AGT-182. This investigational enzyme replacement therapy (ERT) is designed for Hunter syndrome, specifically targeting the central nervous system by utilizing the body’s natural system for transporting substances across the blood-brain barrier. The trial is significant as AGT-182 is unique among potential treatments for its ability to reach the brain. The first cohort involved four patients who received a weekly 1.0-mg/kg dose of AGT-182 intravenously, which was generally well-tolerated, encouraging the continuation to a second cohort with an increased dose.

- In March 2023: Denali Therapeutics advanced its investigational therapy, DNL310, for Hunter Syndrome, demonstrating significant improvements in key biomarkers heparan sulfate and dermatan sulfate. This therapy, which crosses the blood-brain barrier, showed a reduction of these biomarkers by 85% and 89%, respectively, suggesting enhanced peripheral activity over traditional therapies. DNL310 has maintained a consistent safety profile over two years of treatment, with a decrease in the frequency and severity of infusion-related reactions over time.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 1.5 Billion |

| Forecast Revenue (2033) | US$ 2.6 Billion |

| CAGR (2024-2033) | 5.5% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Treatment Type (Enzyme replacement therapy (ERT), Hematopoietic stem cell transplant (HSCT)), By End-use (Hospitals, Clinics, Homecare settings) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Shire, Denali Therapeutics, ArmaGen, Inventiva, Green Cross Corp., CANbridge Life Sciences Ltd., JCR Pharmaceuticals Co. Ltd., REGENXBIO Inc., Sangamo Therapeutics, Terumo Corporation, Thermo Fisher Scientific |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |