Quick Navigation

- Report Overview

- Key Takeaways

- Type Analysis

- Application Analysis

- End-Use Analysis

- Construction Analysis

- Distribution Channel Analysis

- Key Market Segments

- Driver Analysis

- Restraint Analysis

- Opportunity Analysis

- Challenges Analysis

- Geopolitical Impact Analysis

- Regional Analysis

- Key Players Analysis

- Key Development

- Report Scope

Report Overview

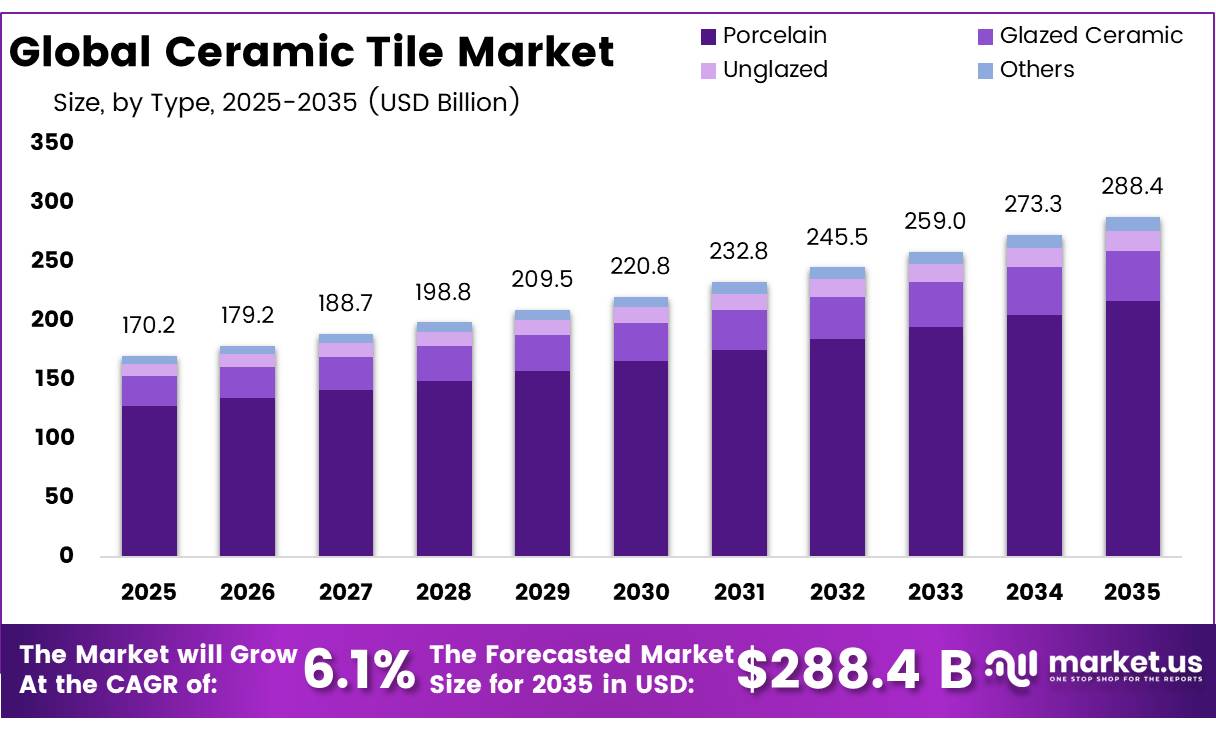

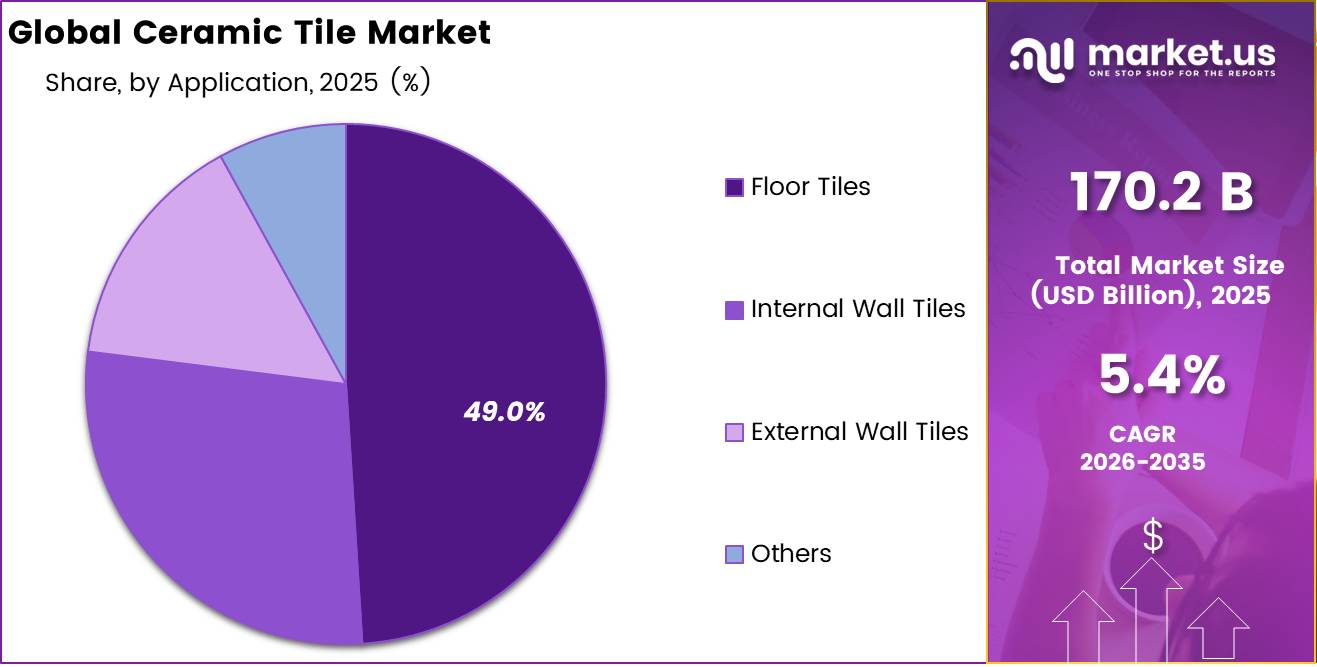

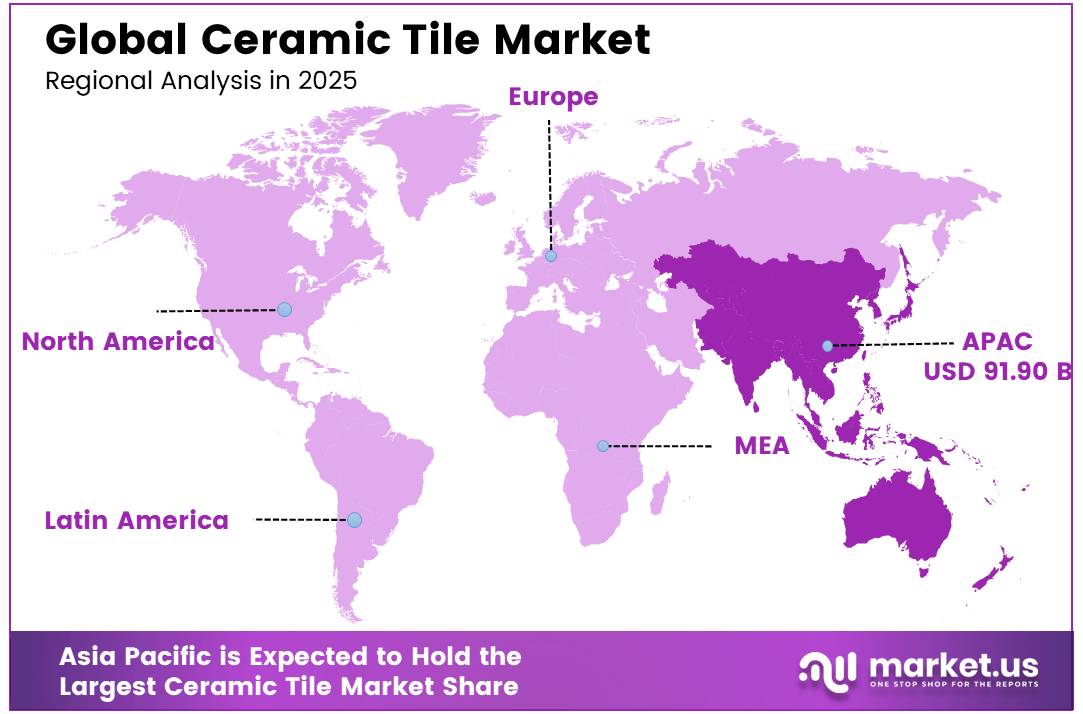

In 2025, the global Ceramic Tile Market was valued at USD 170.2 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 5.4%, reaching about USD 288.4 billion by 2035. In 2025, Asia Pacific led the market, achieving over 54% share with a revenue of USD 91.90 Billion.

Ceramic tiles are manufactured from processed clay, feldspar, and silica that are shaped, glazed, and fired at high temperatures to produce durable surfacing material used in residential flooring, wall cladding, and commercial architectural finishes. The industry falls under the broader non-metallic mineral products sector and relies on a steady upstream supply of mined raw materials alongside cyclical construction demand.

- In February 2026, according to the U.S. Geological Survey, feldspar, a primary flux material in ceramic tile bodies, saw domestic production of 440,000 tons valued at $49 million in 2025, with ceramics, pottery, and related applications accounting for 53% of total domestic feldspar end-use. Separately, the European Commission reports that the broader EU ceramics sector, which includes tile manufacturing, sustains over 338 thousand jobs and generates €27.8 billion in annual production value, with small and medium enterprises forming the bulk of manufacturers.

Key Takeaways

- The global ceramic tile market was valued at USD 170.2 billion in 2025.

- The global market is projected to grow at a CAGR of 5.4% during the forecast period from 2025 to 2035.

- Porcelain tiles dominated the market, accounting for 75.2% of the total market share.

- Floor tiles led the ceramic tile market, contributing around 49.0% of the overall market share.

- Residential segment dominated the market, holding 73.9% of the total market share.

- New construction accounted for the largest share of the ceramic tile market, representing approximately 58.0% of total demand.

- Large home centers dominated the market, contributing nearly 40.0% of the overall market share.

- In 2025, Asia Pacific was the dominant regional market, accounting for 54.0% of the global ceramic tile market share.

Construction and renovation activity remains the principal demand driver, supported by feldspar’s role as a low-cost, geologically abundant flux. Future growth opportunities lie in energy-efficient kiln technologies and recycled-content formulations, as environmental compliance frameworks such as the European Green Deal push manufacturers toward lower-emission, resource-efficient production methods across major producing regions.

Type Analysis

The Porcelain segment dominates the ceramic tile market due to its superior strength and performance.

In 2025, the porcelain tiles segment dominated the global ceramic tile market with a 75.2% share, driven by its high durability, low water absorption, wear resistance, and strong suitability for premium residential and commercial applications. The increasing demand for large-format and full-body porcelain tiles that replicate the appearance of natural stone and wood has further strengthened the segment’s market leadership.

Glazed ceramic tiles held the second-largest market share due to their decorative appeal, wide variety of colors and textures, and cost-effectiveness. These tiles are widely used in mid-range residential projects, particularly across developing economies where affordability and aesthetic design remain important purchasing factors.

Unglazed and specialty tiles continue to witness demand in niche applications where slip resistance, natural appearance, and customized designs are preferred. Specialty variants such as encaustic, terracotta, and cement-look tiles are increasingly being used in luxury interiors and high-end architectural projects.

Application Analysis

Floor Tiles Dominated the Ceramic Tile Market.

Floor tiles account for 49.0% of the global ceramic tile market. This dominance is because people require floor tiles that are durable, easy to clean, and attractive in homes, companies, hotels, and schools. Floor tiles are popular due to their versatility. People’s preference for porcelain floor tiles has increased their popularity. Porcelain is hard, doesn’t absorb water, and comes in a variety of designs. Large porcelain floor tiles are particularly popular in construction in a variety of designs. Large porcelain floor tiles are particularly popular in construction projects.

External wall tiles account for a smaller share of the market. They are becoming increasingly popular. Large porcelain panels are frequently used on the exteriors of buildings to make old structures look new and to create distinctive walls in workplaces and apartments.

End-Use Analysis

Residential Held a Major Share of the market

The residential segment dominated the global ceramic tile market, accounting for 73.9% of total consumption, driven by rapid urbanization, rising residential construction activities, increasing home renovation projects, and growing consumer preference for aesthetically appealing and durable flooring and wall solutions. Ceramic and porcelain tiles continue to witness strong demand in residential applications due to their durability, moisture resistance, low maintenance requirements, and wide variety of designs, textures, and finishes.

Rising disposable incomes and improving living standards, particularly across emerging economies in Asia Pacific and Latin America, are further encouraging consumers to adopt premium and large-format porcelain tiles, wood-look surfaces, and designer tile collections for modern housing projects. Additionally, increasing government investments in affordable housing and expanding apartment construction activities are further strengthening demand for ceramic tiles across kitchens, bathrooms, living spaces, and outdoor residential areas globally.

The other type is non-residential, which includes offices, retail, hotels, hospitals, and public buildings. Even though this category is smaller, the tiles used are typically more expensive per meter. This is because hotels and hospitals frequently use advanced ceramics and special design solutions that are more expensive. Ceramic tiles are utilized in these places because they are long-lasting and easy to clean, which is essential for construction and non-residential structures such as hotels and hospitals.

Construction Analysis

Ceramic Tiles Are Mostly Utilized in the New Construction

The new construction segment dominated the global ceramic tile market, accounting for around 58.0% of the total market share, driven by rapid urbanization, expanding residential and commercial construction activities, and large-scale infrastructure development projects worldwide. Strong demand for ceramic tiles in newly constructed housing complexes, office buildings, shopping malls, hotels, airports, and public infrastructure continues to support segment growth across both developed and emerging economies.

In addition, rising government investments in smart cities, affordable housing schemes, and urban infrastructure development, particularly across Asia Pacific and the Middle East, are significantly contributing to the expansion of the new construction segment globally.

Ceramic tiles are popular in homes, offices, hotels, and commercial structures because they are long-lasting, visually appealing, and easy to maintain. They are an option for builders and architects. New construction projects increase demand for tiles.

Meanwhile, the renovation category is expanding steadily, aided by increased home re-modelling activity, rising disposable incomes, and rising consumer demand for modern interior aesthetics and luxury flooring solutions. Homeowners and commercial property owners are increasingly replacing old flooring and wall materials with beautiful, long-lasting, and low-maintenance ceramic tiles to increase visual appeal and value.

Distribution Channel Analysis

Large Home Centers Are the Most Widely Used Distribution Channel

Large Home centers dominated the global ceramic tile distribution market, accounting for nearly 40% of the total market share, driven by their wide product availability, competitive pricing, and strong consumer accessibility. These retail formats offer a broad range of ceramic and porcelain tiles across different price categories, making them highly preferred by homeowners, contractors, and renovation professionals for both new construction and remodeling projects. Major home improvement retailers such as Home Depot, Lowe’s, Leroy Merlin, and Hornbach continue to strengthen market growth through extensive product portfolios, promotional pricing, and in-store design assistance.

Specialty tile stores also maintain a significant presence in the market by offering premium collections, customized designs, and expert consultation services for luxury residential and commercial projects. Meanwhile, online distribution channels are witnessing rapid growth due to increasing consumer preference for digital product browsing, virtual room visualization tools, and convenient home delivery services, making tile purchasing more accessible and efficient globally.

Key Market Segments

By Type

- Porcelain

- Glazed Ceramic

- Unglazed

- Others

By Application

- Floor Tiles

- Internal Wall Tiles

- External Wall Tiles

- Others

By End-Use

- Residential

- Non-Residential

By Construction Type

- New Construction

- Renovation

By Distribution Channel

- Large Home Centers

- Independent Retailers

- Online Retail

- Others

Driver Analysis

Renovation-led replacement demand

Ceramic tile demand in 2026 is being supported by the renovation cycle more than by broad-based new-build acceleration, especially in Europe where construction activity is moving back into growth after contraction and stagnation in 2024–2025. That matters because renovation consumes higher-value wall and floor finishes per square meter than many shell-and-core new-build packages, particularly in kitchens, bathrooms, facades, and high-traffic retrofit zones; the revenue effect is therefore larger than the pure volume effect.

In the EU, policy pressure around building stock modernization remains structurally relevant, while the broader climate agenda continues to target a 55% emissions reduction by 2030 versus 1990 levels, reinforcing envelope and interior upgrade spending that indirectly benefits tile replacement cycles.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation-led replacement demand | +1.3% | EU core, North America core, GCC urban centers | Short term (≤ 2 years) |

| Porcelain and large-format mix upgrade | +1.1% | Europe, North America, China premium tier, India exports | Medium term (2-4 years) |

| Building-efficiency and low-carbon compliance | +0.9% | EU core, UK, developed APAC, premium urban projects globally | Medium term (2-4 years) |

| U.S. housing normalization and remodel recovery | +0.8% | United States core, Mexico supply chain, Canada spill-over | Short term (≤ 2 years) |

| India export competitiveness and trade rerouting | +0.7% | India, U.S., Middle East, Africa, EU import channels | Medium term (2-4 years) |

| Fuel-cost volatility and capacity rationalization | +0.6% | India Morbi cluster, Southern Europe, MENA manufacturing belts | Short term (≤ 2 years) |

Restraint Analysis

Competition from alternate floorings

Competitive pressure from alternative flooring and surface materials—such as LVT, engineered wood, laminates, and polished concrete—acts as a structural restraint because these categories continue to gain share in key residential and commercial segments on the back of easier installation, lower perceived maintenance, and design improvements that narrow the aesthetic gap with ceramic tiles.

A multi‑year horizon, this competitive dynamic structurally trims tile’s addressable share of floor and wall surfaces, particularly in mid‑priced residential, and can reduce long‑term CAGR by roughly 0.5–1.0 percentage points versus a scenario where tiles maintain their historical share, forcing ceramic producers to double down on niches—such as high‑traffic commercial, outdoor, and premium design—where performance and lifecycle economics still decisively favor fired surfaces.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy and gas cost volatility | -1.2% | India, China, Southern Europe, MENA kilns | Short term (≤ 2 years) |

| Weak / delayed construction cycles | -1.0% | EU, North America, some LATAM | Short–Medium term (≤ 4 years) |

| Trade actions and tariff friction | -0.8% | U.S., EU, India, China export lanes | Medium term (2–4 years) |

| Competition from alternate floorings | -0.7% | North America core, EU, developed APAC | Long term (≥ 4 years) |

| Raw material & logistics volatility | -0.6% | Global corridors, esp. Asia–EU/US | Short–Medium term (≤ 4 years) |

| Environmental & compliance burden | -0.5% | EU core, UK, North America, high-spec APAC | Long term (≥ 4 years) |

Opportunity Analysis

Smart, sensor‑enabled and heated tiles

Current smart‑home spend exceeds hundreds of billions of dollars globally, but only a very small fraction touches hard surfaces directly; diverting even 1–2% of future smart‑interior budgets into ceramic‑based platforms—such as pre‑engineered heated bathroom floors, sensor‑enriched hospitality lobbies, or inductive kitchen counters—could translate into a multi‑billion incremental TAM by the early‑to‑mid 2030s, with product bundles that carry 10–15 percentage points higher gross margin than standard tiles because electronics and controls dominate the bill of materials economics.

This is an opportunity, not a present driver, because it requires new partnerships with electronics OEMs and HVAC integrators, certification against electrical and building codes, and new service models that ceramic players have barely begun to build; those who invest in modular, safety‑certified smart tile platforms in the next four years can carve out 0.5–1.0 percentage point CAGR upside in advanced markets as sensor‑rich surfaces move from showpiece experiments into repeatable SKUs for premium residential, retail, and hospitality projects.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Circular & low-carbon tile portfolio | +1.3% | EU core, UK, North America, high-spec APAC | Medium term (2–4 years) |

| System-based facades & outdoor solutions | +1.1% | Europe, Middle East, North America urban, APAC metros | Medium term (2–4 years) |

| Smart, sensor-enabled and heated tiles | +0.9% | North America core, EU, East Asia affluent cities | Long term (≥ 4 years) |

| Direct-to-consumer and subscription remodel | +0.8% | North America, EU, India Tier-1, GCC | Short–Medium term (≤ 4 years) |

| Emerging-market urban mass premium | +1.0% | India, ASEAN, Africa urban corridors, Latin America | Long term (≥ 4 years) |

| Digital design platforms & data monetization | +0.7% | Global (specifiers, OEMs, large developers) | Medium term (2–4 years) |

Challenges Analysis

Volatile Kiln Fuel and Energy Routing

Kiln fuel and energy routing volatility is a systemic challenge rather than a one‑off restraint because even when tiles keep selling, the industry lives with recurring shocks in gas, LPG, or propane availability and price, especially where energy imports depend on geopolitically sensitive routes, as seen in 2026 when conflict‑driven disruptions in West Asia cut propane flows to India and forced temporary shutdowns in Morbi and created shortages and price spikes in Delhi‑NCR.

A typical mid‑sized plant firing 15,000–20,000 square meters per day may see energy costs fluctuate by 30–50% within a single fiscal year, moving the energy share of COGS from, say, 20% toward 30% and compressing EBITDA margins by 200–400 basis points unless prices are rapidly adjusted; yet downstream retail and project pricing often lags by 3–6 months due to tender structures and distributor contracts.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Fragmented, low-scale manufacturing base | -1.0% | India, China Tier-2 clusters, LATAM | Long term (≥ 4 years) |

| Volatile kiln fuel and energy routing | -0.9% | India, EU periphery, MENA, APAC corridors | Medium term (2–4 years) |

| Skilled installer and plant-tech gap | -0.8% | North America core, EU hubs, GCC | Long term (≥ 4 years) |

| Logistics and corridor disruption risk | -0.7% | Asia–EU, Asia–US, intra-India, intra-EU | Medium term (2–4 years) |

| ESG compliance and data complexity | -0.6% | EU regulatory hubs, UK, North America | Long term (≥ 4 years) |

| Channel digitization and demand visibility | -0.5% | Global retail, distributors, emerging D2C | Medium term (2–4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Ceramic Tile.

Washington’s 2025 tariff overhaul added a new layer of cost pressure across the tile trade. Executive Order 14257 of April 2025 set a baseline 10% reciprocal duty on imports from all countries. Separately, per a White House fact sheet dated July 31, 2025, the administration raised its IEEPA-based tariff on non-USMCA-qualifying Canadian goods from 25% to 35%, effective August 1, 2025, with a 40% rate applied to any shipments found to be transshipped to evade the increase.

A further Federal Register modification in August 2025 required that duty rates on European Union-origin goods, including Spanish and Italian tile, be raised to a 15% floor where the prior combined rate fell short. The legal basis for these measures remains contested. A Congressional Research Service report filed with the Library of Congress notes that IEEPA tariffs on global partners have ranged between 10% and 41%, and that multiple federal courts ruled the President exceeded his statutory authority, though the duties stayed collectible pending Supreme Court review.

Against this backdrop, the U.S. Census Bureau and Bureau of Economic Analysis reported the year-to-date goods and services deficit narrowed by $213.5 billion, or 49.1%, through April 2026, alongside an 11.3% rise in goods exports

Regional Analysis

Asia Pacific Held the Largest Share of the Global ceramic tile Market.

Asia-Pacific dominates the global ceramic tile market with a commanding 54% share, driven by large-scale construction, rapid urbanization, and sustained infrastructure investment. China leads as both the world’s largest producer and consumer, while India’s government-backed housing initiatives like PMAY and smart city projects are generating strong and consistent demand growth.

North America presents a stable and expanding profile driven by residential renovation and a progressive consumer shift toward porcelain tile solutions, with the United States remaining a significant net importer. Latin America is anchored by Brazil as the region’s largest producer and consumer, with Mexico and Colombia emerging as important secondary markets. The Middle East and Africa rounds out the global landscape as an emerging growth market, driven by infrastructure investment and GCC hospitality construction activity.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global ceramic tile industry is very competitive, with key competitors focusing on product innovation, premium designs, sustainability initiatives, and capacity growth to maintain their market position. To address changing customer tastes and environmental requirements, leading corporations are expanding their investments in sophisticated production technologies such as digital inkjet printing, large-format tile manufacturing, and eco-friendly production processes.

The ceramic tile market is mostly controlled by manufacturers from the Asia Pacific region those from China and India. This is because China and India have the ability to produce things at a cost and they are very good at sending their products to other countries. On the hand companies from Europe like those from Italy and Spain are very strong in the high end and luxury ceramic tile segment. They are good at making exciting designs and their products are of very high quality.

The Major Players In The Industry

- Mohawk Industries Inc.

- Grupo Lamosa

- RAK Ceramics

- Kajaria Ceramics Limited

- SCG Ceramics

- Grupo Pamesa

- Siam Cement Public Company Limited (SCG)

- Ceramica Carmelo Fior

- STN Ceramica

- Porcelanosa Grupo A.I.E.

- Crossville Inc.

- Florim Ceramiche S.P.A.

- GranitiFiandre S.p.A.

- LIXIL Group Corporation

- Dongpeng

- Newpearl

- Nitco Tiles

- China Ceramics Co., Ltd.

- Others

Key Development

- In July 2025, Florim Ceramiche S.P.A published its 17th Sustainability Statement, confirming €10 million in 2024 sustainability investment and new showrooms opened in Los Angeles and Seoul between May and June 2025.

- In Q3 2025, SCG Decor reported net profit of 305 million Baht, up 37% from the previous quarter, with EBITDA of 902 million Baht. For 9M 2025, EBITDA reached 2,513 million Baht and net profit was 744 million Baht.

- In October 2025, Mohawk Industries Inc. reported that its Global Ceramic Segment net sales rose 4.4% year-over-year, supported by productivity gains despite higher input costs across its facilities.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 170.2 Bn |

| Forecast Revenue (2035) | USD 288.4 Bn |

| CAGR (2026-2035) | 5.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Porcelain, Glazed Ceramic, Unglazed, and Others), By Application (Floor Tiles, Internal Wall Tiles, External Wall Tiles, and Others), By End-Use (Residential and Non-Residential), By Construction Type (New Construction and Renovation), By Distribution Channel (Large Home Centers, Independent Retailers, Online Retail, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Mohawk Industries Inc., Grupo Lamosa, RAK Ceramics, Kajaria Ceramics Limited, SCG Ceramics, Grupo Pamesa, Siam Cement Public Company Limited (SCG), Ceramica Carmelo Fior, STN Ceramica, Porcelanosa Grupo A.I.E., Crossville Inc., Florim Ceramiche S.P.A., GranitiFiandre S.p.A., LIXIL Group Corporation, Dongpeng, Newpearl, Nitco Tiles, China Ceramics Co., Ltd., and others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |