Quick Navigation

Report Overview

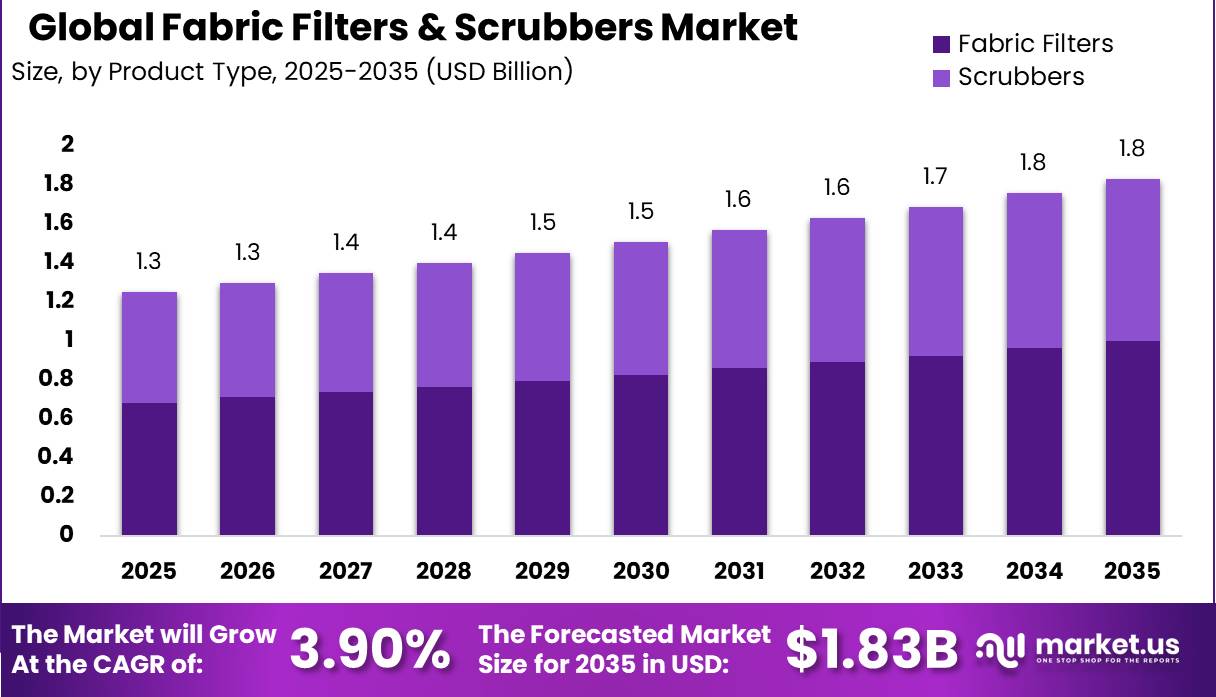

Global Fabric Filters & Scrubbers Market size is expected to be worth around USD 1.83 Billion by 2035 from USD 1.3 Billion in 2025, growing at a CAGR of 3.9% during the forecast period 2026 to 2035. This trajectory reflects sustained capital deployment in industrial air pollution control across heavy-emitting sectors worldwide.

The Fabric Filters & Scrubbers Market covers equipment and integrated systems designed to capture particulate matter, acid gases, and toxic emissions from industrial flue gas streams. The market encompasses fabric filter technologies including baghouse, cartridge, compact modular, and high-temperature configurations, alongside wet scrubbers, dry scrubbers, and hybrid multi-pollutant control trains deployed across power generation, cement, metals, chemicals, waste-to-energy, and related industries.

Key Takeaways

- The global Fabric Filters & Scrubbers Market was valued at USD 1.3 Billion in 2025 and is forecast to reach USD 1.83 Billion by 2035.

- The market is growing at a CAGR of 3.9% during the forecast period 2026 to 2035.

- By Product Type, Fabric Filters dominate with a 54.70% share due to widespread use in high-dust industrial applications.

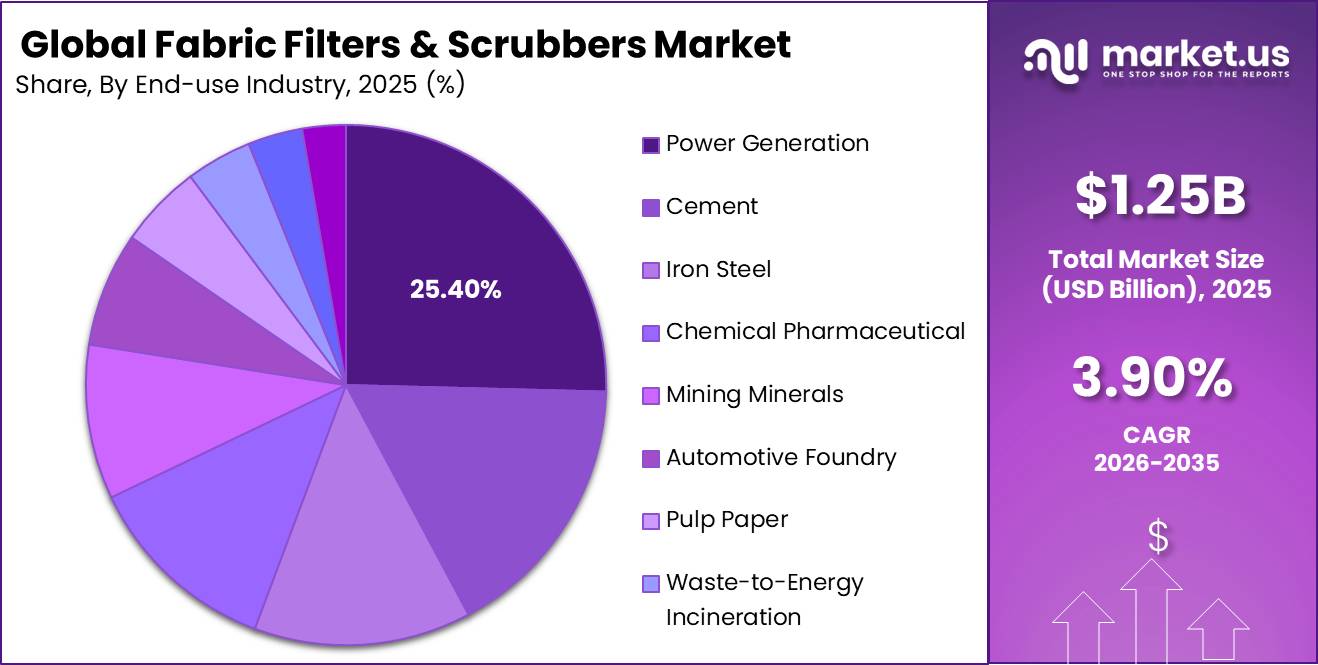

- By End Use Industry, Power Generation holds the leading position with a 25.40% share.

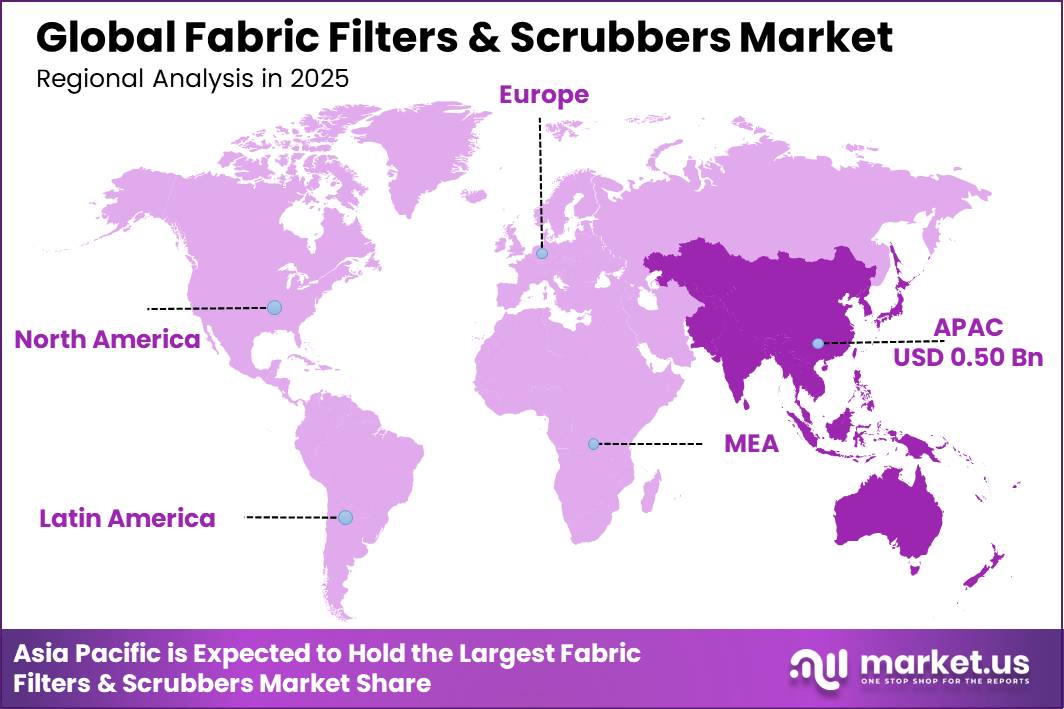

- Asia Pacific is the dominant region with a 40.10% share, valued at USD 0.5 Billion in 2025.

Regulatory frameworks in both the U.S. and Europe are raising the emissions bar across heavy industry. According to ScienceDirect, high-efficiency scrubber systems have achieved 99.7% SO₂ removal, 99.26% PM2.5 removal, and reduced stack opacity from 43.9% to below 0.64%. These performance benchmarks now define the technical floor for new procurement decisions, which compresses the position of legacy low-efficiency equipment in competitive bids.

As reported by ScienceDirect, advanced exhaust-gas scrubbers achieved more than 95% SO₂ removal efficiency across repeated operating cycles in 2025. This consistency under variable load conditions gives plant operators confidence in guaranteed compliance outcomes. This signals a procurement shift toward performance-backed scrubber systems rather than lowest-cost equipment selection.

Product Type Analysis

Fabric Filters dominate with 54.70% due to broad deployment across dust-heavy industrial processes.

In 2025, Fabric Filters held a dominant market position in the By Product Type segment of the Fabric Filters & Scrubbers Market, with a 54.70% share. This dominance reflects their established role in high-particulate environments including cement kilns, power boilers, and metallurgical furnaces. Capital expenditure on baghouse retrofits in aging facilities continues to sustain filter media and replacement bag demand, supporting aftermarket revenue across the installed base.

Scrubbers hold the remaining share within the Product Type segment, with wet and dry configurations serving distinct compliance needs. Wet scrubbers address acid gas and fine particulate removal in power and chemical applications. Dry and semi-dry scrubbers are gaining traction in waste-to-energy facilities where water consumption reduction is an operational priority. This split creates parallel procurement channels for suppliers offering both technology lines.

End Use Industry Analysis

Power Generation dominates with 25.40% due to mandatory emissions compliance across coal, gas, and biomass plants.

In 2025, Power Generation held a dominant market position in the By End Use Industry segment of the Fabric Filters & Scrubbers Market, with a 25.40% share. Stringent particulate and SO₂ limits on combustion units drive continuous investment in baghouse upgrades, scrubber installations, and filter bag replacement cycles. This segment provides a structurally recurring revenue base for both OEM suppliers and aftermarket service providers.

Cement and Iron & Steel are the next largest end-use categories, driven by ultra-low-emission mandates applied to kiln exhausts, sinter plants, and electric arc furnaces. Both industries face compliance gaps that require physical retrofits rather than process adjustments alone. Capital commitments from these two sectors sustain demand for high-temperature fabric filter configurations and integrated multi-pollutant control trains.

Chemical & Pharmaceutical and Mining & Minerals follow, each requiring specialized filtration and gas-cleaning solutions tailored to process-specific dust and chemical emission profiles. Waste-to-Energy & Incineration, Automotive & Foundry, Pulp & Paper, and Food & Beverage Processing collectively hold the remaining share, with Waste-to-Energy posting the highest growth trajectory among the smaller segments due to municipal solid waste capacity additions across Europe and East Asia.

Key Market Segments

By Product Type

- Fabric Filters

- Baghouse Filters

- Cartridge Filters

- Compact Modular Fabric Filters

- High-Temperature Fabric Filters

- Others

- Scrubbers

- Wet Scrubbers

- Venturi Scrubbers

- Packed Bed Scrubbers

- Spray Tower Scrubbers

- Impingement Plate Scrubbers

- Cyclonic Spray Scrubbers

- Multi-Stage Wet Scrubbers

- Others

- Dry Scrubbers

- Spray Dryer Absorbers (SDA)

- Circulating Dry Scrubbers (CDS)

- Dry Sorbent Injection (DSI) Systems

- Others

- Wet Scrubbers

By End Use Industry

- Power Generation

- Cement

- Iron & Steel

- Chemical & Pharmaceutical

- Mining & Minerals

- Automotive & Foundry

- Pulp & Paper

- Waste-to-Energy & Incineration

- Food & Beverage Processing

- Others

Market Dynamics

Market Opportunity Analysis - Space-constrained retrofits, membrane scrubbing, and PFAS compliance open premium entry points for specialized vendors

Compact ionic-liquid scrubber technology offers a structural entry point in space-constrained industrial facilities. As reported by ScienceDirect, ionic-liquid systems reduce installation volume to 27 m³ compared with 200 m³ for conventional NaOH scrubbers, a 77.1% reduction versus Wellman-Lord systems. Annual operating savings reach up to USD 558,000 compared with NaOH scrubbers and USD 300,000 compared with Wellman-Lord desulfurization systems. This cost and footprint advantage creates a direct retrofit pathway in facilities where full-scale scrubber replacement is structurally impractical.

Upstream flue gas pretreatment represents an underexploited efficiency lever for downstream fabric filter performance. Data from MDPI shows microwave-assisted non-thermal plasma pretreatment reduced the PM2.5 fraction in flue gas from 70.25% to 18.63%. This reduction lowers filtration loading and extends filter media service life. Vendors who combine pretreatment modules with baghouse systems can offer a differentiated total-system value proposition rather than competing on filter equipment price alone.

Membrane-based scrubbing systems are an underserved technology segment with measurable performance credentials. Figures from ACS show hollow fiber membrane contactors demonstrated SO₂ permeance of 702.4 GPU, enabling compact scrubbing configurations that conventional wet scrubber designs cannot match. This performance at reduced physical scale creates an addressable market in pharmaceutical, specialty chemical, and semiconductor fab applications where space, water, and reagent constraints rule out traditional scrubber installations.

PFAS destruction and abatement represents the highest-premium white space in the market. Most vendors currently supply standard particulate or acid-gas equipment, leaving the integrated PFAS compliance platform largely unaddressed. Suppliers who package high-temperature destruction, fluorinated off-gas polishing, reagent dosing, and continuous stack monitoring into a single contract can expand average project value by 25% to 40% and capture aftermarket service revenue estimated at 0.3x to 0.5x original equipment value over the first 5 years of installation

Technology and Innovation Landscape - PTFE media advances, digital twins, and composite fiber materials redefine performance benchmarks across filtration and scrubbing systems

PTFE membrane engineering has reached a new performance tier. According to ScienceDirect, PTFE-based filtration membranes maintained filtration efficiency above 99.2% while reducing contaminant accumulation by 75%. A separate ScienceDirect study recorded 99.6% separation efficiency, an operating flux of 4,478 L·m⁻²·h⁻¹, and a 6.7-fold increase in outlet velocity through modified coating structures. These results position PTFE media as the benchmark technology for high-efficiency industrial filtration, raising the performance floor for competitive filter products.

High-permeability filtration materials are expanding the design envelope for gas-phase applications. ScienceDirect indicates advanced filtration membranes achieved gas permeance exceeding 449.1 m³·m⁻²·h⁻¹·kPa⁻¹, while hollow fiber membrane systems recorded SO₂ permeance of 702.4 GPU with removal efficiency above 91%, as reported by ACS. These permeance levels open engineering pathways for compact scrubbing systems that outperform conventional wet scrubbers in space-constrained applications, creating a new product category between filtration and absorption.

Composite fiber filter media are delivering simultaneous performance gains across multiple mechanical and chemical metrics. As reported by ScienceDirect, Lyocell-Basalt fiber media achieved 97.7% PM0.3 filtration efficiency alongside a 136.5% increase in bursting strength and a 128.9% increase in tear strength. Functionalized Basalt Fiber fabrics demonstrated a 200-fold improvement in PM2.5 quality factor compared with conventional woven basalt fabrics while simultaneously removing SO₂. These dual-function materials reduce system complexity by combining particulate capture and gas removal in a single media layer.

Digital-twin frameworks are establishing a new standard for predictive operations management in filtration systems. Data from arXiv shows digital-twin models achieved pressure prediction accuracy within 5% relative error under known operating conditions. Donaldson’s expansion of its iCue™ Connected Technology platform in June 2026 to industrial gas and compressed-air filtration equipment reflects commercial adoption of this technology direction. Vendors who integrate predictive monitoring into their equipment value proposition convert one-time hardware sales into recurring digital service contracts, improving customer retention and margin profile.

Drivers

Industrial emissions tightening across power, steel, cement, and waste combustion is the primary 2026 demand catalyst, converting air-pollution control from discretionary capital expenditure into mandatory compliance investment. In the U.S., updated Mercury and Air Toxics Standards strengthened mercury controls and required continuous emissions monitoring, while Europe’s revised Industrial Emissions Directive accelerates Best Available Techniques updates across cement, waste, and metals sectors. Compliance gaps in large kilns, combustors, and sinter lines require physical retrofits including baghouses, dry sorbent injection, and scrubber systems rather than process tuning alone.

This regulatory shift increases aftermarket intensity through higher reagent consumption, more frequent filter replacement cycles, and demand for bundled EPC solutions combining filtration, controls, fans, ducting, and emissions monitoring. Suppliers who can deliver integrated multi-pollutant compliance trains with performance guarantees hold a structural advantage over equipment-only vendors as regulatory deadlines approach.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial emissions tightening across power, steel, cement, and waste combustion | +2.1% | EU core, China core, India corridors, North America selective | Short term |

| China steel ultra-low-emission completion and retrofit wave | +1.8% | China core, ASEAN spill-over | Short term |

| Waste-to-energy and municipal waste incineration expansion lifting flue-gas cleaning intensity | +1.4% | EU core, Japan, South Korea, selective Middle East | Medium term |

| Dust-heavy capacity additions in cement, DRI, minerals, and bulk materials processing | +1.6% | India core, Southeast Asia, MENA, Latin America spill-over | Medium term |

| Compliance shift toward continuous monitoring and performance-guaranteed APC systems | +1.1% | North America, EU, China, India urban clusters | Short term |

| Retrofit economics favoring baghouse and hybrid scrubber upgrades over full process replacement | +1.3% | North America installed base, EU brownfield assets, APAC industrial estates | Medium term |

Restraints

Extended delivery cycles for highly engineered air-pollution control systems create a persistent commercial restraint. Euro-area supplier delivery times in May 2026 reached their worst level since June 2022, reflecting renewed supply stress across fabricated equipment and specialty components. Standard systems that typically require 24 to 32 weeks can extend to 36 to 50 weeks for corrosion-heavy scrubber trains or shutdown-tied retrofit projects, delaying backlog conversion and increasing working-capital intensity for suppliers.

Installation bottlenecks and constrained outage windows further defer commissioning beyond planned turnaround schedules, prompting customers to postpone orders until installation certainty improves. This dynamic is most acute in APAC export-driven manufacturing hubs and Middle East industrial projects reliant on imported fans, vessels, and control systems. The estimated drag on achievable growth is 1.1 percentage points, driven by project execution delays rather than weak underlying demand.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CapEx deferrals in heavy industry | -1.6% | Europe, North America core, China-linked APAC | Short term (≤ 2 years) |

| High materials and reagent costs | -1.3% | North America, EU, India, ASEAN | Short term (≤ 2 years) |

| Long engineered equipment lead times | -1.1% | APAC corridors, EU, Middle East, North America | Medium term (2-4 years) |

| Wastewater and PFAS compliance burden | -0.9% | EU core, UK, advanced APAC | Medium term (2-4 years) |

| Trade tariffs and carbon border costs | -0.8% | US import market, EU import-dependent OEM base | Medium term (2-4 years) |

| Retrofit permitting and shutdown complexity | -0.7% | Europe, North America, mature industrial Asia | Long term (≥ 4 years) |

Challenges

The central challenge in 2026 is the shift from equipment-centric compliance to data-intensive, continuously verifiable operations. EU Industrial Emissions framework rules and U.S. major-source boiler requirements now require operators to track an additional 15 to 30 operating variables per site and manage compliance documentation workloads that are 20% to 40% higher than legacy systems supported. Recurring external audit and data-integration costs can reach low six figures annually in complex facilities, creating a structural gap between physical process performance and the digital evidence required to prove compliance.

This gap forces procurement decisions toward vendors that deliver integrated monitoring, emissions traceability, and audit-ready reporting. Suppliers without digital compliance capabilities face competitive displacement even when their filtration equipment meets technical performance thresholds. The estimated growth drag from compliance overhead and system complexity is 1.0 percentage point, independent of underlying demand conditions.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Filter Media Volatility | -1.1% | APAC manufacturing base; EU process industries; North America retrofit demand | Medium term (2-4 years) |

| Specialist Labor Deficit | -0.9% | North America core; EU regulatory hubs; India and Southeast Asia service corridors | Long term (≥ 4 years) |

| Red Sea Logistics Drag | -0.7% | Europe import lanes; Middle East; India-to-EU and Asia-to-EU equipment flows | Short term (≤ 2 years) |

| Compliance Data Burden | -1.0% | EU regulatory hubs; North America major-source installations | Medium term (2-4 years) |

| Water-Energy Optimization Gap | -0.8% | Water-stressed APAC sites; EU resource-efficiency regimes; Middle East heavy industry | Long term (≥ 4 years) |

| PFAS Material Transition Risk | -0.6% | EU filter-media supply chain; export-oriented OEMs; high-spec process sectors | Medium term (2-4 years) |

Opportunities

PFAS destruction represents one of the highest-value white spaces in the air pollution control market. Most fabric filter and scrubber vendors still sell standard particulate or acid-gas equipment. Packaging high-temperature destruction, fluorinated off-gas polishing, reagent dosing, and stack analytics into a premium compliance platform for waste combustors and specialty chemical plants converts a mature capex market into a high-value solution stack with service annuities. This integration can expand average project value by roughly 25% to 40% and lift aftermarket attachment rates by 10 to 15 percentage points.

An adjacent serviceable market in continuous monitoring, reagent supply, and residual management is estimated at 0.3x to 0.5x original equipment revenue over the first 5 years of installation. EPA’s 2026 PFAS disposal guidance and active combustor emissions rulemaking increase the probability that customers will favor integrated abatement trains over single-point equipment. Early entrants who lock in reference sites before procurement specifications fully commoditize can capture an estimated +1.4 percentage points of market CAGR upside.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| PFAS destruction systems | +1.4% | North America core, EU | Short term (≤ 2 years) |

| Semiconductor fab utilities | +1.7% | APAC, India, North America | Short term (≤ 2 years) |

| Battery materials abatement | +1.5% | China, EU, US, India | Medium term (2-4 years) |

| Digital compliance services | +1.2% | North America, EU, GCC, APAC | Short term (≤ 2 years) |

| Retrofit roll-up strategy | +1.8% | EU, US, India, Southeast Asia | Medium term (2-4 years) |

| Circular waste-to-value plants | +1.3% | China, India, EU | Long term (≥ 4 years) |

Regional Analysis

Asia Pacific Dominates the Fabric Filters & Scrubbers Market with a Market Share of 40.10%, Valued at USD 0.5 Billion

Asia Pacific commands the largest regional share at 40.10%, valued at USD 0.5 Billion in 2025. China’s ultra-low-emission retrofit mandate across steel and power sectors drives the highest single-country equipment demand. India’s expanding cement and thermal power capacity adds a second high-volume procurement corridor. This dual growth engine makes APAC the most strategically important region for both OEM suppliers and aftermarket service providers through 2035.

North America holds a substantial share underpinned by compliance-driven retrofit demand across aging power, industrial boiler, and waste combustion assets. The U.S. Mercury and Air Toxics Standards and major-source boiler rules require continuous emissions monitoring and higher-efficiency particulate and acid gas controls. Suppliers who offer performance-guaranteed baghouse and scrubber systems with integrated monitoring capabilities are best positioned to capture this replacement and upgrade cycle.

Europe is driven by the revised Industrial Emissions Directive, which is tightening Best Available Techniques thresholds across cement, waste, chemicals, and metallurgical operations. Compliance gaps in brownfield facilities translate directly into baghouse retrofits, dry sorbent injection upgrades, and wet scrubber installations. The EU market rewards integrated EPC solutions that bundle filtration, reagent supply, controls, and audit-ready emissions monitoring into a single contract.

Latin America and the Middle East & Africa represent smaller but structurally growing regional markets. Latin America’s mining, cement, and power sectors are adopting stricter national emission standards modeled on EU benchmarks, creating early-stage retrofit demand. The Middle East is investing in industrial diversification projects including chemicals and waste-to-energy, where multi-pollutant control trains are specified from the outset rather than retrofitted.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

CECO Environmental has built a strong position in emissions management through acquisitions and large-scale project execution. In January 2025, the company completed its acquisition of Profire Energy, extending its combustion management and environmental efficiency capabilities. In December 2025, CECO secured its largest-ever emissions management order valued at more than USD 135 million for a natural-gas power facility, demonstrating its capacity to win performance-critical, high-value compliance contracts.

Donaldson Company, Inc. holds a technology differentiation advantage through its iCue™ Connected Technology platform, which it expanded in June 2026 to industrial gas and compressed-air filtration equipment. This extension delivers real-time monitoring and predictive maintenance across the installed asset base, creating a recurring digital service revenue stream. Donaldson’s ability to link filtration hardware with continuous performance data reduces customer switching costs and positions the company against digital-first challengers in the compliance monitoring space.

Key Players

- CECO Environmental

- Donaldson Company, Inc.

- Babcock & Wilcox Enterprises

- Ebara Technologies

- Thermax Limited

- AAF International

- FLSmidth

- Hamon Group

- Nederman Holding AB

- Camfil Group

- KC Cottrell Co., Ltd.

- Dürr AG

- Mitsubishi Hitachi Power Systems

- Tri-Mer Corporation

- GEA Group

- Scheuch GmbH

- Other Key Players

Recent Developments

- June 2026 – Donaldson expanded its iCue™ Connected Technology platform to industrial gas and compressed-air filtration equipment, extending real-time monitoring and predictive maintenance capabilities across filtration assets.

- August 2025 – Micronics promoted advanced baghouse and fabric filtration technologies through its dedicated Baghouse and Fabric Filtration Seminar targeting cement, power, and metals industries, highlighting ongoing industry investment in filtration performance and operational optimization.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.3 Billion |

| Forecast Revenue (2035) | USD 1.83 Billion |

| CAGR (2026-2035) | 3.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Fabric Filters: Baghouse Filters, Cartridge Filters, Compact Modular Fabric Filters, High-Temperature Fabric Filters, Others; Scrubbers: Wet Scrubbers, Dry Scrubbers), By End Use Industry (Power Generation, Cement, Iron & Steel, Chemical & Pharmaceutical, Mining & Minerals, Automotive & Foundry, Pulp & Paper, Waste-to-Energy & Incineration, Food & Beverage Processing, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | CECO Environmental, Donaldson Company Inc., Babcock & Wilcox Enterprises, Ebara Technologies, Thermax Limited, AAF International, FLSmidth, Hamon Group, Nederman Holding AB, Camfil Group, KC Cottrell Co. Ltd., Dürr AG, Mitsubishi Hitachi Power Systems, Tri-Mer Corporation, GEA Group, Scheuch GmbH, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |