Quick Navigation

- Report Overview

- Key Takeaways

- Service Type Analysis

- Deployment Mode Analysis

- Application Analysis

- End User Analysis

- By Service Type

- By Deployment Mode

- By Application

- By End User

- Drivers

- Restraints

- Opportunities

- Impact of Macroeconomic / Geopolitical Factors

- Latest Trends

- Country Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

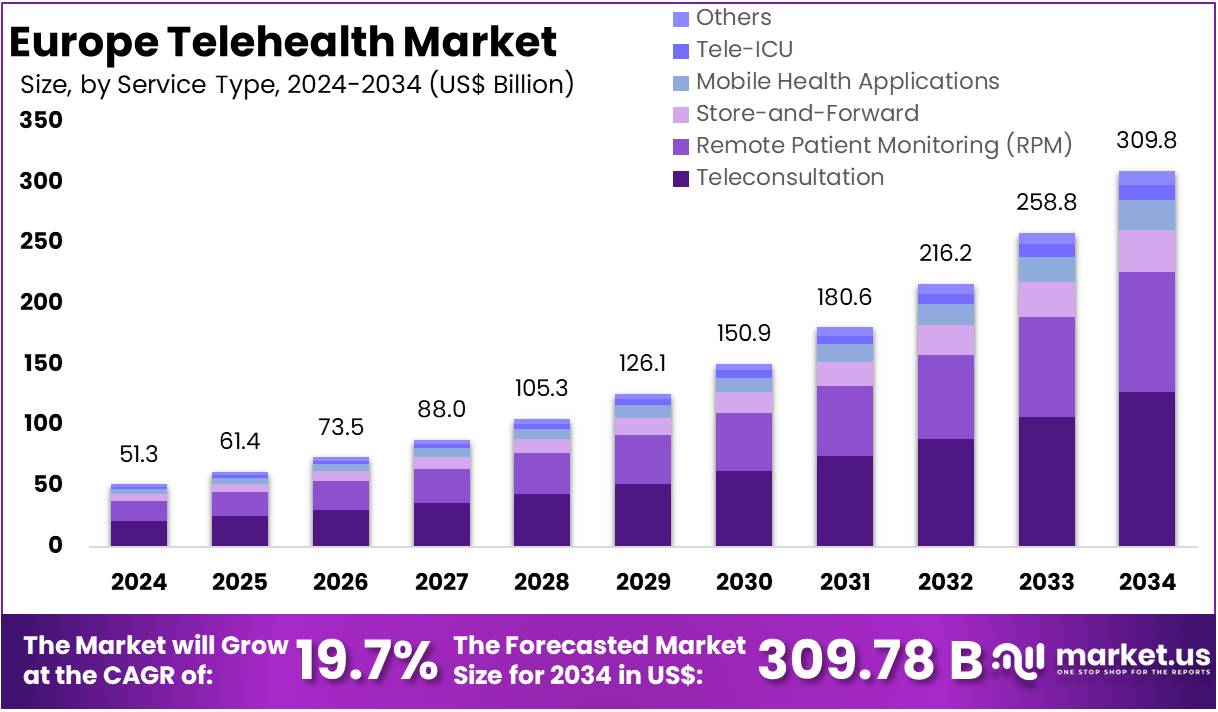

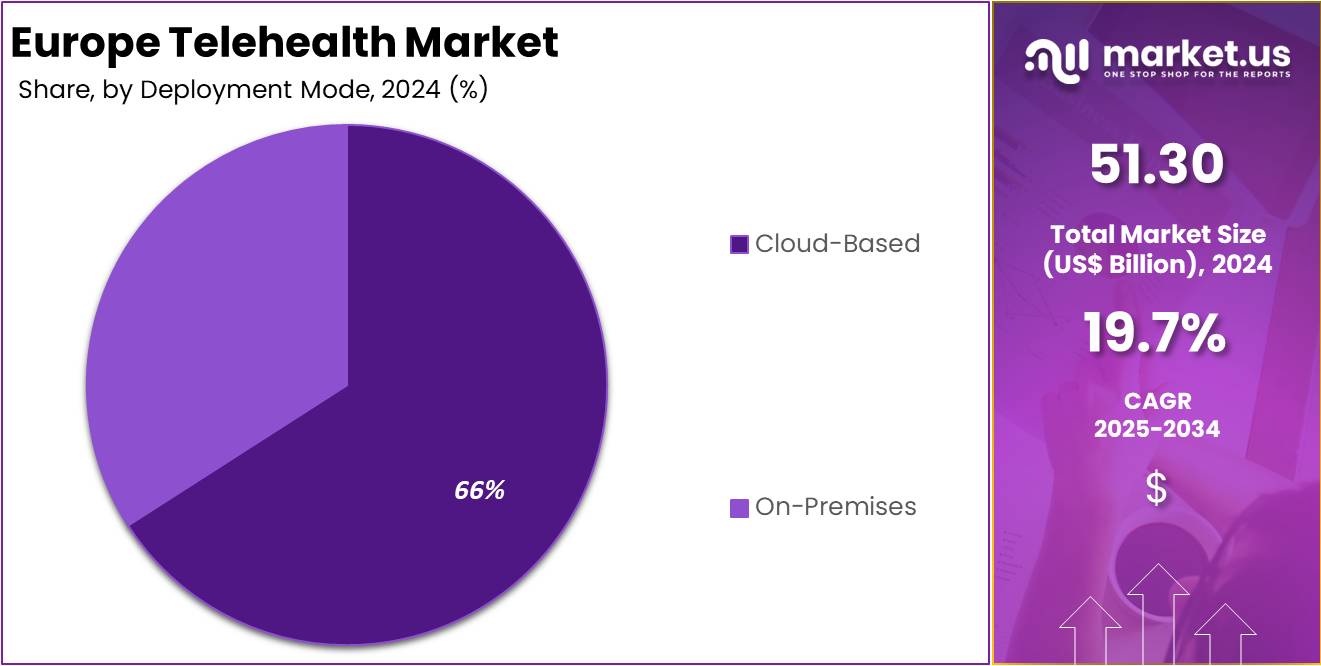

The Europe Telehealth Market size is expected to be worth around US$ 309.8 Billion by 2034, from US$ 51.3 Billion in 2024, growing at a CAGR of 19.7% during the forecast period from 2025 to 2034.

The Europe telehealth market is experiencing rapid expansion, driven by rising demand for remote healthcare, an aging population, and advances in digital health technologies. Key growth factors include the need for chronic disease management, shortages of medical professionals, and increasing adoption of telemedicine platforms, mobile health (mHealth) applications, and wearable devices.

Services, such as remote consultations and patient support, represent the largest revenue segment, while software and hardware (wearables, sensors) also play crucial roles. The mHealth segment alone accounts for over a third of the market’s revenue, reflecting the widespread use of mobile apps for health monitoring and management.

Government initiatives, supportive regulations, and investments in AI and digital infrastructure further accelerate telehealth adoption, particularly in regions with advanced healthcare systems like the UK. Overall, telehealth is transforming healthcare delivery in Europe by improving accessibility, efficiency, and patient outcomes while reducing the need for in-person visits.

Despite the positive outlook, challenges such as data privacy concerns, regulatory complexities, and the need for robust digital infrastructure remain. Addressing these issues will be crucial for the sustainable growth of the telehealth market in Europe. The European telehealth market is poised for substantial growth, driven by demographic shifts, technological innovations, and supportive policies. With continued investment and strategic development, telehealth has the potential to transform healthcare delivery across the continent.

Key Takeaways

- By Service Type, the market is segmented into Teleconsultation, Remote Patient Monitoring (RPM), Store-and-Forward, Mobile Health Applications, Tele-ICU and others. Teleconsultation is expected to hold the largest market share of 40.8% driven by the widespread adoption for virtual doctor-patient consultations across general and specialized care.

- By Deployment Mode, segment includes Cloud-Based and On-Premises. Cloud-Based dominate this market with 65.9% market share, due to its scalability, accessibility, and secure data storage, which enables telehealth services to be accessible from various locations.

- By Distribution Channel, the market is divided into Telepsychiatry, Teleradiology, Teledermatology, Teleneurology, Teledermatology, and Others. Telepsychiatry held the dominant position with 27.5% market share due to the rising demand for mental health services, especially after the COVID-19 pandemic, and the increasing shortage of mental health professionals.

- By End User, the market is divided into Healthcare Providers, Patients, Payers, and Others. Healthcare providers dominated the end-user segment with 46.2% market share, as hospitals, clinics, and individual practitioners are the largest adopters of telehealth services for providing care.

Service Type Analysis

Teleconsultation is the dominating service type in the European telehealth market with 40.8% market share. It provides a virtual healthcare delivery model where patients can consult healthcare providers via video calls, phone calls, or text-based messaging platforms. Teleconsultation is particularly popular due to its convenience and accessibility, enabling patients to receive medical advice and prescriptions without needing to visit healthcare facilities physically.

The demand for teleconsultation services has surged, particularly since the COVID-19 pandemic, which saw a rapid adoption of virtual healthcare due to lockdowns and social distancing measures. This service is widely used in primary care, mental health services, and urgent care, covering a wide array of health concerns from routine check-ups to minor illnesses.

Teleconsultation’s growth in Europe is further supported by advancements in digital health technologies and the increasing preference for remote care among patients. Additionally, government policies and health insurance reforms across European countries have enhanced the reimbursement options for teleconsultation services, making it more accessible to the general population. The European Health Data Space (EHDS) Regulation came into force in March 2025, enabling companies to access and share electronic health data for care and research, which is set to boost teleconsultation services across the EU.

Deployment Mode Analysis

Cloud-Based deployment is the dominant mode in the European telehealth market with 65.9% market share. This model enables healthcare providers to deliver telehealth services via a scalable, flexible, and cost-effective infrastructure that can be accessed from anywhere. Cloud-based solutions allow for seamless integration with electronic health records (EHR) systems and other healthcare technologies, providing healthcare providers with real-time access to patient data and facilitating virtual consultations, remote monitoring, and other telehealth services.

The popularity of cloud-based solutions is driven by several factors, including the need for efficient data storage, the ability to handle large volumes of patient information securely, and the flexibility to scale services as demand grows. This model is also advantageous in terms of cost-efficiency, as healthcare organizations do not need to invest in expensive on-premises hardware or IT staff. Furthermore, cloud-based platforms support interoperability across different healthcare systems, which is crucial for coordinated care in telehealth services.

In February 2025, Philips announced the expansion of its cloud-based HealthSuite Imaging platform to Europe. This software-as-a-service (SaaS) solution is hosted on Amazon Web Services (AWS) and offers radiology departments secure, remote access to imaging studies and AI-enabled workflows. The platform integrates generative AI for tasks like conversational reporting, aiming to reduce clinician workload and improve diagnostic speed and quality. The rollout covers countries including Italy, UK, Belgium, Netherlands, France, Austria, and more.

Application Analysis

Telepsychiatry is the dominating application segment with 27.5% market share in the European telehealth market. This segment has seen significant growth due to the rising demand for mental health services, especially in the wake of the COVID-19 pandemic. Telepsychiatry enables patients to access psychiatric care, therapy, and counseling remotely via video consultations, phone calls, or text-based platforms. The growing awareness of mental health issues, combined with the shortage of mental health professionals, particularly in rural and underserved areas, has created a strong demand for telepsychiatry services.

In Europe, telepsychiatry has been instrumental in reducing the stigma associated with seeking mental health care. It provides a private and convenient way for individuals to access support, improving overall accessibility and patient engagement. Governments and health insurers have increasingly expanded coverage for mental health services, further driving the adoption of telepsychiatry. The integration of AI and digital tools to support mental health assessments and treatment plans is also contributing to the growth of this segment.

End User Analysis

Healthcare Providers dominate the end-user segment with 46.2% market share in the European telehealth market. Hospitals, clinics, private practices, and specialist healthcare providers are the primary adopters of telehealth services, leveraging virtual consultations, remote monitoring, and telemedicine platforms to deliver care. The demand for telehealth solutions among healthcare providers has surged due to their ability to extend services to patients, particularly in underserved areas, and improve care continuity while managing increasing patient loads.

Telehealth allows healthcare providers to optimize their workflows, reduce in-person visits for non-urgent matters, and address both routine and follow-up care remotely. The integration of telehealth solutions into electronic health records (EHR) and other systems further enhances the efficiency of care delivery.

Additionally, healthcare providers are increasingly adopting telehealth due to government incentives, reimbursement expansion for telehealth services, and the ongoing pressure to reduce costs while improving patient outcomes. The flexibility and scalability of telehealth platforms enable healthcare providers to offer services to a broader patient base, contributing to market growth in Europe.

By Service Type

- Teleconsultation

- Remote Patient Monitoring (RPM)

- Store-and-Forward

- Mobile Health Applications

- Tele-ICU

- Others

By Deployment Mode

- Cloud-Based

- On-Premises

By Application

- Telepsychiatry

- Teleradiology

- Teledermatology

- Teleneurology

- Teledermatology

- Others

By End User

- Healthcare Providers

- Patients

- Payers

- Others

Drivers

Increasing Demand for Accessible Healthcare

One of the primary drivers of the Europe Telehealth Market is the increasing demand for accessible and convenient healthcare. The aging population across Europe, coupled with the rising incidence of chronic diseases, has significantly increased the pressure on healthcare systems. Patients are seeking more flexible and timely solutions to manage their health, which has contributed to the rapid adoption of telehealth services. Telehealth provides a valuable solution by offering remote consultations, reducing travel time, and enabling patients to access healthcare services from the comfort of their homes.

The COVID-19 pandemic accelerated this trend by forcing patients and healthcare providers to adopt remote care solutions to ensure continuity of care while maintaining social distancing measures. Governments across European countries have also recognized the potential of telehealth to alleviate the burden on traditional healthcare settings, leading to policy reforms and increased reimbursement for telehealth services. As healthcare systems aim to provide more personalized, cost-effective, and accessible care, telehealth is poised to play a central role in reshaping healthcare delivery across Europe.

Restraints

Regulatory and Data Privacy Concerns

Despite the promising growth of the Europe Telehealth Market, regulatory challenges and data privacy concerns act as significant restraints. Telehealth services involve the transmission of sensitive patient data, which makes them vulnerable to breaches and unauthorized access. Europe has stringent data protection regulations, particularly under the General Data Protection Regulation (GDPR), which sets high standards for data security and patient privacy. Telehealth companies must comply with these regulations, which can be complex and vary from country to country.

The inconsistent regulatory framework across European countries can also hinder the seamless integration of telehealth services. While some countries have established clear guidelines for telehealth, others have ambiguous regulations, making it difficult for providers to operate across borders. Furthermore, there is still a lack of uniform reimbursement policies across European healthcare systems, which can limit the financial viability of telehealth services.

These regulatory and data privacy challenges create barriers to widespread adoption, particularly for smaller telehealth companies or those looking to expand their services across multiple countries. Ensuring compliance with regulations and addressing privacy concerns will be crucial for the sustainable growth of the telehealth market in Europe.

Opportunities

Expansion in Rural and Underserved Areas

An exciting opportunity for the Europe Telehealth Market lies in the expansion of telehealth services in rural and underserved areas. Rural regions across Europe often face challenges such as a shortage of healthcare professionals, limited access to medical facilities, and long travel times to the nearest healthcare provider. Telehealth can bridge this gap by enabling patients in these areas to access healthcare services remotely, improving access to essential care and reducing healthcare disparities.

The European Union (EU) and several member states are investing in digital health initiatives to improve healthcare accessibility in underserved areas. Government-funded programs and public-private partnerships are creating favorable conditions for the expansion of telehealth in these regions. Telehealth platforms can offer remote consultations, monitoring for chronic conditions, and mental health services, which are particularly important for rural populations.

Impact of Macroeconomic / Geopolitical Factors

Economic conditions in Europe, such as inflation rates, healthcare spending, and unemployment levels, directly impact the demand for telehealth services. During economic downturns, healthcare budgets may be constrained, pushing healthcare providers to seek more cost-effective solutions. Telehealth, with its lower operational costs compared to traditional in-person visits, presents a valuable solution to manage healthcare expenses.

Additionally, the economic burden of an aging population, particularly in countries like Italy and Germany, increases the demand for remote healthcare services to manage chronic diseases and elderly care. However, if economic conditions lead to reduced healthcare spending, it may limit the expansion of telehealth infrastructure and services.

Geopolitical tensions, such as the ongoing conflict in Ukraine, can disrupt the flow of goods and services, potentially affecting the supply chains of telehealth technology and equipment. Political instability and trade barriers might slow down the adoption of telehealth solutions in certain countries. On the other hand, the European Union’s efforts to create a unified digital health ecosystem through initiatives like the European Health Data Space can foster cross-border telehealth services, increasing accessibility and reducing regulatory hurdles.

Latest Trends

Integration of AI and Digital Health Technologies

A prominent trend in the Europe Telehealth Market is the growing integration of artificial intelligence (AI) and other digital health technologies into telehealth services. AI is being leveraged to improve diagnostics, personalize patient care, and streamline healthcare processes. In telehealth, AI-driven tools can assist healthcare providers in analyzing medical data, such as medical images or patient history, to make faster and more accurate diagnoses.

AI is also being used in symptom-checking apps and virtual assistants to triage patients and provide initial consultations, making healthcare more efficient. In addition, predictive analytics and machine learning algorithms can help monitor patients’ health remotely, particularly for those with chronic conditions, enabling early intervention and better disease management.

Digital health technologies, including wearable devices, mobile health apps, and remote monitoring systems, are becoming increasingly integrated with telehealth platforms. These technologies allow healthcare providers to collect real-time data from patients and provide personalized care based on continuous health monitoring.

This trend towards digital health integration enhances the overall telehealth experience, improving both the quality and efficiency of care. As AI and digital health technologies continue to evolve, they will play a central role in shaping the future of the telehealth market in Europe.

Country Analysis

The European telehealth market is experiencing varied growth across different countries. Germany leads with strong market adoption, supported by a well-integrated healthcare system and government-backed digital health initiatives. France is witnessing rapid telehealth adoption, driven by both patient demand and increasing government support, particularly in rural and underserved areas. The UK has a robust telehealth infrastructure, largely driven by the National Health Service (NHS), offering extensive virtual consultations and integrating telehealth with public health systems.

Spain is expanding its telehealth services, focusing on rural populations and elderly care, addressing accessibility challenges. Italy sees growing telehealth adoption, fueled by its aging population and government-driven digital health programs. In Russia, while the market is emerging, telehealth adoption is still limited but showing signs of growth. The Netherlands is ahead in integrating telehealth solutions into its national healthcare system, with advanced technologies in remote patient monitoring. Rest of Europe displays varying telehealth adoption rates, with increasing momentum in digital health solutions across the region.

Key Countries

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Key Players Analysis

Leading companies in the market are Doctolib, Kry / Livi, Babylon Health, Zava, Ada Health, Push Doctor, Livi, HealthHero, Medbelle, TeleClinic, Cureety, Medi24, Qare, Bingli, Diagnose.me, Immedicare, AccuRx, Min Doktor, Formel Skin, Onera Health, and Others. Doctolib is one of Europe’s largest telehealth platforms, providing online appointment booking, teleconsultation, and health management services. Doctolib initially focused on simplifying the appointment scheduling process for patients and healthcare providers.

Kry, known as Livi in certain markets like the UK and France, is a Swedish-based digital healthcare provider that offers remote consultations through its app. Founded in 2014, Kry operates across multiple European countries and has rapidly expanded its telehealth offerings. Babylon Health is a UK-based digital health company that has revolutionized telehealth with its AI-powered platform. Babylon offers a combination of virtual consultations with doctors and health assessments powered by AI.

Top Key Players in the Europe Telehealth Market

- Doctolib

- Kry / Livi

- Babylon Health

- Zava

- Ada Health

- Push Doctor

- Livi

- HealthHero

- Medbelle

- TeleClinic

- Cureety

- Medi24

- Qare

- Bingli

- me

- Immedicare

- AccuRx

- Min Doktor

- Formel Skin

- Onera Health

- Others

Recent Developments

- In April 2021, Digital healthcare company Kry, operating as Livi in the UK and France, has announced a US$ 297.7 million (€262 million) funding round to support its European expansion. The Series D funding round was led by CPP Investments (CPPIB) and Fidelity Management & Research LLC, with participation from existing investors including the Ontario Teachers’ Pension Plan (Ontario Teachers’), Index Ventures, Accel, Creandum, and Project A.

- In March 2020, Doctolib, one of Europe’s leading e-health companies, has raised US$ 170 million (€150 million), bringing its valuation to over US$ 1.13 billion (€1 billion) and making it Europe’s newest unicorn. Doctolib provides doctors and hospitals with a comprehensive software solution designed to improve operational efficiency. Its suite of online services helps healthcare professionals reduce overhead costs and minimize no-shows, while offering patients the ability to find and book healthcare practitioners 24/7, access remote medical consultations via video, and receive digital prescriptions through their online accounts.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 51.30 billion |

| Forecast Revenue (2034) | US$ 309.78 billion |

| CAGR (2025-2034) | 19.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Teleconsultation, Remote Patient Monitoring (RPM), Store-and-Forward, Mobile Health Applications, Tele-ICU, and Others), By Deployment Mode (Cloud-Based, and On-Premises), By Application (Telepsychiatry, Teleradiology, Teledermatology, Teleneurology, Teledermatology, and Others) and By End User (Healthcare Providers, Patients, Payers, and Others) |

| Country Analysis | Germany, France, The UK, Spain, Italy, Russia, Netherland, and Rest of Europe |

| Competitive Landscape | Doctolib, Kry / Livi, Babylon Health, Zava, Ada Health, Push Doctor, Livi, HealthHero, Medbelle, TeleClinic, Cureety, Medi24, Qare, Bingli, Diagnose.me, Immedicare, AccuRx, Min Doktor, Formel Skin, Onera Health, and Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |