Quick Navigation

Report Overview

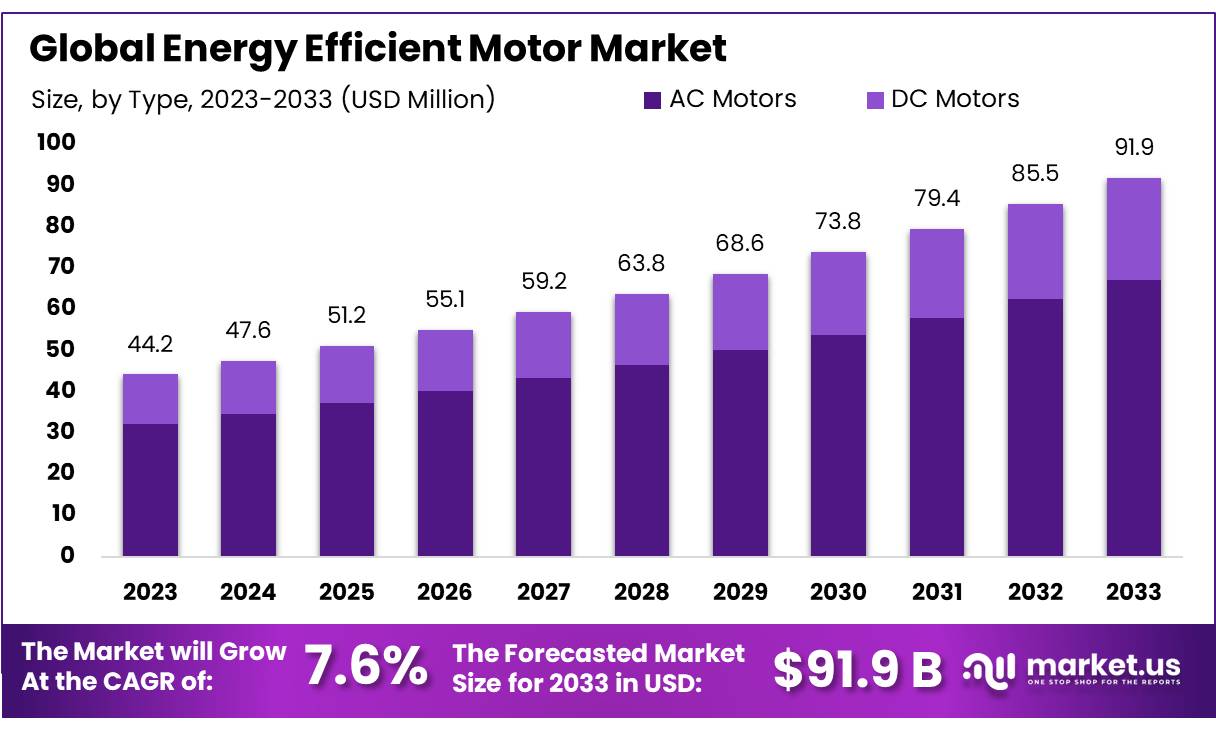

The Global Energy Efficient Motor Market size is expected to be worth around USD 91.9 Billion by 2033, from USD 44.2 Billion in 2023, growing at a CAGR of 7.6% during the forecast period from 2024 to 2033.

An energy-efficient motor is a type of electric motor designed to achieve higher energy efficiency compared to standard motors. These motors consume less electrical energy while delivering the same or better performance, effectively reducing operational costs and environmental impact.

Energy-efficient motors are constructed using improved materials, advanced designs, and better manufacturing techniques which contribute to their enhanced performance. These modifications can include the use of higher quality magnets, more precise winding, and reduced electrical losses in the motor’s core. Deliver significant improvements in energy efficiency, offering a competitive edge in sectors where reducing energy consumption is a top priority.

The rise in energy-efficient motor adoption is further supported by government initiatives aimed at improving energy efficiency and reducing carbon emissions. For example, the European Union has implemented the EcoDesign Directive, which mandates higher efficiency standards for motors used in industrial and commercial applications.

As part of the EU’s Green Deal, the directive has set stricter performance standards, with goals to reduce energy consumption by 32.5% by 2030. Similar regulations are being adopted in North America, with the U.S. Department of Energy (DOE) enforcing energy efficiency standards for motors through its Energy Independence and Security Act (EISA).

This act, alongside global initiatives, has led to increased demand for energy-efficient motors, particularly in industries like manufacturing, HVAC, and transportation, where motors are essential for operational processes.

In addition to regulatory pressure, businesses are increasingly recognizing the financial benefits of energy-efficient motors. As electricity costs rise, companies are seeking ways to optimize energy use and reduce operational costs.

Studies show that energy-efficient motors can reduce energy consumption by 20-30%, resulting in substantial cost savings over the motor’s lifetime. These savings, coupled with the lower maintenance costs associated with more efficient motors, make the investment in energy-efficient motors financially viable for many organizations.

Furthermore, the growing focus on sustainability is encouraging industries to adopt more energy-efficient technologies. With environmental concerns at the forefront of global agendas, energy-efficient motors offer a way to reduce greenhouse gas emissions and contribute to a more sustainable industrial landscape.

As organizations strive to meet sustainability targets and comply with regulations, the adoption of energy-efficient motors is expected to increase steadily across sectors. The market is also seeing significant growth in applications for energy-efficient motors in renewable energy projects, particularly in wind and solar power generation, where energy conservation is critical to maintaining efficiency.

In conclusion, the energy-efficient motor market is poised for significant growth due to a combination of regulatory pressure, cost-saving potential, and the global shift towards sustainability. As more industries seek to reduce their energy consumption and carbon footprint, energy-efficient motors will continue to play a crucial role in achieving these goals, offering enhanced performance, reduced costs, and environmental benefits.

Key Takeaways

- Energy Efficient Motor Market size is expected to be worth around USD 91.9 Billion by 2033, from USD 44.2 Billion in 2023, growing at a CAGR of 7.6%.

- AC motors held a dominant market position in the energy efficient motor sector, capturing more than a 73.4% share.

- 2.2-375 kW held a dominant market position in the energy efficient motor sector, capturing more than a 45.4% share.

- IE3 efficiency held a dominant market position, capturing more than a 44.4% share.

- Totally Enclosed Fan Cooled (TEFC) motors held a dominant market position, capturing more than a 68.1% share.

- HVAC systems held a dominant market position in the energy-efficient motor market, capturing more than a 25.4% share.

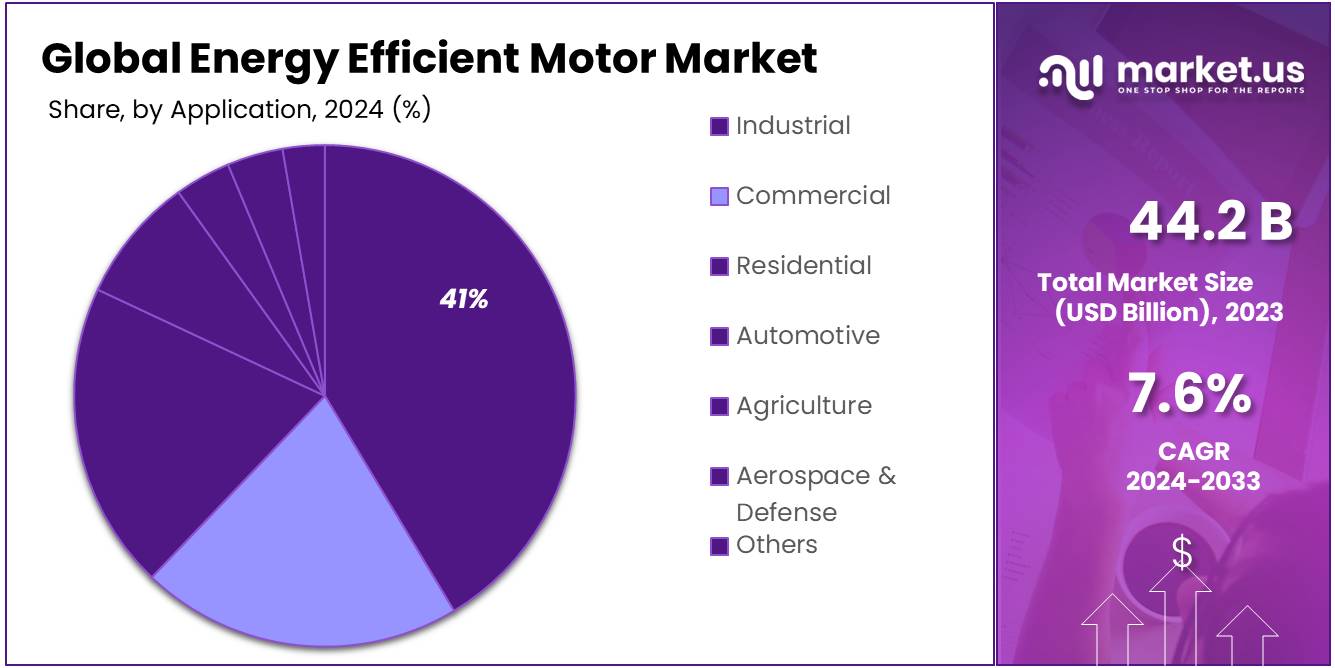

- Industrial applications held a dominant market position in the energy-efficient motor market, capturing more than a 45.5% share.

- Asia Pacific (APAC) region dominates the global energy-efficient motor market, accounting for 46.4% of the market share, valued at approximately USD 20.5 billion.

By Type

In 2023, AC motors held a dominant market position in the energy efficient motor sector, capturing more than a 73.4% share. This significant market dominance can be attributed to their wide application across various industries, including manufacturing, HVAC, and automotive, where the demand for energy efficiency is particularly high. AC motors are favored for their reliability, cost-effectiveness, and ability to operate at variable speeds with high efficiency, making them suitable for a broad range of industrial uses.

Conversely, DC motors, while possessing a smaller segment of the market, are critical in applications requiring high torque and precise speed control, such as in electric vehicles and industrial robotics. DC motors are appreciated for their simplicity and high-performance capabilities in demanding applications that require precise control over motor speed and quick response to changing loads.

By Power Output Rating

In 2023, motors with a power output rating of 2.2-375 kW held a dominant market position in the energy efficient motor sector, capturing more than a 45.4% share. This segment’s prominence is largely due to its broad applicability across various industrial applications that require substantial power but also demand high efficiency, such as in manufacturing processes, large HVAC systems, and heavy machinery. These motors are pivotal in settings that balance the need for significant mechanical power with energy conservation goals.

Motors with a power output of <1 kW, while suitable for smaller applications like domestic appliances and office equipment, occupy a smaller market share. These motors are ideal for applications where compact size and low power consumption are critical.

The 1-2.2 kW range is also essential but typically finds its niche in medium-scale applications, bridging the gap between low-power and high-power needs. This range is particularly common in commercial applications and smaller industrial machinery, where they provide a good compromise between power and efficiency.

Motors with a power output of >375 kW are used in the most demanding industrial environments, such as mining and large-scale manufacturing. Although they represent a smaller portion of the market, their impact on energy consumption is significant, highlighting the importance of energy efficiency in these high-power applications. These motors are crucial for industries aiming to reduce their energy footprint while maintaining high productivity levels.

By efficiency level

In 2023, motors rated at IE3 efficiency held a dominant market position, capturing more than a 44.4% share. This dominance is largely due to the balance IE3 motors strike between cost and efficiency, making them a preferred choice for industries looking to reduce energy consumption without incurring the higher costs associated with IE4 and IES motors. IE3 motors are widely recognized for their high efficiency and reliability in various applications, including pumps, fans, and compressors, where moderate to high energy savings is crucial.

Following IE3, the IE4 motors also represent a significant portion of the market, especially in applications where even higher energy efficiency is necessary. Although more expensive, IE4 motors offer superior efficiency and lower energy consumption, which can lead to cost savings over the motor’s operational life, particularly in continuous or high-duty applications.

Motors with an IE2 rating are generally less efficient than IE3 and IE4 but continue to be used in environments where the initial cost is a more critical factor than long-term energy savings. These motors are suitable for less demanding applications where the benefits of higher efficiency levels do not justify the higher initial costs.

The emerging category of IES (Super Premium Efficiency) motors, while holding the smallest market share, is gaining attention for its potential to provide maximum energy savings and operational efficiency. These motors are typically used in highly specialized applications that prioritize energy efficiency above all other factors. As global energy standards become more stringent, the demand for IES motors is expected to grow, reflecting the industry’s movement towards more sustainable and energy-efficient technologies.

By Installation Type

In 2023, Totally Enclosed Fan Cooled (TEFC) motors held a dominant market position, capturing more than a 68.1% share. This dominance is primarily due to their design, which allows them to operate in a wide variety of environments without exposure to external conditions such as dust, moisture, and other contaminants.

TEFC motors are particularly favored in industries where such protective features are crucial, including manufacturing, chemicals, and outdoor applications. Their robust enclosure ensures that internal components are shielded from environmental elements, which significantly enhances durability and reliability.

Open Drip Proof (ODP) motors, while occupying a smaller portion of the market, are preferred in cleaner, cooler environments where moisture and particulate contaminants are minimal. These motors are cost-effective and typically used in indoor applications, such as in commercial buildings and light manufacturing, where the ambient conditions are controlled. ODP motors offer sufficient cooling and protection for many general-purpose uses but do not have the same level of environmental isolation as TEFC motors.

By Application

In 2023, HVAC systems held a dominant market position in the energy-efficient motor market, capturing more than a 25.4% share. This significant share is primarily due to the widespread adoption of energy-efficient motors in heating, ventilation, and air conditioning systems across commercial, residential, and industrial sectors. HVAC systems are crucial for energy management in buildings, and the integration of energy-efficient motors significantly reduces energy consumption and operational costs.

Pumps are another major application segment, utilizing energy-efficient motors to enhance operational efficiency and reduce energy costs in various industries, including water management, chemicals, and oil and gas. The demand for energy-efficient pump solutions continues to grow as industries seek to meet sustainability goals and reduce environmental impact.

Fans and compressors also represent key application areas. Fans equipped with energy-efficient motors are extensively used in commercial building ventilation, industrial processes, and cooling systems. Compressors with energy-efficient motors are critical in refrigeration, air conditioning, and industrial applications, where improved energy efficiency directly translates into cost savings and reduced greenhouse gas emissions.

Refrigeration, material handling, and material processing applications further contribute to the demand for energy-efficient motors. In refrigeration, these motors help reduce electricity usage in cooling systems. In material handling and processing, they enhance the efficiency of operations such as conveyor systems, packaging, and manufacturing processes. Each of these applications leverages the benefits of energy-efficient motors to not only save energy but also improve system reliability and longevity.

By End User

Key Market Segments

By Type

- AC motors

- DC motors

By Power Output Rating

- <1 kW

- 1-2.2 kW

- 2.2-375 kW

- > 375 kW

By efficiency level

- IE1

- IE2

- IE3

- IE4

- IES

By Installation Type

- Open Drip Proof (ODP) Motors

- Totally Enclosed Fan Cooled (TEFC) Motors

By Application

- HVAC

- Pumps

- Fans

- Compressors

- Refrigeration

- Material Handling

- Material Processing

By End User

- Residential

- Commercial

- Industrial

- Automotive

- Agriculture

- Aerospace & Defense

- Others

Drivers

Government Incentives and Subsidies

Many governments have introduced financial incentives to promote the adoption of energy-efficient motors. For example, in the United States, the DOE’s Industrial Efficiency and Decarbonization program provides financial support for upgrading to energy-efficient systems, including motors.

According to the U.S. DOE, energy-efficient motor systems can cut energy use by up to 30%, translating to billions of dollars in savings for U.S. manufacturers. Additionally, tax credits and rebates for purchasing energy-efficient equipment are common in countries like Canada, Germany, and Australia.

According to the International Energy Agency (IEA), the EU’s policy is estimated to save 77 TWh of electricity annually, reducing CO2 emissions by approximately 39 million tonnes. Similarly, in the United States, the Department of Energy (DOE) set minimum efficiency standards for motors used in industrial applications. These regulations, which focus on ensuring compliance with higher performance standards, are accelerating the shift toward energy-efficient motors across key industries.

Environmental Sustainability Goals

Governments and organizations are increasingly prioritizing sustainability as part of their climate action plans. The adoption of energy-efficient motors is crucial for meeting these environmental targets. The United Nations (UN) Sustainable Development Goals (SDGs), especially Goal 7 (Affordable and Clean Energy) and Goal 13 (Climate Action), emphasize the need for industries to reduce their carbon footprints and optimize energy usage.

Energy-efficient motors, which reduce energy consumption and greenhouse gas emissions, are key contributors to these global sustainability targets. According to the U.S. Environmental Protection Agency (EPA), industrial motors account for about 70% of global electricity use in manufacturing. By switching to energy-efficient motor technologies, companies can significantly reduce their energy consumption and support global efforts to combat climate change.

Long-Term Cost Savings and Economic Benefits

As energy prices continue to rise, energy-efficient motors provide businesses with long-term cost savings. According to the International Finance Corporation (IFC), companies in developing economies can save up to 40% on energy costs by upgrading to energy-efficient motors. These savings come not only from reduced energy consumption but also from lower maintenance and longer equipment lifespans.

As energy-efficient motors consume less electricity, businesses can benefit from reduced operational costs over time. Governments support these upgrades through initiatives like the U.S. Department of Energy’s Save Energy Now program, which helps industries improve their energy efficiency while providing financial assistance to mitigate installation costs.

Restraints

High Upfront Investment

Energy-efficient motors, particularly those with higher efficiency ratings such as IE3, IE4, or IES, typically come with a higher price tag than standard motors. The premium price can range anywhere from 20% to 40% higher, depending on the motor’s power rating and efficiency level.

For example, according to the U.S. Department of Energy (DOE), energy-efficient motors may cost up to 30% more than conventional models. While this difference in cost can be recovered over time through energy savings, the initial investment can deter businesses, particularly SMEs, from making the switch to energy-efficient alternatives.

This higher upfront cost can be a major barrier in industries where budget constraints limit the ability to upgrade machinery. For example, the food processing industry, which is energy-intensive, often operates on thin profit margins and may find the initial costs of upgrading to more efficient motors prohibitive. Even with government incentives or rebates, which help offset the cost, some industries may still struggle with financing these upgrades.

Payback Period Concerns

While energy-efficient motors lead to savings over time, the payback period—the amount of time it takes for the savings to cover the initial investment—can be a concern for businesses. For instance, in industrial settings where the motor runs continuously, the payback period for an energy-efficient motor may take several years.

According to the U.S. Department of Energy, the payback period for replacing a standard motor with an energy-efficient model can range between 2 to 4 years, depending on the size of the motor and the energy savings achieved.

However, in some cases, especially for industries operating with older or less energy-efficient equipment, the long payback period may not be acceptable, particularly if the company is undergoing financial challenges or has limited access to capital. Smaller businesses may prefer cheaper, less efficient motors due to the immediate cost savings, even though the long-term energy savings would outweigh the initial investment.

Opportunity

Global Energy Efficiency Regulations

Government regulations requiring energy efficiency improvements in industrial processes are a major driving force for energy-efficient motor adoption. The European Union, for example, has set ambitious targets to reduce carbon emissions by 55% by 2030, compared to 1990 levels, through initiatives like the EcoDesign Directive.

The EU has mandated that motors must meet specific efficiency criteria to reduce energy waste and carbon emissions. These regulations, along with similar standards from the U.S. Department of Energy (DOE) and China’s efforts to improve energy efficiency, create a huge growth opportunity for energy-efficient motors.

According to the International Energy Agency (IEA), policies and regulations targeting motor efficiency can save up to 550 TWh of energy annually globally by 2030, which is equivalent to the electricity consumption of around 170 million households. This significant energy-saving potential is driving manufacturers to upgrade to energy-efficient motors, expanding market demand.

Government Incentives and Subsidies

In addition to regulations, governments are offering subsidies, tax incentives, and grants to encourage industries to invest in energy-efficient equipment, including motors. For example, the U.S. Department of Energy’s Motor Challenge Program offers financial incentives and rebates to businesses that replace older, less-efficient motors with energy-efficient alternatives.

Similarly, countries like India and Japan have introduced financial incentives to drive energy efficiency in industrial sectors. According to the U.S. Department of Energy, replacing an older motor with an energy-efficient model can reduce energy consumption by up to 20%, offering significant long-term savings.

For instance, in 2022 alone, the DOE’s programs helped businesses save an estimated $2 billion in energy costs. These financial benefits encourage companies to prioritize energy-efficient motor installations, further accelerating market growth.

Industry-Specific Incentives

Several industries are seeing more targeted government incentives that directly impact energy-efficient motor adoption. For instance, the manufacturing sector, one of the largest consumers of motors, benefits from various national and international policies promoting the use of energy-efficient equipment.

In 2023, the Indian government announced a scheme under the Perform, Achieve and Trade (PAT) initiative, which offers rewards for energy efficiency improvements across industries, including motors. Similarly, the European Union’s Horizon Europe program, which funds green technology projects, is supporting the development of next-generation energy-efficient motors. These initiatives create a favorable environment for companies to adopt energy-efficient technologies and help them meet stricter energy consumption regulations.

Trends

Integration of IoT for Enhanced Performance Monitoring

The integration of IoT technologies in energy-efficient motors is revolutionizing how industries monitor and manage motor performance. IoT sensors enable remote monitoring of motors, allowing companies to track performance metrics like energy consumption, temperature, vibration, and motor speed.

For example, smart motors can alert users about impending failures, enabling predictive maintenance, which helps to avoid unexpected downtime. According to the U.S. Department of Energy (DOE), the IoT-based predictive maintenance approach can reduce energy waste by up to 20% and increase motor lifespan by up to 30%, offering significant cost savings in the long run.

Advancements in Motor Control Technologies

Another key trend driving the energy-efficient motor market is the advancement in motor control technologies, particularly Variable Frequency Drives (VFDs). VFDs allow the motor’s speed to be adjusted according to the specific requirements of the application, thereby reducing energy consumption during partial load operations.

According to the U.S. Environmental Protection Agency (EPA), VFDs can reduce energy consumption by up to 60% in certain applications, such as pumps, fans, and compressors. These technologies, when used with energy-efficient motors, help maximize energy savings and enhance operational efficiency.

Sustainability and Compliance with Environmental Regulations

A significant factor driving the demand for energy-efficient motors is the growing emphasis on sustainability and compliance with environmental regulations. Governments worldwide are imposing stricter energy efficiency standards, and industries are under pressure to reduce energy consumption and minimize environmental impact.

In Europe, the Ecodesign Directive requires all motors above 0.75 kW to comply with specific efficiency levels (IE2, IE3, IE4). The European Commission estimates that its regulations could save up to 64 TWh of energy by 2030, reducing CO2 emissions by 17 million tons annually. Similarly, in the U.S., the DOE’s updated efficiency standards for electric motors, which were implemented in 2020, are expected to save approximately $2 billion annually in energy costs.

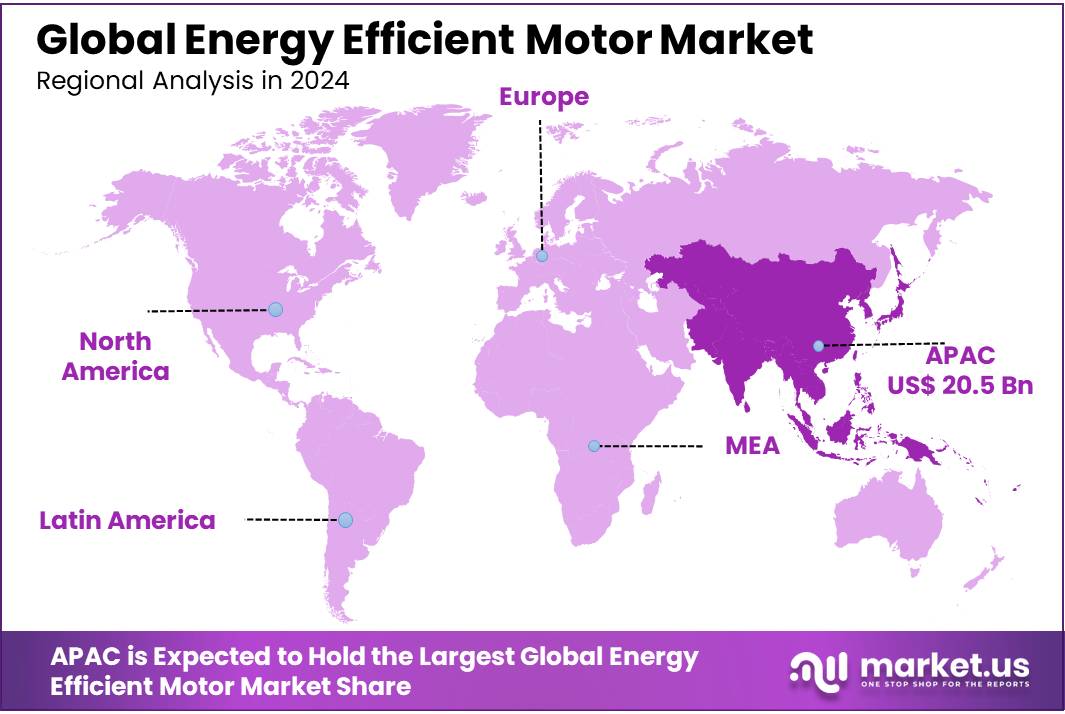

Regional Analysis

The Asia Pacific (APAC) region dominates the global energy-efficient motor market, accounting for 46.4% of the market share, valued at approximately USD 20.5 billion. The dominance of this region is driven by rapid industrialization, increasing demand for energy-efficient solutions, and robust manufacturing sectors in countries like China, India, and Japan.

APAC is expected to maintain its lead due to stringent government regulations promoting energy efficiency and the growing trend of automation across industries such as automotive, manufacturing, and HVAC.

In North America, the market is expected to witness steady growth due to the rising adoption of green technologies and sustainability initiatives across industrial sectors. The U.S. is the largest contributor to the region, with an increasing focus on reducing carbon emissions and energy consumption. By 2028, the North American market is projected to reach approximately USD 8.6 billion.

Europe also plays a significant role in the energy-efficient motor market, supported by the European Union’s strict energy efficiency policies and regulations. The market in this region is driven by high demand for energy-efficient products in sectors like transportation and industrial manufacturing. Europe’s market is expected to grow at a compound annual growth rate (CAGR) of 5.7% over the forecast period.

The Middle East & Africa (MEA) market is showing promising growth, driven by rising industrial activities and government initiatives in countries like Saudi Arabia and the UAE. However, the market is relatively smaller compared to other regions, representing a moderate share of around 7% globally.

In Latin America, countries like Brazil and Mexico are embracing energy-efficient motors as part of their energy conservation strategies, leading to steady market growth. The market is expected to see a CAGR of 4.5% in the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Energy Efficient Motor Market is highly competitive, with several key players leading the industry by offering innovative solutions. ABB, a global leader in power and automation technologies, is one of the most prominent players, providing a wide range of energy-efficient motors across various industries.

General Electric (GE), with its extensive industrial portfolio, focuses on delivering advanced motor technologies that cater to energy conservation in commercial and industrial applications. Siemens and Schneider Electric also stand out for their commitment to sustainability and energy efficiency, providing state-of-the-art motors integrated with intelligent controls for optimized performance.

Other notable players in the market include Bosch Rexroth AG, Honeywell International, and Johnson Controls, all of which leverage their technological expertise to develop motors that align with the global trend of reducing energy consumption.

Nidec Corporation, through its subsidiary Nidec Motor Corporation, is another significant contributor, offering energy-efficient motors that cater to a variety of sectors including HVAC, automotive, and industrial automation.

The market is further strengthened by companies like Marathon Electric, Kirloskar Electric Company, WEG, and Regal Beloit Corporation, each with a strong regional presence and robust product portfolios. These companies are focusing on innovation and expanding their global footprint to capitalize on the growing demand for energy-efficient technologies. With increasing demand from industries across North America, Europe, and APAC, these key players continue to push the boundaries of energy efficiency in motor technology.

Top Key Players

- ABB

- AG Regal

- Bosch Rexrot

- Bosch Rexroth AG

- Crompton

- Crompton Greaves

- GE

- General Electric

- Havells

- Honeywell International, Inc.

- Johnson Controls Inc.

- Johnson Electric

- Kirloskar

- Kirloskar Electric Company Ltd.

- Marathon Electric

- Microchip Technology, Inc.

- Mitsubishi

- Nidec Corporation

- Nidec Motor Corporation

- Regal Beloit Corporation

- Rockwell Automation

- Schneider Electric

- Siemens

- Toshiba

- WEG

Recent Developments

In 2023 ABB has seen strong growth in its motor business, with a reported revenue of approximately USD 10.2 billion from its motors and drives division in 2023, contributing significantly to its overall electrification and automation revenues.

In 2023, Regal Beloit reported USD 6.5 billion in total revenue, with a significant portion of this coming from their motor and drive systems segment, which has been growing steadily due to increasing demand for energy-efficient products.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 44.2 Bn |

| Forecast Revenue (2033) | USD 91.9 Bn |

| CAGR (2024-2033) | 7.6% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (AC motors, DC motors), By Power Output Rating (<1 kW, 1-2.2 kW, 2.2-375 kW, > 375 kW), By efficiency level (IE1, IE2, IE3, IE4, IES), By Installation Type (Open Drip Proof (ODP) Motors, Totally Enclosed Fan Cooled (TEFC) Motors), By Application (HVAC, Pumps, Fans, Compressors, Refrigeration, Material Handling, Material Processing), By End User (Residential, Commercial, Industrial, Automotive, Agriculture, Aerospace and Defense, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ABB, AG Regal, Bosch Rexrot, Bosch Rexroth AG, Crompton, Crompton Greaves, GE, General Electric, Havells, Honeywell International, Inc., Johnson Controls Inc., Johnson Electric, Kirloskar, Kirloskar Electric Company Ltd., Marathon Electric, Microchip Technology, Inc., Mitsubishi, Nidec Corporation, Nidec Motor Corporation, Regal Beloit Corporation, Rockwell Automation, Schneider Electric, Siemens, Toshiba, WEG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |